Published August 12th 2025

3-min read

Inflation Data Offers Modest Relief

The latest CPI release was broadly in line with expectations. Headline MoM inflation matched consensus at 0.2%, holding at 2.7% YoY, while core rose 0.3% MoM and 3.1% YoY, fractionally softer than forecast. Gasoline prices fell 9.5% YoY, providing some headline relief. Pre-release chatter had leaned toward upside risk, so the in-line outcome steadied sentiment and supported a dovish market tone. FOMC pricing shifted toward more than two cuts by year end, with September odds edging higher.

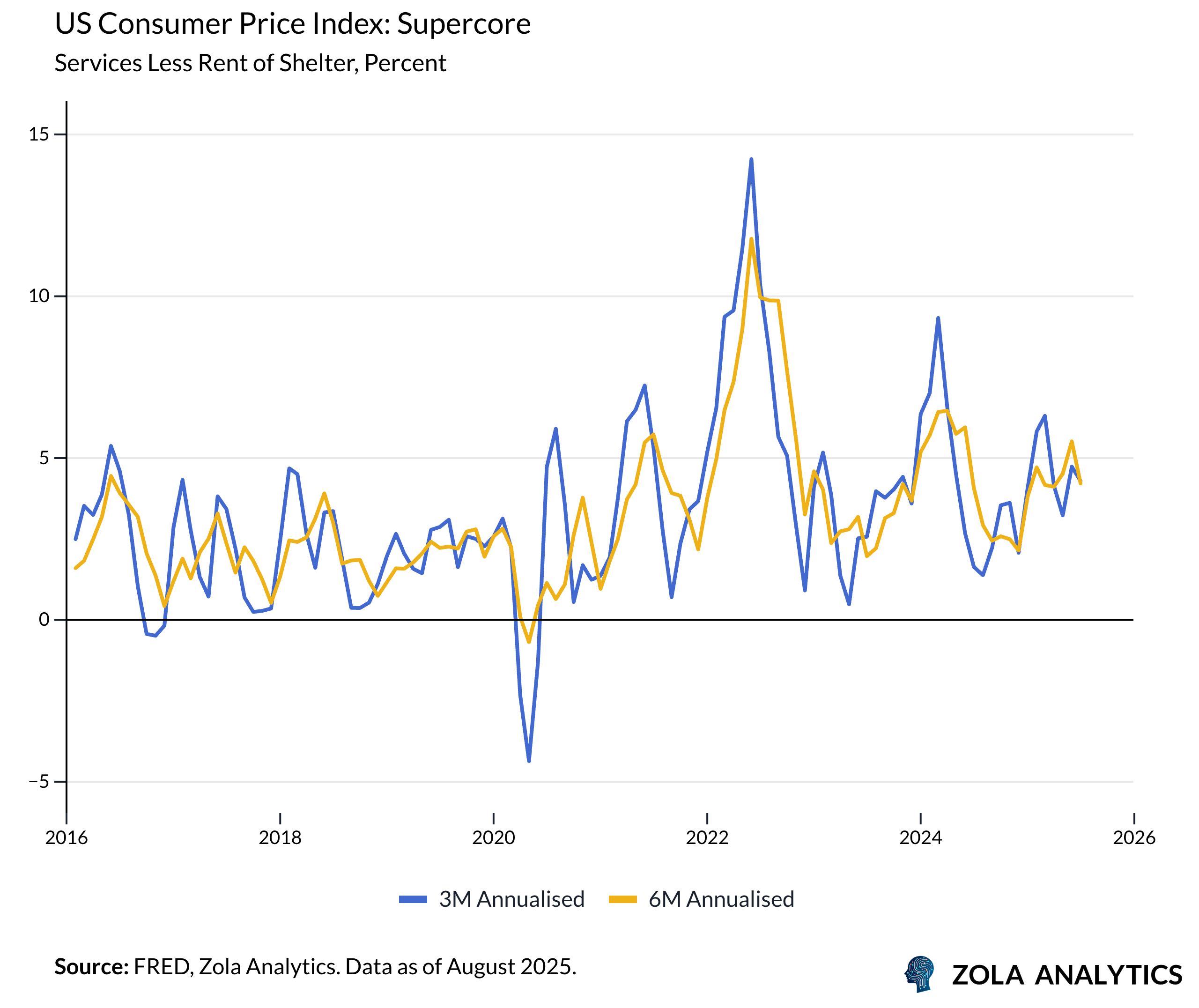

Supercore inflation advanced 0.5% MoM, the second-strongest since early 2024, although the 3M annualised rate remains contained. This stability keeps near-term Fed expectations anchored.

Goods Remain Benign For Now

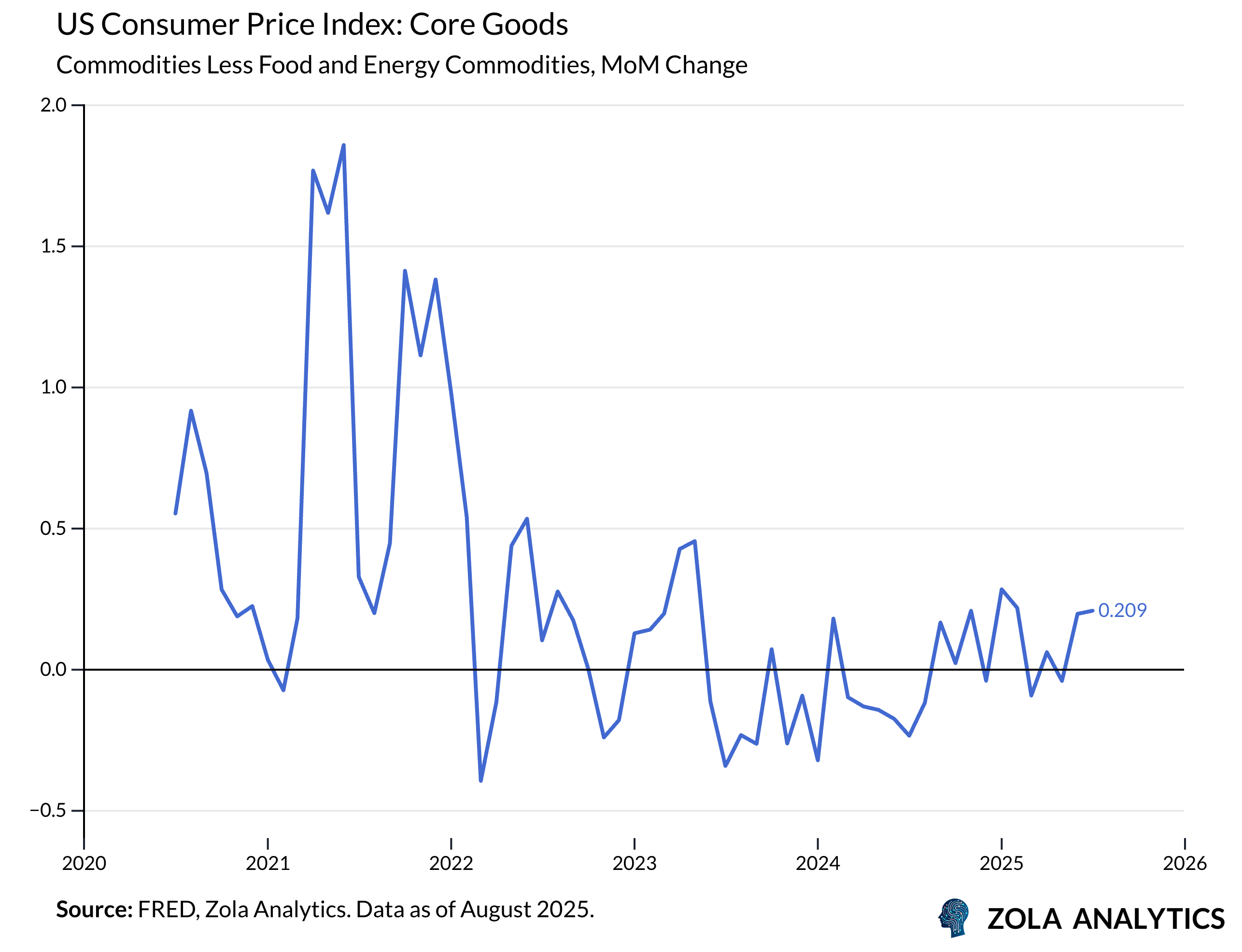

Core goods rose 0.2% MoM versus expectations near 0.4%. Apparel gained 0.1%, home furnishings increased 0.7% after 1.0% in June, new autos were flat, and used cars climbed 0.5%.

Softer momentum fits the inventory cycle: manufacturers and wholesalers restocked in Q1 to front-run higher duties, while retailers did less, delaying pass-through until back-end inventories clear. These cycles often run for two quarters, and we are near the end of that window. Holiday restocking is underway, so clearing prices for goods arriving in Q4 may begin to reflect higher tariff rates. Pass-through tends to come in phases: margins compress first, then prices adjust as inventories turn and competitors move together. The pace will depend on demand and logistics, yet the direction points to a firmer goods pulse into Q4.

Services Still Carry The Load

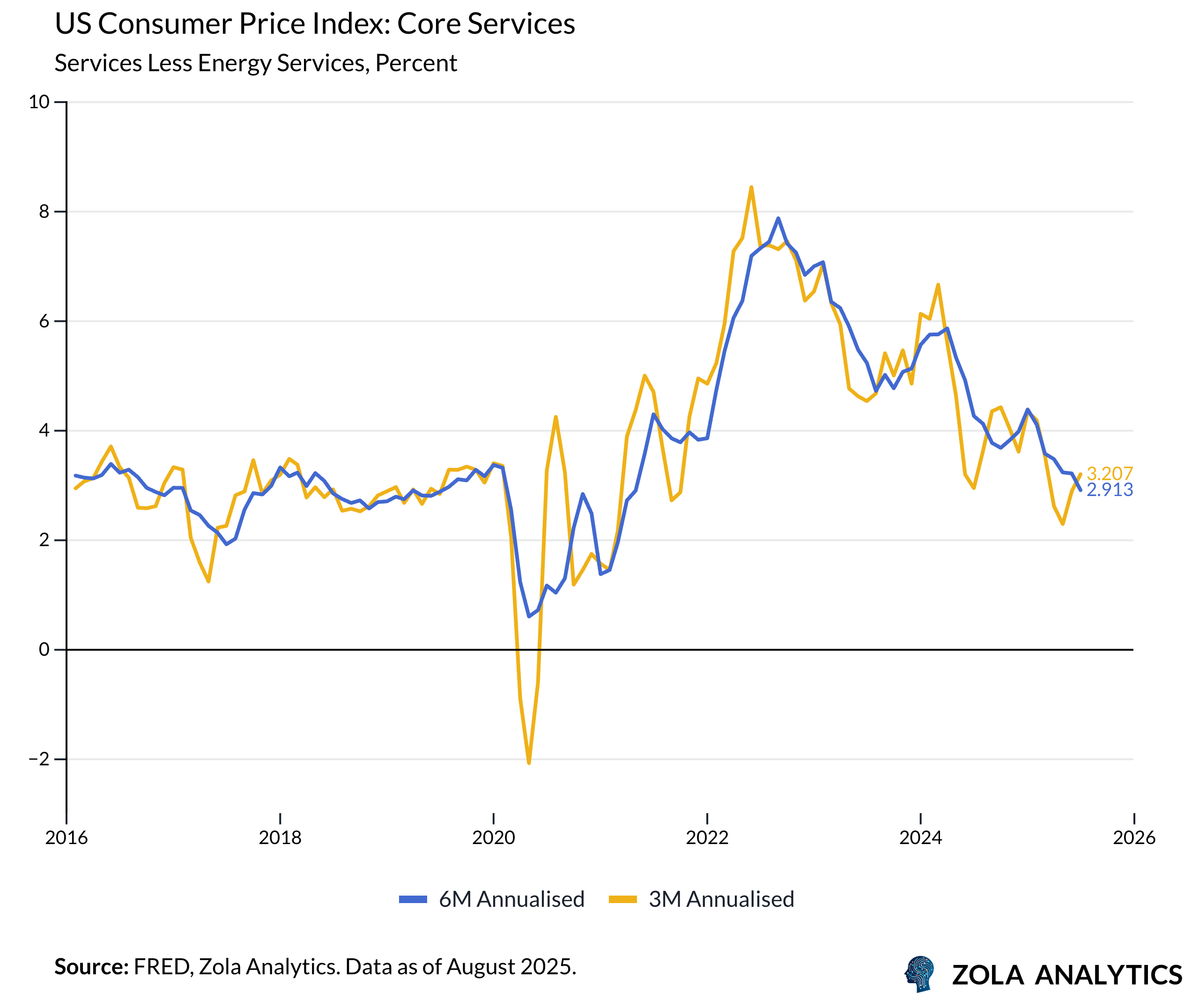

Core services rose 0.4% MoM, with medical care up 0.7% and shelter steady at 0.2%. Shelter remains the largest single driver of services inflation.

The trend remains mixed with 3M annualised core rate at 3.2% while the 6M rate eased to 2.9%, the lowest since early 2021. Slower wage growth and reduced job turnover limit scope for a broad services reacceleration, but the sector’s persistence still warrants attention.

Fed Path Toward 3.5%

Goods disinflation in July gives the Fed breathing room, even as tariff pressures build into Q4. Markets read the mix as dovish and now expect cuts at the remaining FOMC meetings this year, taking the Fed funds rate toward 3.5%.

Powell’s calculus weighs limited tariff pass-through so far against softening in parts of the labor market and the risk of a goods rebound as holiday inventories arrive. A late-year tariff bump may not halt easing, though it could slow the cadence. For now the bias points lower, with an uneven path shaped by the next rounds of labor, PPI, and spending data.