Published June 3rd 2025

Taco Trade or Tariff Trap? Markets Struggle with Reflexive Volatility

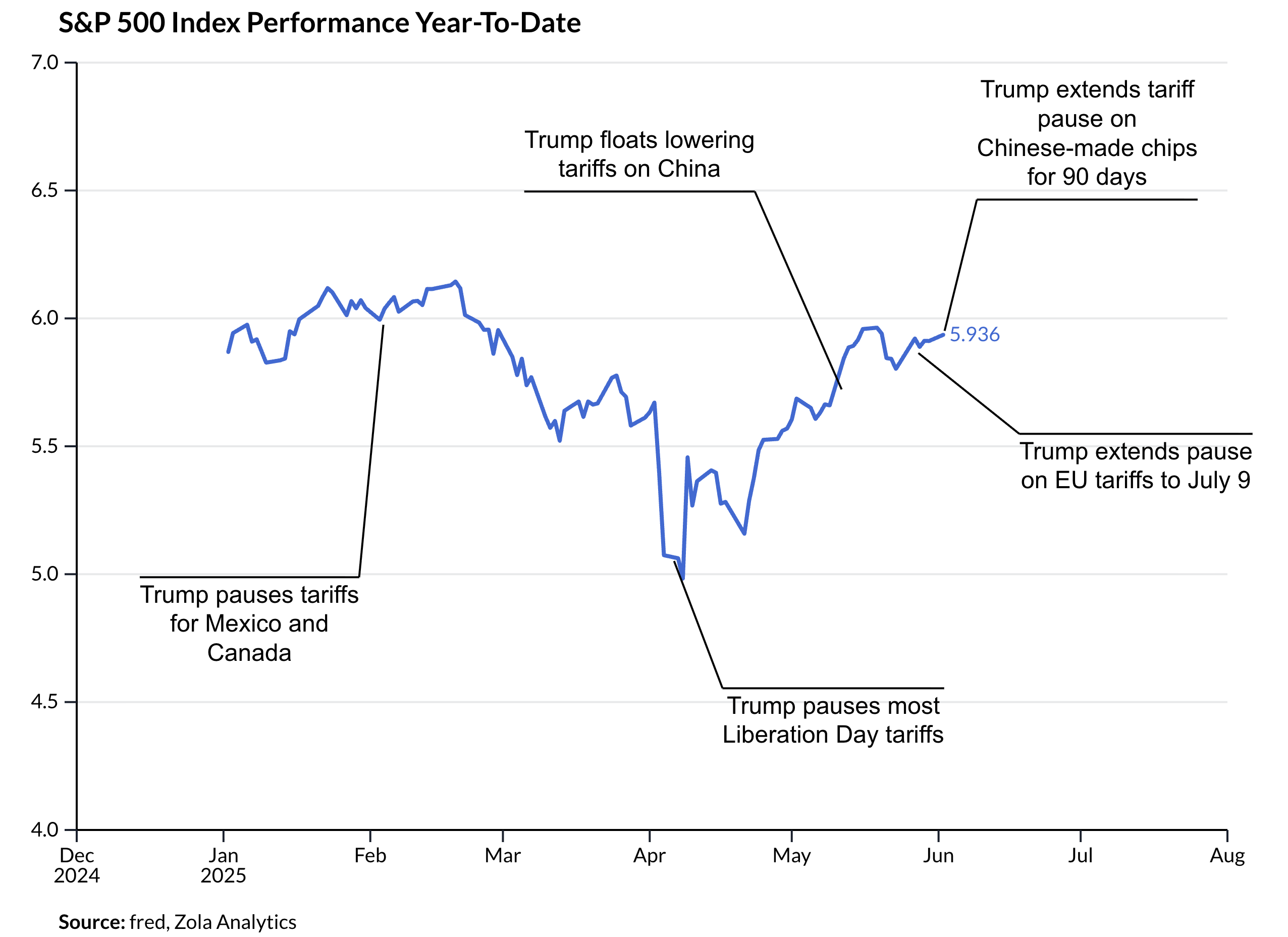

The phenomenon dubbed the “Taco trade” – shorthand for Trump Always Chickens Out – encapsulates a key feature of recent US market dynamics: the frequent threat of disruptive policy followed by tactical retreat. This cycle of shock and partial reversal has created a reflexive environment where investors respond not to fundamentals, but to headline-driven probabilities.

Yet this rhythm appears increasingly fragile. As the administration becomes more attuned to how markets interpret its moves, its behaviour evolves. Strategic retreats may no longer come predictably. A growing willingness to follow through – especially with baseline tariffs – suggests a shift from theatre to entrenched policy. The 10% tariff, for instance, now appears foundational, supported by political incentives rather than economic logic. It enables ideological coherence across fiscal hawks and populist rhetoric, while offering the illusion of fiscal discipline through customs revenue.

Market Psychology and Risk Premia

This environment breeds two problems for investors. First, it embeds policy uncertainty into valuations. Equity markets, especially in the US, rely not just on economic data but on the predictability of governance. When that predictability is lost, the risk premium demanded by investors increases – even if earnings and growth expectations remain stable.

Second, the volatility itself becomes self-defeating. Every cycle of sell-off and rebound contributes to a higher bar for participation. Fast money may play the swings, but longer-term capital – pensions, insurers, endowments – becomes hesitant. Even a short-lived shock, if frequent enough, erodes confidence in the underlying trend.

The Structural Drag

Beyond sentiment, structural headwinds from tariff policy are beginning to weigh more visibly on the economy. While a full-scale trade war has been avoided, the persistence of elevated tariffs acts as a stealth tax on business: discouraging investment, slowing inventory turnover, and compressing margins. Even firms able to pass on higher costs are seeing volumes erode, as real incomes remain pressured and demand softens.

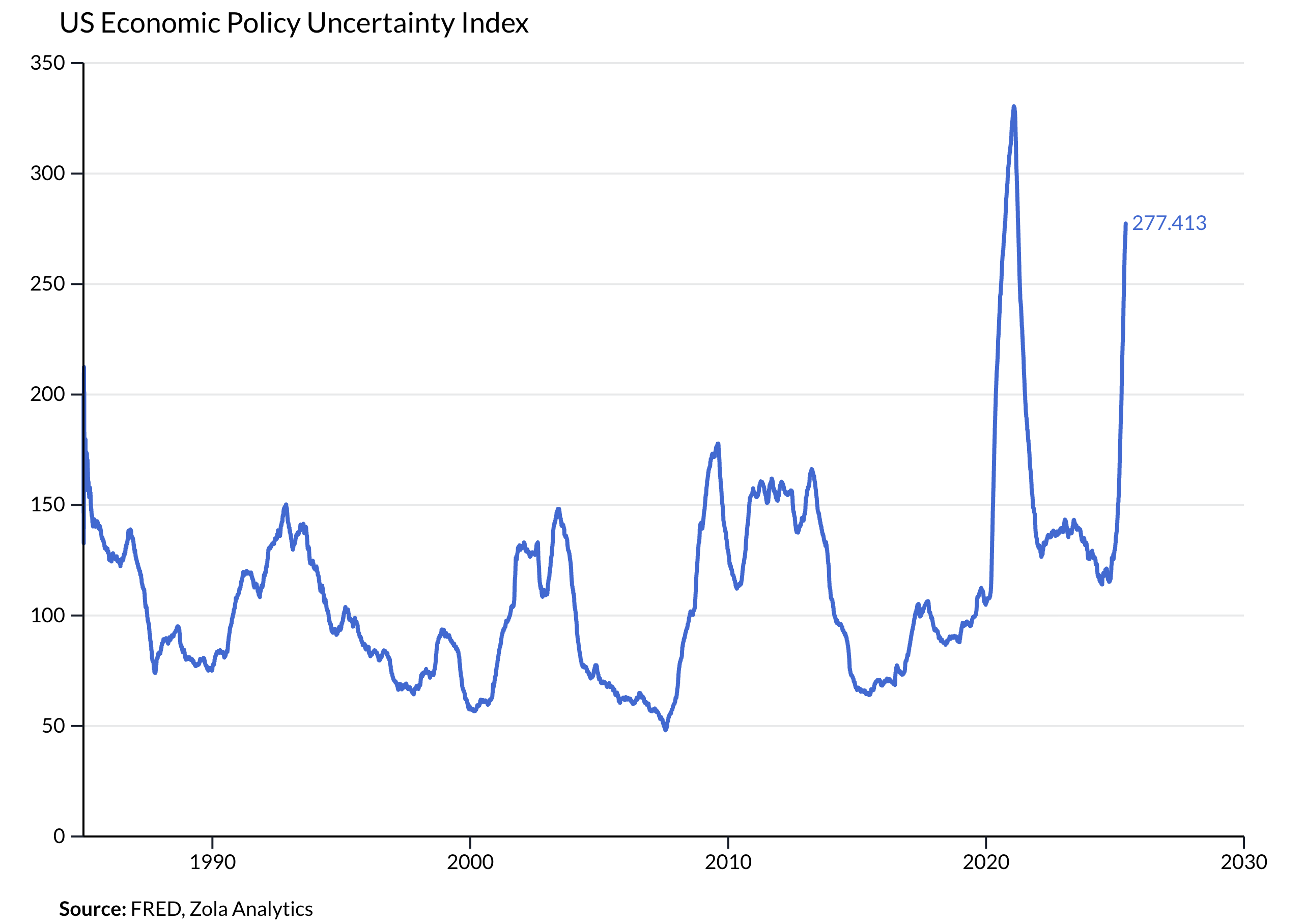

This is happening in an environment of heightened policy ambiguity. The U.S. Economic Policy Uncertainty Index has remained elevated compared to pre-pandemic norms, reflecting a broader breakdown in clarity around fiscal, trade, and regulatory direction. When firms can’t reliably model the policy outlook, they defer hiring, capex, and long-term planning – all of which depress trend growth.

Compounding the drag are restrictive immigration policies and a fading fiscal impulse. Labour supply constraints now risk becoming semi-permanent, limiting expansion potential just as global conditions worsen. The result isn’t crisis, but “grey stagnation”: chronic underperformance relative to potential, driven more by self-inflicted frictions than cyclical weakness.

The Global Dimension

The US also risks losing its asymmetric appeal. For much of the post-COVID cycle, American assets outperformed on the basis of stronger growth, tech dominance, and policy credibility. That appeal is now in question. Rebalancing is underway not through coordinated global policy, but via diminished US leadership. European and Asian economies, under pressure from external shocks, are beginning to stimulate more actively – potentially closing the growth gap from below.

Conclusion: Rangebound Risk

Markets may continue to find technical support in global liquidity, especially as other central banks pivot dovishly. But the US story now lacks the clear macro tailwinds that once made it dominant. Investors are likely to face a rangebound environment – no crash, but no breakout. Volatility will remain elevated, not as a signal of opportunity, but as a cost of engagement.

In this environment, prudence trumps conviction. Equity exposure should favour resilience – sectors with pricing power and global diversification – while fixed income may benefit from a reassessment of global duration, particularly in economies less encumbered by self-inflicted shocks.

The Taco trade might still be on the menu – but increasingly, it leaves a sour aftertaste.