Published May 28th 2026

6 minute read

A Confidence Game

In November 1990, during her final session of Prime Minister’s Questions, Margaret Thatcher faced a familiar heckle. Dennis Skinner shouted that her next job would be governor of the Bank of England. She paused, smiled, and replied: “What a good idea.” Only a generation ago, central bank independence was still a radical notion. In response to Skinner, Thatcher went on to criticise the idea of a European central bank, arguing that it would be “accountable to no one, least of all national Parliaments.”

In the decades that followed, governments across the world ceded monetary power to technocrats. Independence and credibility became the creed of modern central banking.

This week’s Zola Chartbook traces that evolution: how the need for independence arose from the crises of the 1970s, how its intellectual foundations hardened into orthodoxy, and how a series of shocks, from the financial crisis to the pandemic, has brought its contradictions to the surface.

Old Consensus

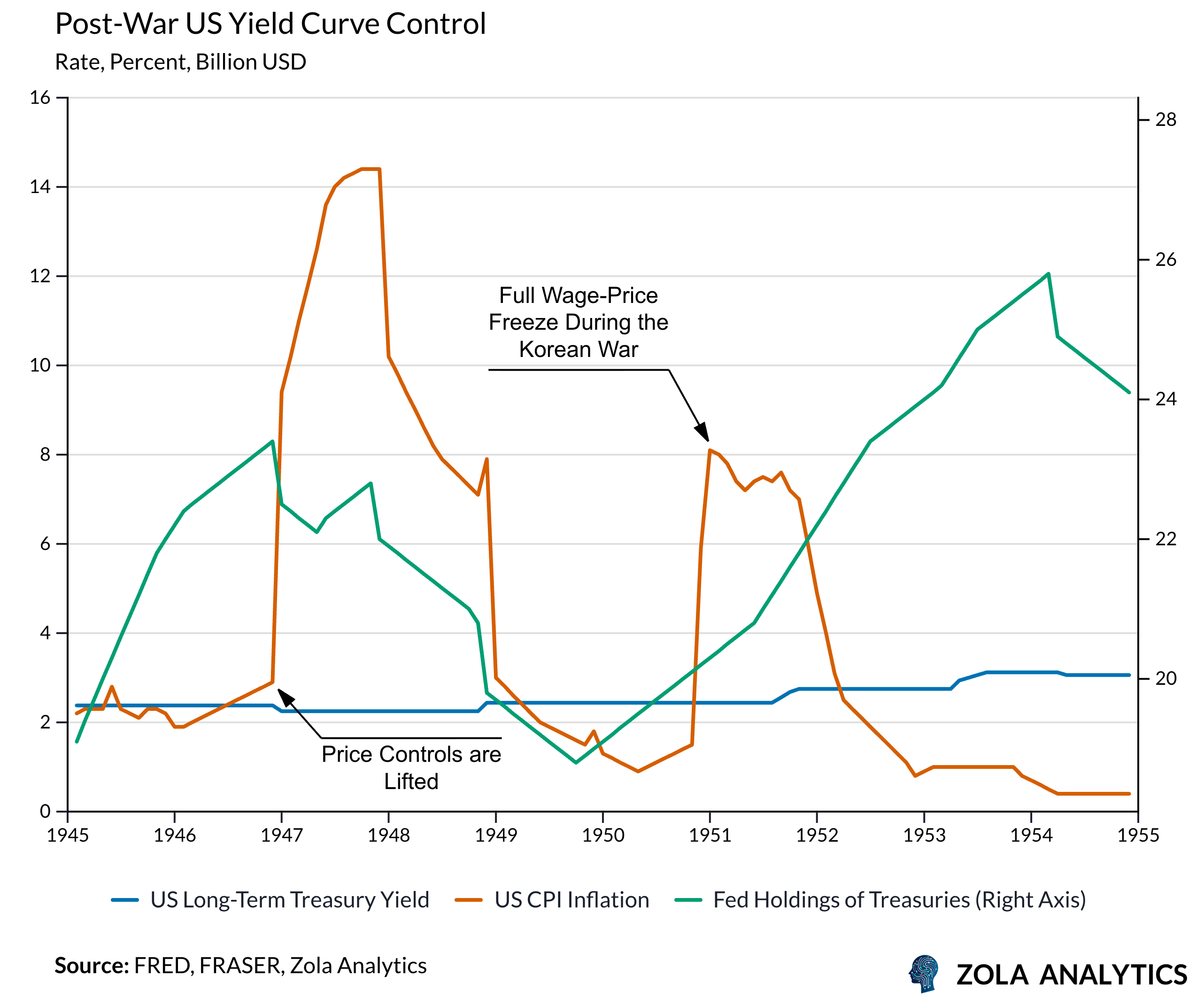

In the aftermath of the Second World War, with wartime debts towering, fiscal needs dictated monetary policy. In the US, the Federal Reserve maintained fixed long-term interest rates to facilitate Treasury borrowing, a policy of yield-curve control.

By 1951, the Fed’s reluctance to keep monetising government debt led to the Treasury–Fed Accord. Operational independence for the Fed was fully established.

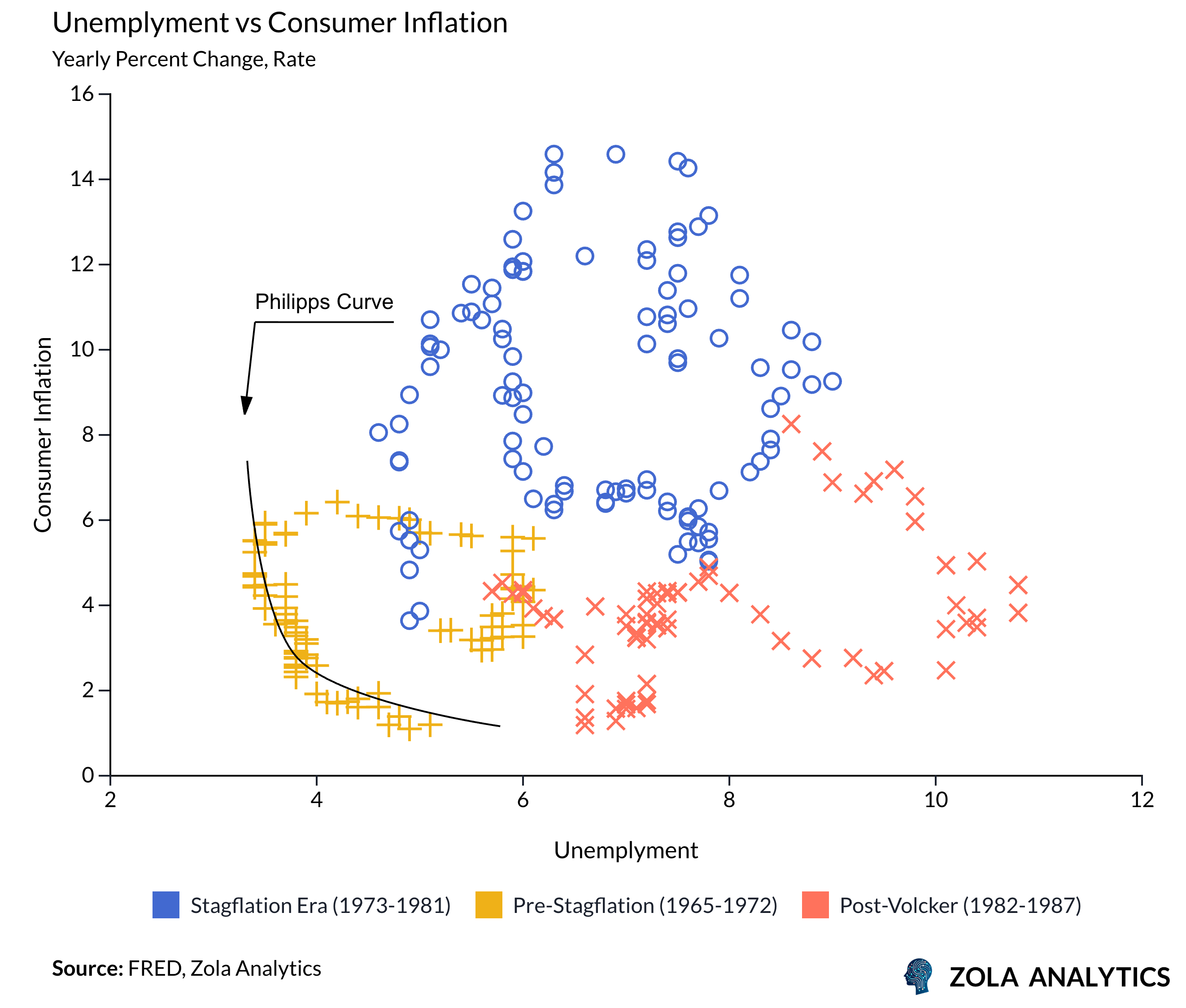

In the postwar period, the prevailing view in the economics profession was that inflation and unemployment could be balanced through policy intervention. The Phillips Curve seemed to promise policymakers a menu of choices between inflation and jobs. That logic guided post-war macroeconomic policy.

The 1970s shattered this assumption. Economists such as Milton Friedman and Edmund Phelps had argued that attempts to maintain unemployment below its natural rate would eventually lead to accelerating inflation once expectations adjusted. The simultaneous rise of inflation and unemployment seemed to vindicate their warnings.

The Nixon years were a turning point in this story. Determined to avoid a recession ahead of the 1972 election, President Richard Nixon repeatedly pressured Federal Reserve Chair Arthur Burns to keep monetary policy loose, even as inflation began to rise. Transcripts later revealed Nixon urging Burns to “kick the economy in the rear” and to think about “the election, not the textbook.” Under political pressure, the Fed expanded credit and held rates down, contributing to the inflationary surge that followed.

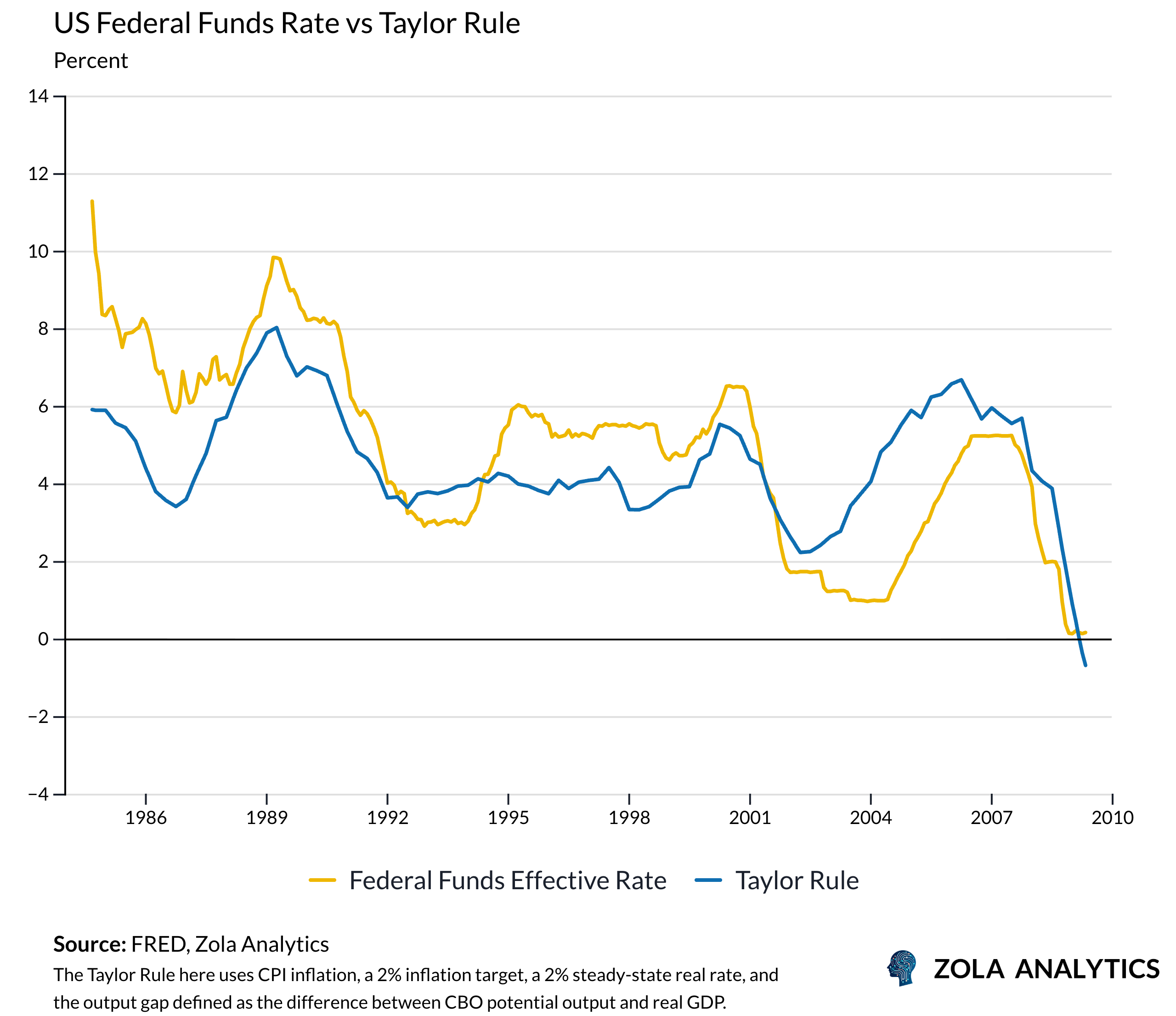

When Paul Volcker became Chair of the Federal Reserve in 1979, he was determined to break the back of inflation. Between 1979 and 1983, the Federal Reserve sharply tightened policy to re-anchor expectations. The disinflation that followed came at the cost of a deep recession, but it re-established monetary control and demonstrated the potential value of an institution able to operate independently of short-term political pressures. In retrospect, economists see the recession’s severity as the cost of lost credibility. With greater trust in the Fed’s commitment to price stability, inflation might have fallen with less pain. The lesson was clear: monetary policy needed insulation from politics.

Other countries followed a similar path. The Bank of England, nationalised in 1946 and largely subordinate to the Treasury for decades, was granted operational independence in 1997. The change allowed it to set interest rates to meet a government-specified inflation target. The reform completed the transition from fiscal dominance to delegated monetary authority. The cure for inflation would become the doctrine of independence.

The Credibility Revolution

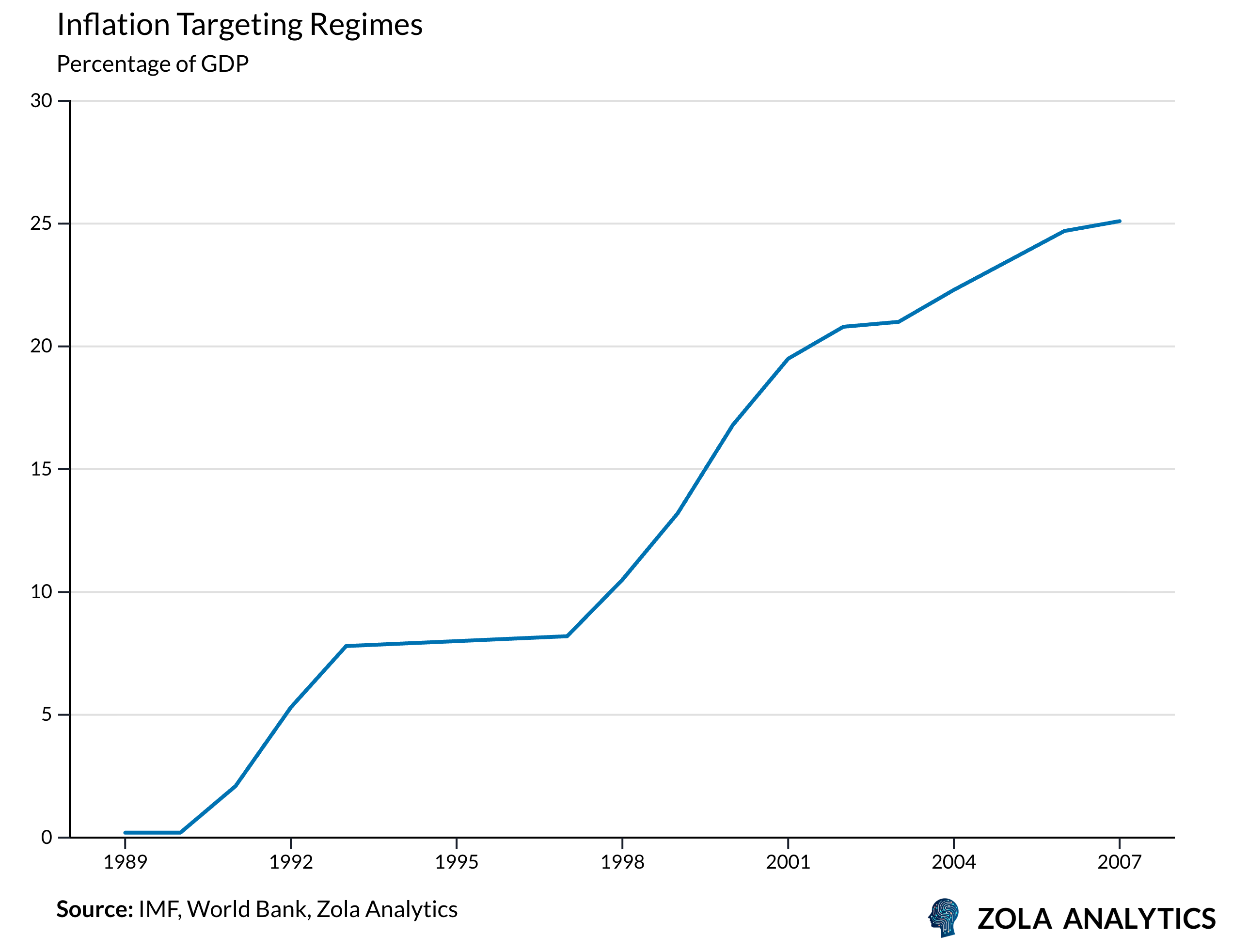

That doctrine soon found theoretical blessing in the models of the 1990s, as New Keynesian frameworks argued that stabilising inflation could also stabilise output under certain conditions. It promised that rules and credibility could deliver both price and output stability. This idea supported the growing trend toward formal inflation-targeting regimes. New Zealand adopted the approach in 1990, followed by the United Kingdom and many others.

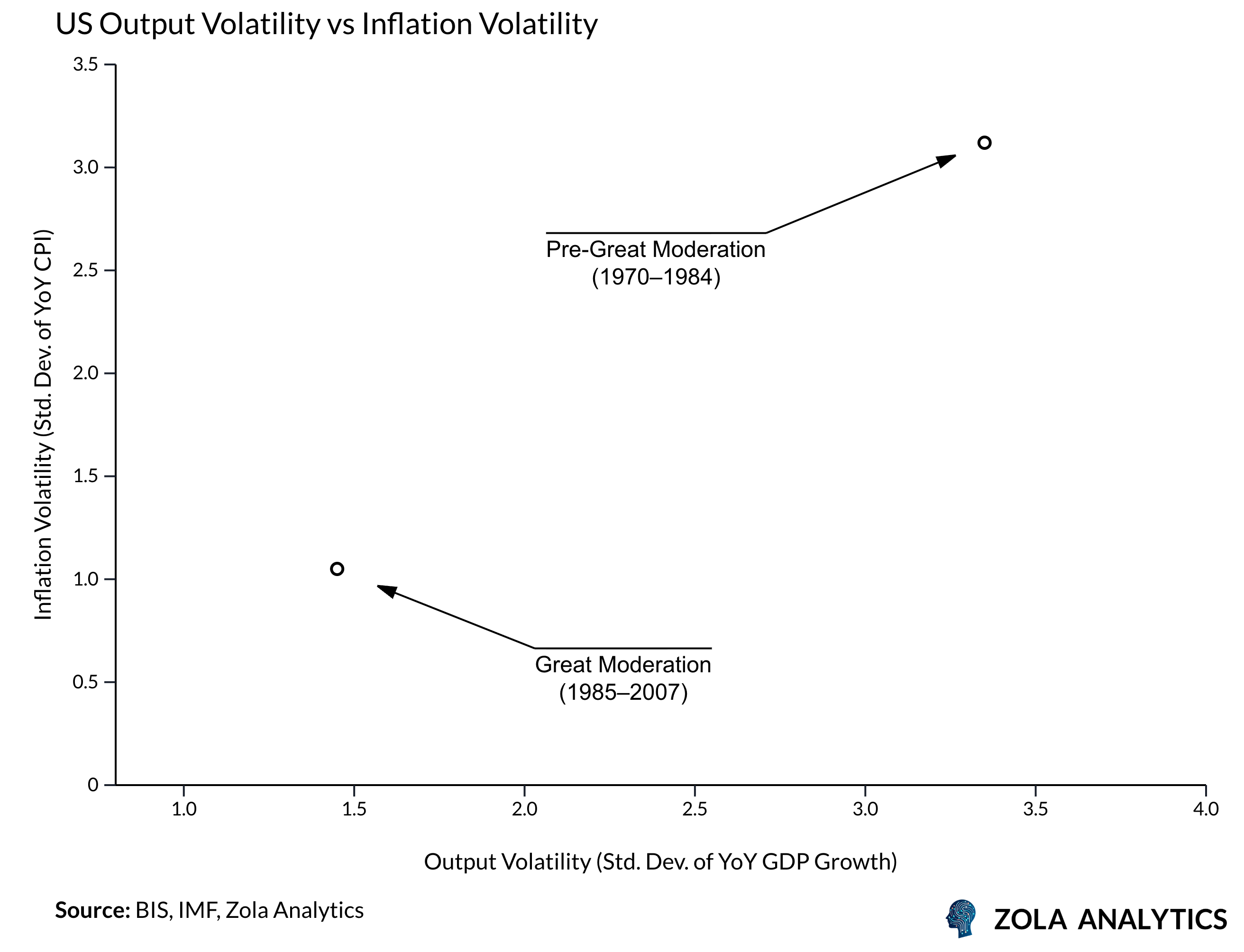

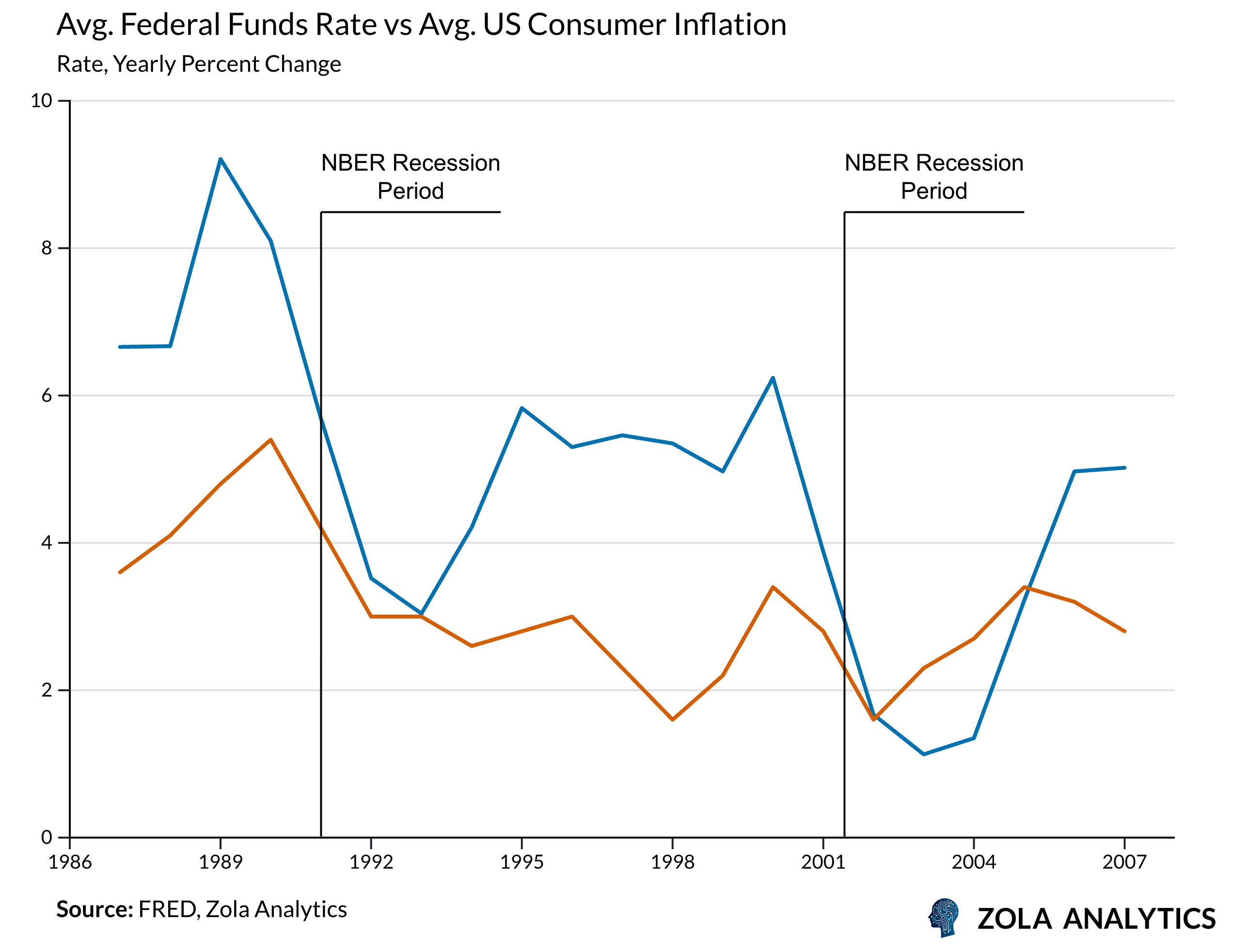

The subsequent period of macroeconomic stability, often termed the Great Moderation, appeared to validate this theory. From the mid-1980s to the mid-2000s, advanced economies experienced low inflation, steady output growth, and relatively mild recessions.

During this period, central banks became increasingly rule-oriented and transparent. Policy credibility came to depend on consistency and predictability rather than discretionary flexibility. The belief that monetary policy could deliver both nominal and real stability through systematic management became widely accepted.

However, the framework’s effectiveness relied on specific conditions. Low and stable inflation coincided with structural changes in the global economy that contained cost pressures. Globalisation, technological advancement, and weaker collective bargaining power reduced the risk of wage-price spirals.

By the mid-2000s, the apparent alignment between price and output stability had encouraged confidence in the capacity of independent central banks to maintain equilibrium. Yet that confidence rested on supply conditions that could never be guaranteed.

Neutral No More

Alan Greenspan’s tenure as Chair of the Federal Reserve came to symbolise the perceived success of the independent central bank model. His management of policy during several episodes of market stress reinforced the view that credible and pre-emptive monetary adjustments could stabilise both inflation and output.

By the early 2000s, this confidence had become self-reinforcing. Financial innovation, subdued inflation, and moderate business cycles supported the impression that monetary policy could manage macroeconomic outcomes without major costs.

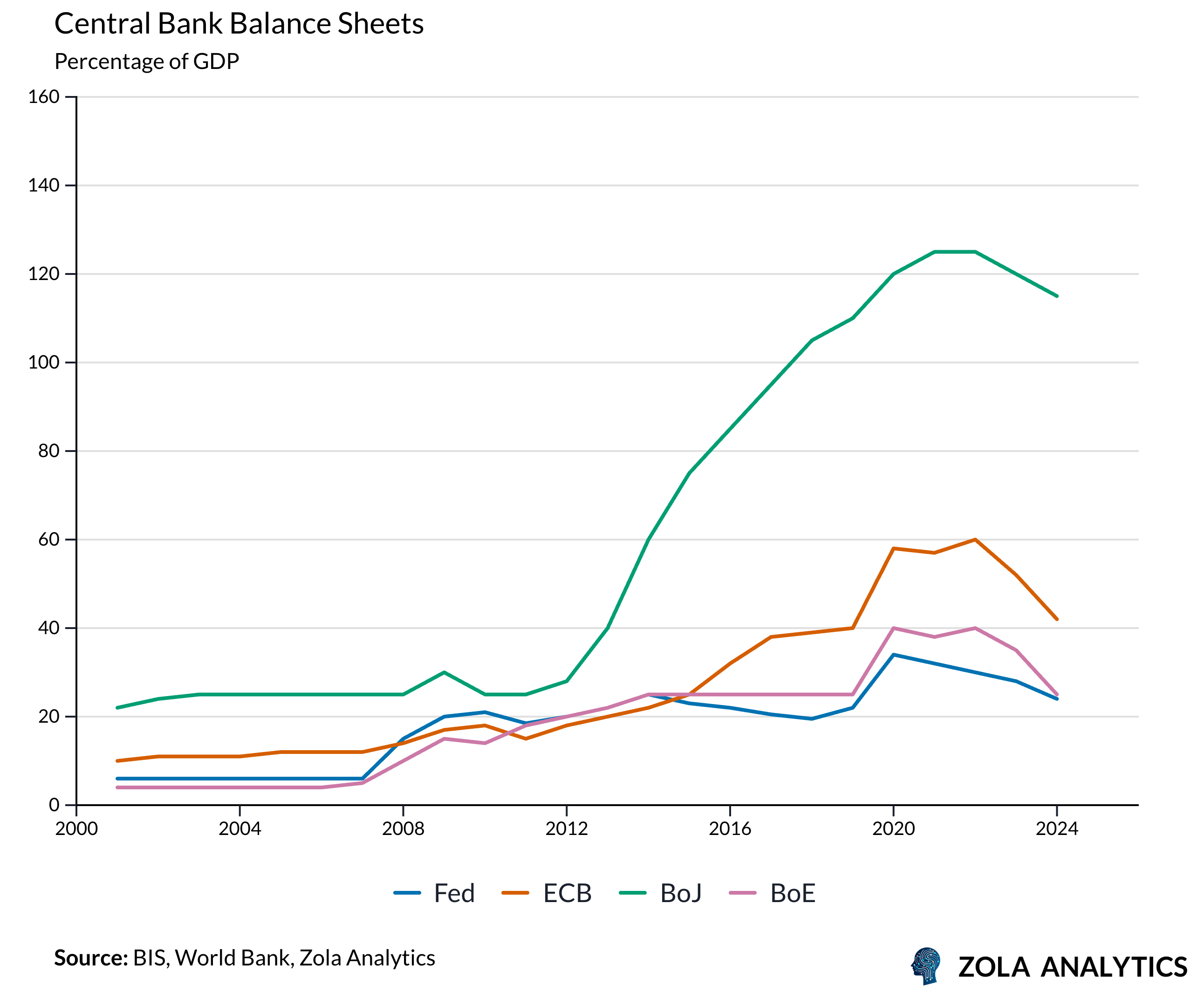

The global financial crisis of 2008 revealed the limitations of this view. As policy rates reached the lower bound, central banks adopted unconventional measures such as quantitative easing and forward guidance to restore market functioning and prevent deflation.

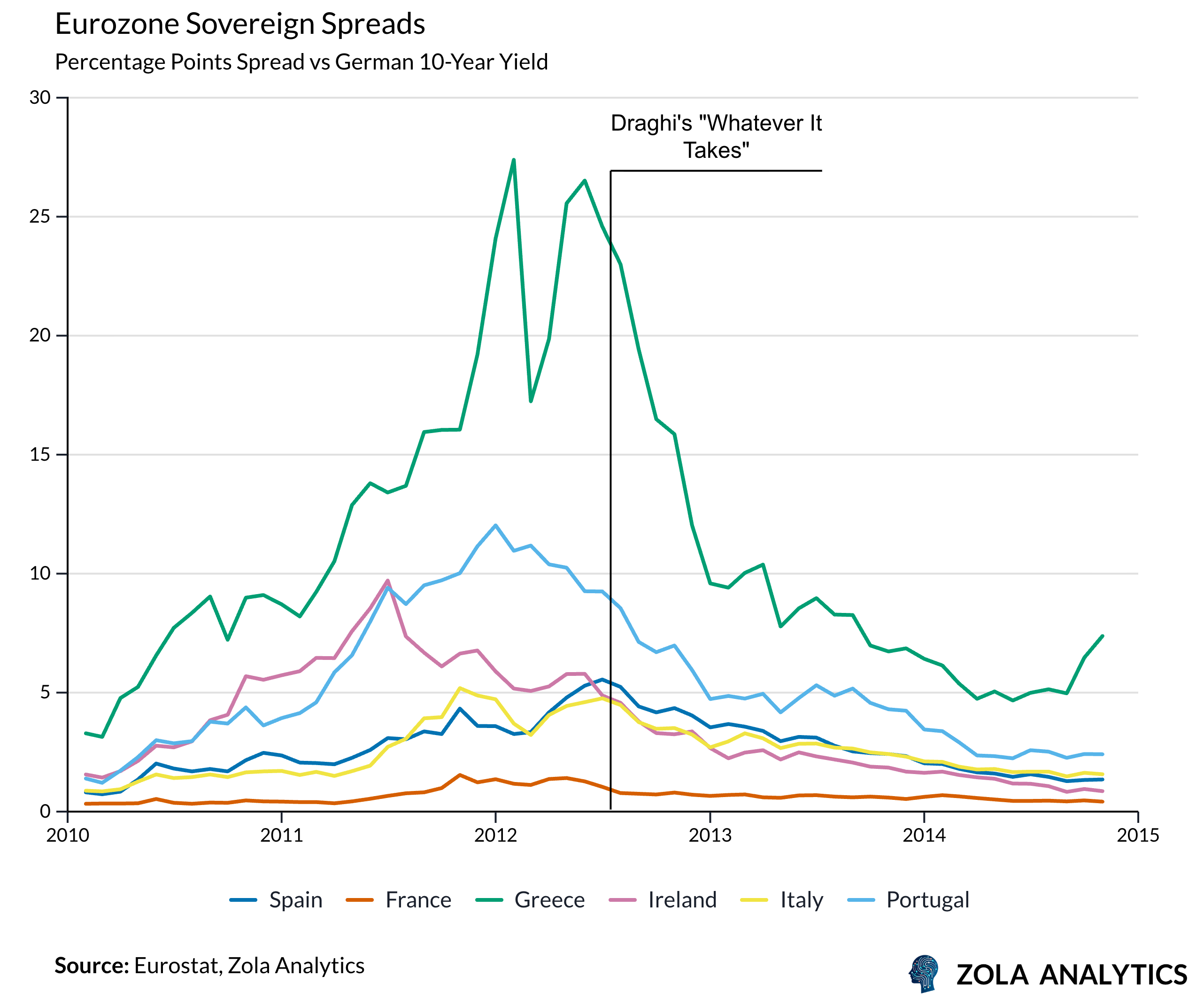

The European experience demonstrated the political dimension of this shift. The structure of the euro area, a monetary union without fiscal integration, required the European Central Bank to take actions with significant distributional effects. Supporting particular sovereign bond markets influenced financing conditions across member states.

By intervening in credit and sovereign markets, central banks extended their remit beyond aggregate demand management. Central banks are now involved in inherently political activities:

Sovereign debt management

The distribution of credit

Climate policy through the greening of collateral frameworks and prudential rules.

Neutrality, once the essence of independence, is now hard to sustain.

The Return of Trade-Offs

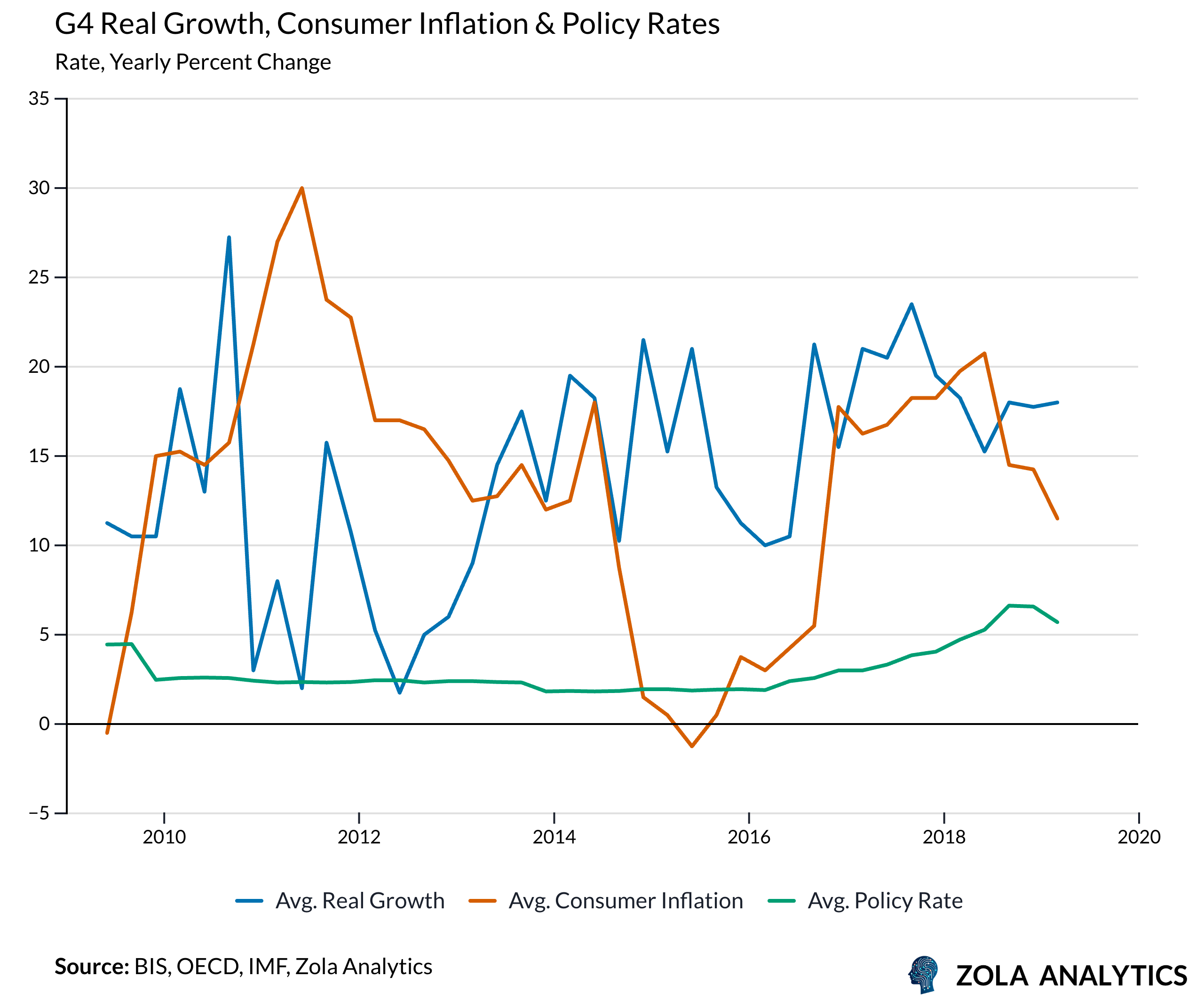

The post-crisis environment was characterised by persistently low growth and inflation. Despite low policy rates and large-scale asset purchases, price pressures remained subdued. Central banks faced diminishing returns from monetary policy, which had become the main instrument of macroeconomic management in the absence of sustained fiscal support.

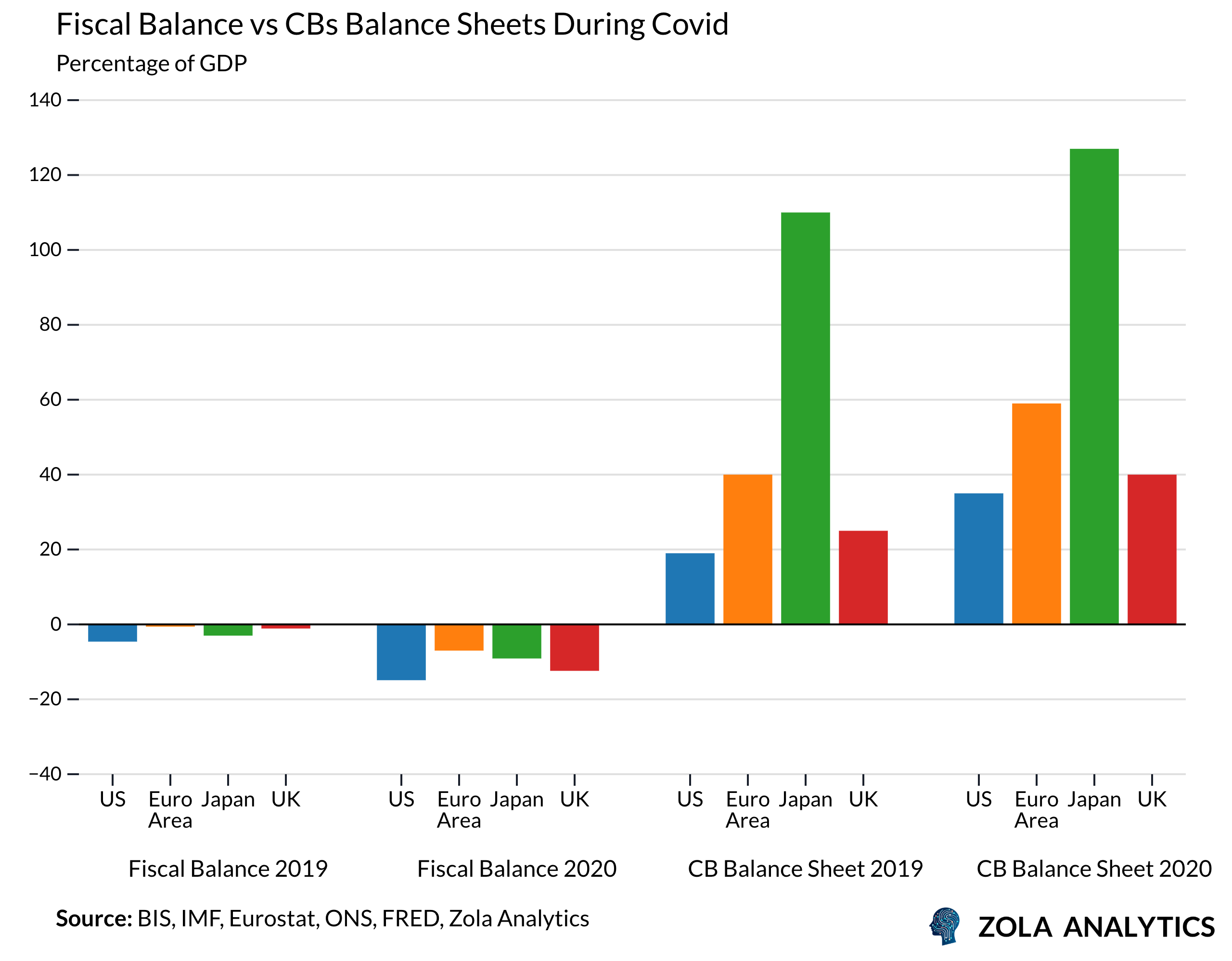

The COVID-19 pandemic intensified these challenges. The initial contraction in output was met by coordinated monetary and fiscal action. Central banks expanded their balance sheets again, while governments introduced large-scale fiscal support. The separation between fiscal and monetary policy temporarily disappeared.

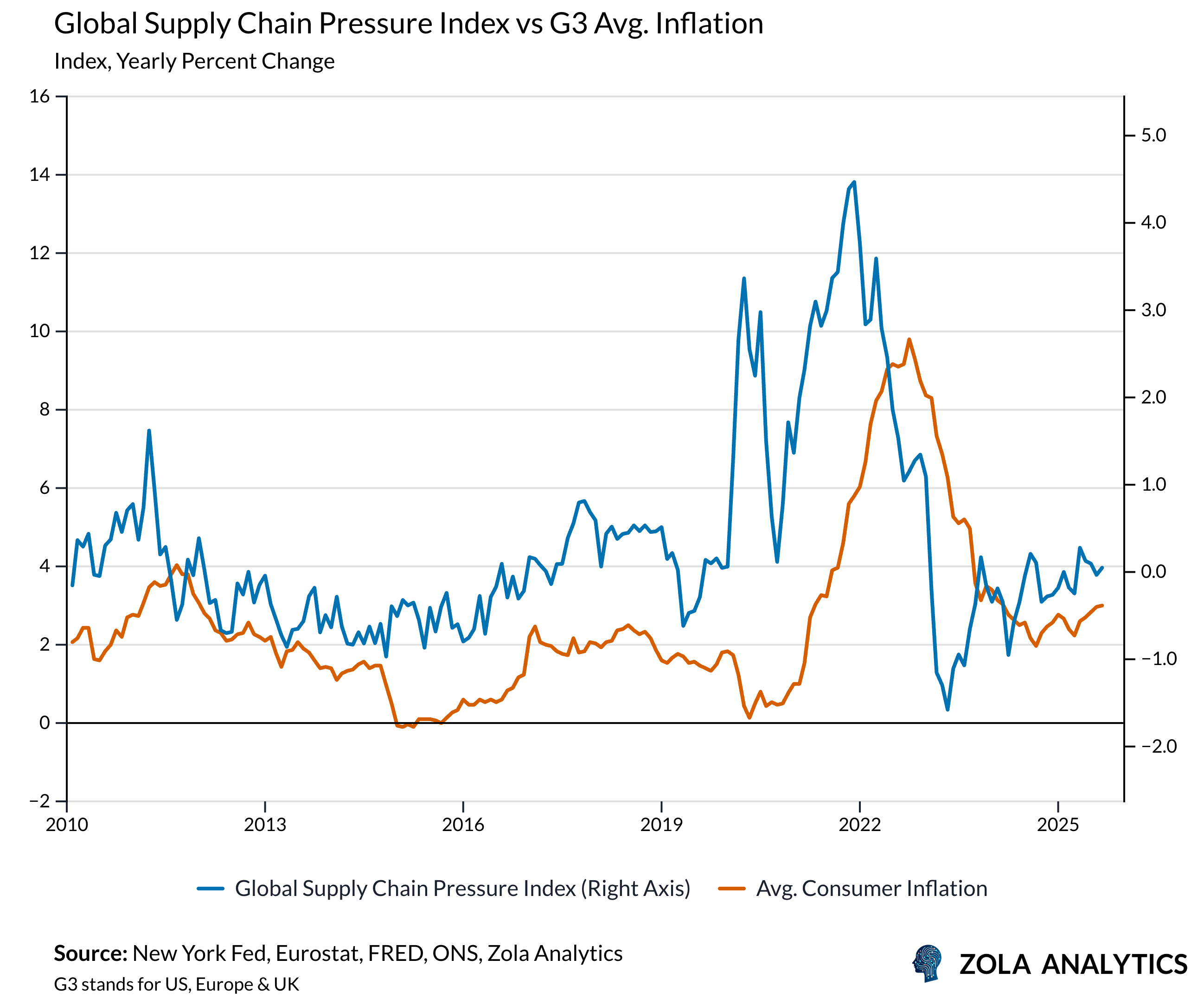

As economies reopened, supply constraints emerged, including disrupted production, labour shortages, and energy price shocks. These conditions generated inflation primarily from the supply side.

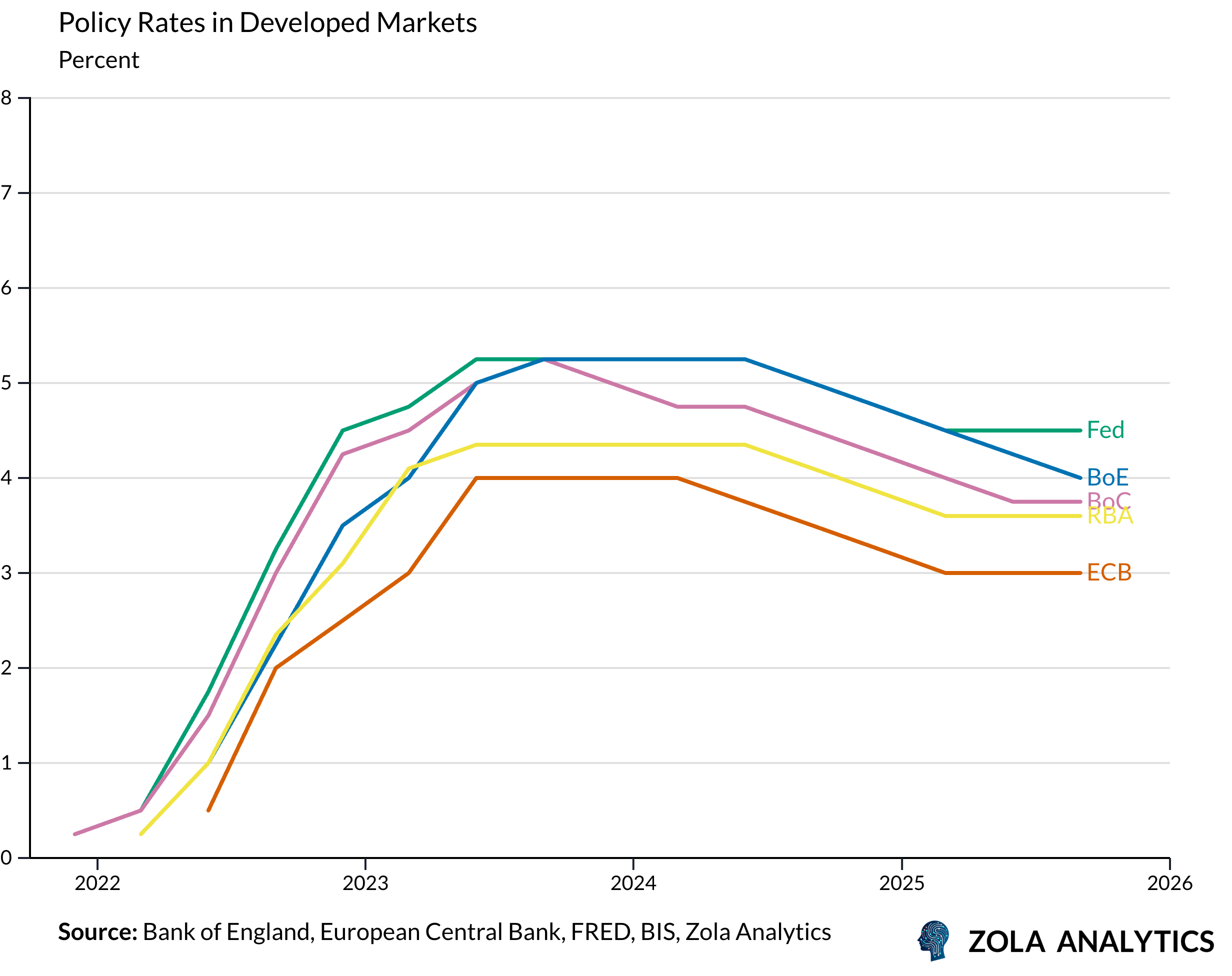

Central banks then faced renewed trade-offs. Tightening policy to contain inflation risked slowing recovery, while maintaining accommodation threatened credibility. The subsequent rate increases from 2021 onwards constituted the most rapid and synchronised tightening cycle in several decades.

Higher rates could not clear ports or reopen factories, yet they remained the only tool available to keep inflation expectations anchored. The result was a renewed emphasis on credibility over growth. This adjustment reintroduced a political dimension, as central banks were criticised both for reacting too late and for tightening too much once they acted.

A Brave New World

The world is now far less forgiving to central banks than it was in the era of the Great Moderation. Supply disruptions, fiscal expansion, and geopolitical fragmentation have replaced the calm of global integration. Managing inflation today means confronting real shocks, not just adjusting expectations.

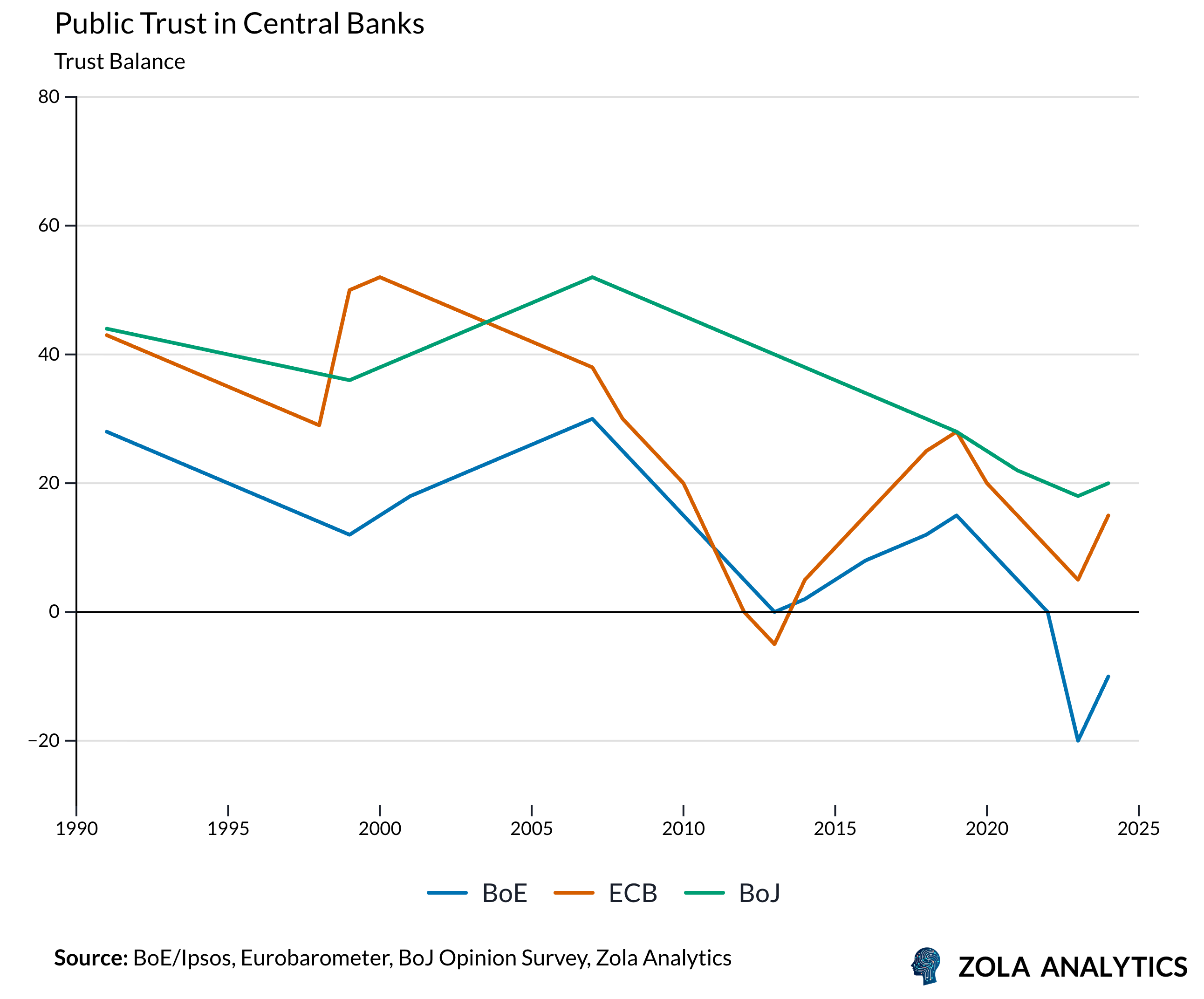

Unconventional tools, such as quantitative easing, forward guidance, and vast balance sheets, have blurred the line between technical management and distributional choice. Their visible effects on wealth and markets have eroded public confidence.

Central banks remain powerful, but their authority now rests on public trust, not distance from politics. Formal independence survives, yet legitimacy depends on openness and accountability. Thatcher’s 1990 warning about unelected authority still resonates: independence once protected monetary stability; now it must earn it anew.

Sign up to receive the Zola Global Macro Chartbook every week: https://www.zolaanalytics.com/insights?signUp