Published July 28th 2025

4-min read

Fed Up: Powell Is Navigating A Political Minefield

Market drama comes in many flavours—surprise inflation spikes, geopolitical flare-ups, earnings disasters—but few match the spectacle of a sitting US President brandishing a 'draft letter' threatening to sack his Fed Chair.

The showdown between President Trump and Chair Powell isn't just a political soap opera, it's a major macro risk event. With signs the business cycle is waking up from a two-year nap and Trump's tariff deadline looming on August 1st, we have a volatile cocktail of political uncertainty and cyclical jitters for the market to digest, just as most in the City are heading off for their summer holidays.

Banana Republicans

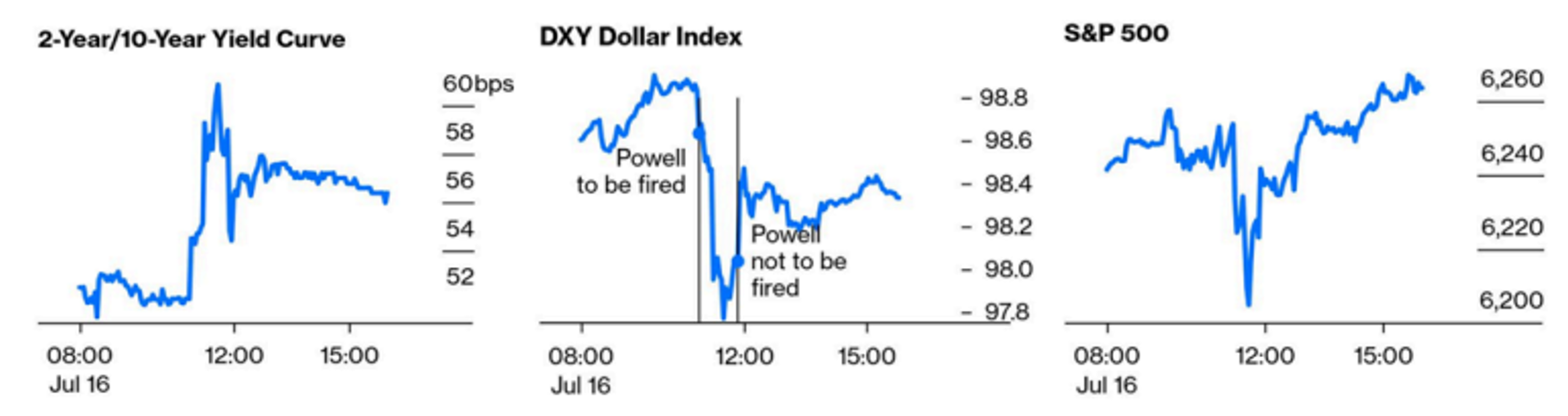

Trump’s campaign to bend the Fed to his will shows no signs of cooling. Friday’s hard-hat moment said it all, with Trump’s threats to fire Powell now as routine as his tariff tantrums. The endgame is clear: whether Powell gets the axe now or walks away next May, Trump plans to install a loyalist who will slash rates on command.

But here’s the kicker—even if Trump gets his wish, it’s likely to backfire. Undermining Fed independence doesn’t lower borrowing costs in the long run; it raises them as markets price in policy chaos. We already got a preview of things to come. When Powell firing rumours briefly surfaced, bonds sold off hard, the dollar cratered, and stocks tanked before Trump walked it back.

Recent research by Thomas Drechsel (2024) exploring decades of presidential meddling with the Fed, shows that politically-driven rate cuts ignite persistent inflation with no meaningful growth to show for it.

The Nixon-Burns fiasco of 1971–72 serves as a case study. Facing re-election pressures, Nixon met with Fed Chair Arthur Burns an unprecedented 34 times in just six months (the normal pace is around six times per year). The result of all that aggressive easing? Inflation surged over 8% without any real GDP payoff—setting the stage for a decade of high inflation.

When presidents lean on the Fed inflation expectations spike and the economy gets all the pain with none of the gain.

Powell Holds The Line

The latest data doesn’t give the Fed a compelling reason to cut. Beneath the surface lies a credibility trap that makes holding rates the only logical move.

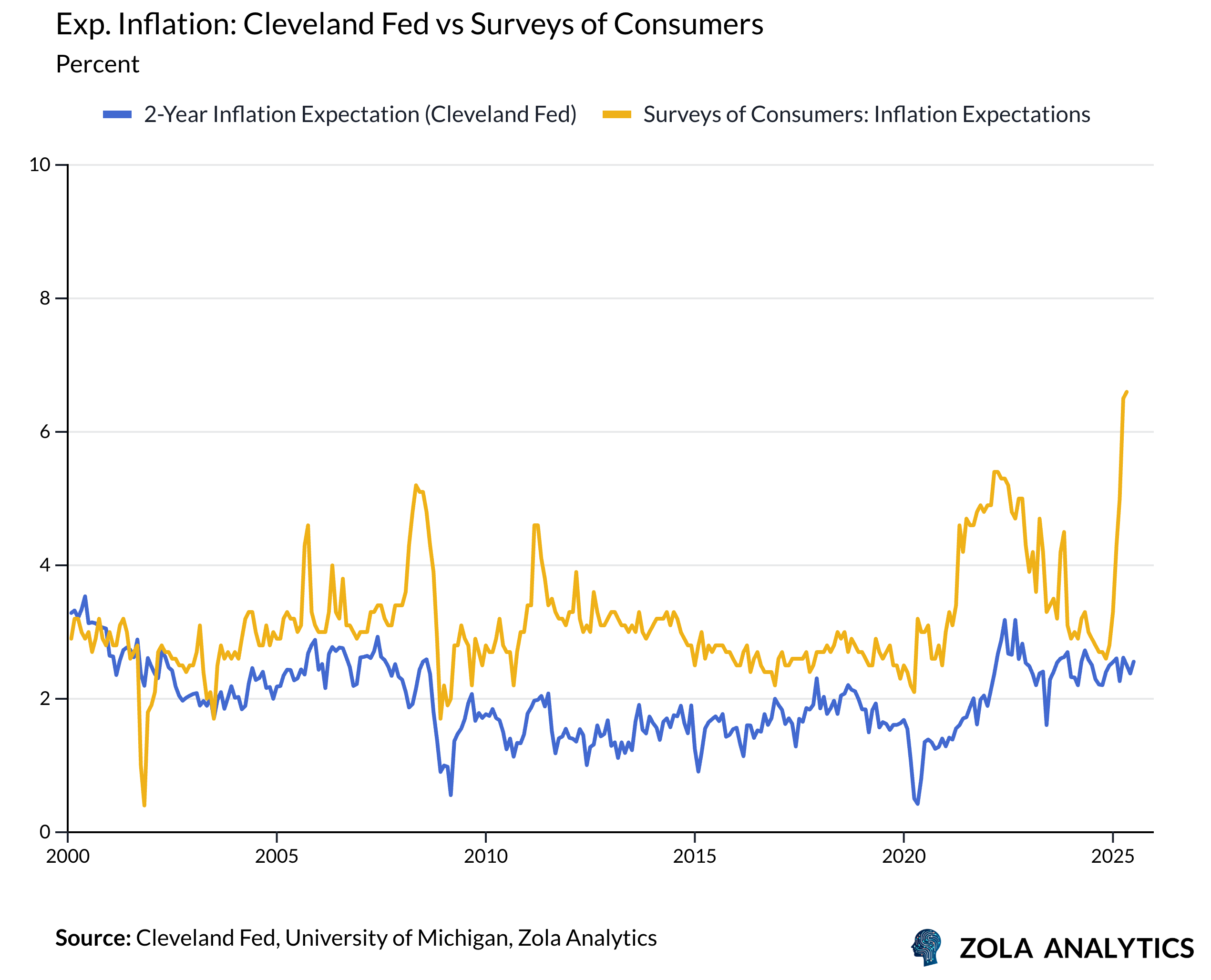

Headline inflation sits at a tame 2.7%, but consumers feel the squeeze once you factor in mortgages and credit card rates, as this NBER working paper shows. That perception gap matters politically. Even if the hard data looks benign, real wages remain about 4% below pre-pandemic trends, so households still feel squeezed.

The real risk? Expectations. Whilst market measures of inflation expectations remain calm, surveys of consumers show lingering anxiety. Cutting too soon risks undoing the hard fought battle to keep expectations under control following COVID.

Despite dissents from Trump-appointed governors Bowman and Waller, the FOMC’s policy centre is holding firm. With tariffs trickling into prices and unemployment edging down, the Fed can credibly signal it has the luxury to wait. Cuts will likely come later this year, once policy uncertainty has fed through into investment.

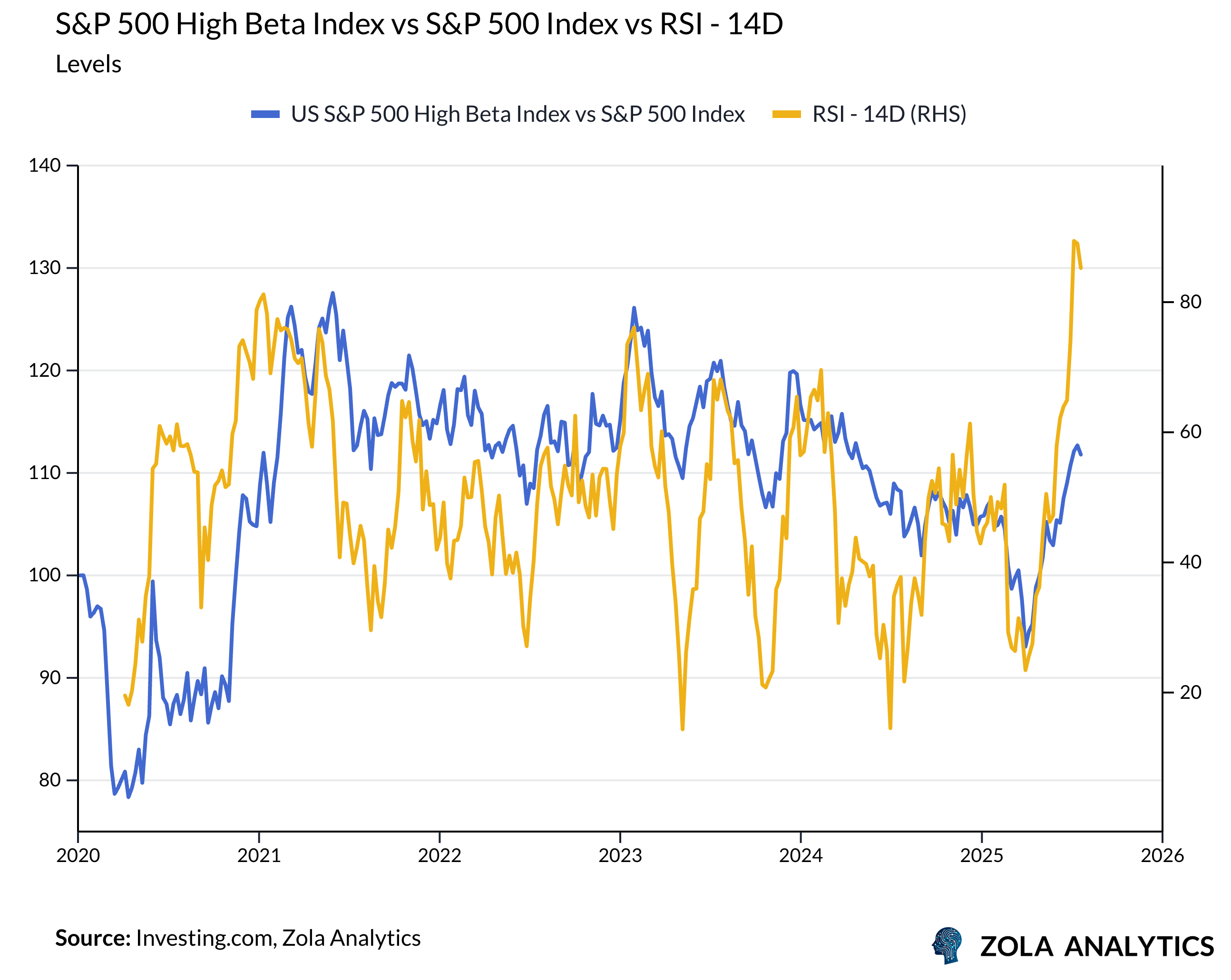

On the data front, the business cycle might finally be turning. Market-based gauges of the cycle —like high-beta stocks versus the S&P 500, the copper/gold ratio, and the Baltic Dry Index—are all flashing green. Global growth surprised to the upside last quarter, US composite PMIs have climbed into solid expansion, and regional Fed surveys are ticking higher. The summer rebound still has room to run.

There’s another reason for the Fed to wait. It remains unclear what the macro impact of the AI capex boom will be. Both Big Tech and Big Government are splurging:

US tech companies are planning roughly USD 7 trillion in spending by 2030.

Congress has passed Trump Big Beautiful Bill that includes permanent bonus depreciation and a nuclear power build-out that could unlock USD 2 trillion in investment.

Europeans are finally spending, with Germany leading a EUR 850 billion charge over the next five years.

Chinese policy has pivoted from “prudent” to “moderately loose”.

For that reason, the Fed has little to lose in waiting to see how far these measures offset the policy uncertainty caused by Trump’s trade war.

Sign up to receive the Zola Global Macro Chartbook every week: https://www.zolaanalytics.com/insights?signUp

Disclaimer: Zola Analytics provides this material for informational and entertainment purposes only. It does not constitute investment advice.