Published 19th January 2026

6 minute read

The Spender’s Shield

The Federal Reserve’s ability to control inflation relies on an old trade-off in the labour market. Fewer jobs mean less income, which curtails spending and remains the most reliable lever for taming rising prices. In this week’s edition of the Zola Chartbook we look at whether the pandemic has permanently degraded the Fed’s most important tool.

Vanished Guard

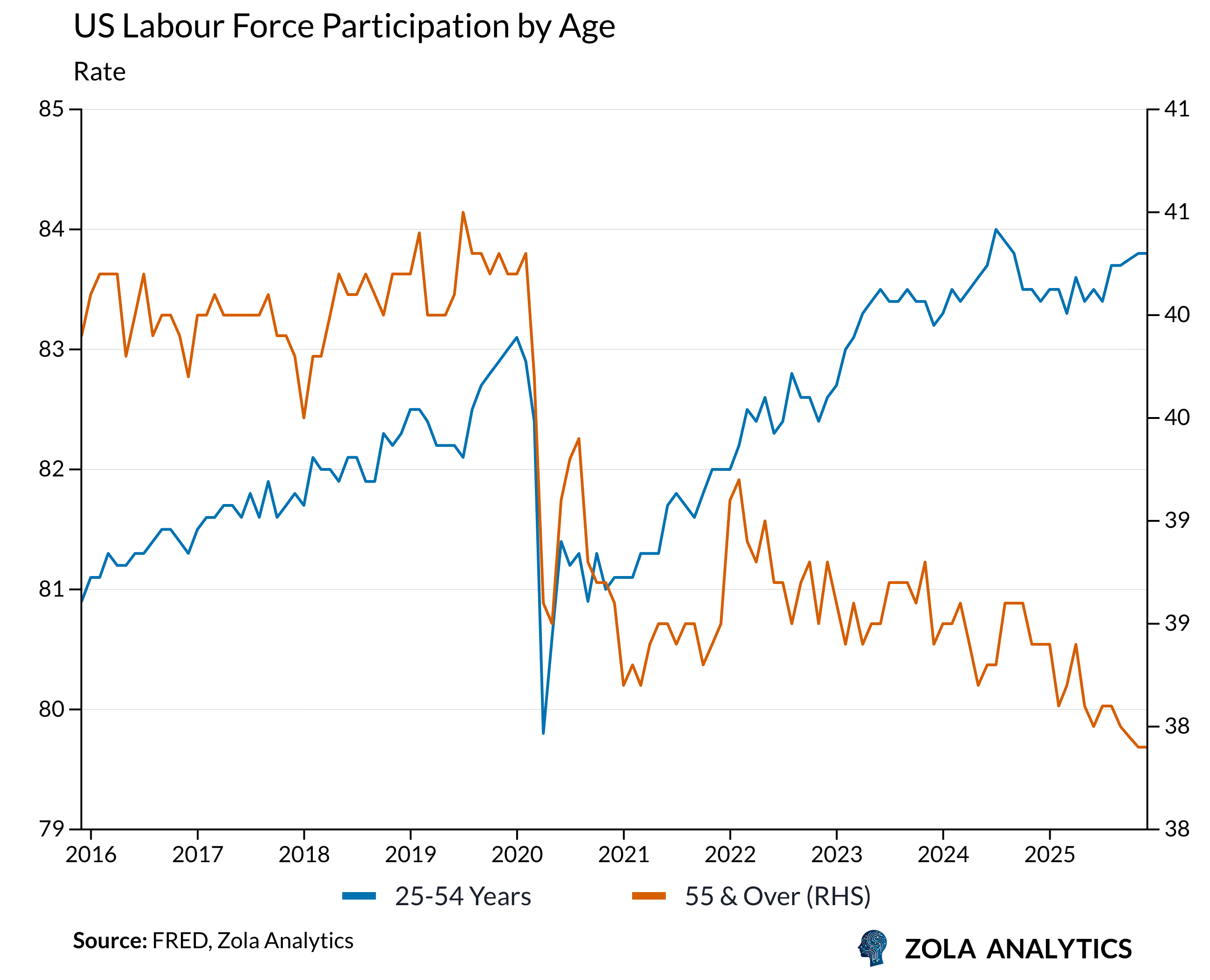

There is currently a shortfall of 2.4 million workers aged 55 and older from the labor force compared to pre-pandemic levels. Approximately 6% of older American workers are no longer working due to accelerated retirement or long term health issues, which contributes to the labor market tightness of recent years.

This shift means that fewer Americans among those doing the most spending have jobs to lose.

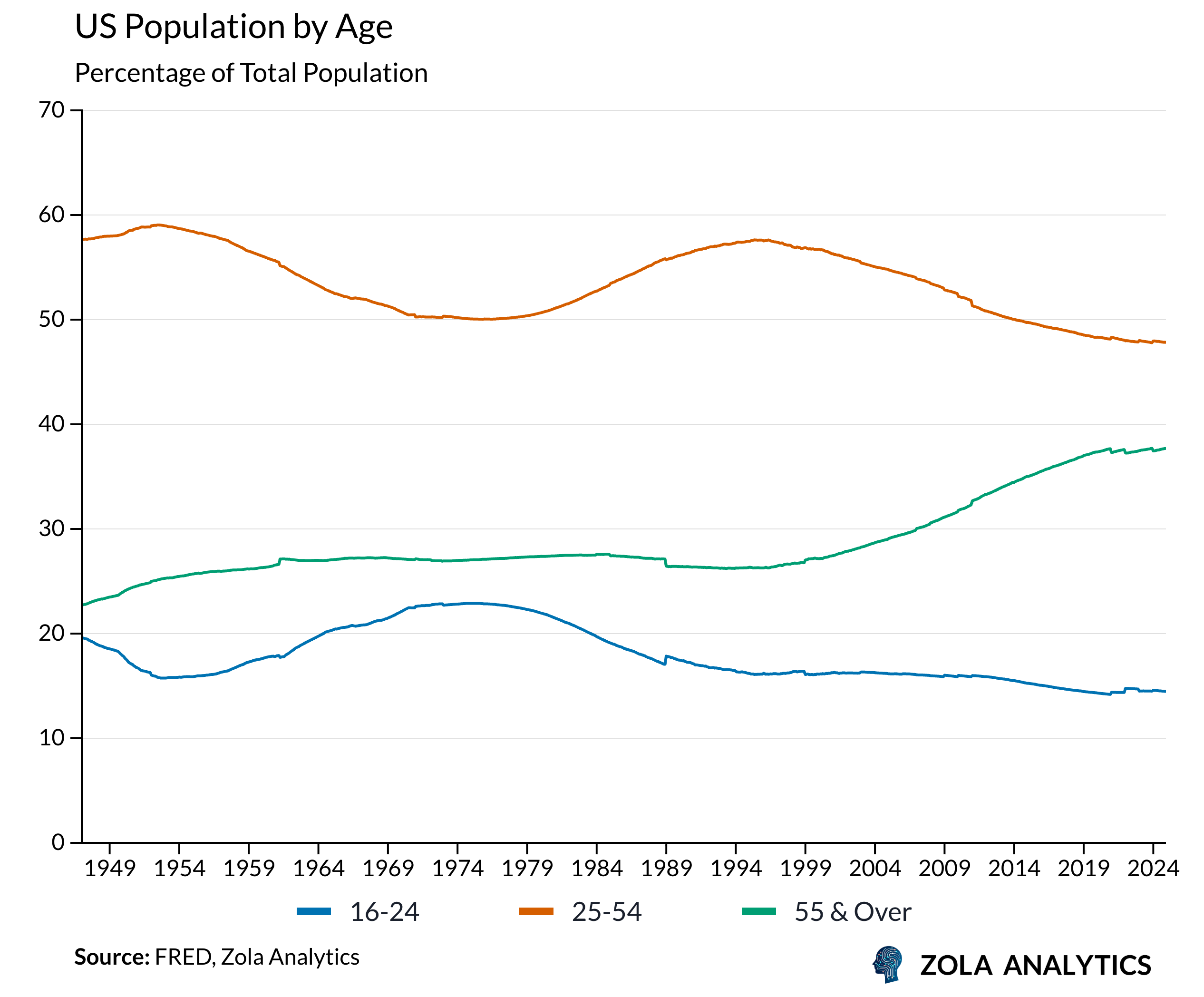

This is driven in part by the sheer size of the Baby Boomer generation entering retirement.

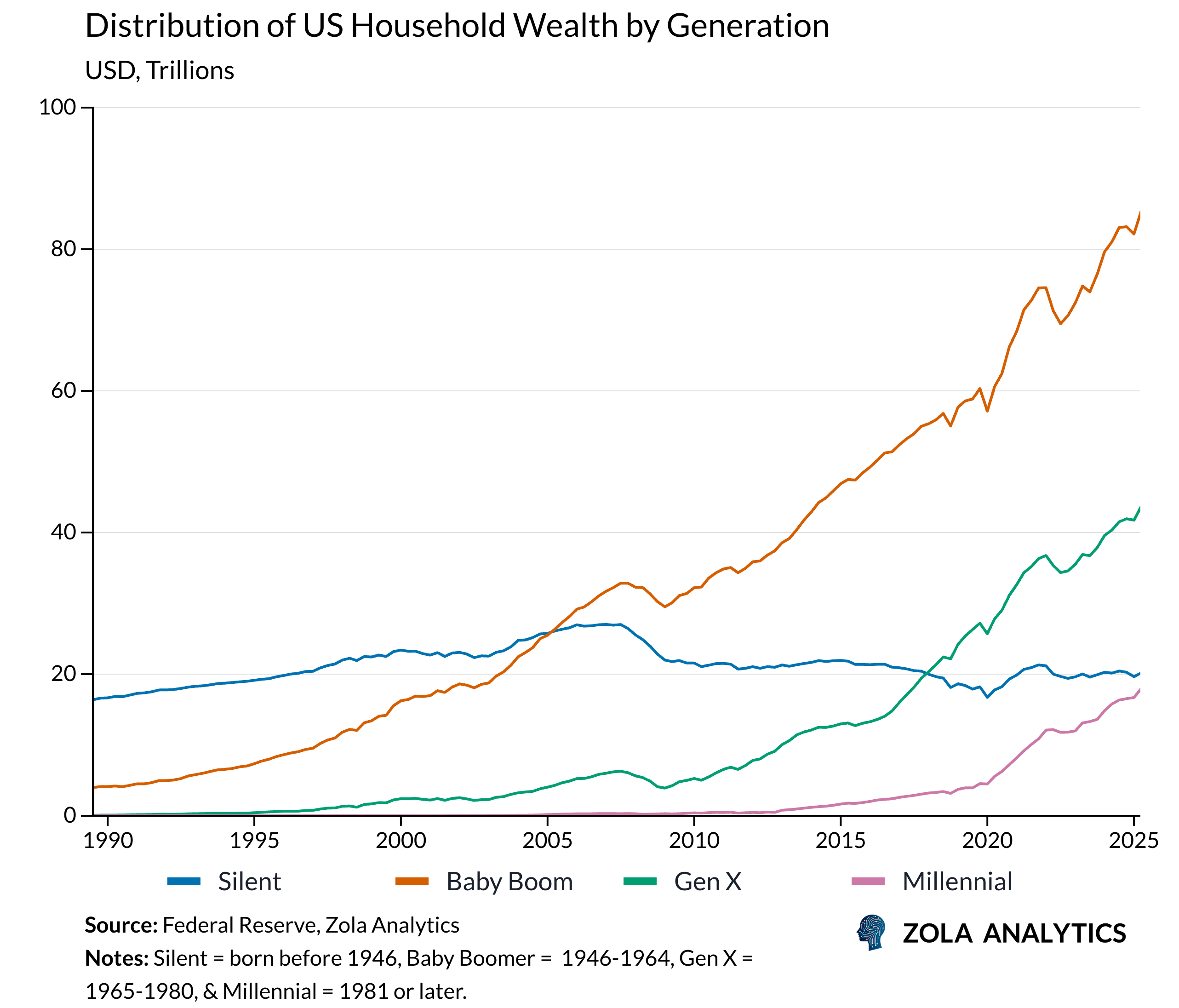

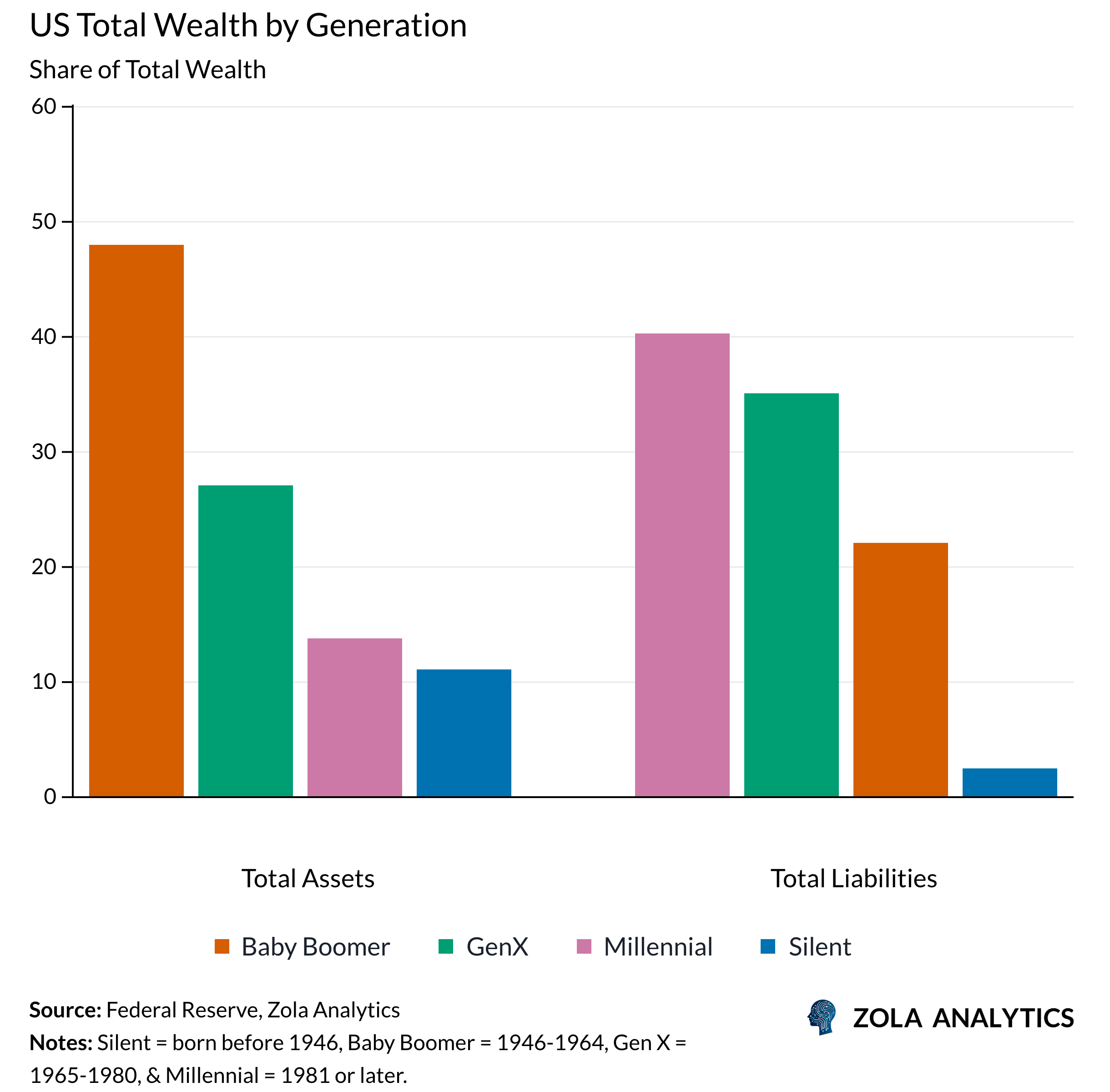

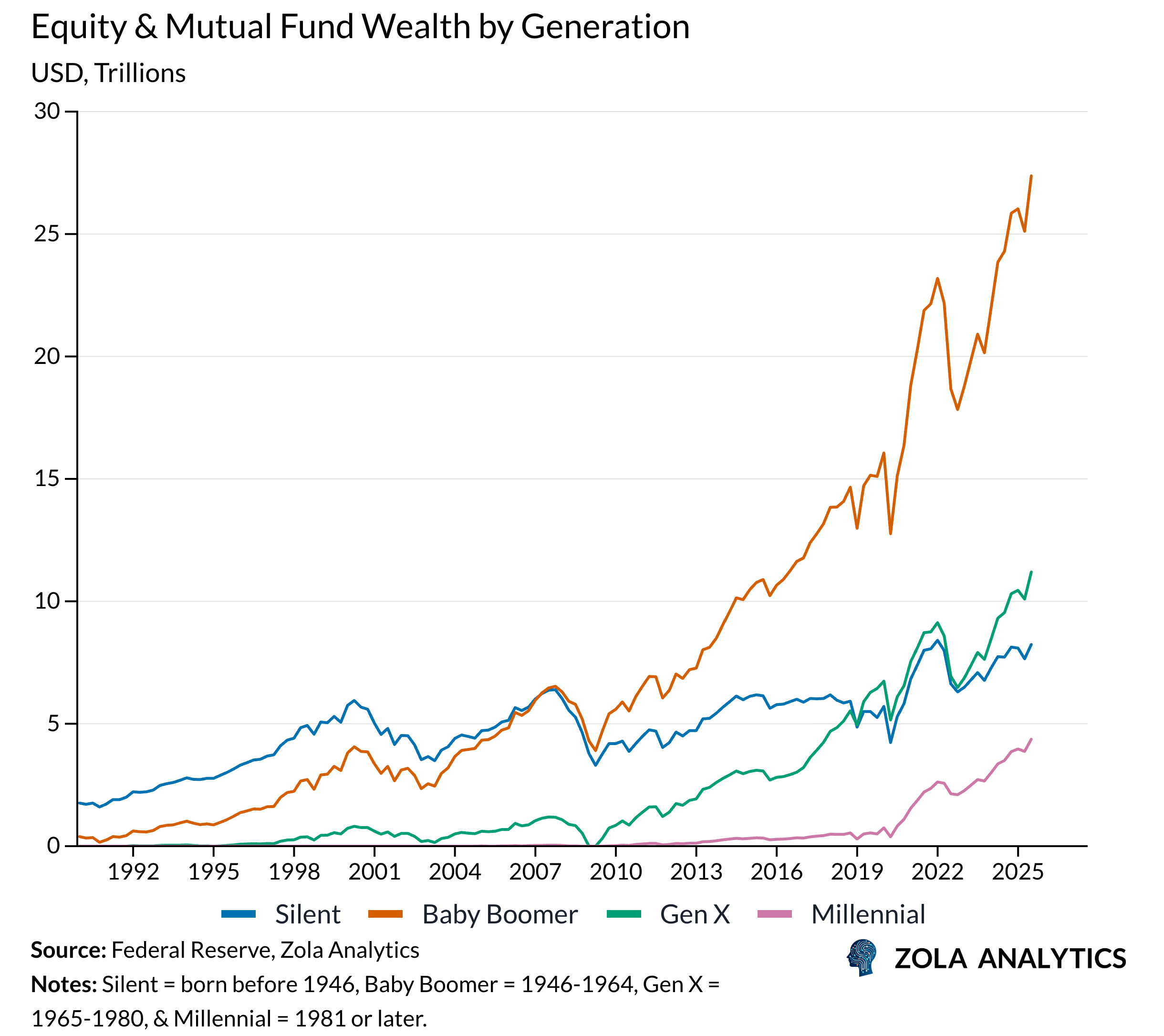

And by entering retirement wealthier than any generation before them, with 51% of US household wealth now sitting with those aged 55+, a share that has risen by 12% over the past 20 years.

Golden Armour

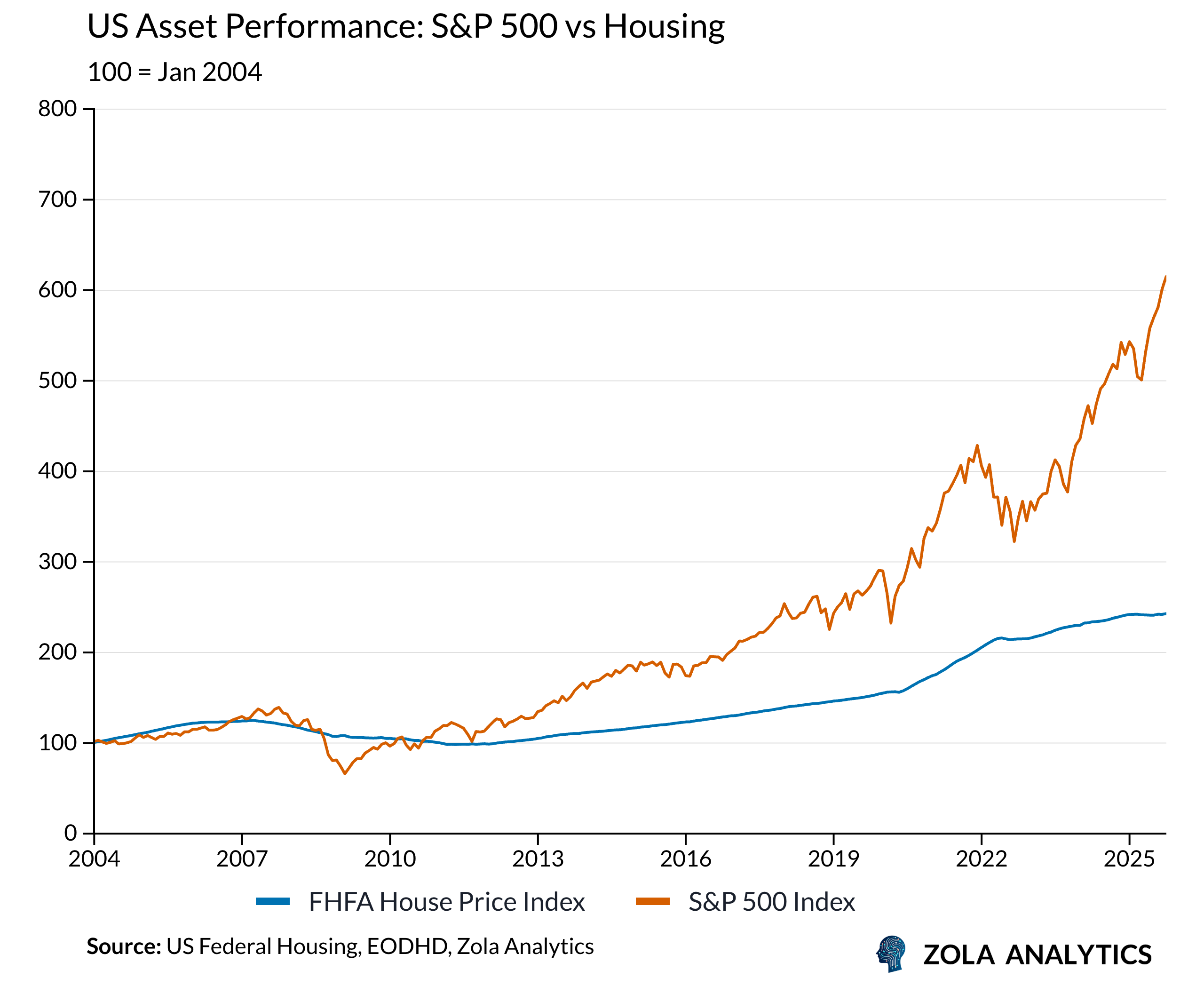

This wealth is not only the result of decades accumulation, but also the multi-decade bull-run in American asset prices. Over the past two decades, equities have increased more than 6 fold, while average home prices have more than doubled.

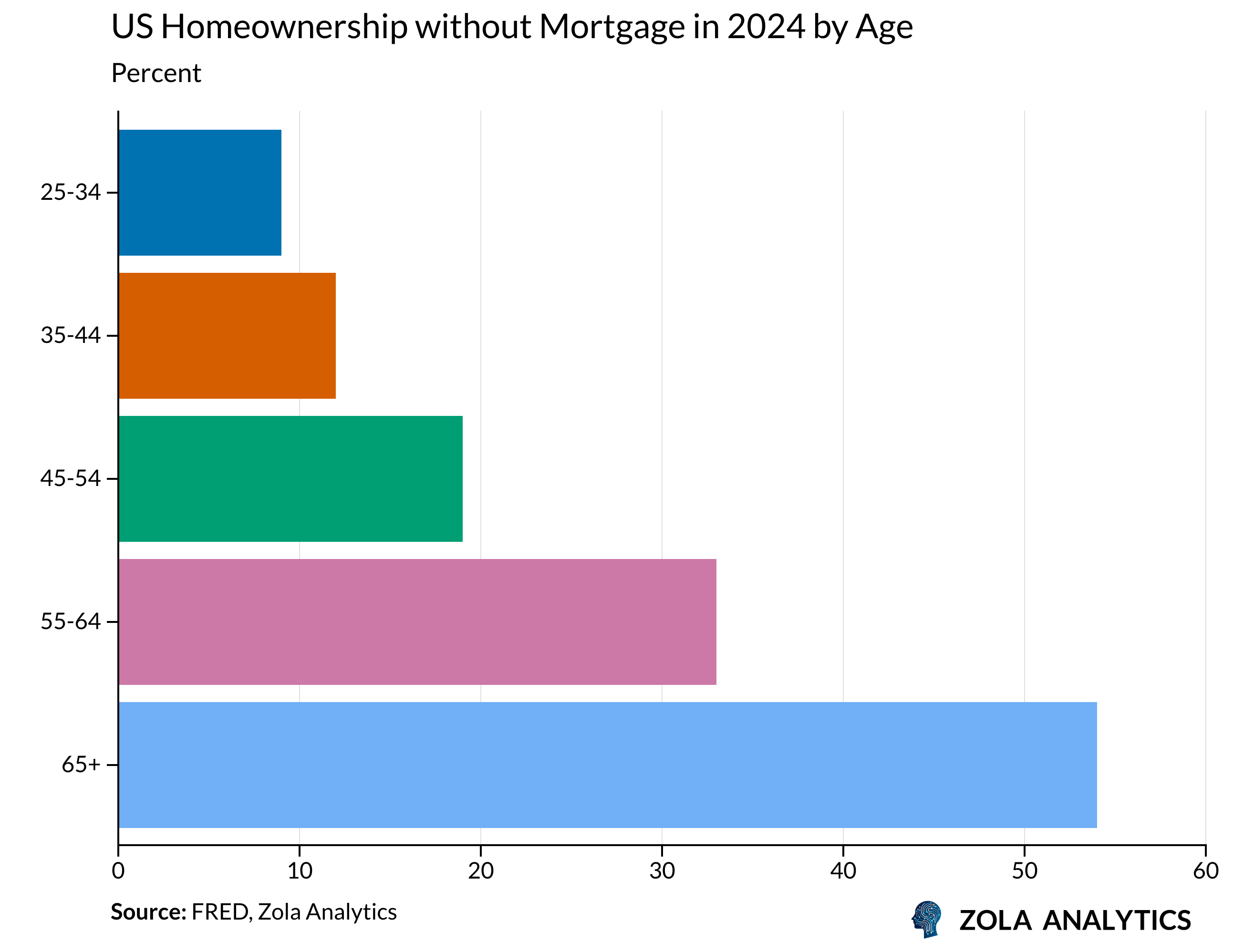

On top of that, more than half of homeowners aged 65 and older own their homes outright, and those who carry mortgages mostly hold fixed rate loans locked in before rates rose.

The strong balance sheets of older cohorts now stand in stark contrast to those of the young. The same forces that allowed Baby Boomers to compound wealth through rising asset prices and falling interest rates have left younger households far more leveraged, with a greater share of their economic exposure sitting on the liability side of the balance sheet.

Misfiring Weapons

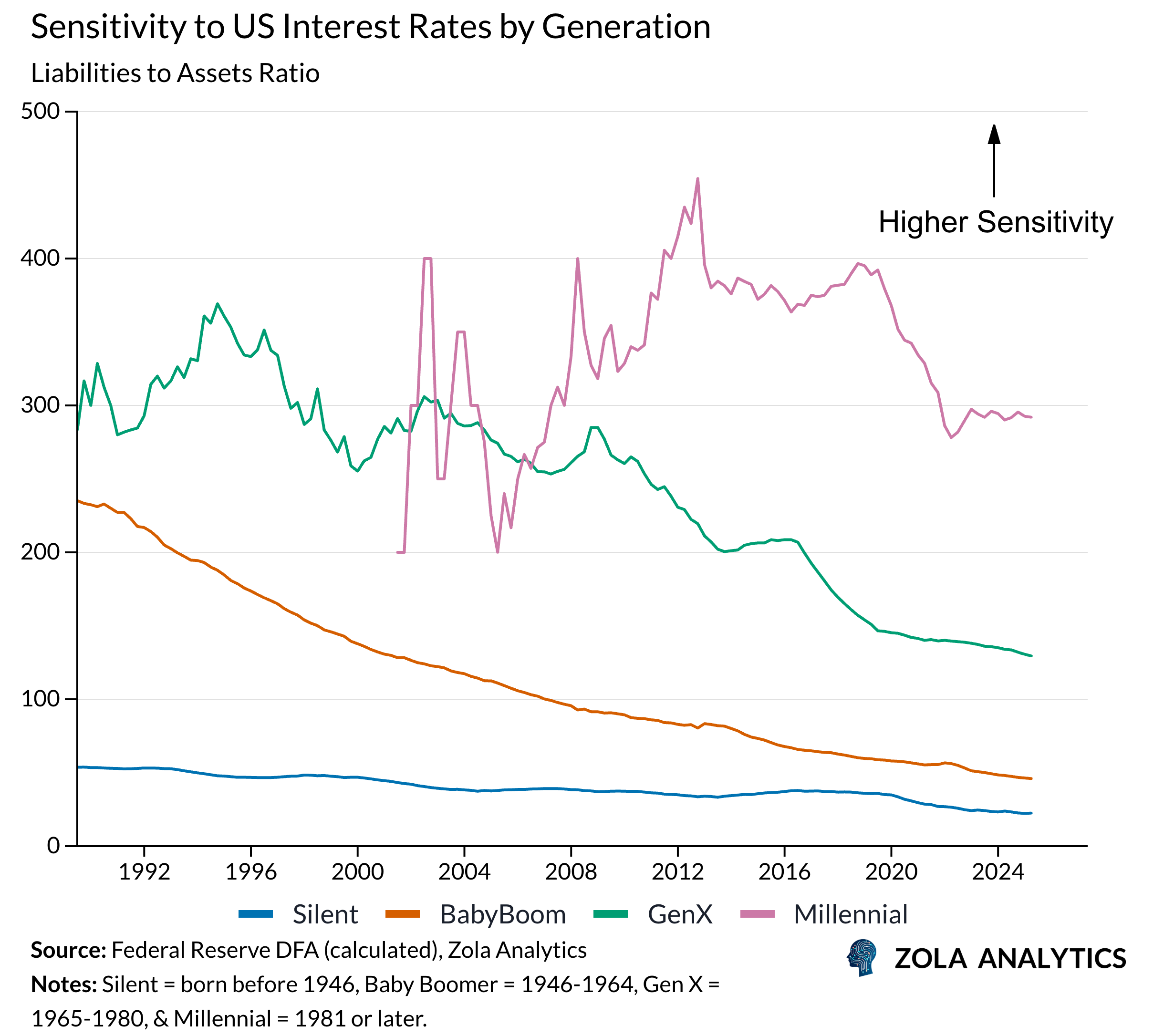

This structure reshapes monetary transmission by creating sharply different interest rate sensitivities across generations. Younger households exhibit high rate sensitivity because higher interest rates quickly erode disposable income through rising mortgage and borrowing costs.

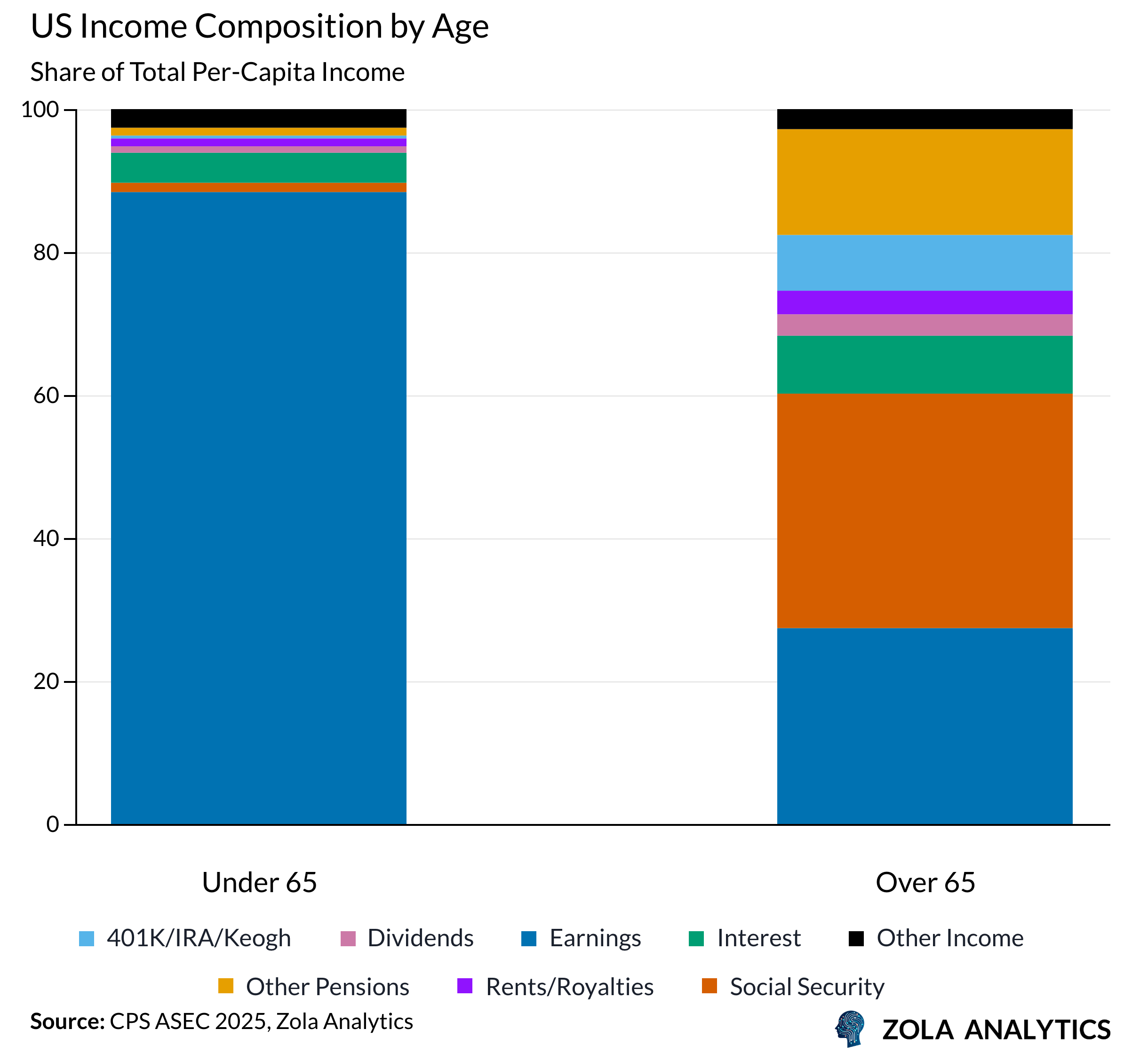

For those under 65, 88% of income comes from earnings, which is the very channel the Fed targets when it tightens, while for those over 65, earnings account for just 27%; the remaining 73% flows through Social Security, interest, dividends, and retirement drawdowns.

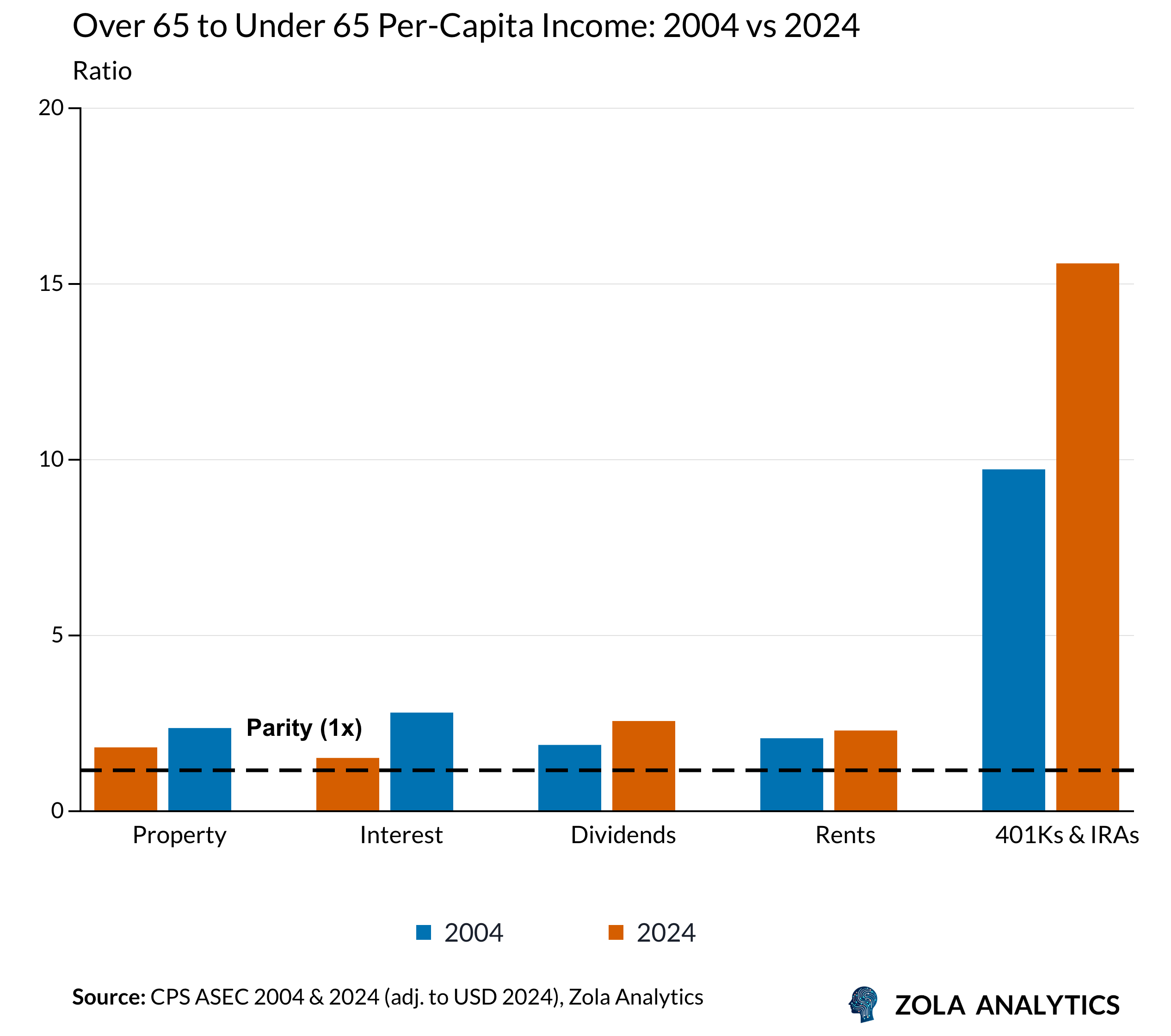

Over the past two decades, this insulation has only deepened. While younger workers have saved more, interest still represents double the share of income for seniors compared to those under 65. Meanwhile, the ratio of 401K income has surged from 9.7x to 15.6x as retirees draw down decades of accumulated savings.

Raising rates shifts income from younger borrowers to older lenders, perversely increasing disposable income for the very cohort the Fed needs to slow. This suggests that headline spending strength masks a deepening structural imbalance. Because senior spending remains resilient, the Fed may be forced to maintain higher rates for longer, widening the gap between a younger generation constrained by credit and an older generation whose spending power is essentially decoupled from borrowing costs.

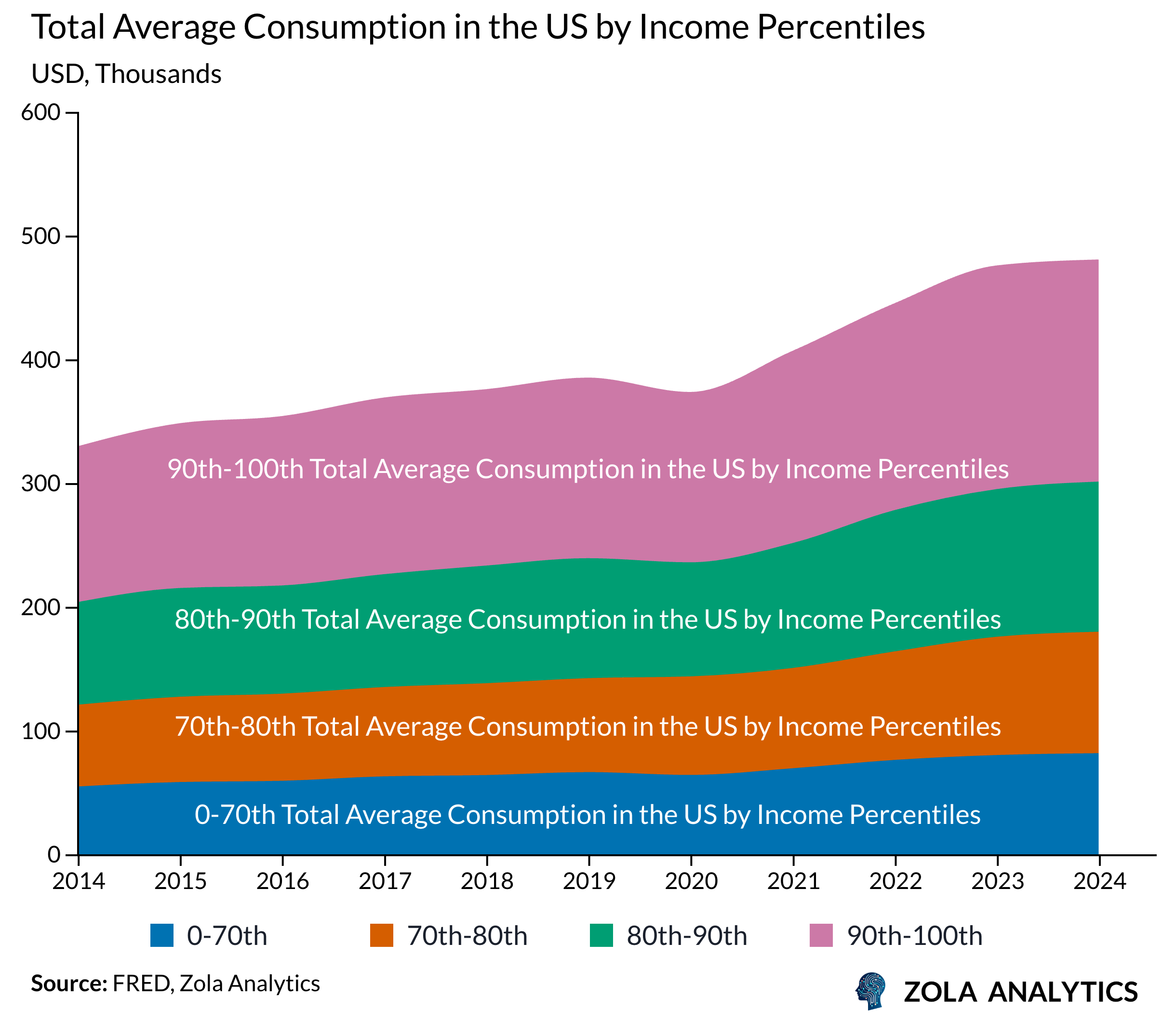

This concentration of consumption at the top illustrates the difficulty of the Fed's position. When the primary spending engine is driven by a narrow, asset-rich cohort, traditional interest rate hikes lose their broad effectiveness.

Consumption Floor

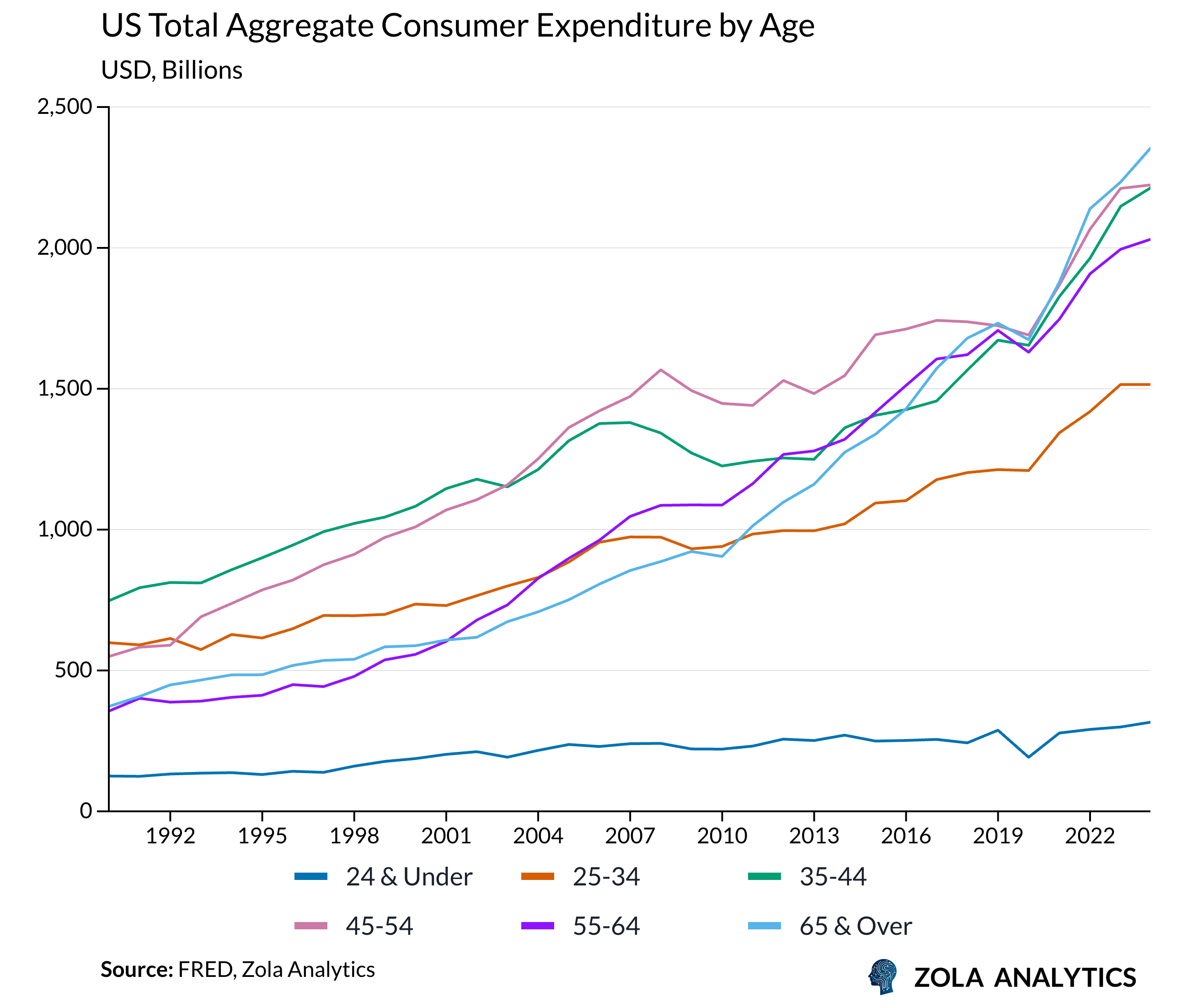

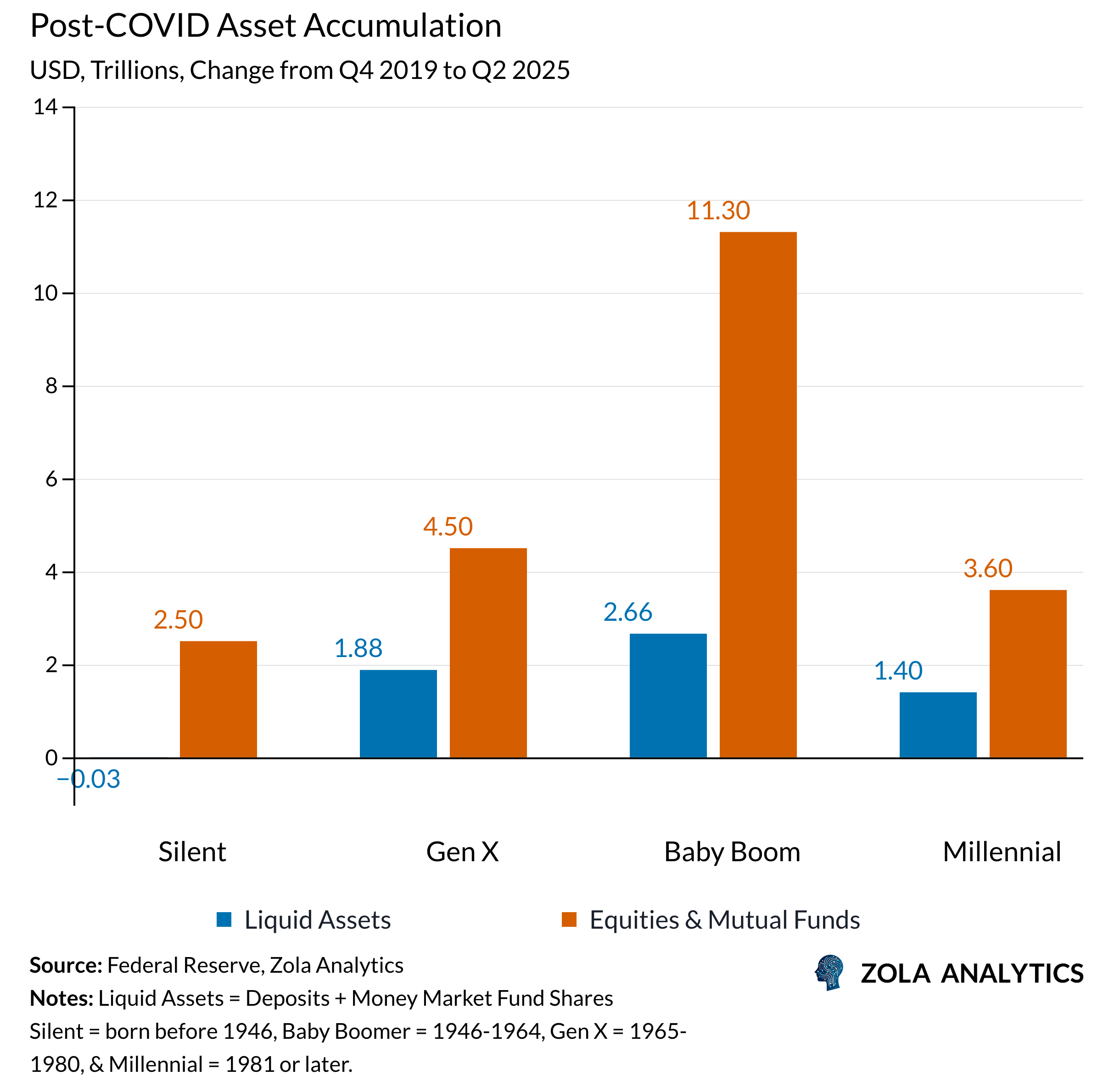

Whilst these trends in wealth distribution have been in motion for decades, since COVID they have sharply accelerated. Baby Boomers have captured the greatest gains since 2020.

Retirees today hold massive amounts of wealth, and the SECURE 2.0 Act is forcing that money into the economy. The law now requires individuals to start withdrawing a minimum amount from their 401Ks and IRAs once they reach age 73. Because these withdrawals are mandatory, retirees are forced to move money out of their investment accounts and into their bank accounts, regardless of whether they actually need the cash or if the market is performing well.

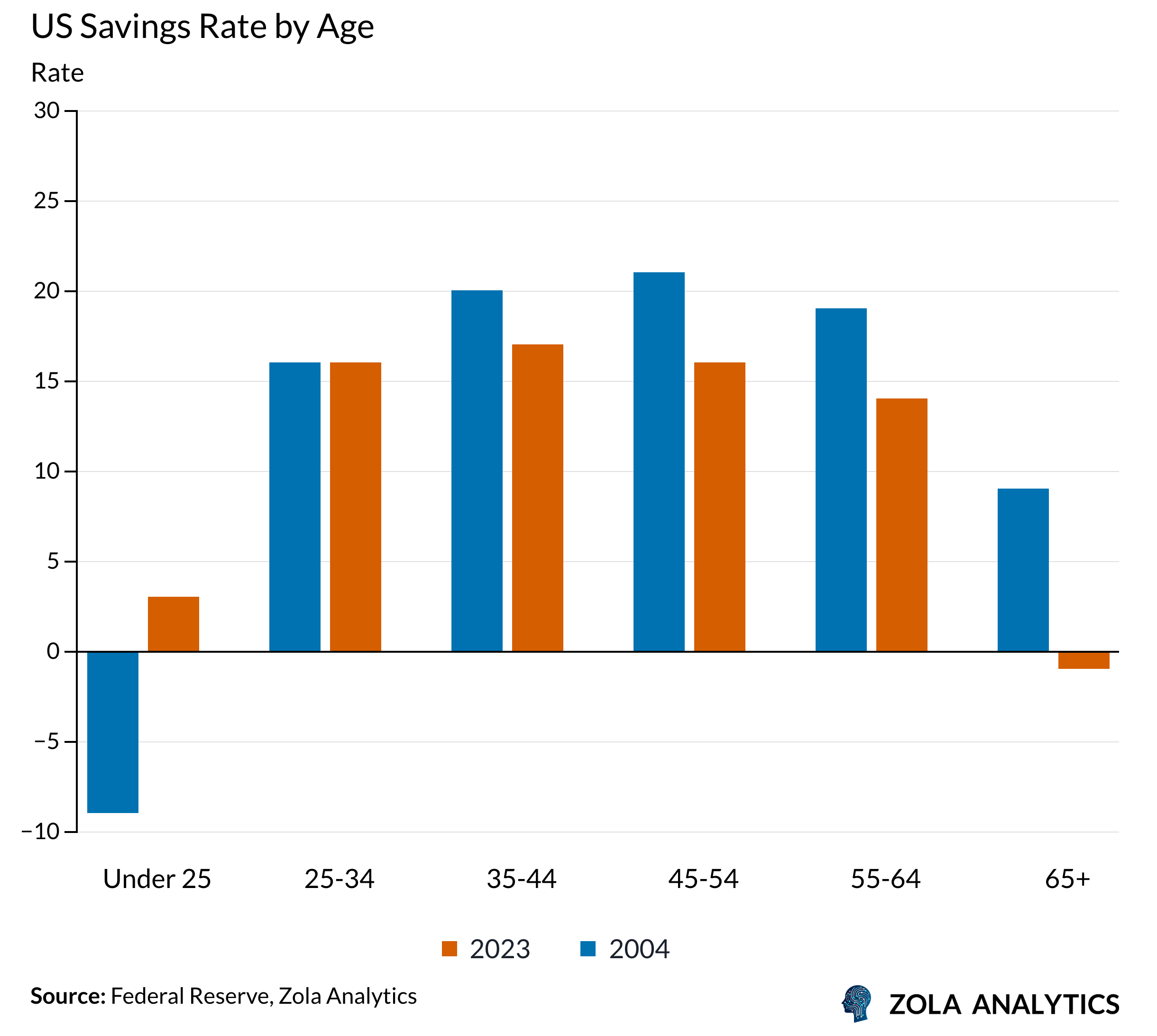

This trend is breaking the mold of the retirement smile, which is the long held assumption that spending naturally fades in later life. Instead, today’s retirees are defying expectations. Savings rates have declined across all age cohorts over the past two decades, but the fall has been steepest among those 65 and older.

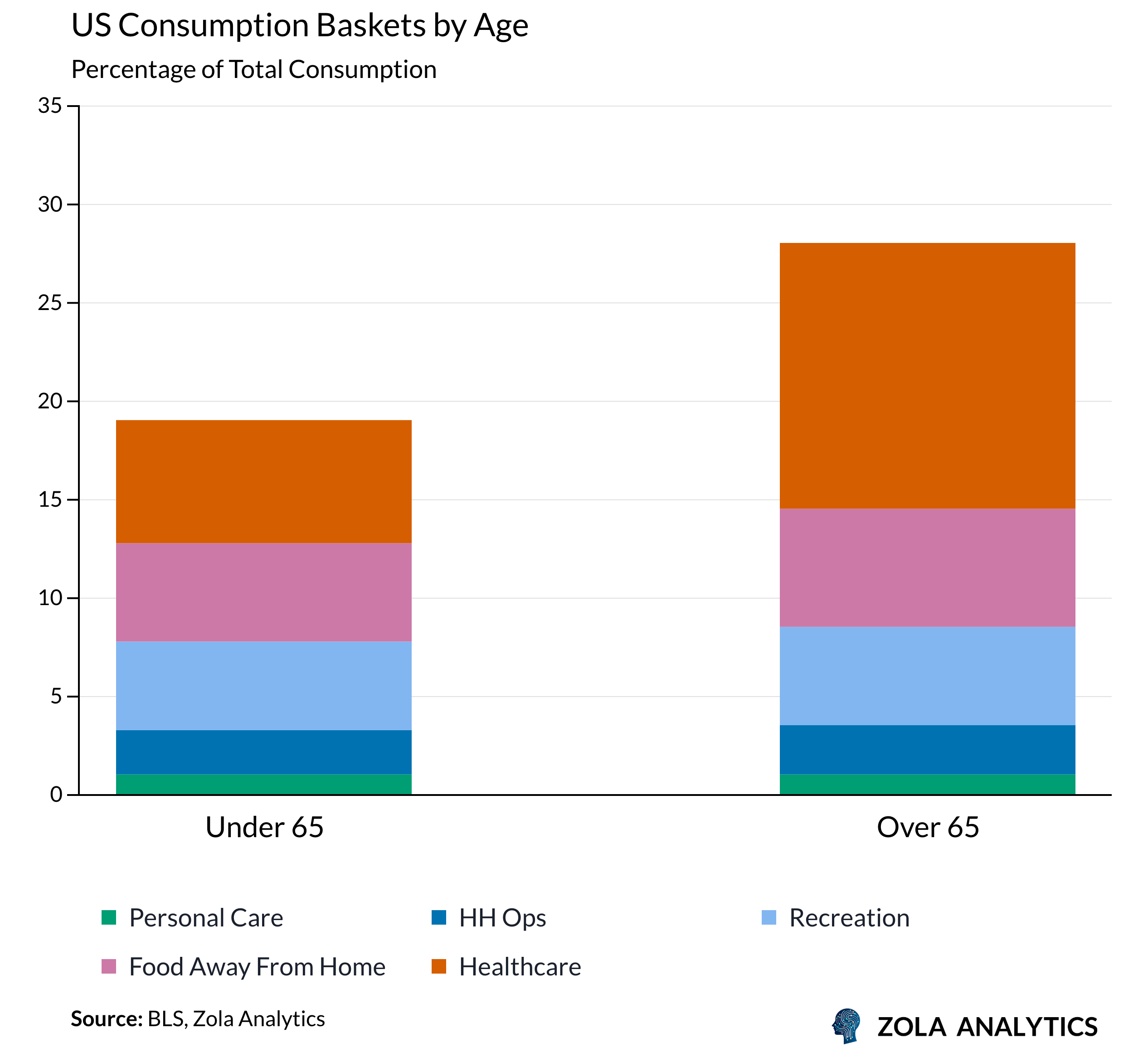

In addition, whilst they spend more than twice the average share on healthcare, they are also maintaining their budgets for travel and home maintenance.

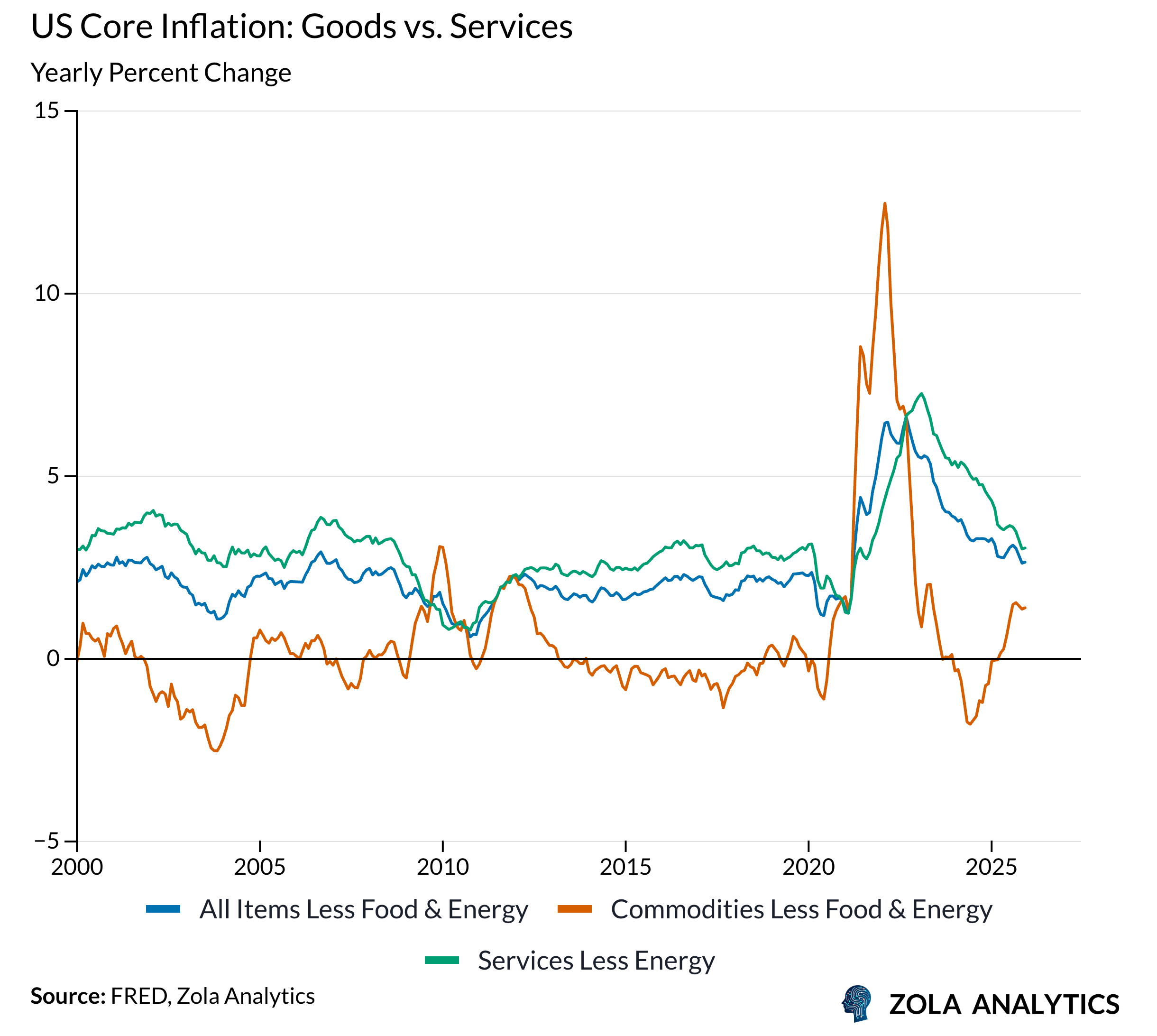

These categories are inherently labor intensive, seniors are exerting pressure on both supply and demand. Seniors are exerting pressure on the economy by exiting the labor force in record numbers while simultaneously concentrating their spending in these high demand service sectors. This shift reduces the overall labor supply while keeping demand for these workers high. As a result, core goods prices have largely normalized though core services have not. The composition of senior consumption now maps almost perfectly onto the current landscape of sticky inflation.

The Two-Front War

For forty years, the Baby Boom generation shaped the economy by saving. Now they shape it by spending, and the Fed’s primary tools cannot reach them. However, these spenders of last resort have a vulnerability. They hold approximately 54% of all corporate equities.

This wealth concentration breaks the traditional transmission mechanism because the primary spending engine now relies on assets rather than credit.

This creates a policy trap. Because the primary spending engine relies on equities, it is more sensitive to market volatility than to interest rates. If the Fed cuts rates to help workers, it inflates the assets that power senior spending. If it keeps rates high, it fails to slow the main source of demand. The central bank is left with an increasingly narrow path to price stability.

Ultimately, this structural misalignment threatens to strip the central bank of its reputation as a neutral arbiter, revealing an economy caught between two generations with irreconcilable financial realities by the traditional central bank toolkit.