Published June 4th 2025

Europe Shines Amid Global Strain

As global investors recalibrate for a world shaped increasingly by US policy unpredictability and rising geopolitical risk, Europe is beginning to look less like a source of weakness and more like a centre of relative stability. Quietly but noticeably, the euro area is absorbing external shocks and positioning itself for a more durable – if modest – recovery.

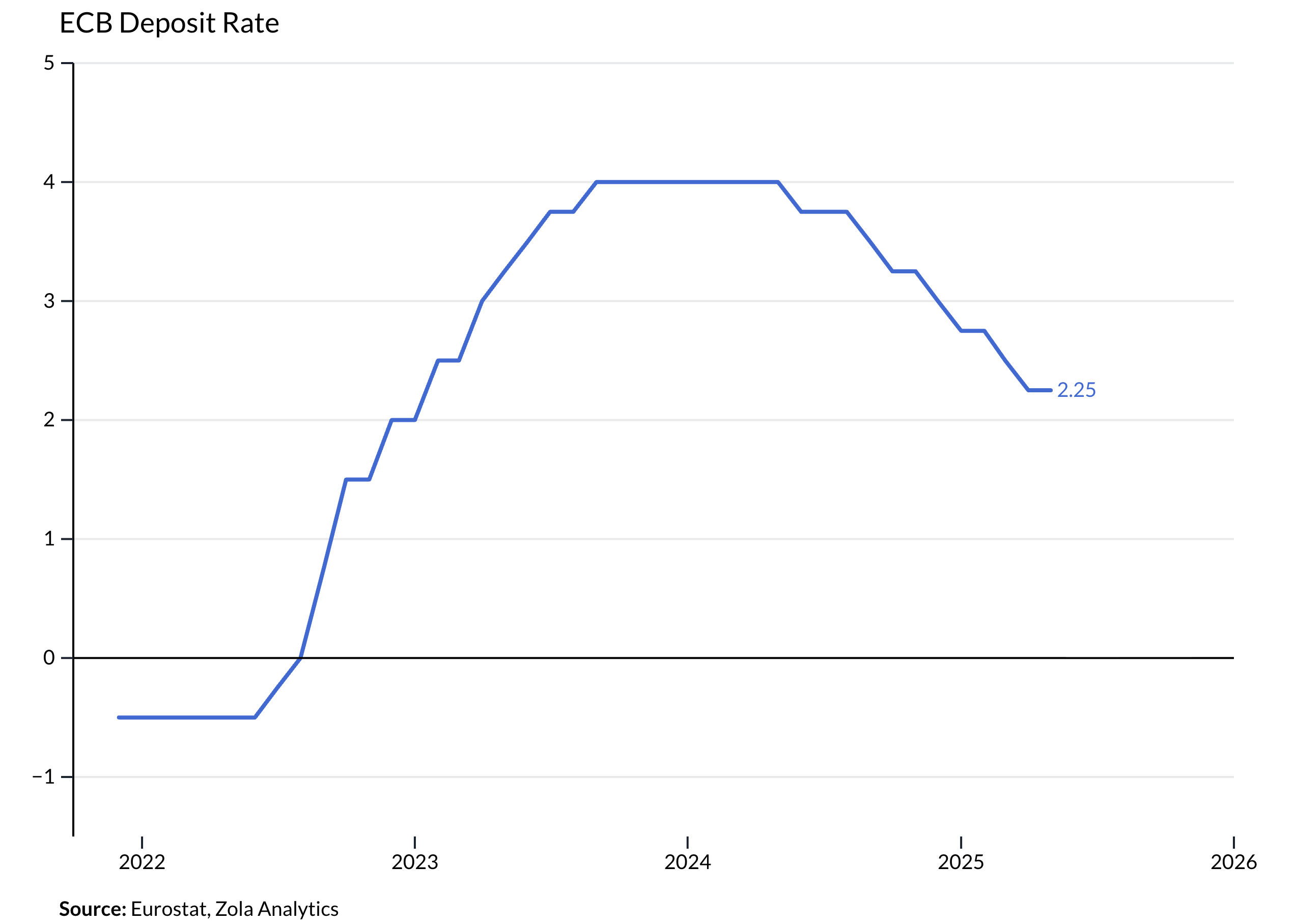

Recent data confirms this shift. Inflation in the euro area is converging towards the ECB’s target more decisively than in the US. With inflation pressures easing, energy prices subdued, and wage growth moderating, the ECB is set to deliver a 25bp rate cut this week. This marks the start of a more accommodative cycle, likely totalling 225bp in cuts – a strong contrast to the still cautious tone of the Federal Reserve.

From Fragility to Flexibility

Growth in the eurozone remains tepid, with Q2 and Q3 likely to show only modest quarterly expansion (0.2–0.3%). However, what was once interpreted as stagnation may now be viewed as resilience. Domestic drivers – including real wage growth, tight labour markets, and nascent fiscal expansion – are quietly reinforcing the foundations of demand.

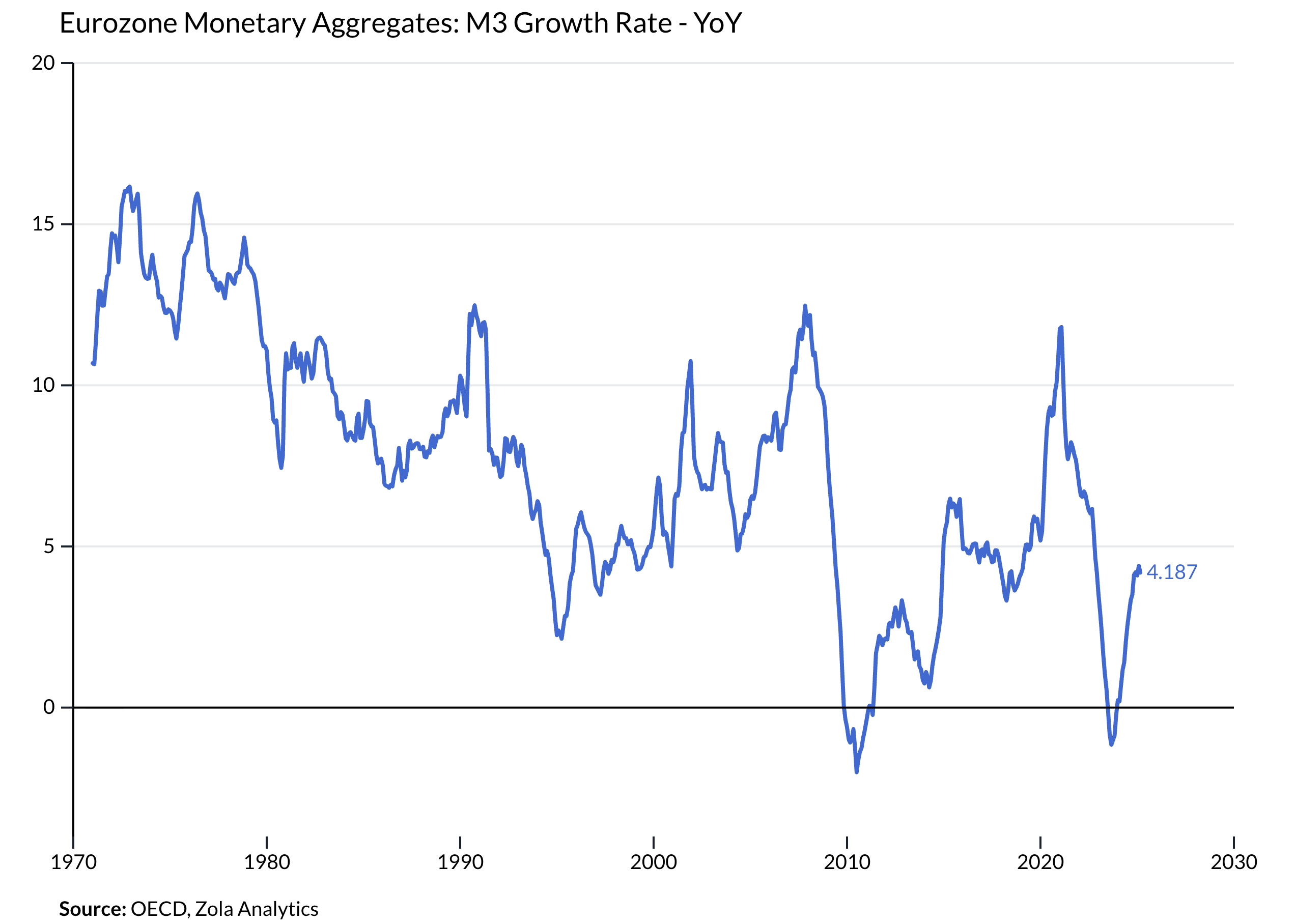

Credit growth has turned positive, money supply is rising, and plans for substantial defence and infrastructure investment (including Germany’s EUR500bn fund) hint at a shift in policy orthodoxy. Europe, long criticised for its fiscal conservatism, is slowly pivoting to a more countercyclical stance. This could compound the support from lower interest rates and improve the medium-term outlook.

Benefiting from US Overreach

Importantly, Europe is also a relative beneficiary of US policy errors. As the US expands tariffs and risks its fiscal credibility, investors are reassessing safe havens. European bonds are once again in demand, and euro-denominated assets may capture flows displaced from US treasuries.

Moreover, with the US increasingly perceived as politically volatile, the eurozone’s steady governance – while often fragmented – appears more predictable by comparison. This matters for capital allocation in a world where geopolitical risk is a core input.

Caveats and Catalysts

To be sure, Europe faces its own headwinds. The continent remains exposed to external demand, particularly for manufactured goods, and the service sector is showing signs of softness, as seen in recent PMIs. Additionally, structural challenges around energy dependence, demographic drag, and productivity remain unresolved.

Yet the broader shift is clear: Europe is no longer the global laggard. Instead, it may be emerging as a safe, if uninspiring, port amid the policy storm brewing across the Atlantic.

Conclusion: Repricing Europe

For investors, this suggests a re-evaluation of euro area assets is warranted. While absolute returns may remain modest, the region offers diversification, duration safety, and cyclical convergence. In a year where relative stability is at a premium, Europe may quietly outperform expectations.

Disclaimer: Zola Analytics provides this material for informational and entertainment purposes only. It does not constitute investment advice.