Published August 1st 2025

4-min read

US Labour Market Turns

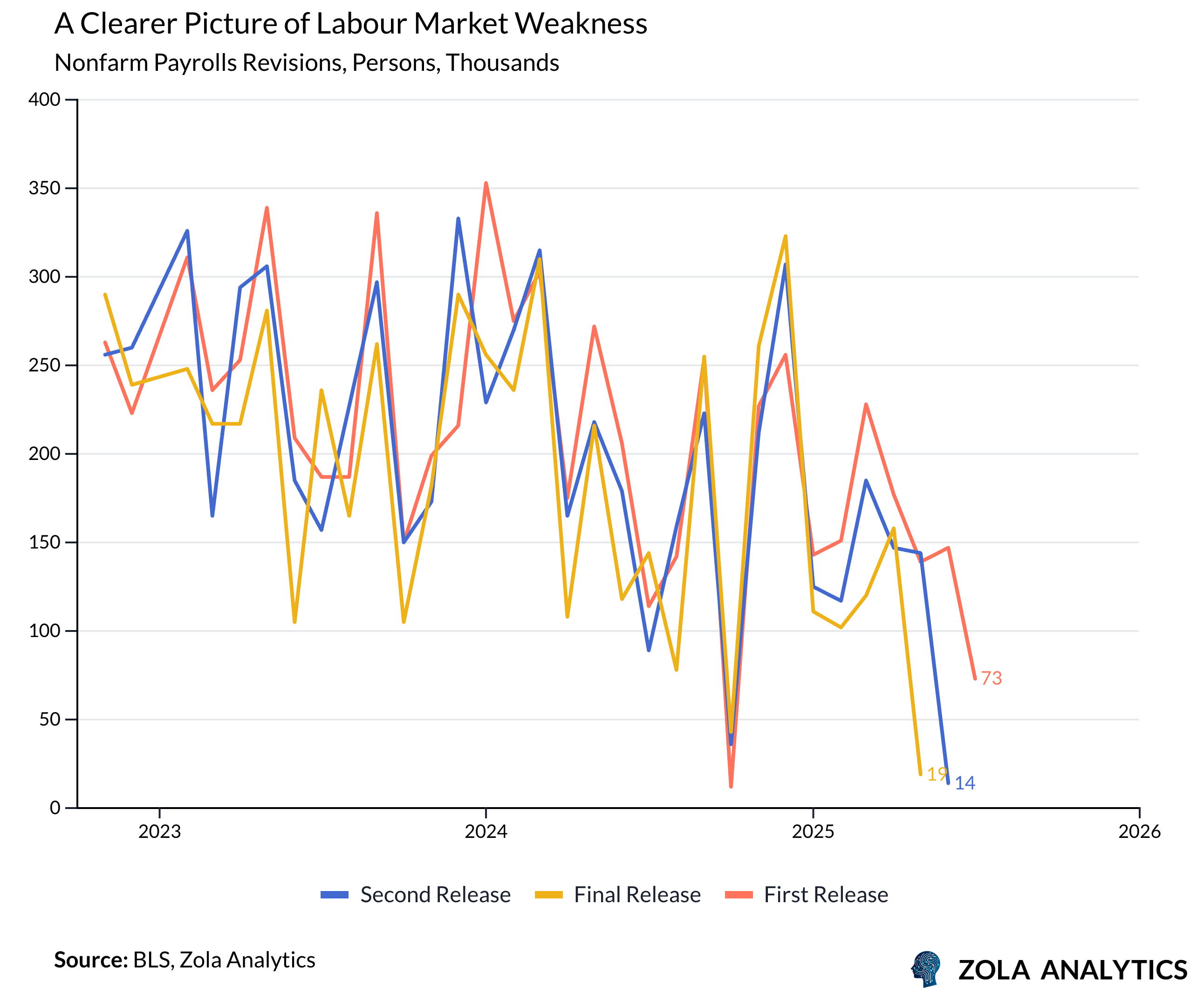

The July employment report marks a clear shift in the U.S. labour market narrative. While headline payroll growth came in at a modest +73,000, well below consensus, the more consequential development lies beneath the surface: sharp downward revisions to prior months reveal a much more fragile backdrop than previously understood. With the three-month average payroll gain collapsing to just +35,000, down from +150,000, labour market momentum appears to have not only slowed but potentially turned.

Payroll revisions are often dismissed as statistical noise. But historically, they’ve carried strong cyclical signals, particularly around inflection points when estimation models struggle to account for firm births, deaths, and seasonal volatility. The July report fits this pattern. Revisions to May and June wiped out a significant chunk of job gains, recasting the trend from “resilient slowdown” to “incipient contraction.”

This shift in the revision profile suggests the slowdown is not new, it’s merely being revealed with a lag.

Narrow Job Gains Mask Underlying Weakness

Health care and social assistance continue to carry the labour market. Without these sectors, payroll growth would have been negative for three consecutive months. This concentration is not just a statistical footnote — it speaks to the lack of breadth in hiring.

In July, only half of the major sub-industries added jobs. Manufacturing and government both saw job losses, declining by 11,000 and 12,000, respectively. Such sectoral weakness is a classic symptom of a maturing cycle where private-sector hiring becomes more selective, and public hiring retreats.

Unemployment Rate Doesn’t Tell the Full Story

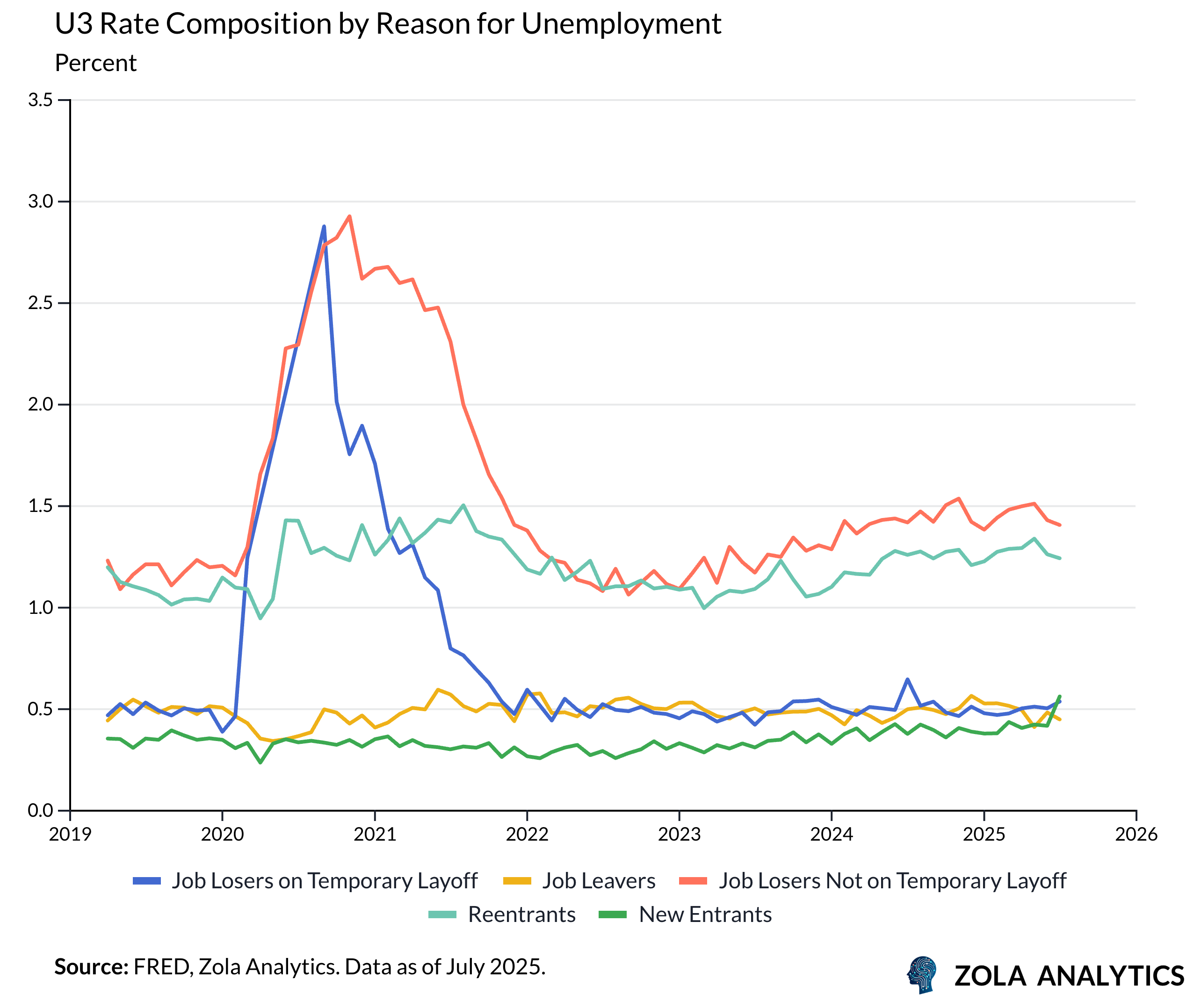

Despite the labour market’s loss of steam, the unemployment rate edged up only modestly to 4.2%. But this masks more worrying developments under the surface.

A few dynamics stand out:

Job leavers are declining, a sign that workers are more cautious about switching jobs, consistent with weaker hiring appetite.

Labour force growth is stalling, possibly reflecting slower immigration and ageing demographics.

Flows from “not in the labour force” to unemployed are rising sharply, suggesting more people are trying — and failing — to re-enter the job market. Most of these are reentrants: people who previously left work, for caregiving, retirement, or school, and are now struggling to find a way back in. But new entrants are also facing growing headwinds, with their contribution to unemployment jumping by 14 basis points in July, a sharp move that may reflect rising job search activity among recent migrants.

These internal flows indicate a labour market that’s becoming less dynamic and more exclusionary, often a precursor to rising headline unemployment.

September Becomes a Live Meeting

While the Fed held rates steady in July, two dissents in favour of a cut suggest that internal momentum is building toward a policy pivot. With labour data softening and revisions pointing to prior misreads, the bar for a rate cut in September has lowered meaningfully.

Markets are already adjusting. The post-NFP response — a bull steepening of the yield curve — reflects rising expectations of easing and renewed confidence that the next move is down.

If August brings further confirmation, weaker inflation and continued labour softness, the Fed may find itself compelled to move more quickly than previously signalled.