Published June 10th 2025

Locked and Loaded

War is hell — but war is also big business Nations and corporations across the world are hooked on weapons, and the global gun economy is booming. Governments spent a record USD 2.4 trillion on militaries in 2023, the largest one-year increase since 2009 (SIPRI). From legal arms mega-deals to black-market bullets, money is changing hands as fast as weapons. The world’s addiction to arms has become an economic force — propping up jobs, exports, and even entire national budgets.

The Legal Arms Bazaar: Who Sells and Who Buys

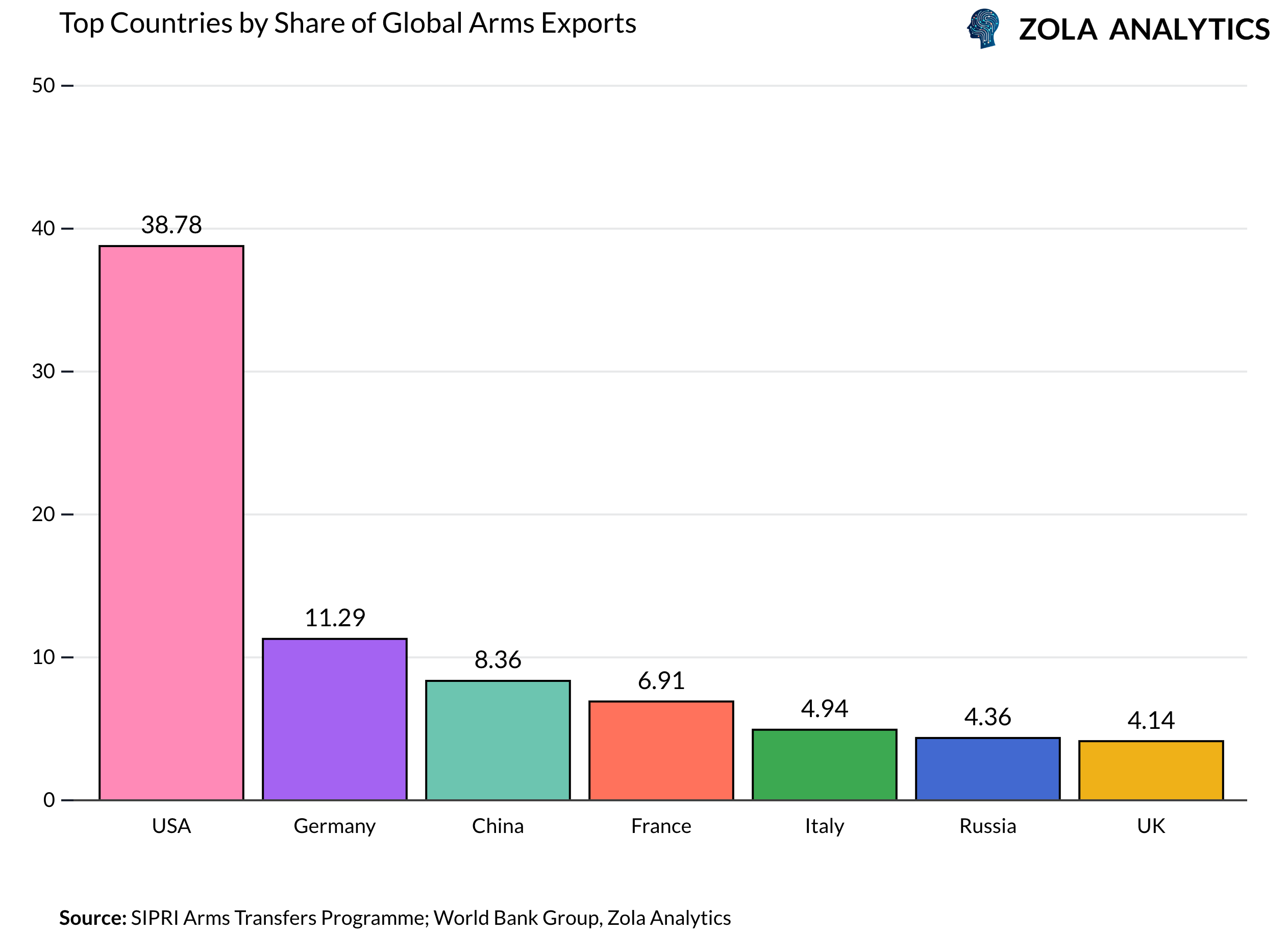

On the legal market, a handful of players dominate weapons exports. The United States alone accounts for 39% of global major arms exports, more than four times the next largest exporter, France (SIPRI). The U.S. has become the world’s primary armoury, supplying much of the advanced weaponry used by both allies and proxy forces.

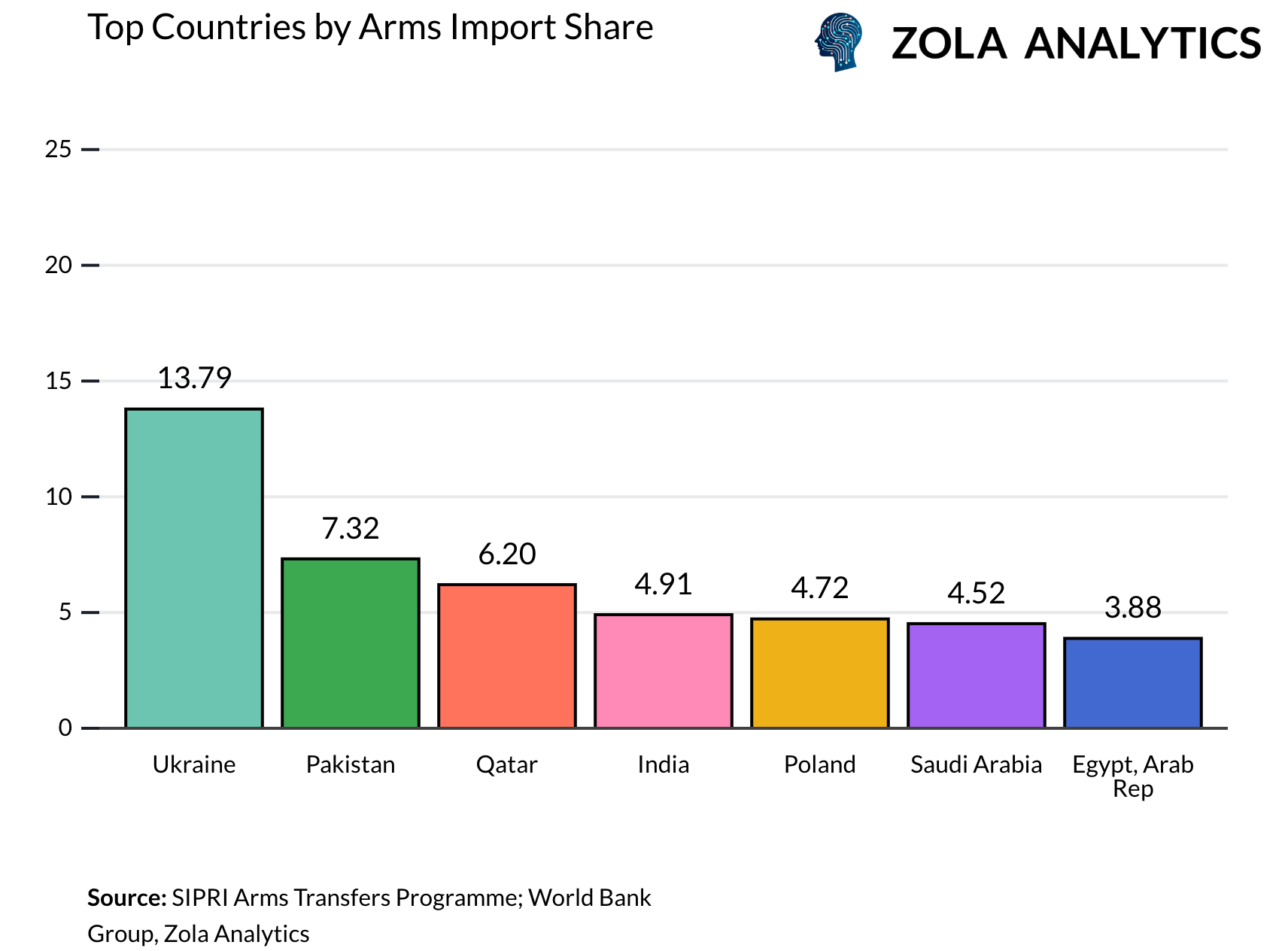

On the demand side, the biggest importers are often conflict-prone or security-driven states such as Ukraine, Qatar, and Saudi Arabia. The resulting cycle — where geopolitical insecurity fuels ever-larger arms purchases — sustains a lucrative global trade.

Russia’s share of arms exports has plummeted by 64%, as war and sanctions forced Moscow to redirect weapons to its own front lines (SIPRI). France has stepped into the vacuum, climbing to the No. 2 spot with aggressive exports of fighter jets and missiles. China, meanwhile, has reduced its reliance on foreign arms by slashing imports 64% and building up a self-sufficient military-industrial base (SIPRI).

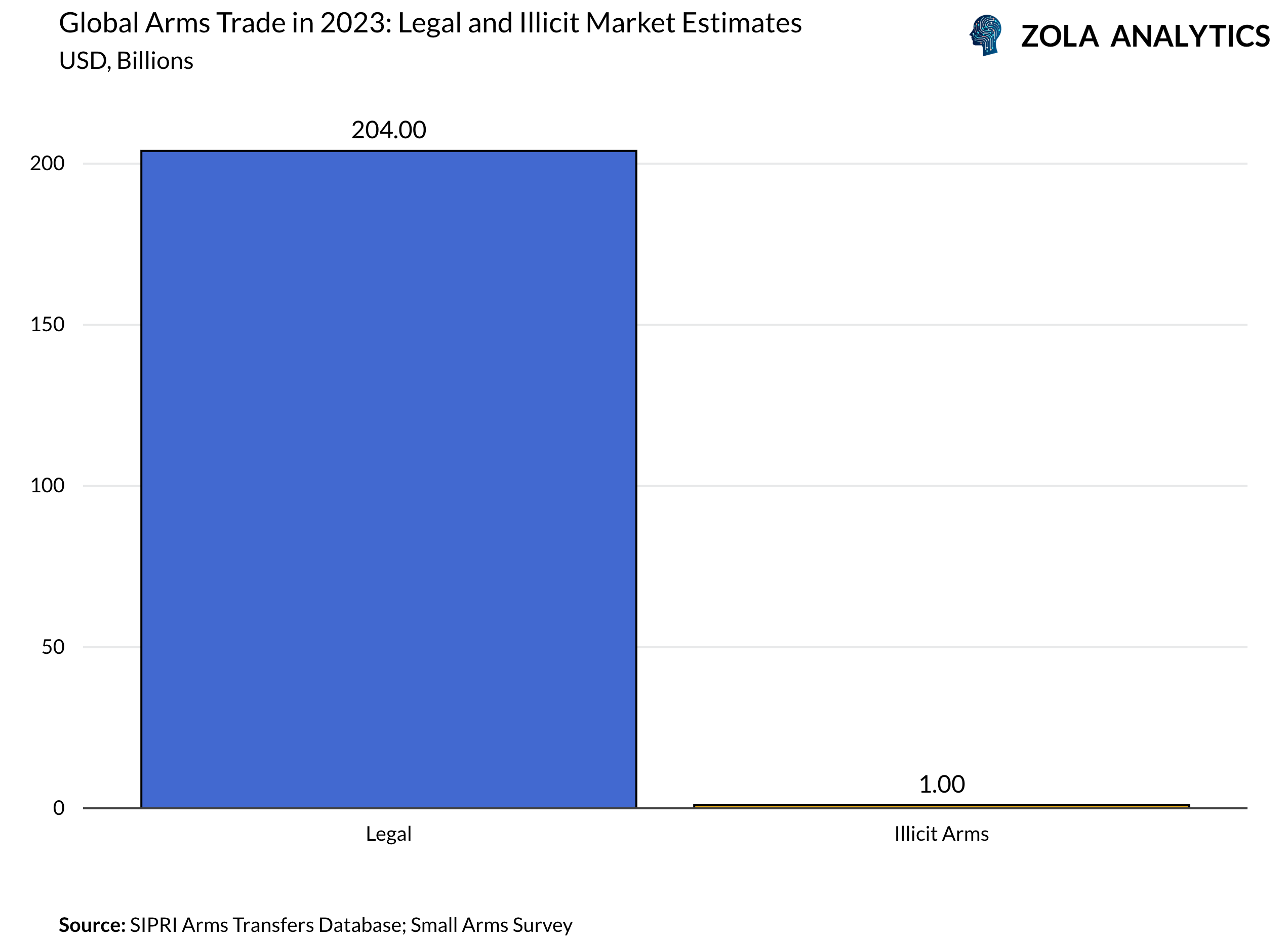

This formal market sees an estimated USD 138 billion in arms exchanged each year, making it a pillar of global trade — one that provides security for some and strategic leverage for others.

Corporate Firepower: The Arms Titans

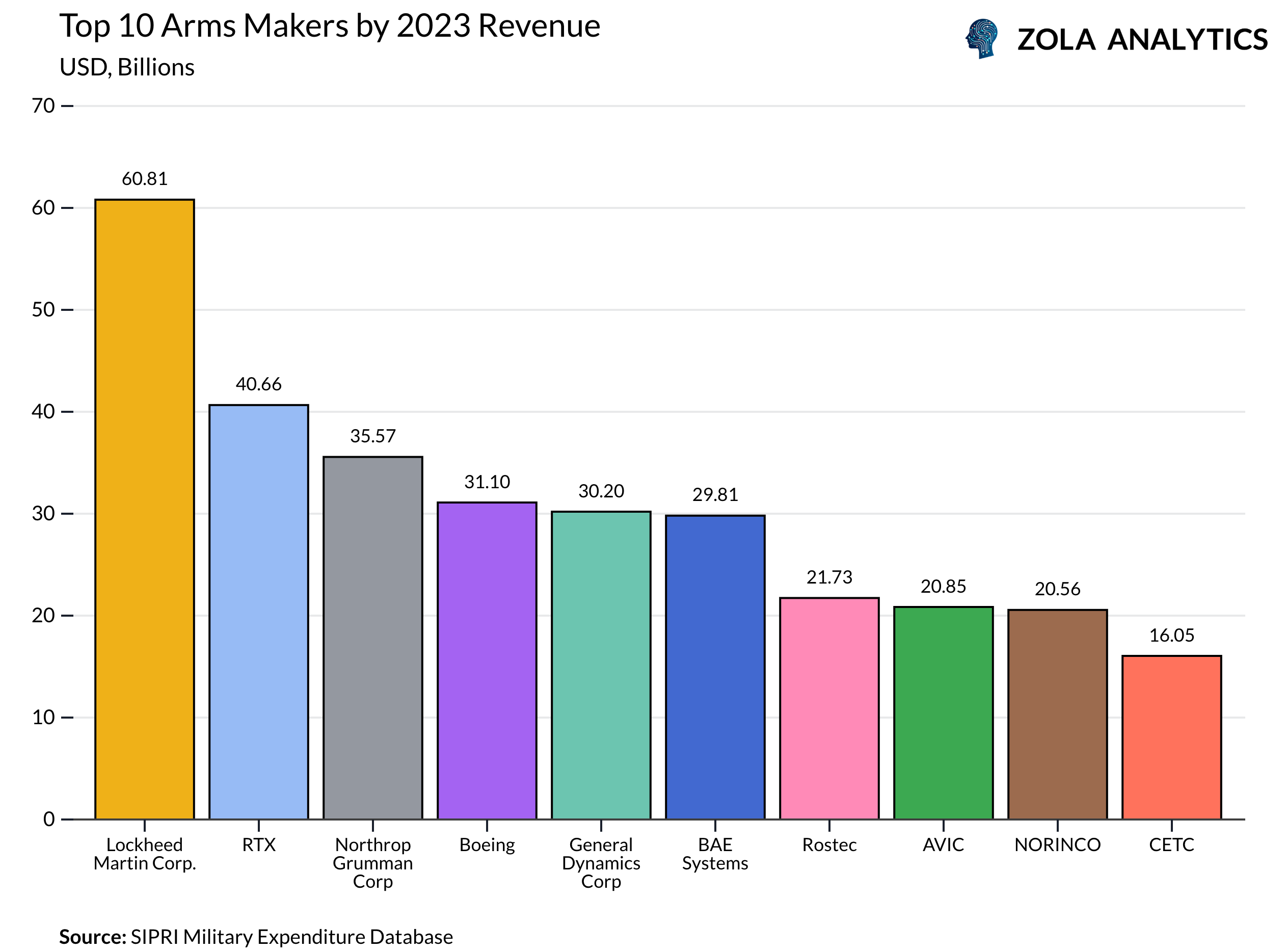

If countries are the arms dealers, then defence corporations are the manufacturers and profiteers. In 2023, the top 100 arms companies sold USD 632 billion worth of weapons and military services — a revenue stream that exceeds the GDP of many nations (SIPRI).

American firms dominate this landscape, occupying four of the top five spots. In fact, half of the world’s 20 largest arms makers are U.S.-based. These companies form the backbone of the military-industrial complex, raking in nearly USD 196 billion in U.S. military revenue in 2022 alone.

Their success stems from a guaranteed customer: governments. U.S. defence contractors receive over 70% of their revenue from public defence contracts (Echols, 2023). This tight embrace between state and supplier means taxpayer dollars fuel private profits — creating an economic ecosystem dependent on sustained military spending.

Not surprisingly, their fortunes rise with global conflict. Stock prices and order backlogs typically surge during wars, such as in Ukraine. From an economic standpoint, these firms are as strategically important to the U.S. as big oil or big tech — supporting jobs, innovation, and industrial exports.

Defence Dollars and National Budgets

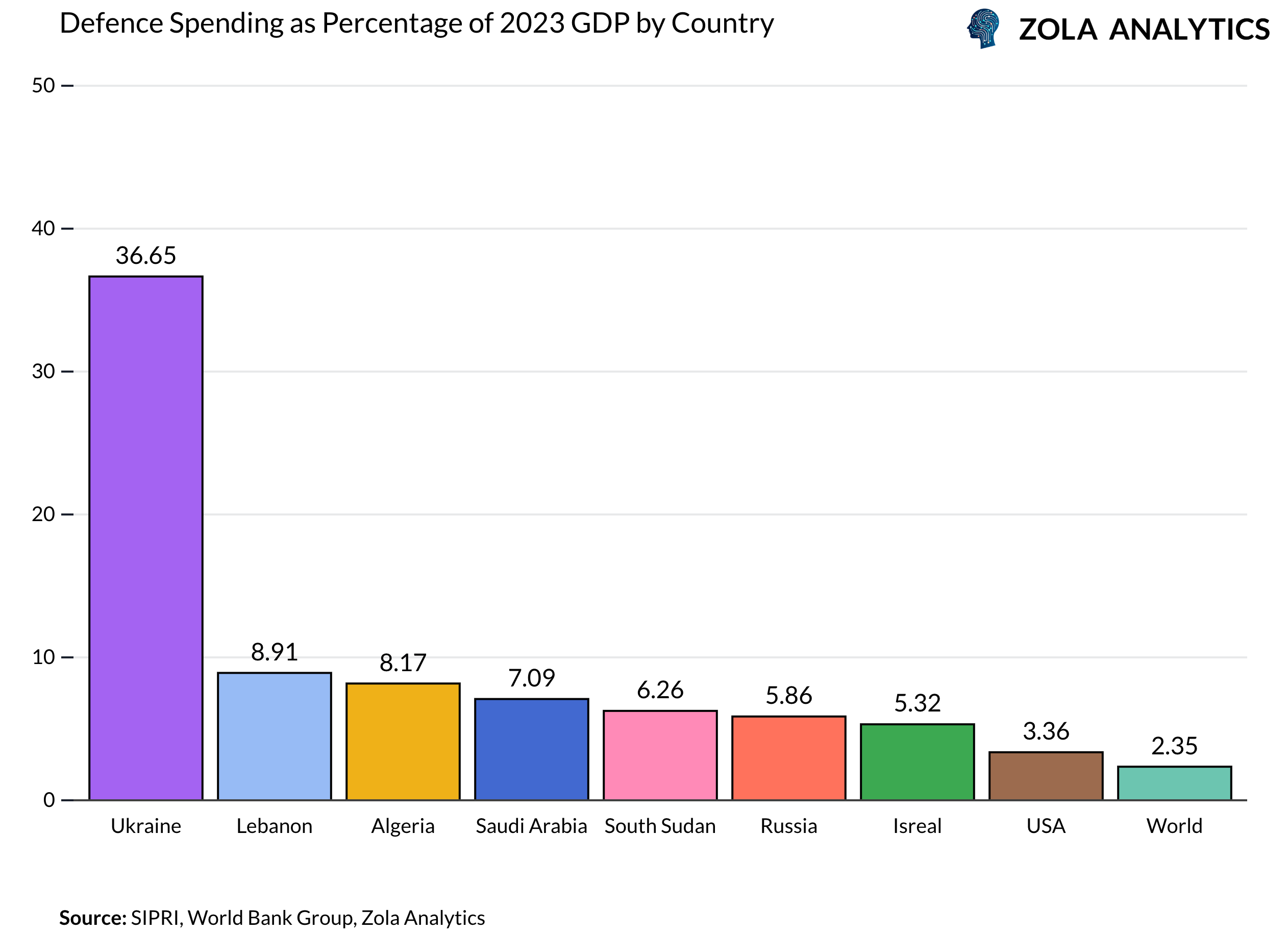

Governments often justify arms spending in terms of security — but it's also an economic decision. With military expenditure reaching an all-time high of USD 2.44 trillion, defence is reshaping national budgets, reflecting a belief that economic security flows through military strength.

Defence industries generate jobs, drive R&D, and boost exports. But the trade-off is stark: every dollar spent on tanks is a dollar not spent on infrastructure, healthcare, or education. In macroeconomic terms, the gun economy is a double-edged sword — providing short-term stimulus while potentially crowding out long-term investment in other productive sectors.

Still, the political will to spend on arms continues to grow, as countries double down on military readiness and bet that firepower will secure prosperity — or at least survival.

Economies Addicted to Arms Production

Weapons aren’t just tools of war — they are export goods, and some countries are now economically dependent on producing and selling them.

Israel offers a striking example: nearly 20% of its merchandise exports are weapons, a significant slice of its high-tech economy. In Russia, France, and the U.S., arms exports account for 2–3% of total exports — a small percentage in relative terms, but tens of billions of dollars in absolute value.

The economic entrenchment runs deeper still. In the U.S., defence contracts account for 10% of total manufacturing demand, supporting entire supply chains, regions, and towns (ClearedConnections). Similar patterns exist in other major exporters, where arms production provides skilled jobs and regional economic lifelines.

This isn’t just an industry — it’s an embedded part of national economies, linking GDP, employment, and foreign policy.

The Shadow Arms Market

Beyond the official arms trade lies a thriving illicit market, valued at USD 1 billion annually—a fraction of the USD 204 billion legal trade, but with an outsized impact. These weapons bypass state controls and flow directly to insurgents, militias, terrorist groups, and organised crime networks. In fragile states, even modest volumes can destabilise entire regions, tipping power balances, prolonging conflicts, and undermining governance. The UN has linked illicit small arms to up to 90% of conflict deaths in certain areas. Unlike regulated sales, these weapons often circulate indefinitely, amplifying violence long after the initial transaction. In effect, each dollar spent on illicit arms yields exponentially greater systemic risk than its legal counterpart.

This dependency creates a perverse incentive: when an industry of such scale and reach relies on continuous demand, disarmament starts to look economically risky. Indeed, conflict drives business – for instance, defenCe contractors saw sales jump over 4% in 2023 largely due to the wars in Ukraine and. In such an environment, the incentive structure skews toward ever more spending and new “next-gen” weapons, ensuring the arms assembly lines keep rolling and profits stay protected.

Guns, Growth, and the Cost of Conflict

This dependency creates a perverse incentive: when a trillion-dollar industry sustains millions of jobs and props up national budgets, disarmament starts to look like an economic liability. Conflict drives business — defence contractors saw sales rise over 4% in 2023, fuelled by wars in Ukraine and broader geopolitical tensions. In this environment, the system is wired for escalation: more spending, more contracts, and a relentless push for “next-gen” weapons to keep the demand machine running.

Breaking the grip of the gun economy will take more than diplomacy — it demands a reimagining of how nations pursue security and growth. Until then, weapons will remain not just instruments of war, but engines of profit, power, and policy. And the arms race, far from being a relic of the past, is still booming — literally.