Published 24th October 2025

6 minute read

A New Golden Age

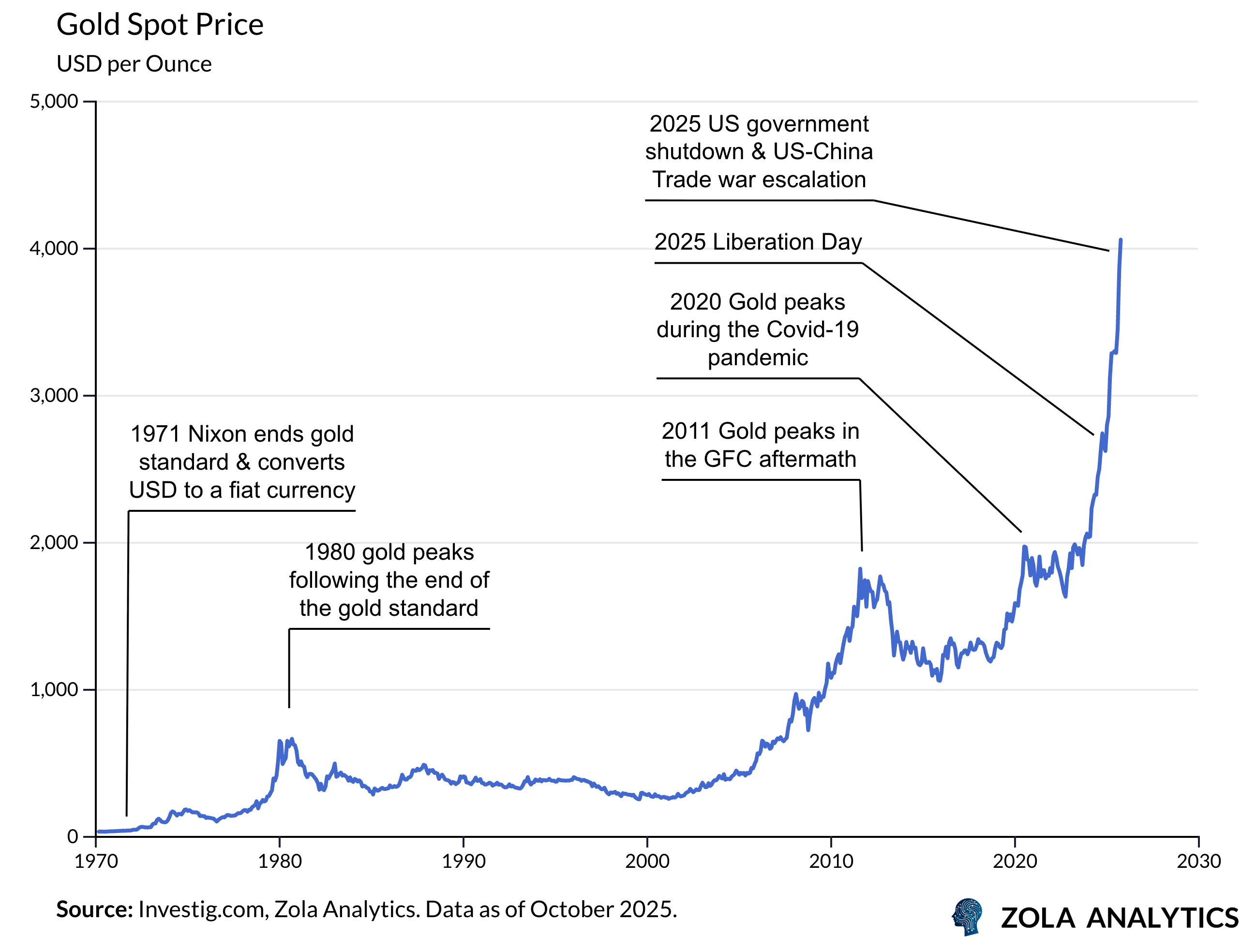

Since antiquity, gold has been an object of fascination. The breathtaking rally of 2025, with prices up more than 55% year to date, shows that the metal has not lost its lustre. What began as a slow grind higher turned into one of the most powerful moves in decades, driven by overlapping waves of official and private demand. In this week’s edition of the Zola Chartbook, we dissect the drivers of gold’s rise, and examine its sudden reversal.

The Classical Drivers

Gold’s supply changes slowly. The total stock of above-ground gold increases by only about 1-2% each year, since new mining adds little to what already exists. As a result, gold’s price depends far more on shifts in demand than on changes in physical supply.

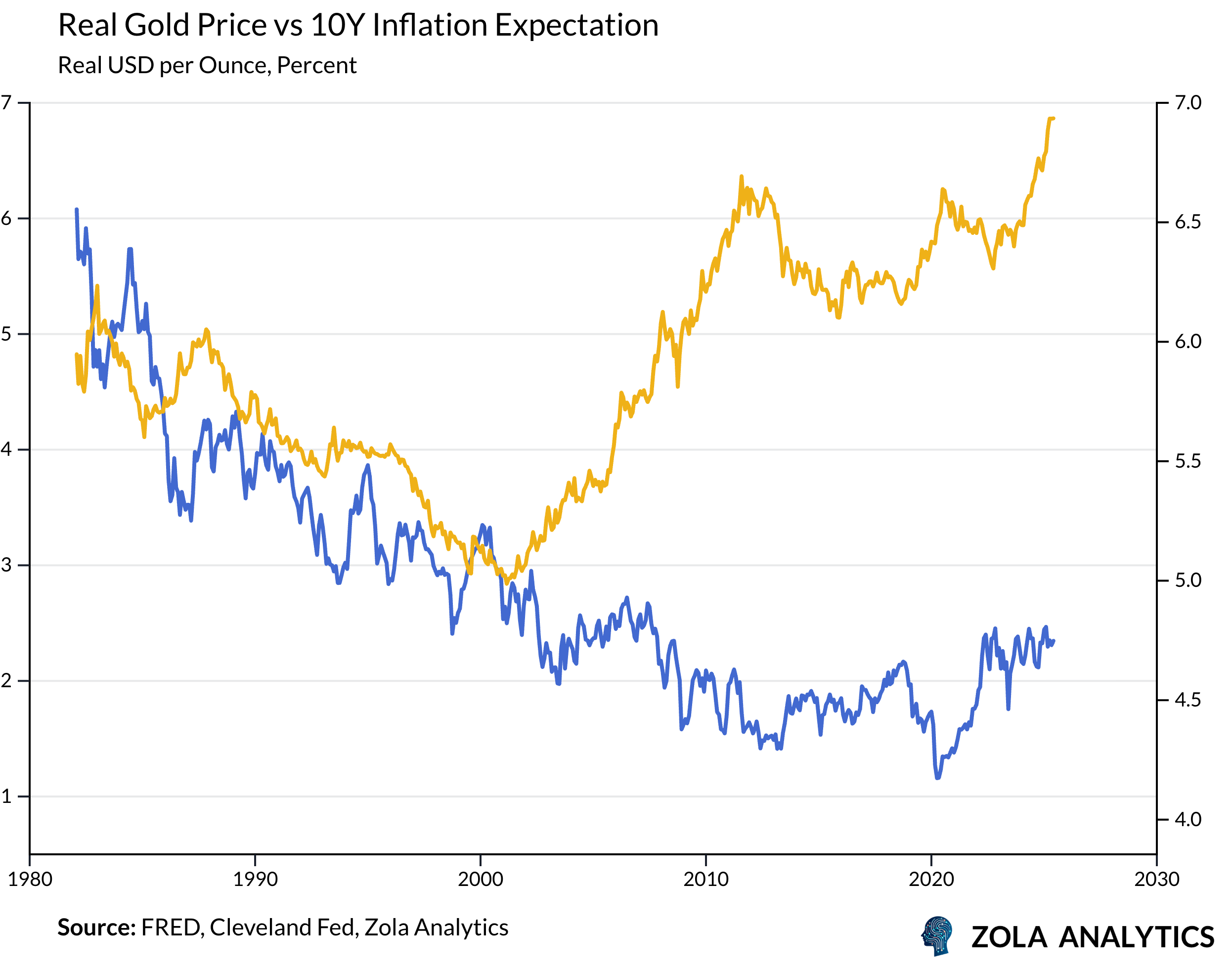

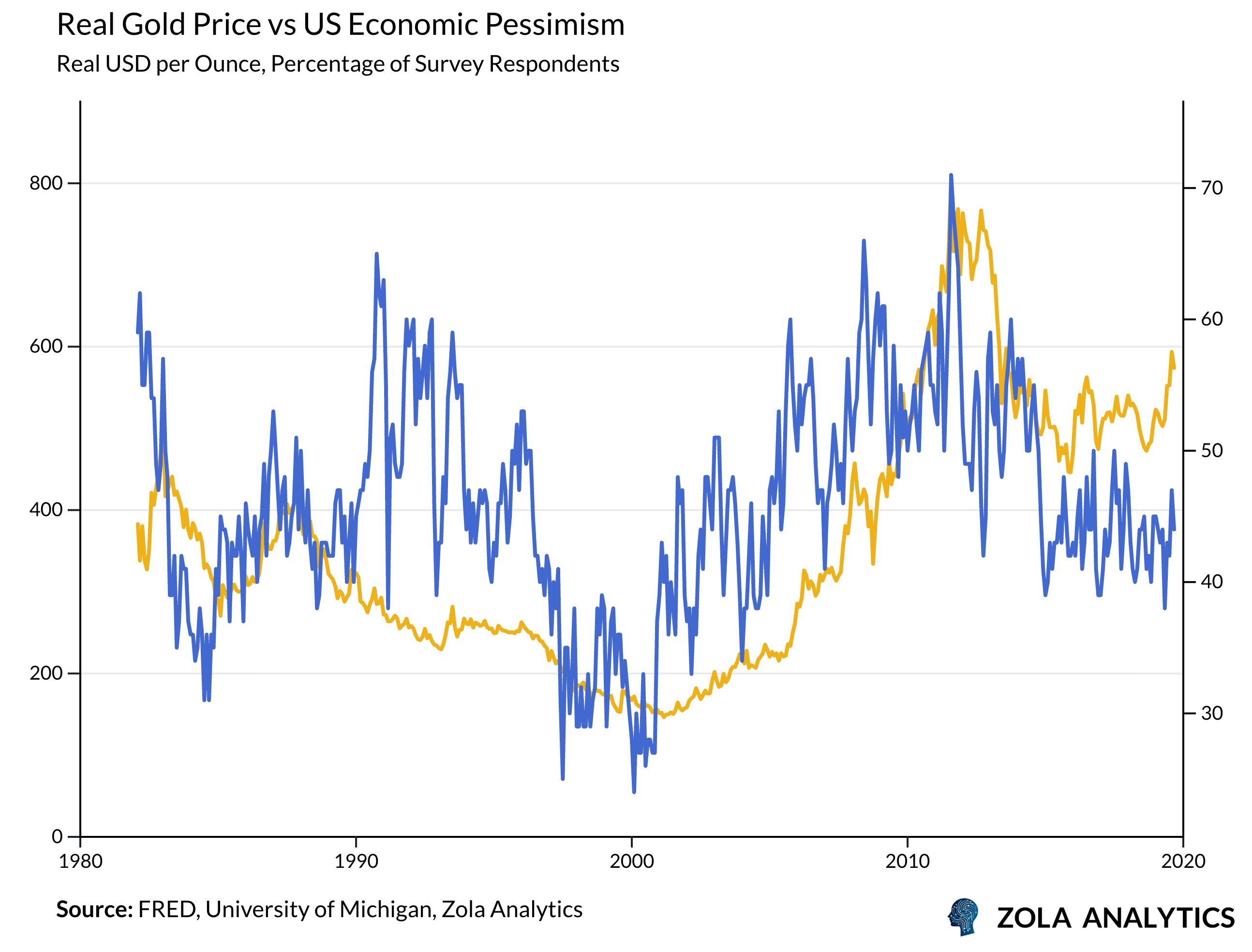

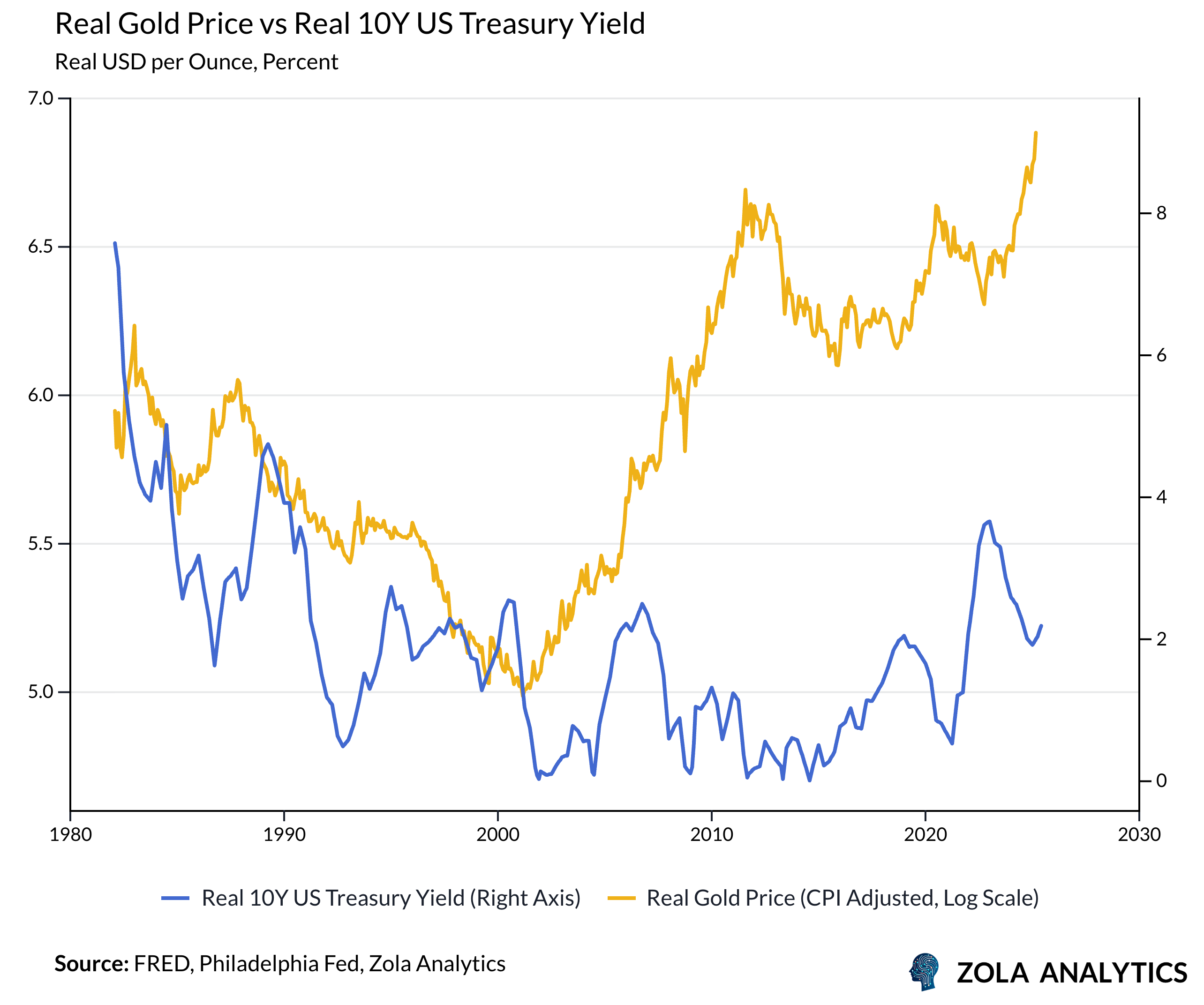

For half a century after gold was freed from its dollar peg in 1971, economists and investors have returned to the same three variables when trying to explain its movements: inflation expectations, uncertainty, and real interest rates.

When inflation expectations rise, investors reach for gold as a store of value. From 1970-1990, this was a key influence on gold prices. During periods of low and stable inflation, such as 1990-2020, the relationship is much weaker.

In bad times, when pessimism and uncertainty abound, gold has been a refuge for investors. When investors doubt growth or fear policy failure, they shift toward assets that feel permanent.

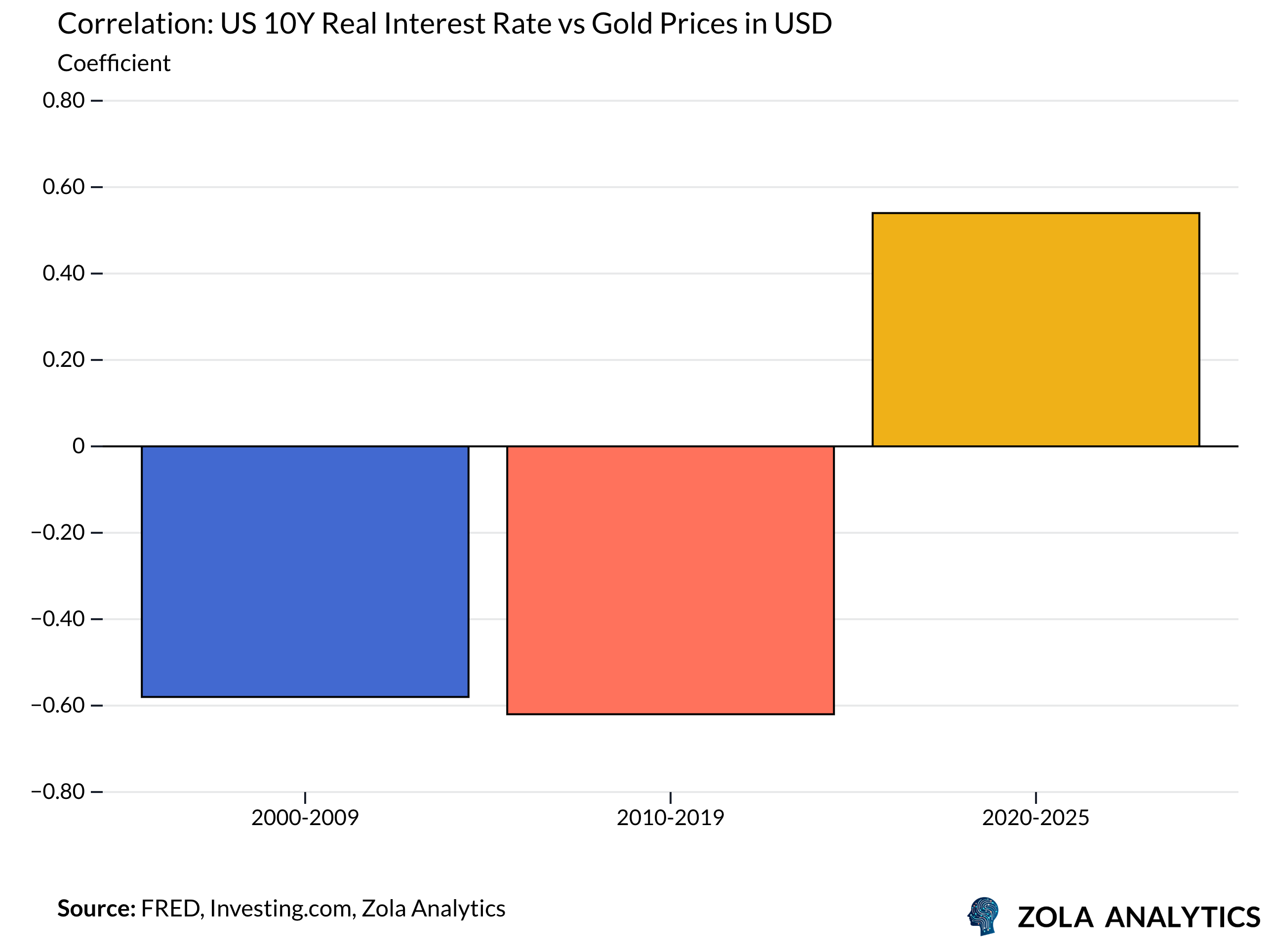

Real interest rates represent the opportunity cost of holding a non-yielding asset. Gold tends to rise when real yields fall, since the trade-off between holding gold and earning real income elsewhere narrows.

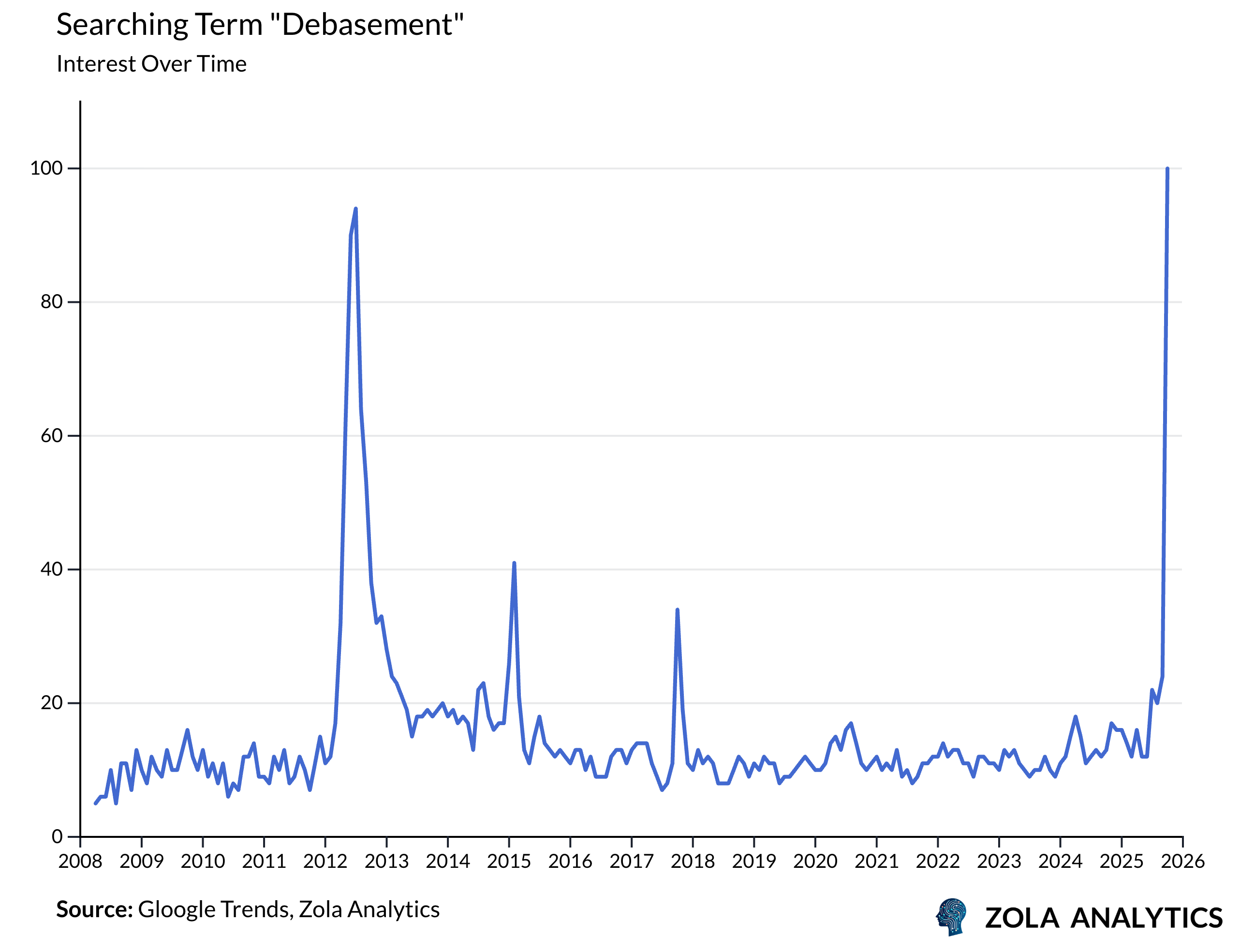

Each of these traditional drivers has shifted profoundly in recent years. The post-pandemic period brought the first sustained inflation shock in a generation, eroding confidence in central banks’ control of price stability. Even as inflation cooled through 2024 and 2025, expectations of higher prices remain embedded in investor psychology. At the same time, the fragile fiscal position of major economies, strained by pandemic spending and rising debt service costs, has revived public concern about monetary debasement.

In contrast, the classical relationship between gold and real interest rates has broken down. Historically, rising real yields signalled confidence in growth and tighter monetary policy, conditions that tended to weigh on gold. In the 2020s that relationship weakened. Real yields increased not because the world felt safer, but because governments issued vast quantities of debt and investors demanded greater compensation to hold it. Higher real rates reflect higher risk, not growth.

The common denominator is pervasive uncertainty deepened. Geopolitical tension, economic fragility, and social instability have all risen since 2020. In this environment of high uncertainty and low trust, gold shines.

From Fear To FOMO

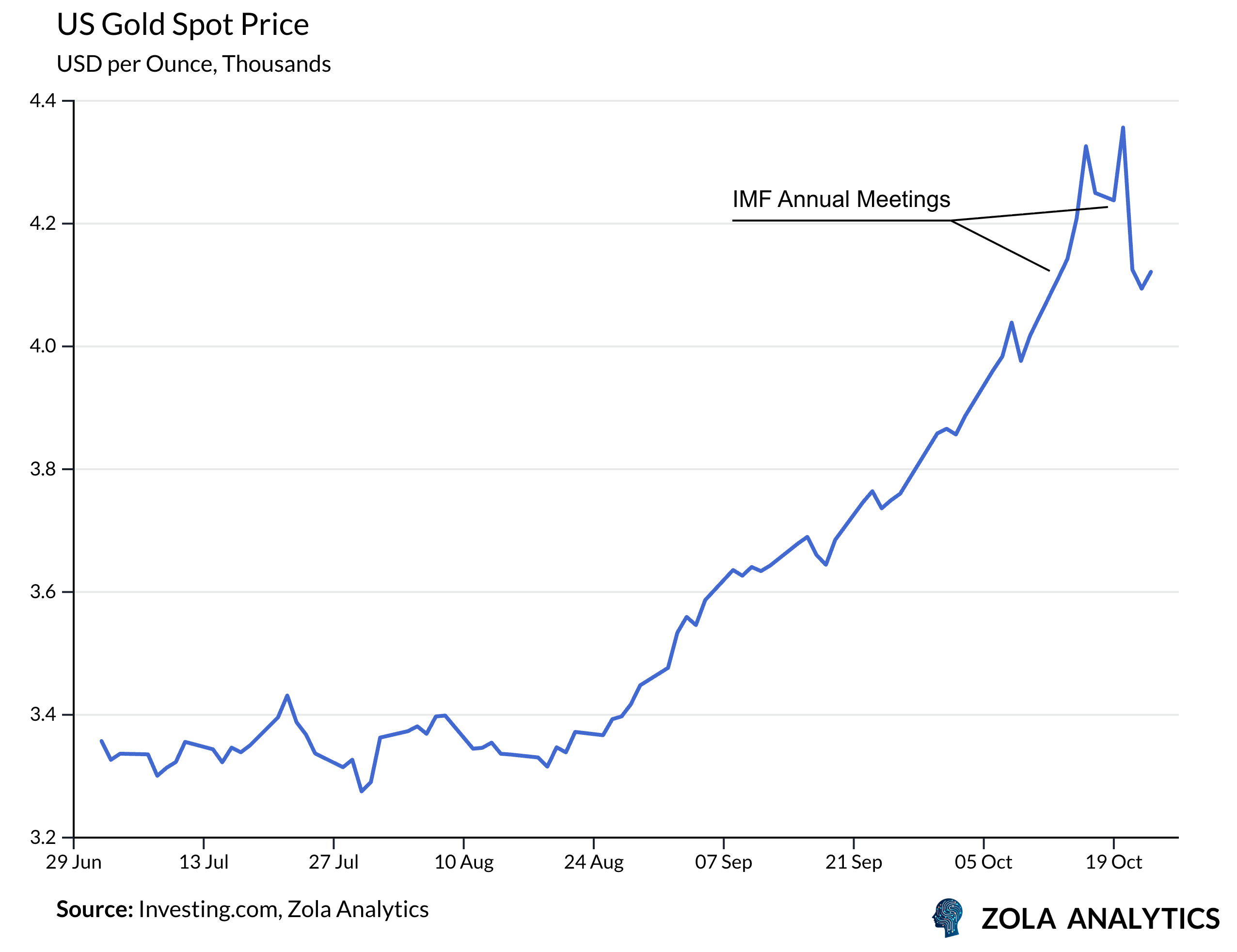

In 2025, the rally accelerated. A series of overlapping demand shocks saw gold’s price rise to an October peak of about $4,350 per troy ounce. Part of this reflected the forces we have already discussed. What changed this year was the mix and scale of buyers, and the channels through which demand reached the market.

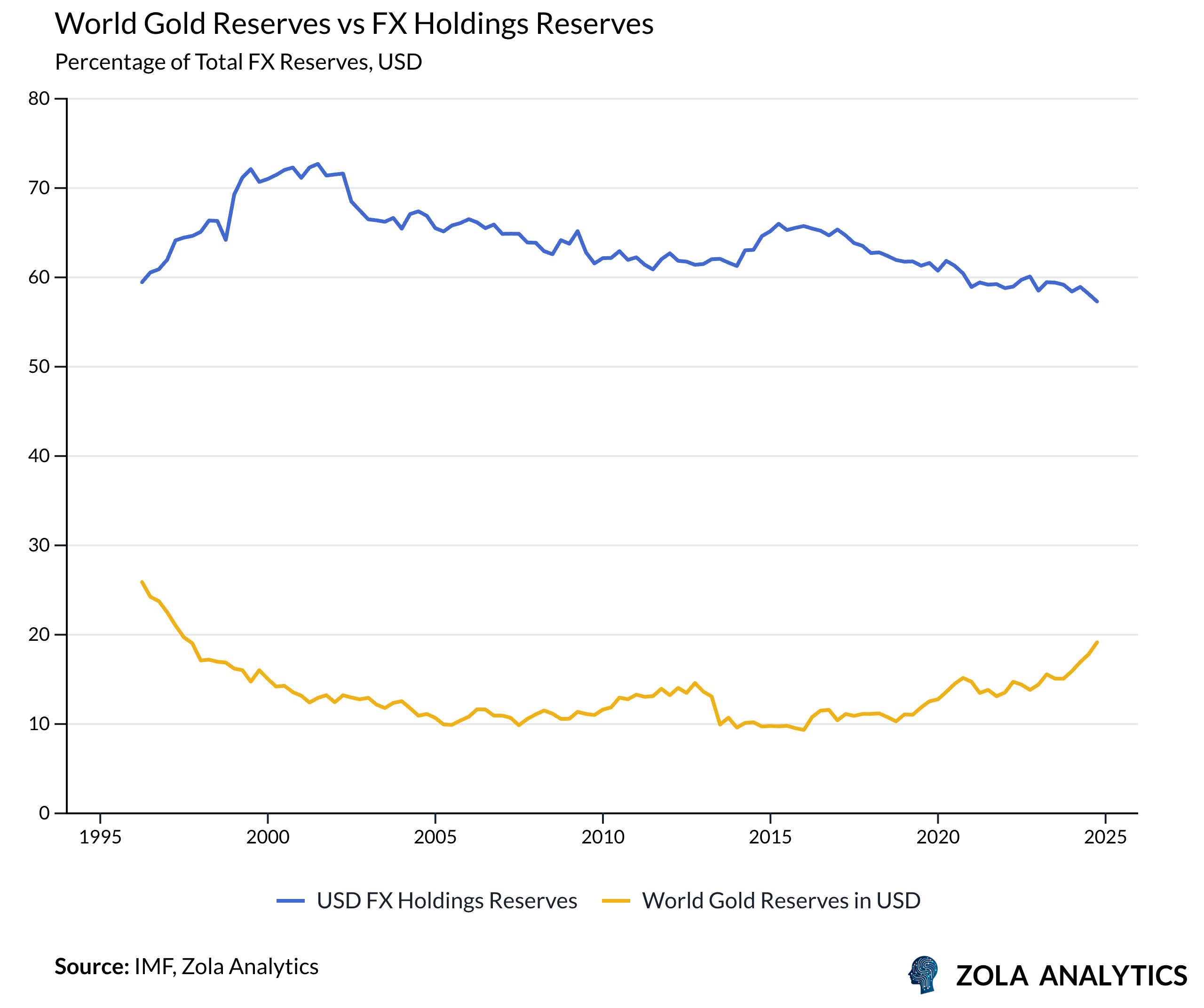

Accumulation by price-insensitive central banks has anchored demand. Reserve managers raised their gold allocation to cut sanction and settlement risk. Whilst the dollar remains the dominant reserve asset, desire to diversify has led to an increased demand for gold, given gold is the only widely accepted reserve asset with no counterparty. This is evident in the declining share of foreign reserves held in dollars and in the steady rise of reported gold holdings, with emerging markets leading the increase.

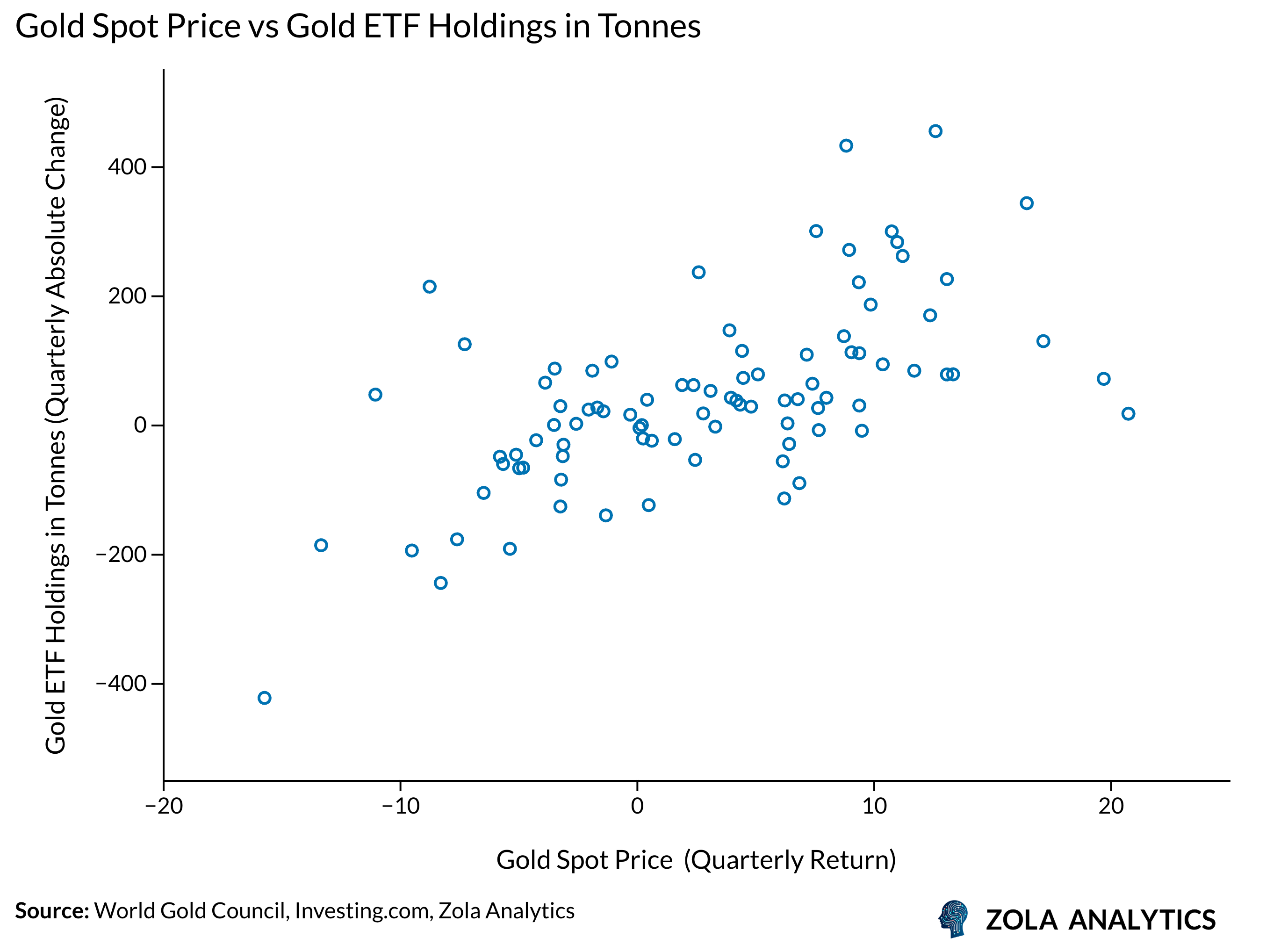

Another major change in the gold market has been financialisation. Gold is no longer just a physical market. ETFs and other wrappers have turned it into a liquid, frictionless exposure that can be scaled instantly.

In 2025, that mattered. The search for diversification revived as correlations across asset classes rose and bonds lost much of their defensive value. Investors who once relied on duration to offset equity risk now found few reliable hedges left. Gold ETFs offered a simple substitute: they trade like equities but behave differently. Flows were amplified by momentum, as rising prices validated the allocation case and drew in more capital. What began as cautious diversification turned into self-reinforcing demand, channelled through financial vehicles that make portfolio insurance as easy as buying an index fund.

Losing Its Shine?

This month, after an eighteen-month ascent, gold suffered a reversal. The October correction followed a subtle but important shift in tone around the IMF meetings. Global policymakers projected renewed confidence in managing inflation and debt, undercutting the narrative of persistent monetary erosion that had driven the rally. Even without major moves in yields or the dollar, the change in story was enough to trigger profit-taking and de-risking across a crowded trade.

Several emerging-market central banks paused purchases after two years of record accumulation, either to manage optics or to rebalance reserves after sharp valuation gains. With that anchor bid temporarily absent, the market became more sensitive to shifts in investor sentiment and liquidity. Positioning amplified the move. ETF holdings and speculative futures positions were elevated after months of steady buying, leaving the market vulnerable to even small narrative shifts. As sentiment turned, systematic and macro funds reduced exposure, triggering a wave of mechanical selling across futures and ETFs.

Hedging assets rarely deliver strong returns. Insurance pays out in crisis, not in calm, and gold is no exception. After large rallies, its real returns have historically been low or negative for several years as fear subsides and positioning normalises.

Even so, the underlying drivers of the bull market remain largely intact. The fiscal and geopolitical backdrop that lifted it has not changed, and new sources of demand may yet emerge. What follows will depend less on sentiment than on whether these trends endure.

Sign up to receive the Zola Global Macro Chartbook every week: https://www.zolaanalytics.com/insights?signUp