Published August 14th 2025

3-min read

Growth Beat With Momentum Set To Ease

Growth above potential but reliant on temporary supports

Government offset soft private demand

Early-year boosts from tariffs and taxes have faded

Labor market and investment momentum weakening

Trend growth near 0.3% caps acceleration

Front loading defined the year’s start. Tariff timing and the April stamp duty deadline pulled activity into Q1 before partially unwinding in Q2. GDP rose 0.3% QoQ in Q2, and even with that drag, H1 growth averaged about 0.5% QoQ, above the UK’s estimated potential pace of roughly 0.3% QoQ. By that measure, Q2 was solid.

What Drove Q2 Growth

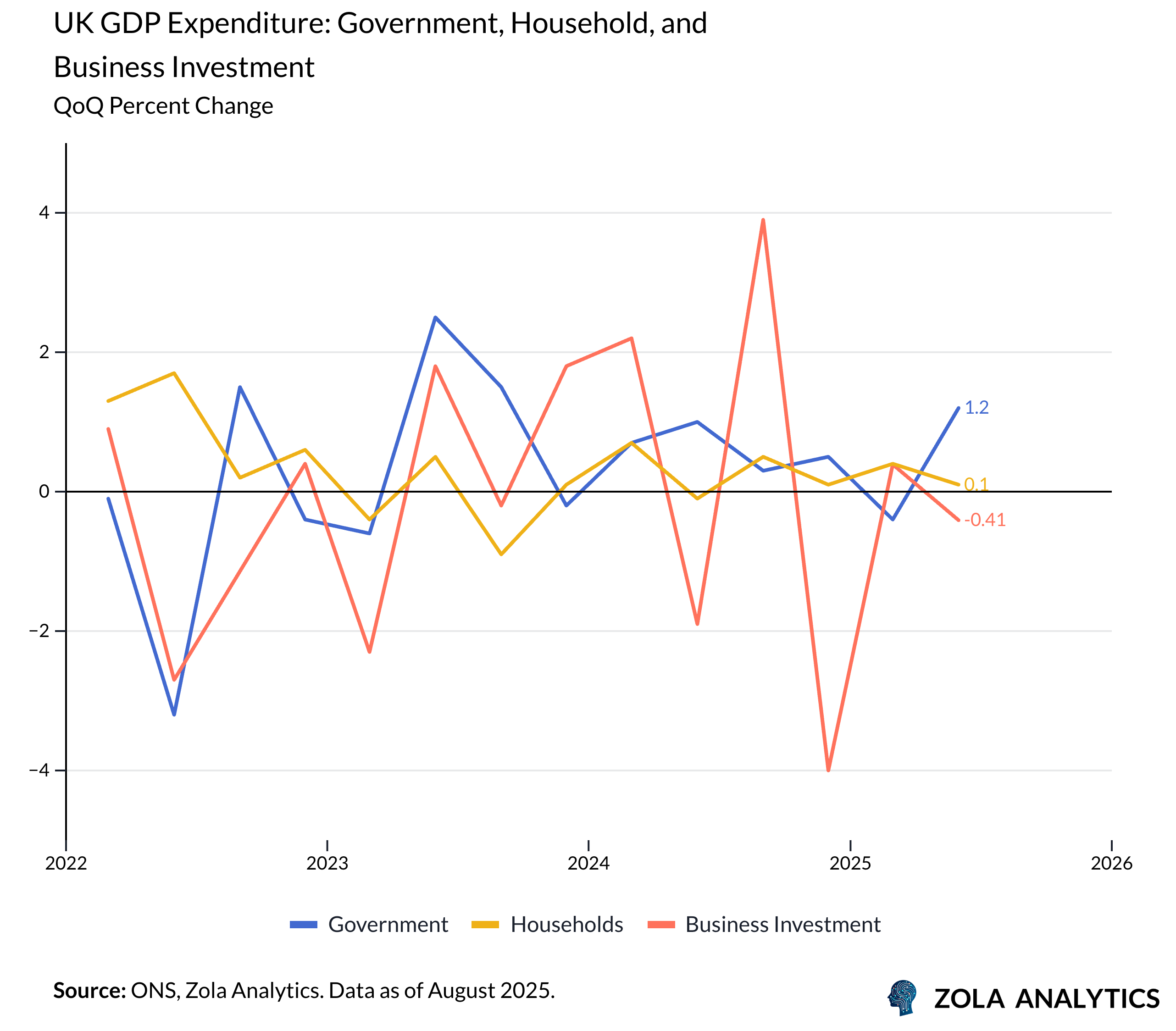

Government consumption increased 1.2% QoQ and contributed roughly 0.3 pp to growth, reflecting temporary items such as vaccination volumes. June showed manufacturing up 0.5% MoM and services up 0.3% MoM, including a small lift from electronics linked to defence orders. Private-sector breadth remained limited. Household consumption rose 0.1% QoQ, a soft outturn for core demand. Business investment fell 4% QoQ, payback after a strong Q1.

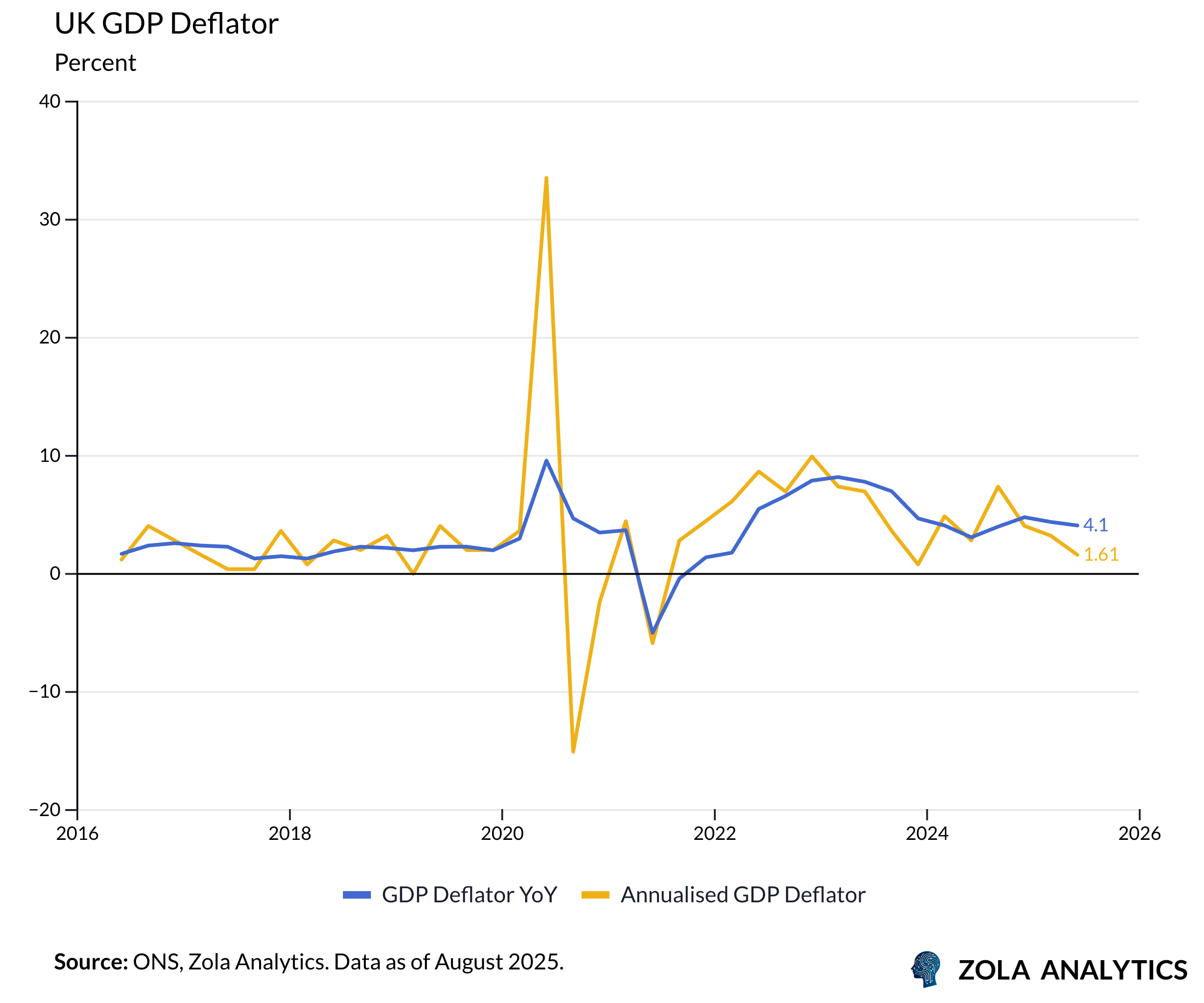

The GDP deflator cooled to an annualised pace near 1.6% in Q2, with the YoY rate still close to 4%. That mix helps headline real growth, yet it does not resolve the split between public-sector support and soft private-sector impulse. It also feeds into the policy debate over how quickly to normalise rates.

Short-Term Versus Structural Forces

Short-term supports fade in the second half. The Q1 tariff front running and April deadlines have already washed through. Some of June’s pop likely pays back in July and August. Investment intentions have softened and hiring has cooled, with payrolled employment falling in most recent months. These near-term forces lean against a sustained reacceleration.

Structural constraints persist. Potential growth has slowed compared with pre-2007 norms, with post-crisis scarring and Brexit frictions curbing supply capacity and trade intensity. In this world, 0.3% quarterly growth is no longer tepid. It sits near cruising speed in a supply-constrained economy. Growth north of that mark risks reigniting price pressure unless supply expands.

What To Expect Next

Markets will parse the upside surprise for signals on the Bank of England. The mix argues for caution. Policymakers remain focused on inflation and the labor market rather than headline GDP. Softer deflators in Q2 help, yet underlying private demand slowed and the jobs backdrop deteriorated. Hawks may point to above-potential H1 growth. Doves will stress the composition and the risk that H2 growth reverts back to sub-trend.

Expect a weaker flavour to H2 prints as June strength unwinds, fiscal consolidation bites, and fixed-rate mortgage resets keep a lid on discretionary outlays. A modest gain in Q3 is plausible, roughly in line with survey signals, with risks skewed by upcoming inflation and labor data. Rate cut timing hinges on those releases, not on a single GDP print.