Published July 18th 2025

Glass Three-Quarters Empty

Labour Market: The Recession Has Arrived

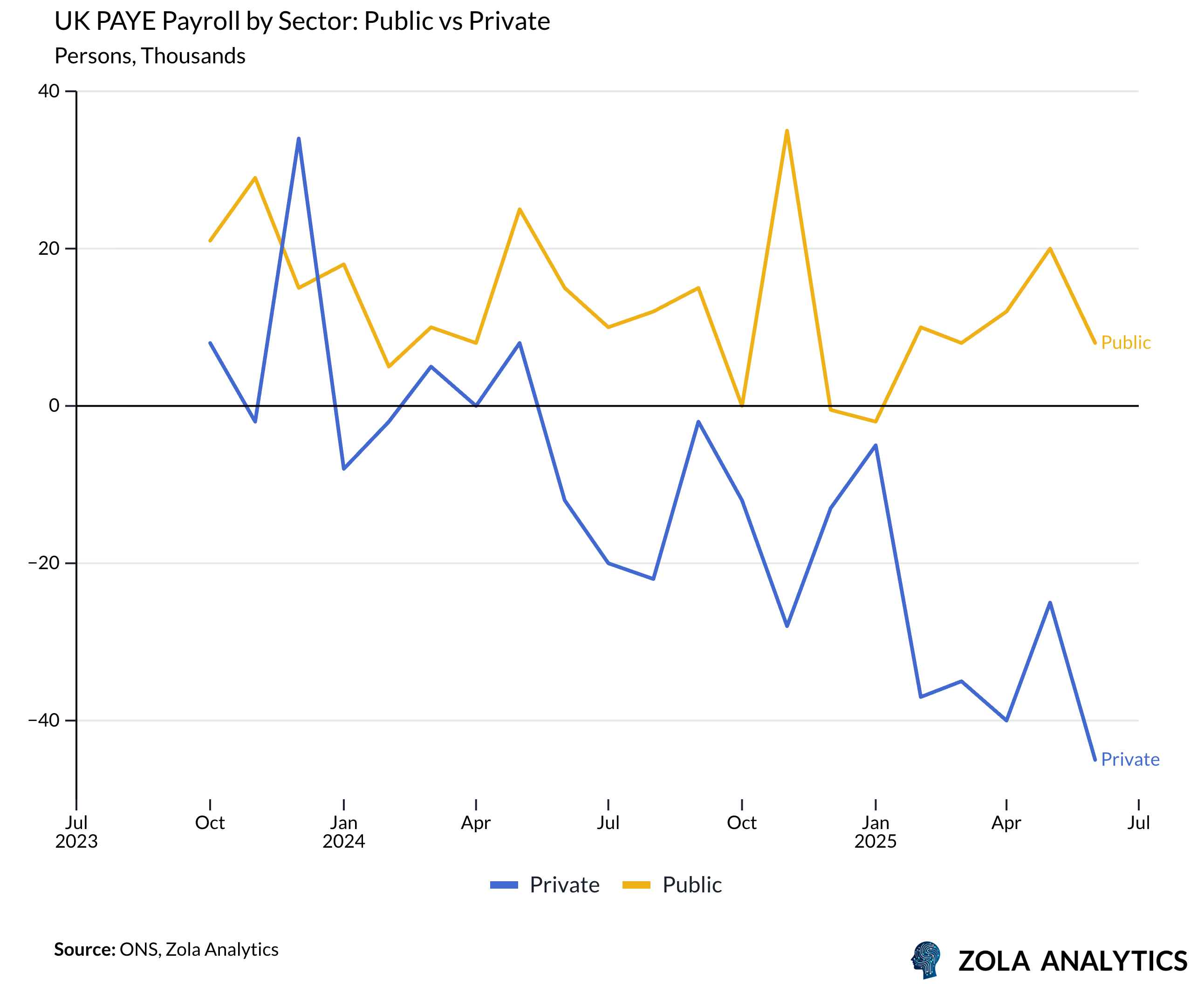

UK labour market data confirm a clear deterioration. Payroll employment fell by 41,000 in June, marking the fifth consecutive monthly decline. While May’s initially alarming 109,000 drop was revised to 25,000, the underlying trend remains unmistakable: the jobs market is stagnating and likely contracting.

The split between public and private sector employment is stark. Private-sector payrolls have been falling consistently since mid-2024, while the public sector continues to add jobs at the margin. Headline stability is masking the reality: the economy’s growth engine—the private sector—is in reverse. Cyclical industries such as hospitality, retail, and construction show accelerating job losses.

The unemployment rate has climbed to 4.7%, exceeding the BoE’s Q2 forecast, while vacancies are shrinking at an annualised 26% pace on a three-month basis. Hiring intention surveys reinforce the picture of a demand freeze. Redundancies remain limited for now, but history suggests that once job cuts gain momentum, they rarely reverse without policy intervention.

Crucially, labour market slack is feeding through to wages. Private-sector regular pay growth has cooled to 4.9% YoY, down from 6.3% six months ago, undershooting the BoE’s expectations. This easing in wage pressure addresses one of the central bank’s primary inflation concerns.

The Times captured the mood with its headline: “Bank of England could cut rates if job market slows down.” Based on the latest data and recruiter surveys, that slowdown is already here.

Inflation: Seasonal Stickiness, But Trend Is Down

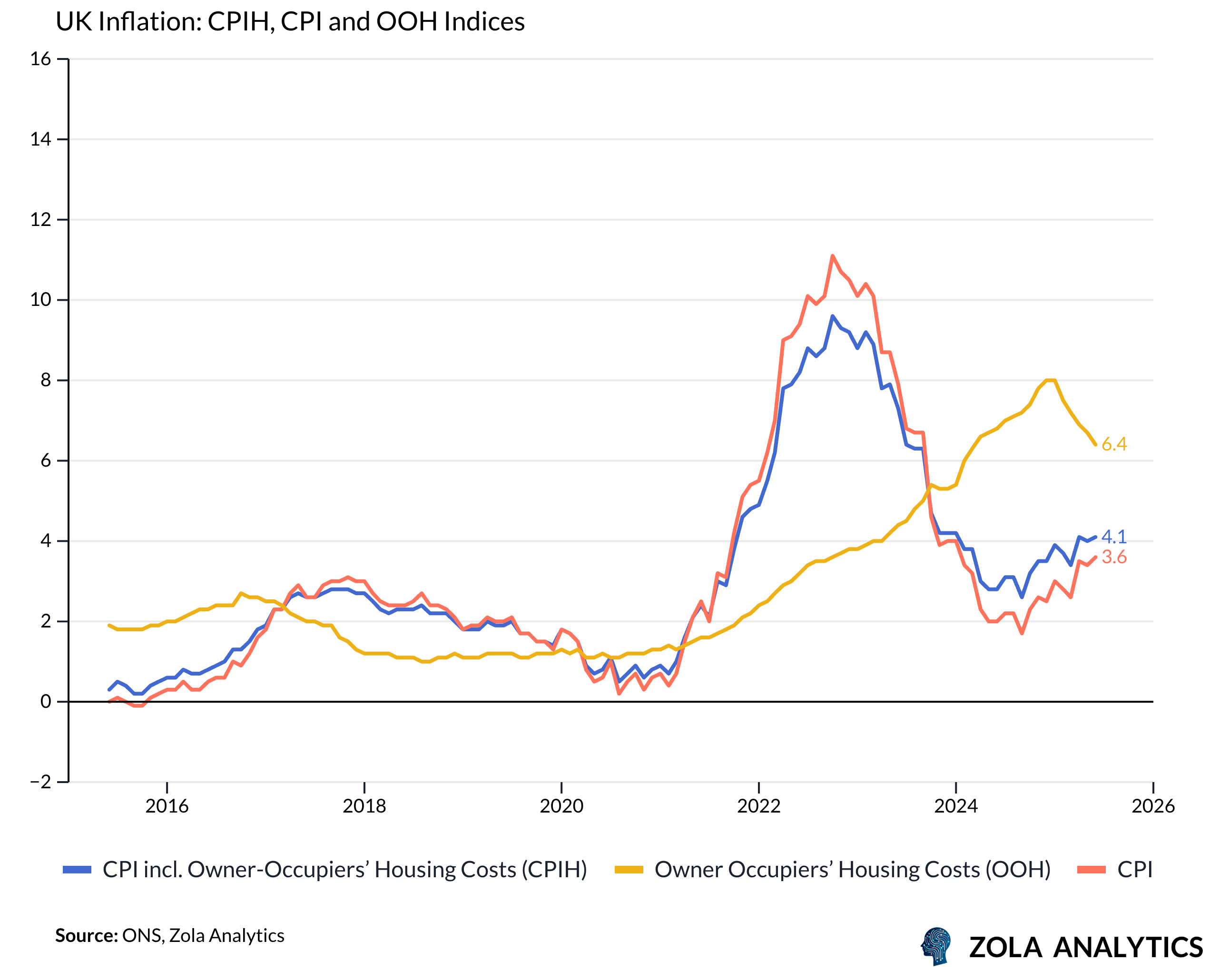

Headline CPI rose to 3.6% YoY in June, prompting concerns about renewed inflation risks. However, the drivers are largely seasonal and temporary—a surge in transport costs from peak holiday travel and base effects from fuel price movements. These do not signal persistent inflation.

The medium-term outlook remains disinflationary:

Housing: New-let rental growth is running well below official CPI measures and will feed through gradually, reducing housing contributions ahead.

Energy: EDF price cap forecasts point to a sharp disinflationary impulse from Q4.

Food: Global price trends in GBP suggest food inflation is near its peak.

Transport: Contributions will stay high through summer but fade quickly thereafter.

If oil prices hold near current levels, inflation may stay above target through year-end but should fall sharply from early 2026, driven by energy, food, and softer housing costs.

Policy Outlook: Rates Likely to Fall Further Than Markets Expect

The BoE faces a dilemma: headline inflation remains above target, but labour market conditions are deteriorating faster than expected. Rising unemployment, falling vacancies, and slowing pay growth signal a rapid increase in slack, reducing underlying inflation risk.

Against this backdrop, an August rate cut now looks highly probable—and likely the first step in a deeper easing cycle than markets currently expect. Pricing reflects a modest pace of cuts, but if current trends persist, policy rates may need to fall much further and faster, with employment stress—not inflation—becoming the dominant policy driver through 2026.

Disclaimer: Zola Analytics provides this material for informational and entertainment purposes only. It does not constitute investment advice.