Published June 25th 2025

Can Chile’s White Gold Shine Again?

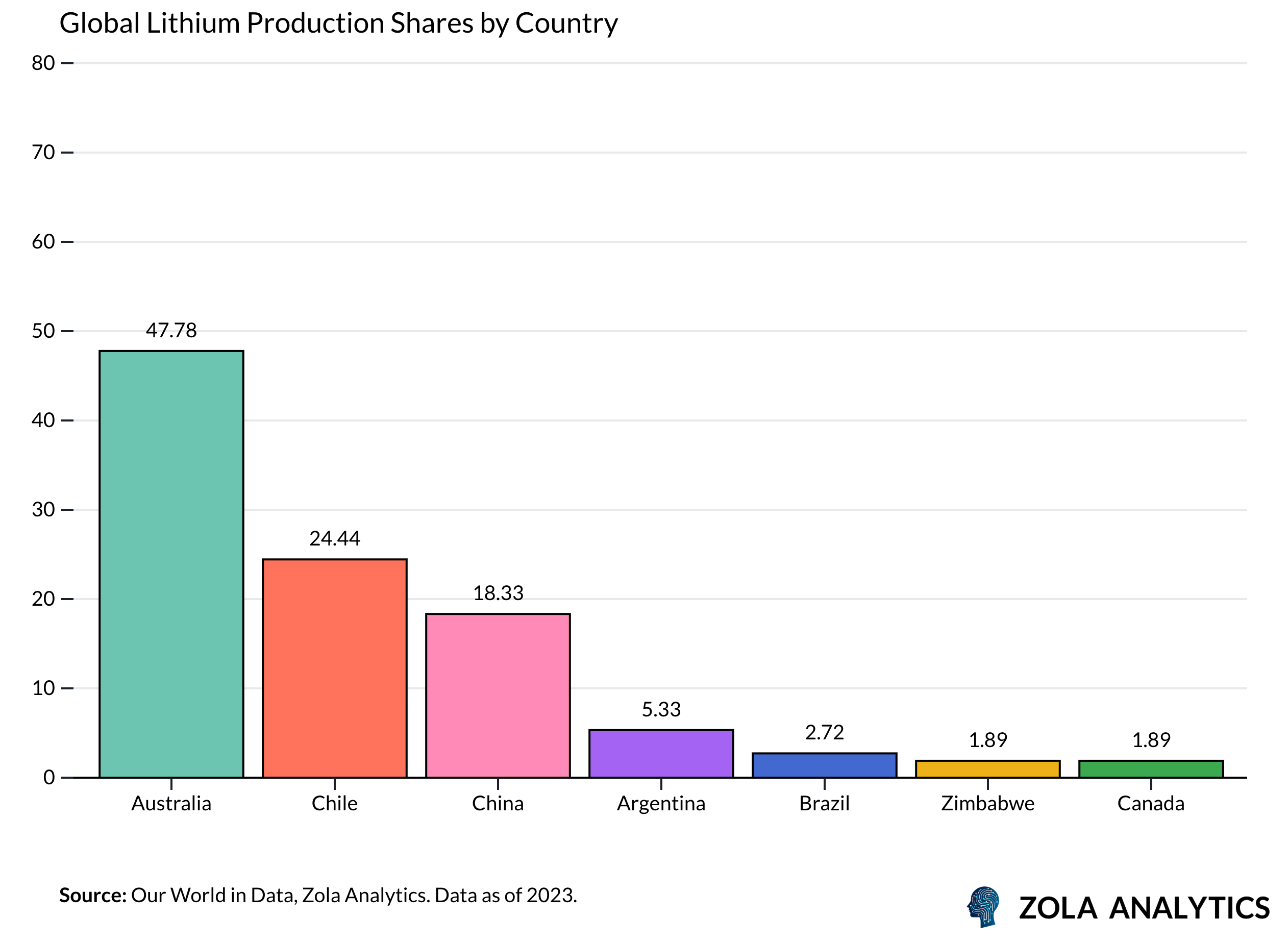

As the energy transition accelerates, lithium has emerged as a cornerstone of the new industrial era. Chile, home to the world’s largest lithium reserves, sits at the epicentre of this transformation. Yet, its position is complicated by evolving global demand, domestic politics, and rising competition—especially from neighbours like Argentina. Chile’s recent National Lithium Strategy brings new urgency to this dynamic.

Demand Dynamics: EV Boom Meets Cyclical Soft Patch

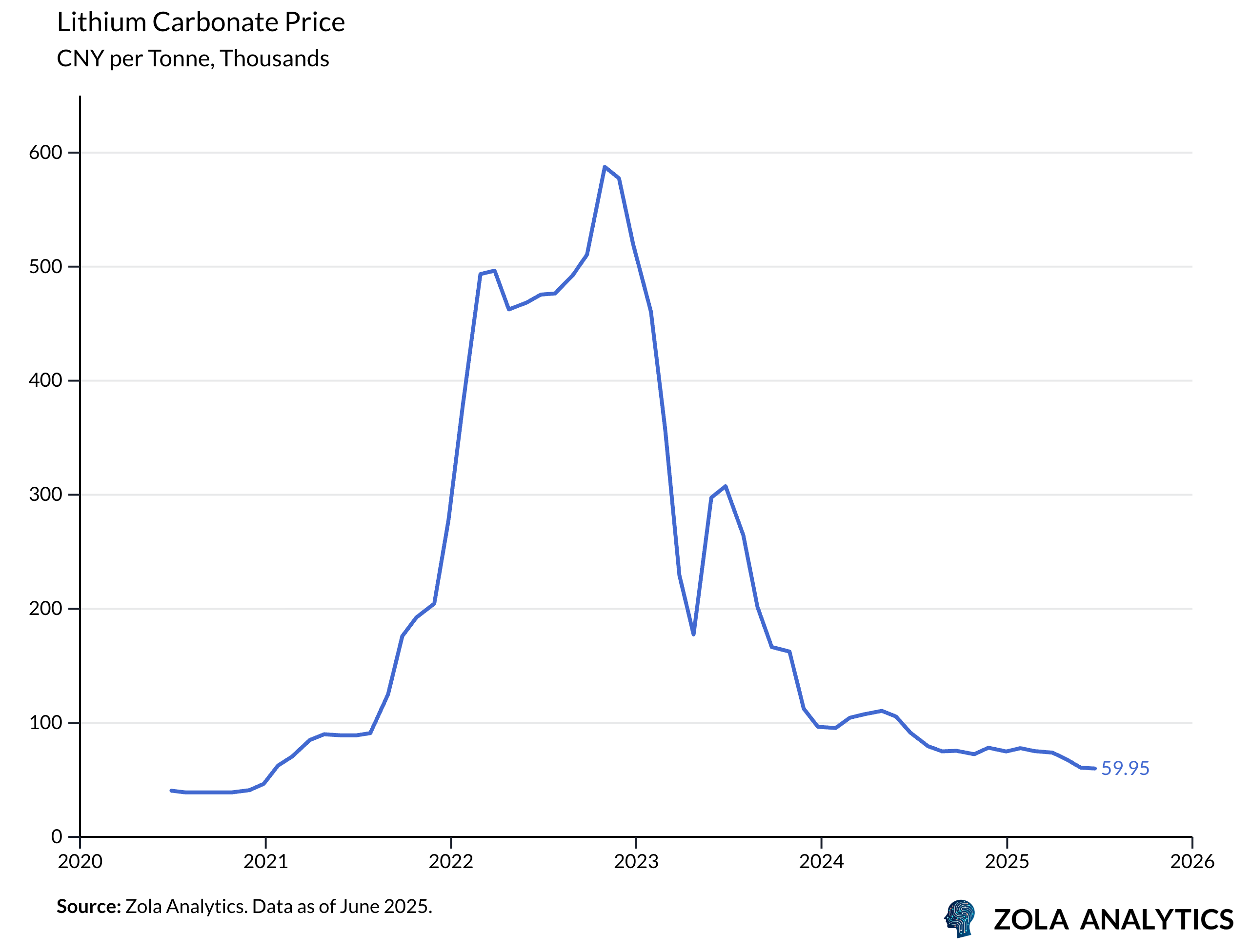

Lithium demand remains structurally strong, driven by the rapid growth of electric vehicles (EVs) and stationary energy storage. Lithium-ion batteries, which account for nearly 90% of lithium consumption, are expected to expand at ~15% annually through 2030. However, the near-term outlook is clouded by cyclical weakness: EV sales growth has softened, lithium prices collapsed by ~90% since late 2022, and miners’ capital expenditures have peaked (see chart below).

This cyclical softness coincides with Chile’s own challenges: SQM, the country’s flagship lithium producer, saw net income fall over 70% in 2024 amid the price crash. Yet volumes surged by 27% in Q1 2025, highlighting resilience but also underscoring that Chile is only keeping pace with global growth rather than pulling ahead.

Chile’s Strategic Position: Nationalisation and Its Double-Edged Sword

Chile’s National Lithium Strategy, unveiled by President Boric in 2023, aims to secure state control over lithium production by placing Codelco, the state-owned copper giant, at the center of public-private partnerships. This approach has already attracted major investment: Rio Tinto announced a USD 1.4 billion commitment, including a landmark 50% stake in Codelco’s Salar de Maricunga project.

Yet risks loom large. Regulatory complexity, Codelco’s inexperience in lithium, and heavy reliance on China—which takes ~70% of Chile’s lithium carbonate exports—pose vulnerabilities (see chart below). Such concentration risks could expose Chile to geopolitical tensions, especially as the US seeks to diversify away from Chinese-controlled critical minerals.

Moreover, Chile’s national strategy has sparked concerns that investment may shift to Argentina’s more welcoming regulatory environment, potentially allowing it to overtake Chile as Latin America’s top producer.

Political Stability and Investment Climate: Balancing Pragmatism and Ambition

Despite fears of radical leftward swings, Chile’s economic policies have remained pragmatic, with fiscal orthodoxy and measured reforms. Recent municipal election results and polling suggest a political shift back toward the centre-right by late 2025, which could boost business confidence. Meanwhile, ongoing monetary easing has improved macro fundamentals.

The early success of Boric’s strategy—evidenced by Rio Tinto’s entry—demonstrates Chile’s capacity to balance public control with private investment. But effective execution will be crucial: delays, social conflicts, or regulatory missteps could undermine the plan and deter future investors.

Structural vs. Temporary Drivers

Short-term headwinds include oversupply fears, price volatility, and geopolitical friction. However, structural drivers remain intact: tightening emission standards in Europe, the push for EV adoption, and the massive energy storage buildout globally will all support lithium demand through 2030.

Chile’s nationalisation approach could amplify or undercut these structural opportunities. If executed well, it could ensure value capture for the state while securing foreign investment; if mismanaged, it could slow production growth and cede ground to regional rivals.

Implications for Growth and Markets

A successful balancing act—meeting production targets, managing geopolitical risks, and maintaining investment attractiveness—would position Chile to harness the next surge in lithium demand later this decade. This, in turn, could reinforce its fiscal revenues, strengthen the peso, and sustain economic resilience even amid copper price fluctuations.

For global investors, patience will be key: lithium prices may remain under pressure in the near term, but Chile’s unique resource base and early signs of effective partnership models hint at significant medium-term opportunities. Chile’s ability to navigate regulatory complexities and geopolitical shifts will determine whether its lithium becomes a competitive advantage or a missed opportunity.

The Verdict So Far

Chile’s future as a linchpin of the global lithium supply chain hinges on the interplay of near-term demand softness, longer-term structural growth, and a stabilising political environment. While cyclical turbulence clouds the immediate outlook, the fundamentals of the energy transition suggest Chile’s lithium will remain indispensable, offering investors a strategic lever on the green revolution (see chart below).