Published August 22nd 2025

14 minute read

Abenomics at the Crossroads

In the mid-16th century, the great warlord Mōri Motonari sat down to teach his three sons a lesson. Handing each a single arrow, he watched them snap with ease. But when he bound three arrows together, they proved unbreakable.

Like those in the legend, the three arrows of Abenomics - monetary easing, flexible fiscal policy, and structural reform - are supposed to reinforce each other. Each alone is ineffective, but together they are strong enough to break Japan out of the economic malaise that has gripped the country since the 1980s. At least, that’s the theory. More than a decade on, what are the results?

Abe’s Quiver

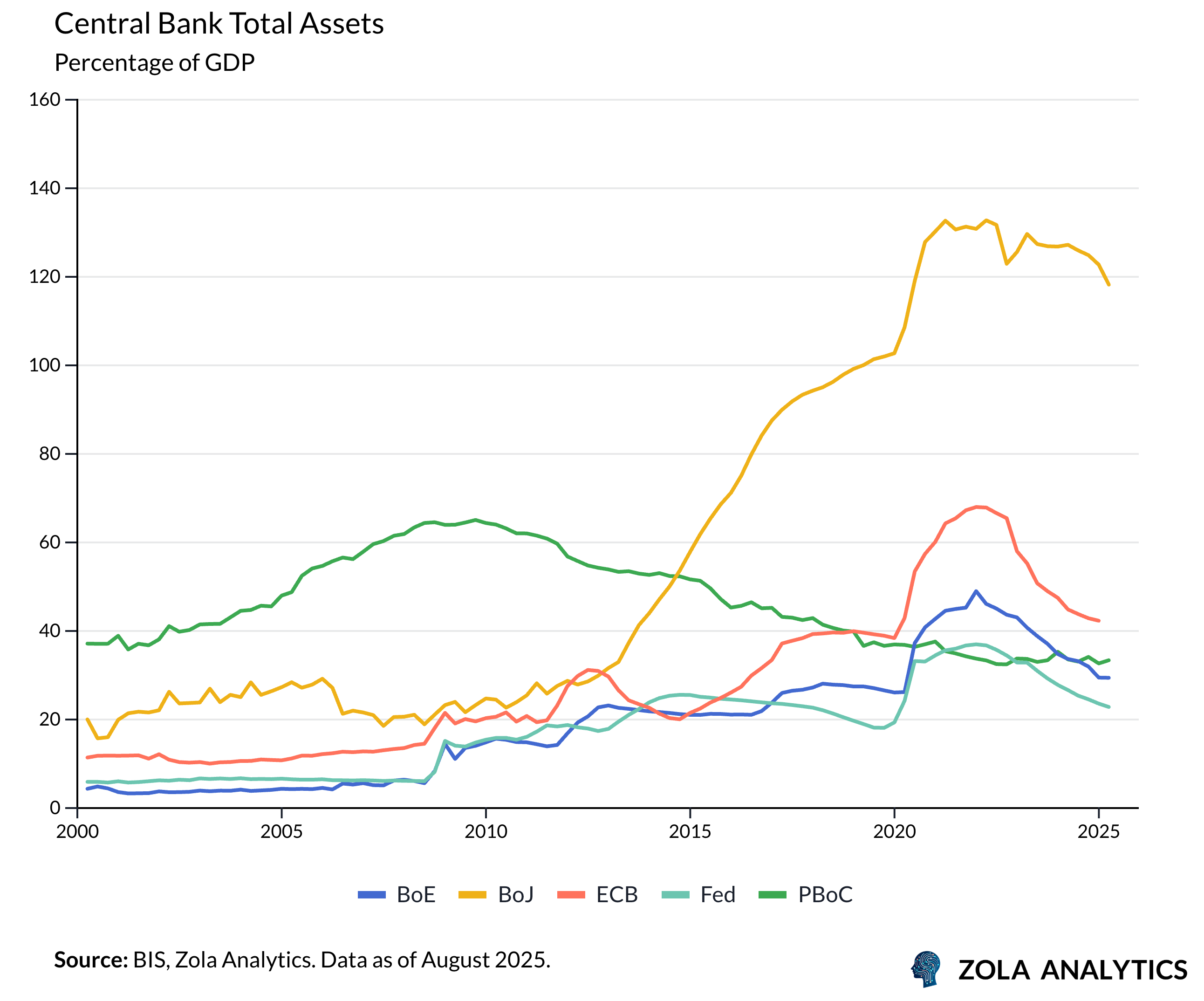

In the first weeks of his government, Abe quickly deployed his first arrow. Haruhiko Kuroda was appointed to head the Bank of Japan (BoJ) with a mandate to generate 2% inflation. To this end, the BoJ implemented aggressive monetary measures: quantitative easing, negative interest rates from February 2016, and yield curve control capping 10-year government bond yields from September 2016. As a result, the BoJ’s balance sheet ballooned to unprecedented levels, with central bank assets relative to GDP far surpassing those of its peers.

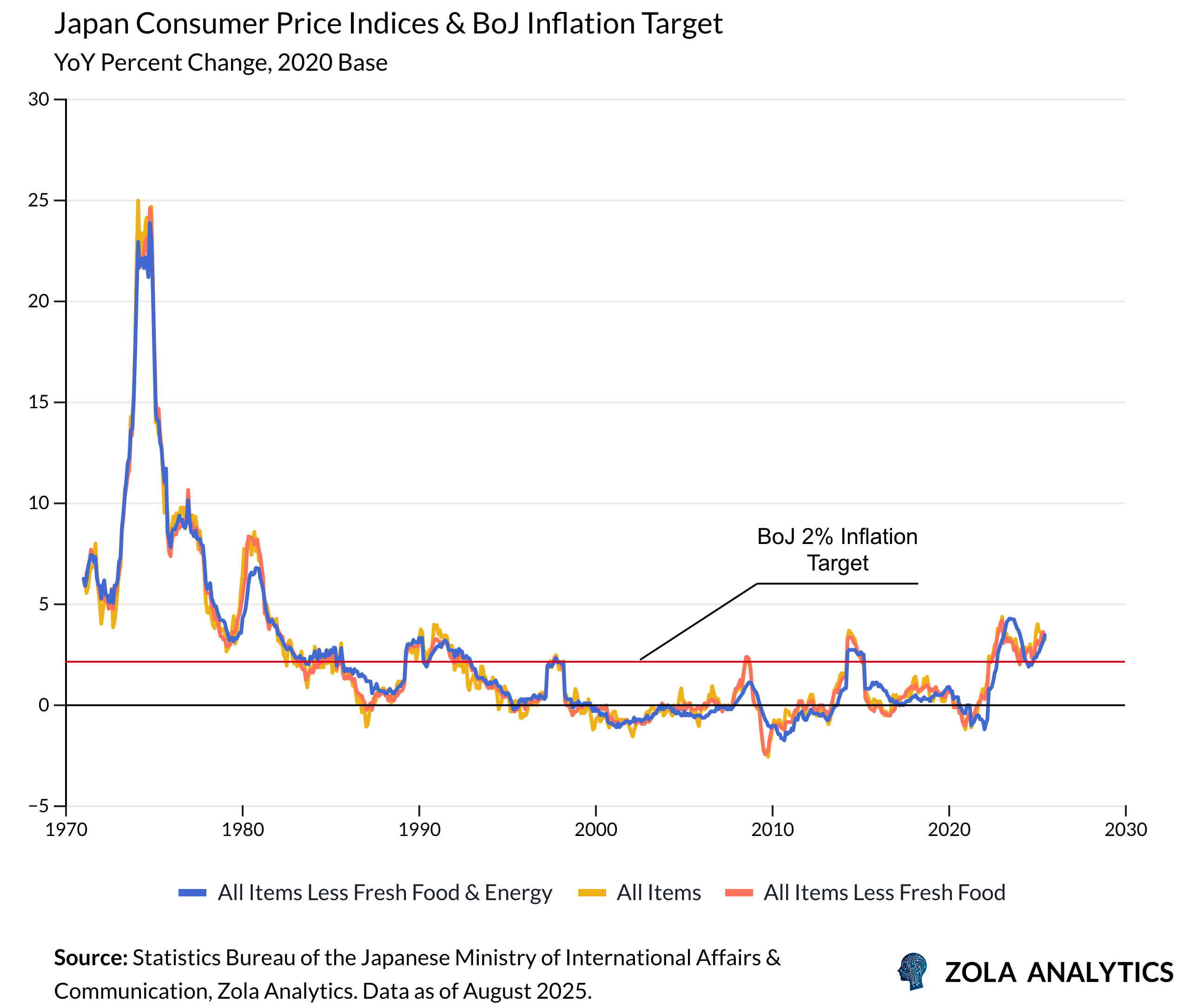

Twenty years of deflation had entrenched expectations of falling prices, causing households and businesses to delay spending and investment. Breaking this mindset required extraordinary intervention. Yet two structural factors made it particularly difficult for the BoJ to convince Japan that higher inflation was either desirable or sustainable.

First, inflation expectations are heavily conditioned by lived experience. Having grown up in an environment of near-zero inflation, younger generations assumed it as the norm. Wage demands remained modest, and households planned their finances around stability rather than erosion of purchasing power. For the BoJ, trying to ignite higher expectations was like trying to light damp firewood.

Second, Japan’s demographics and savings structure created a powerful constituency against inflation. The country is the oldest society in the world, and retirees hold a disproportionate share of household wealth - much of it in cash and deposits. Rising prices erode the real value of these assets. With older citizens both numerous and politically active, high inflation became toxic: policymakers could not credibly commit to it without alienating the very voters who dominate the electorate.

These constraints meant that even with bold monetary tools, the BoJ’s credibility problem was built in. Inflation could be nudged temporarily, but sustained reflation ran up against the political economy of an ageing, cash-rich society. The long view of Japanese inflation illustrates how deeply ingrained deflation had become by the time Abe’s government took office.

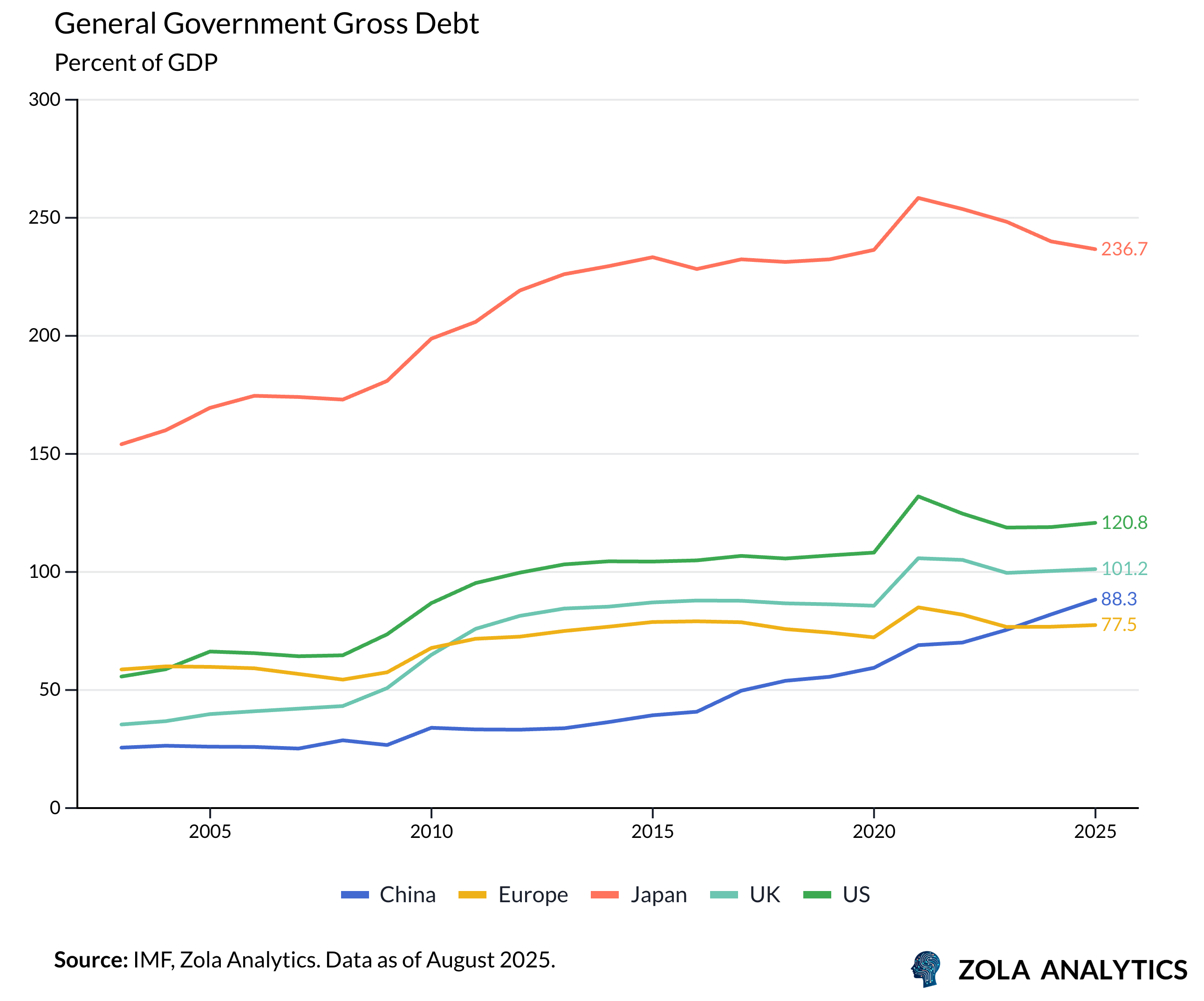

The second arrow aimed to harness fiscal policy in service of two goals that were often in tension. The first was to stimulate demand through public spending and infrastructure investment, giving the economy the push it needed to escape decades of stagnation. The second was to ensure long-term sustainability by containing a public debt burden already exceeding 230% of GDP, the highest in the advanced world.

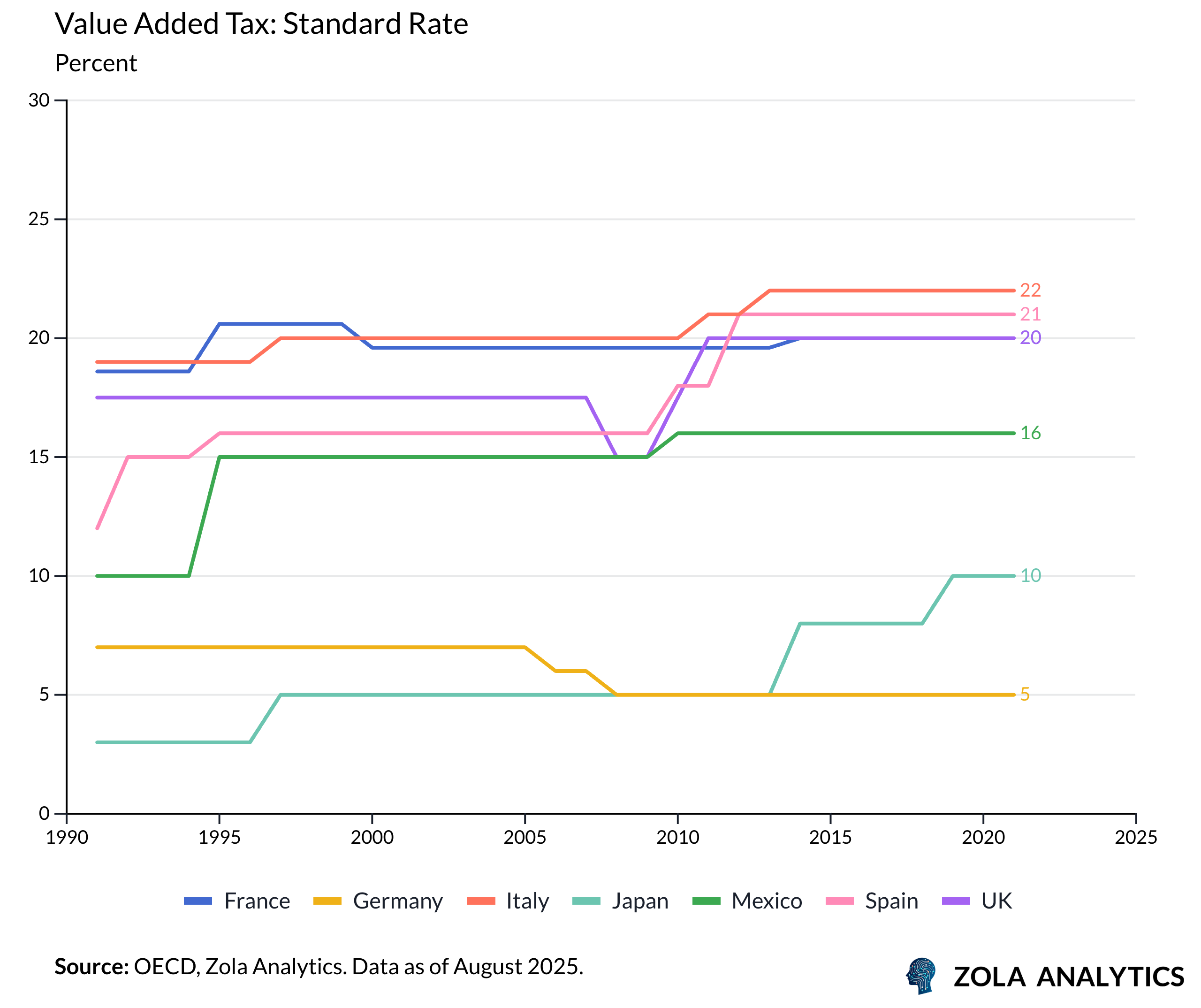

An ageing society made the challenge sharper. Rising healthcare and pension costs locked in structural spending pressures, even as revenue growth lagged. To address this, policymakers turned to the consumption tax. At 5%, it was among the lowest rates internationally, offering a potential source of stable revenue if increases could be implemented without stalling growth.

In theory, the fiscal arrow was meant to provide short-term stimulus while charting a credible path to medium-term consolidation. The government would spend to restart growth, then gradually narrow deficits through a broader tax base. Like the other arrows, its effectiveness depended on timing and coordination: stimulus to reignite demand, consolidation to secure confidence, both in support of Japan’s wider economic renewal.

The third arrow targeted structural constraints on Japanese growth. Chief among them was Japan’s dual labour market, which divided workers between secure lifetime employment and precarious part-time roles often held by women and younger people. This fragmentation limited mobility, suppressed wages, and held back productivity.

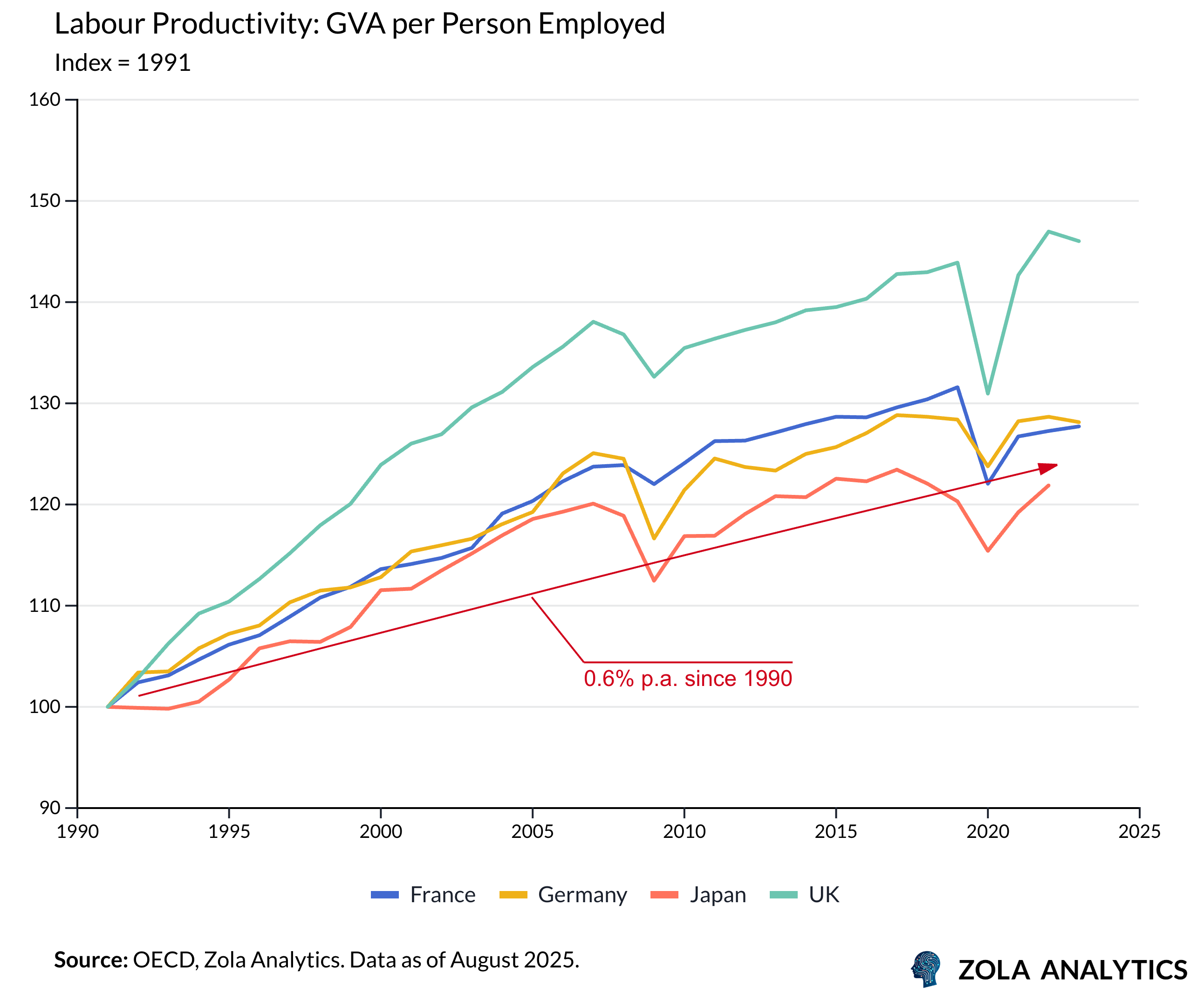

By the early 2010s, labour productivity growth had slowed to just 0.6% annually. Decades of manufacturing had been offshored to lower-cost countries, while the domestic economy tilted increasingly toward services concentrated in retail and food service rather than high-value industries. Cultural norms against layoffs kept employment rates high, but with so many people locked in low-productivity roles, output per worker barely moved.

The effectiveness of the first two arrows ultimately depended on the third - the promise that structural reform would lift productivity, narrow labour market divides, and unlock the growth that monetary and fiscal stimulus alone could not deliver.

Missing The Mark

So how did these ambitious reforms fare? The results tell a story of partial success undermined by deeper failures. While some initiatives produced visible gains, the fundamental transformation never materialized.

Structural reform - the third arrow - was supposed to give Japan the self-sustaining growth that stimulus alone could not deliver. In practice, the outcomes were mixed.

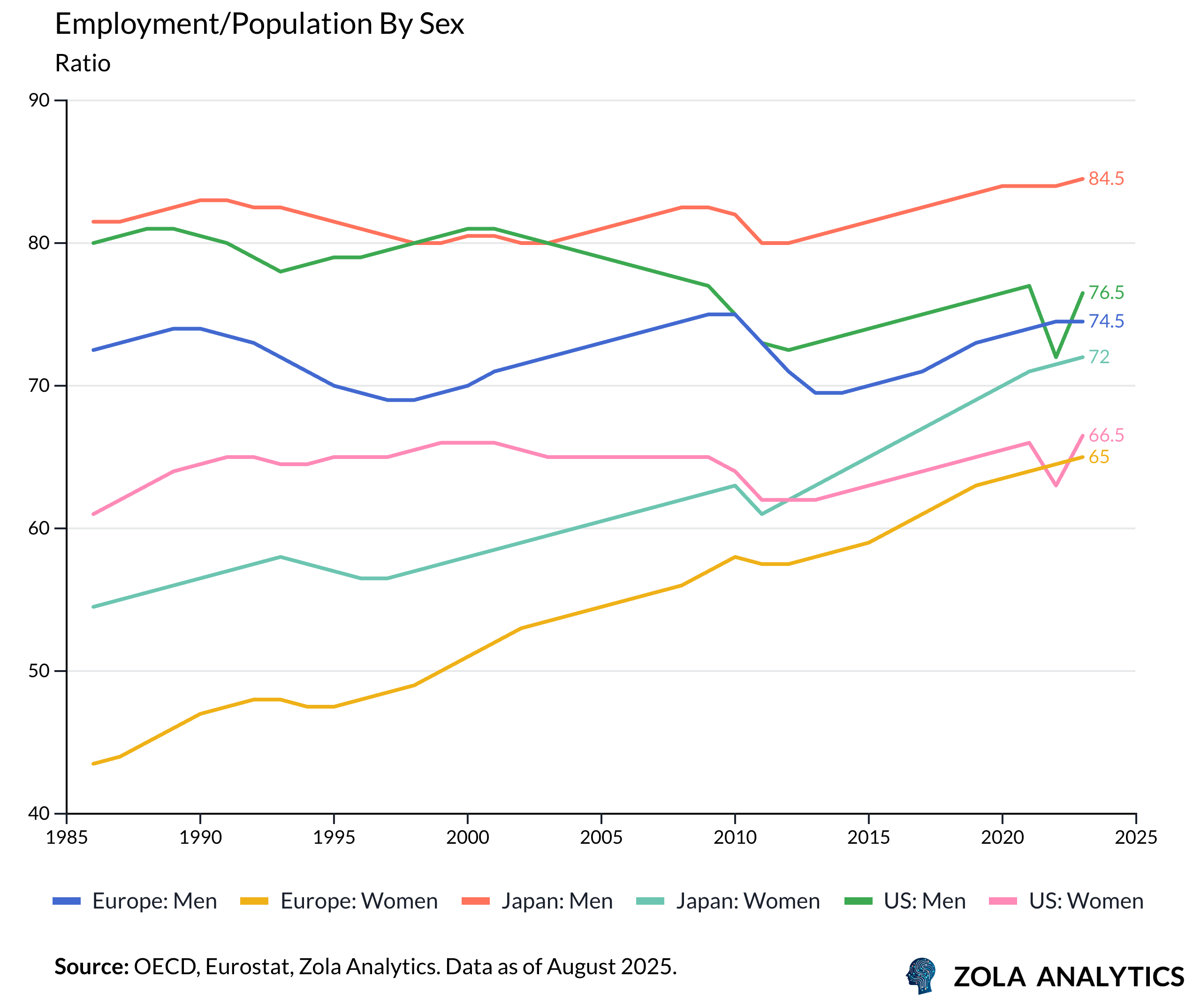

There were visible successes. Womenomics expanded childcare and promoted female managers, lifting female employment from 62% in 2012 to 72% today - now higher than in the US or Europe - even as Japan’s working-age population shrank by 15%. Seniors also stayed in the workforce longer, pushing Japan’s effective retirement age to the top of the OECD. Immigration doubled without political backlash, a quiet revolution in a historically closed society.

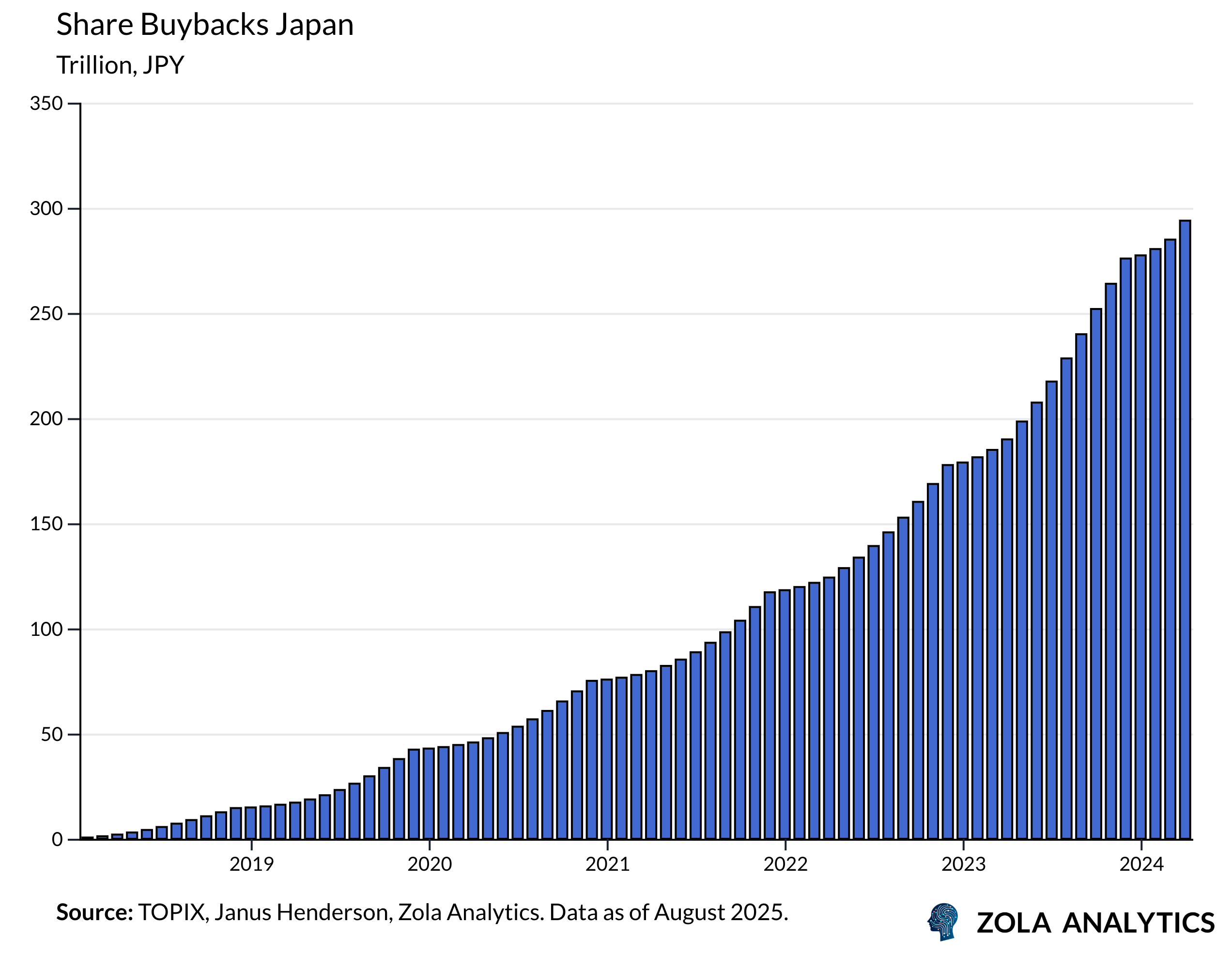

Corporate governance reform marked another shift. New stewardship and governance codes encouraged transparency. Cross-shareholdings declined while buybacks surged. Return on equity improved markedly. For shareholders, the rewards were unprecedented - on the surface, corporate Japan had finally turned a page.

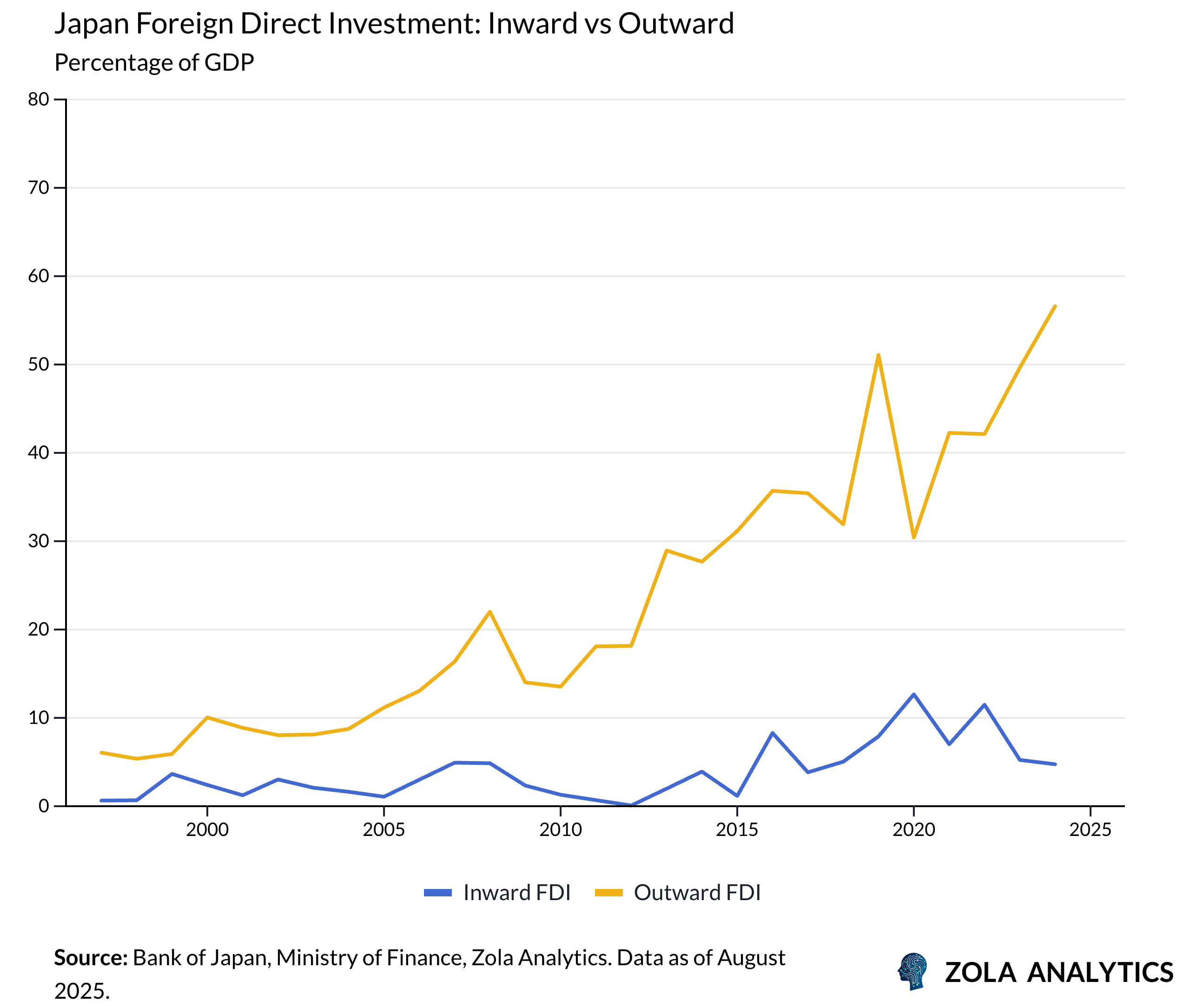

Yet these gains concealed deeper weaknesses. Outward FDI soared from 5% of GDP in the mid-1990s to 55% today, as firms deployed their cash abroad rather than at home. Inward FDI, by contrast, stagnated at just 5% of GDP - far below other advanced economies. Without foreign entrants to inject competition, governance reform boosted valuations but failed to rekindle domestic dynamism.

As balance sheets swelled, firms unlocked value not by building new factories or investing in productivity but by returning capital to shareholders. Retained earnings ballooned, but capital expenditure lagged. Outward foreign investment climbed sharply, while buybacks set record highs. The result was paradoxical: equity markets flourished even as the real economy remained stuck. Japan’s corporate caution, far from being overcome, had simply been financialized.

The deeper renewal never came. Many reforms were “comply or explain” - symbolic rather than binding. Capital efficiency improved, but productivity stagnated. Japan lost ground in advanced technologies despite record R&D spending. Labour market duality kept wages suppressed and efficiency low, while vast corporate cash piles sat idle. Ultra-low interest rates propped up unproductive firms, compounding inefficiency.

In the end, structural reform allowed Japan to adapt to demographic pressures and raised corporate standards, but it never transformed the growth model. Productivity gains remained elusive, and households carried the burden through weak wage growth and higher import costs. With domestic demand faltering, Japan relied on the United States as the consumer of last resort - exporting into American consumption rather than igniting growth at home.

Stop-and-Go

If structural reform disappointed through timidity, fiscal policy faltered through inconsistency. Abe’s government introduced a JPY 10.3 trillion stimulus package early on, but public investment quickly receded as a share of GDP.

The 2014 consumption tax hike (5% to 8%) triggered a steep economic backlash - real GDP contracted roughly 7% annualised in Q2, and household spending fell nearly 6% year-on-year. The 2019 hike to 10% carried a notable negative income effect - estimated to shave about 0.7% off consumption and 0.4% off GDP and came on the eve of the COVID shock.

Throughout, fiscal policy often worked at cross-purposes with monetary stimulus. The BoJ pushed aggressively with asset purchases, while the Finance Ministry remained narrowly focused on debt sustainability, sending mixed signals. By contrast, other central banks coordinated explicitly with fiscal authorities. Japan’s mix was different: it gave with one hand while taking with the other.

The Limits of Accommodation

With structural reforms stalling, the burden fell back on policy accommodation. Fiscal space narrowed as debt climbed toward 250% of GDP, and repeated consumption tax hikes in 2014 and 2019 undercut household demand. That left monetary easing as the dominant force.

In the short term, it delivered results. The BoJ’s swollen balance sheet and negative rates helped end two decades of deflation. Consumer prices rose 3.3% year-on-year by mid-2025, while the spring Shuntō wage round delivered the largest pay hikes in more than three decades. A weaker yen inflated corporate profits in yen terms, and equity markets surged. Unemployment remained low, and Japan avoided the prolonged stagnation many had feared.

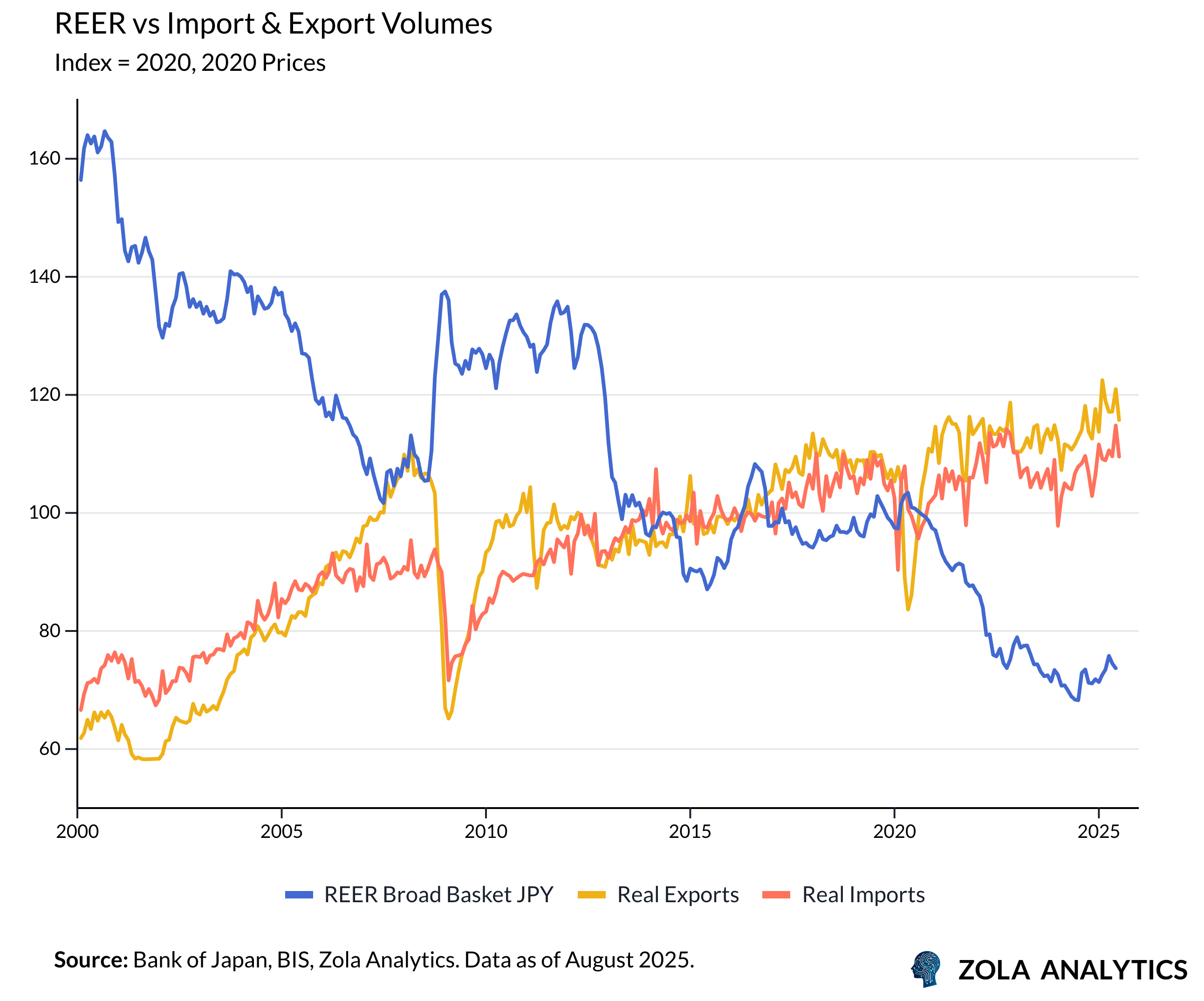

But the limits of accommodation became clear. Credit growth stayed muted, and export volumes stagnated despite historic depreciation. Estimates suggest that a 1% fall in the real effective exchange rate lifted exports by less than half a percent.

The competitive gains proved smaller than expected. Many exports are invoiced in dollars, limiting the benefit of yen depreciation. Meanwhile, imports priced in foreign currency exposed households directly to higher costs. Inflation expectations shifted only slowly, underscoring how difficult it was to change underlying behaviour.

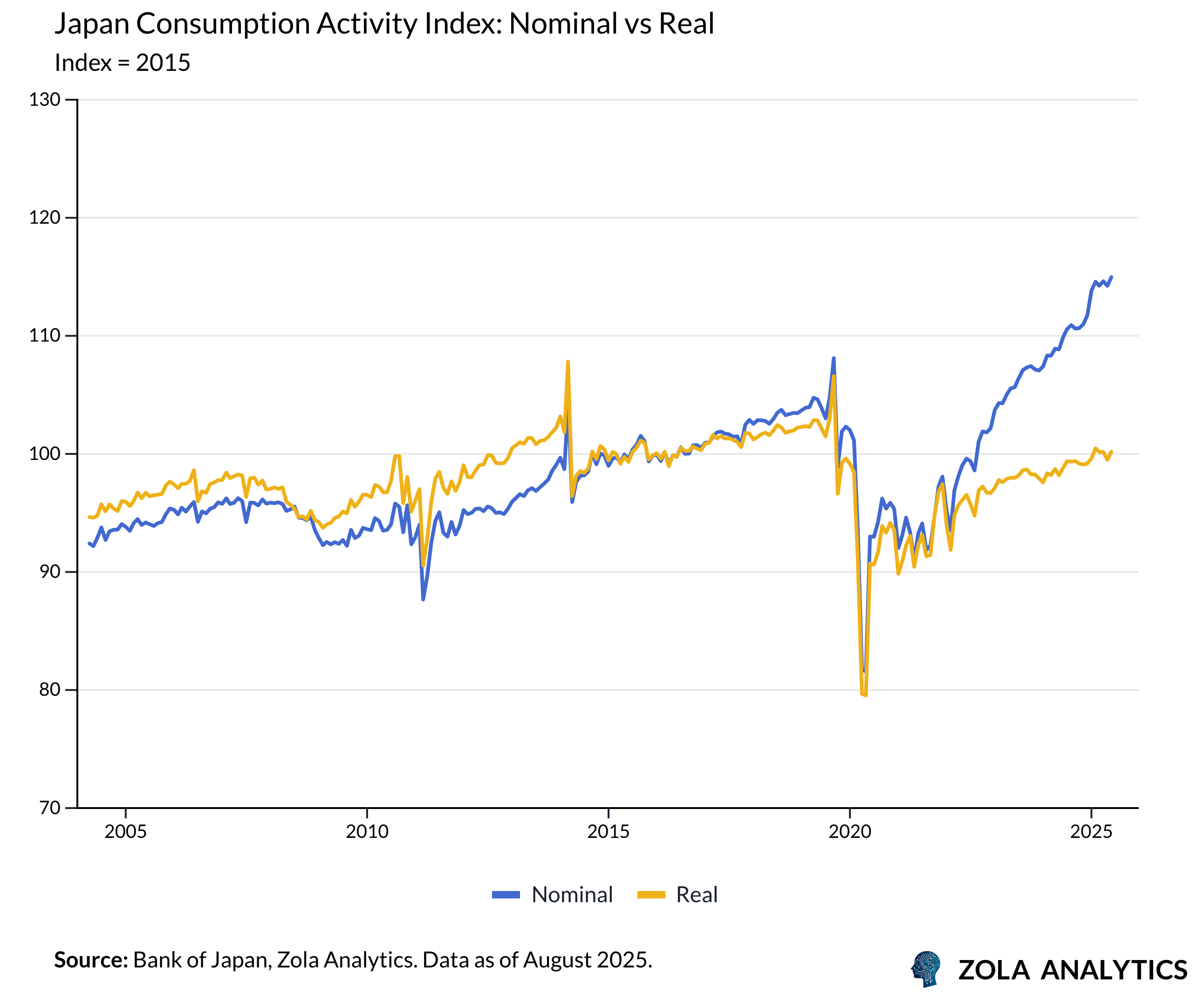

The central gamble of Abenomics was that defeating deflation would unleash pent-up demand. In practice, earlier mild deflation had coexisted with steady consumption, while the recent return of inflation eroded purchasing power without producing the spending surge policymakers had hoped for.

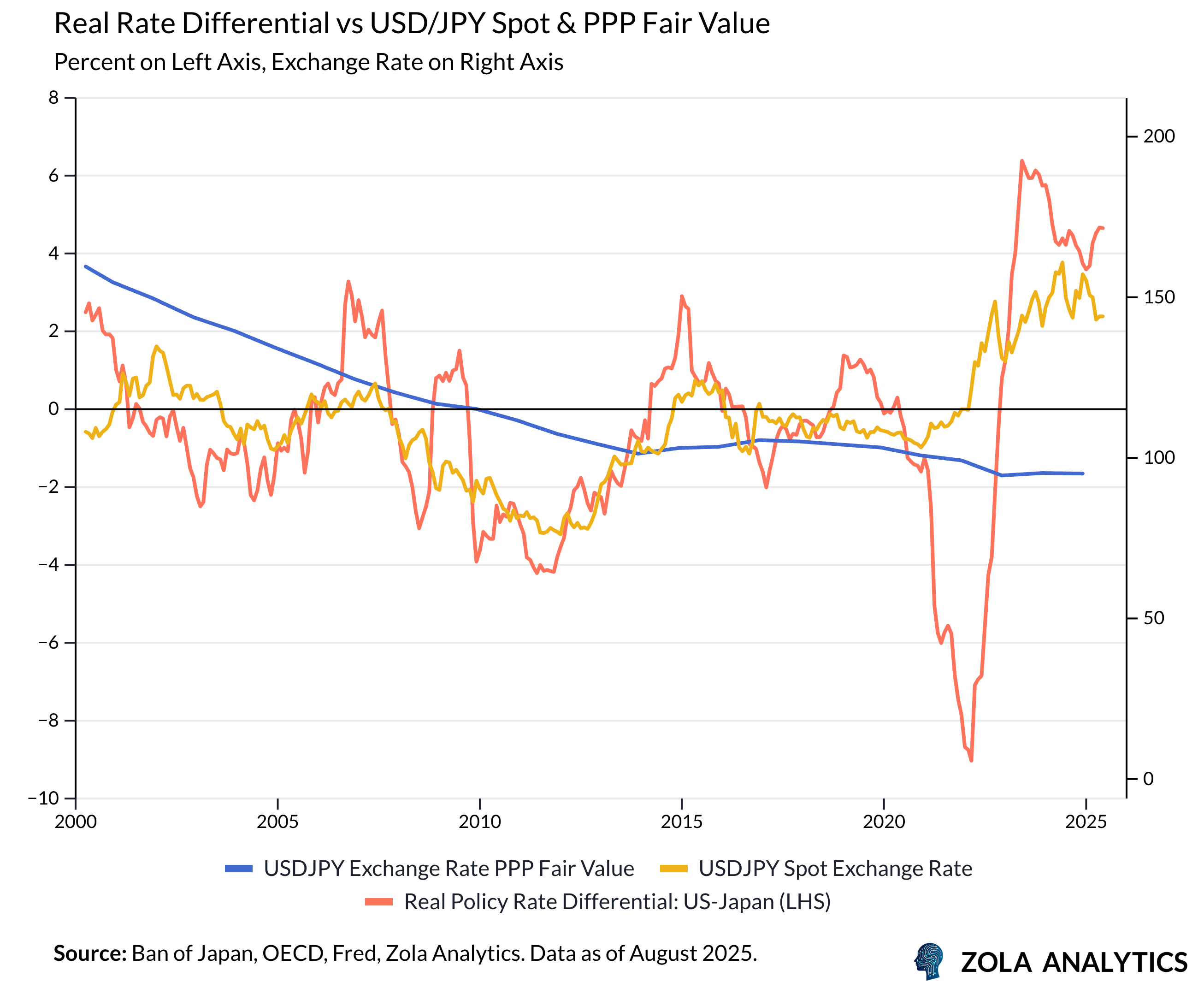

The weight placed on monetary easing was also visible in the currency. The yen’s path increasingly mirrored real interest rate differentials with the US. On purchasing power parity measures, it should be much stronger, highlighting how prolonged ultra-loose policy distorted exchange rates.

In the end, monetary easing bought valuable time, restored modest price growth, and kept labour markets strong. Yet without structural renewal it could not on its own deliver a lasting lift.

Hollow Wealth

The most visible successes of Abenomics appeared not in the real economy but in financial markets. Ultra-loose monetary policy and governance reforms lifted equity valuations, boosted property prices, and encouraged households to rebalance their portfolios. Yet much of this reflected global liquidity and generational shifts rather than domestic reform, and it did little to revive underlying productivity.

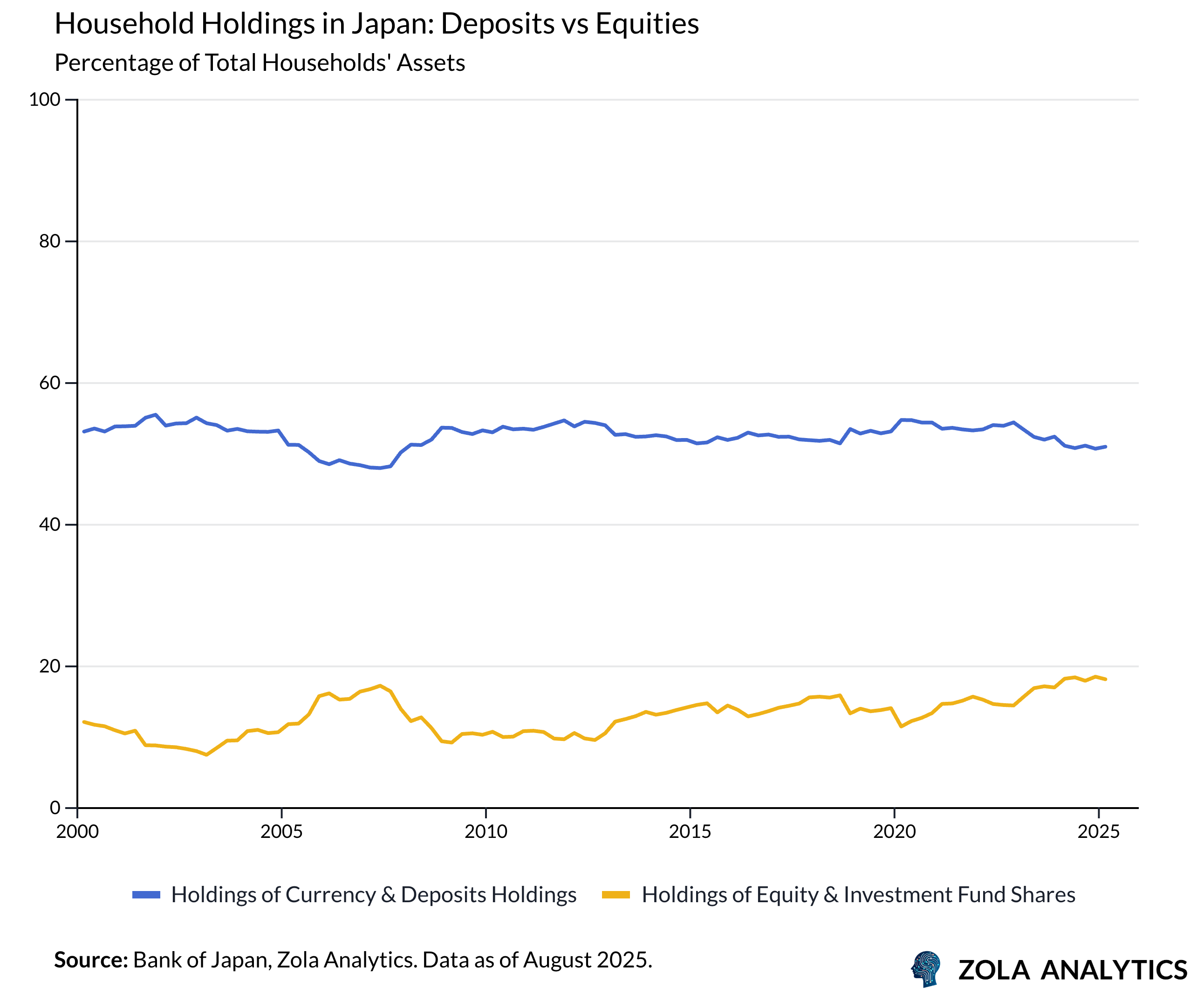

Household behaviour reinforced this imbalance. Savings continued to accumulate, keeping the cash-to-GDP ratio among the highest in the world.

More than half of financial assets remain in deposits. This conservative allocation amplified the income effects of policy. Low interest rates eroded returns for savers, while rising prices reduced real balances. Recent inflows into equities through the new Nippon Individual Savings Account (NISA) signalled the beginnings of change, but the persistence of excess savings underlined how deeply entrenched Japan’s liquidity preference remains.

The gains were also unevenly shared. Large firms and asset holders profited from a weaker yen, higher equity valuations, and buoyant property markets. But smaller firms and wage-dependent households faced rising import costs, eroded purchasing power, and an increase in bankruptcies. The result was a financial system flush with liquidity, but a real economy still short of dynamism.

The End of the Weak-Yen Era

In 2000, Ben Bernanke published a paper that called on Japanese policymakers to display “Rooseveltian resolve” in confronting deflation. 25 years on, it is clear that Abenomics answered that call. Abenomics ended deflation and restored Japan to modest price growth - an achievement once thought impossible. The three arrows broke the psychology of deflation, supported wages, and stabilised employment. In the battle against entrenched stagnation, Abe’s first arrow flew further than many predicted.

But resolve was not enough. Monetary easing weakened the yen and boosted profits, yet firms hoarded cash instead of investing. Fiscal support faltered under the weight of debt, and structural reform lagged, leaving productivity stagnant. The weak-yen growth model has now reached its limits. Export volumes have stagnated despite historic depreciation, while households have borne the costs through higher import prices, weaker real wages, and rising bankruptcies among smaller firms.

The challenge ahead is sharper than the one Abe confronted. The geoeconomic landscape is shifting: America, under Trump’s second administration, is seeking to rebalance trade and reduce its role as global consumer of last resort. For decades, Japan could rely on U.S. demand as an outlet for its exports. That cushion is now eroding, making it harder to “free-ride” on American consumption. A growth model built on yen weakness and external demand looks increasingly untenable.

Japan now stands at a crossroads. To fulfill the ambition of Abenomics, it must summon its resolve to complete the unfinished work of structural reform and fiscal consolidation without leaning on currency weakness or external demand.

Sign up to receive the Zola Global Macro Chartbook every week: https://www.zolaanalytics.com/insights?signUp