Published 3rd October 2025 3 minute read

Putting Pieces Together

With today’s payrolls report cancelled by the shutdown, the task falls to other signals to tell us how the labour market is evolving. But this is hardly new. Initial NFP prints have long struggled with accuracy, delivering noisy first estimates that are often followed by significant revisions. In many respects, the more reliable story is already visible in the pipeline.

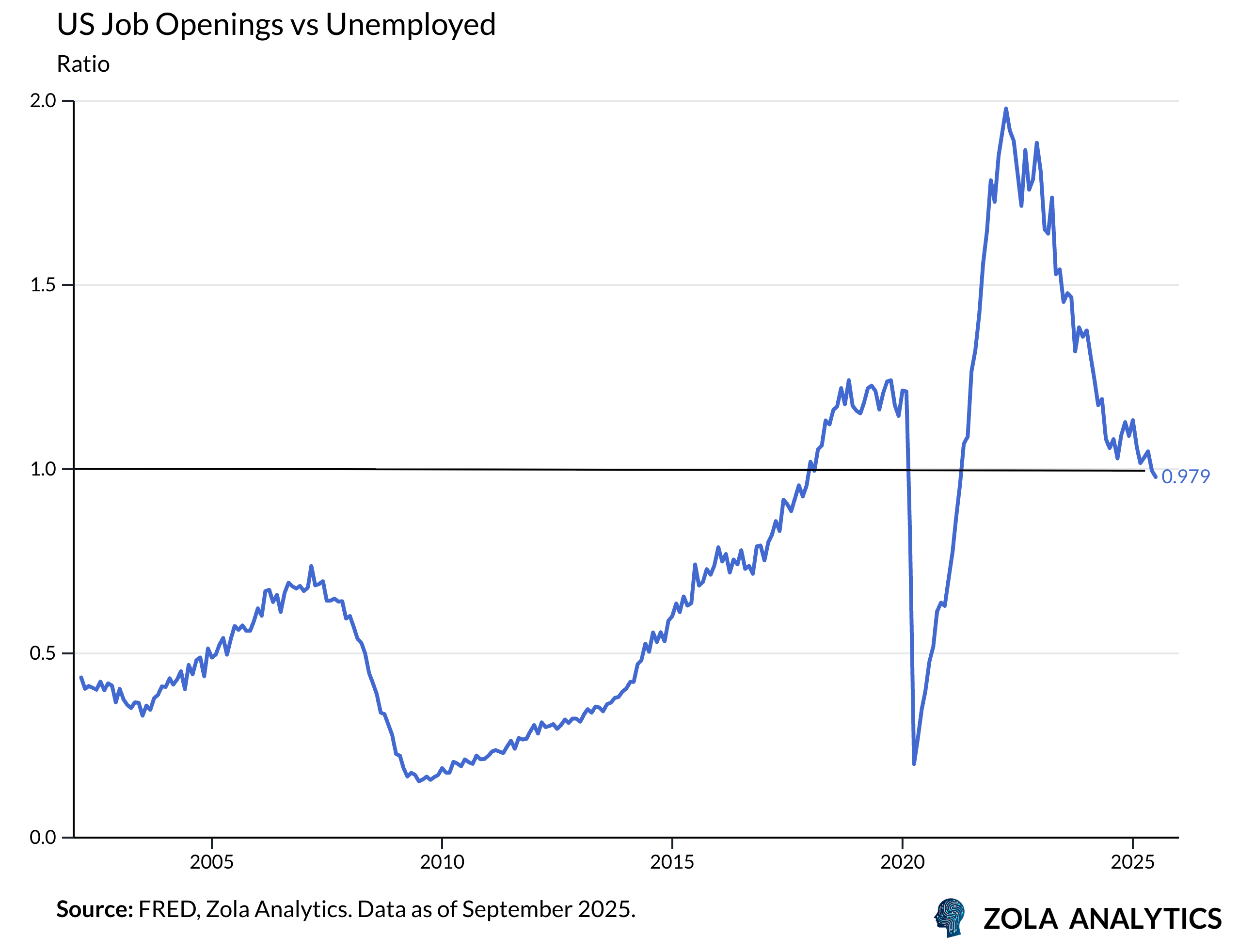

The clearest signal comes from job vacancies. Openings edged up in August, but on a three-month basis they have slipped to just over 7.2 million, the lowest since the reopening. For the first time in years, unemployed workers now outnumber available jobs. The vacancy-to-unemployed ratio, once a hallmark of labour market tightness, has fallen below one.

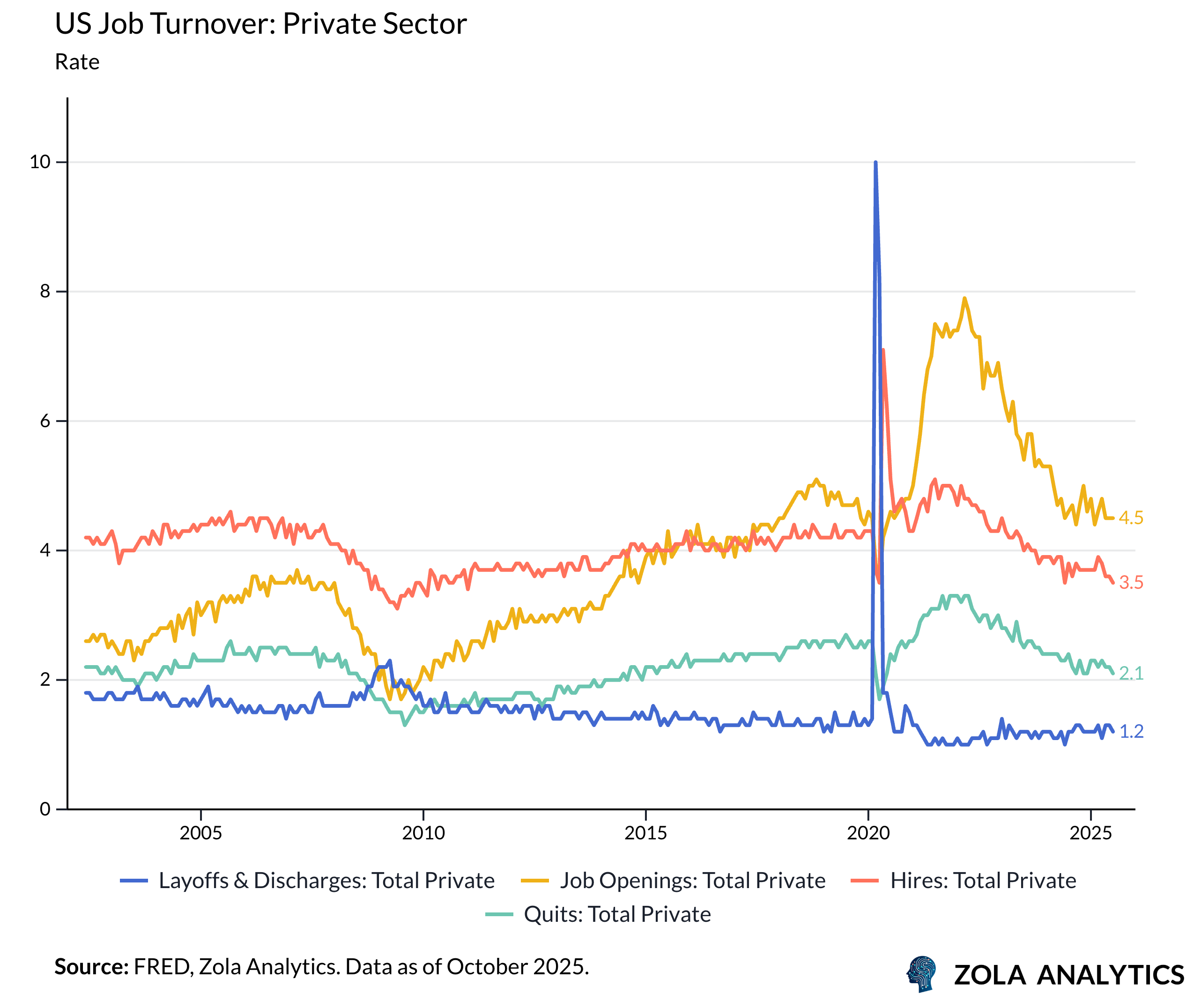

Turnover data point in the same direction. The hiring rate has dropped to 3.5%, a cycle low. The quits rate has eased to 2.1%, also a cycle low, showing less worker confidence in finding better positions. Firms are holding back on recruitment, and employees are less willing to move. Yet layoffs remain subdued at 1.2%, underscoring that the adjustment is gradual rather than disorderly.

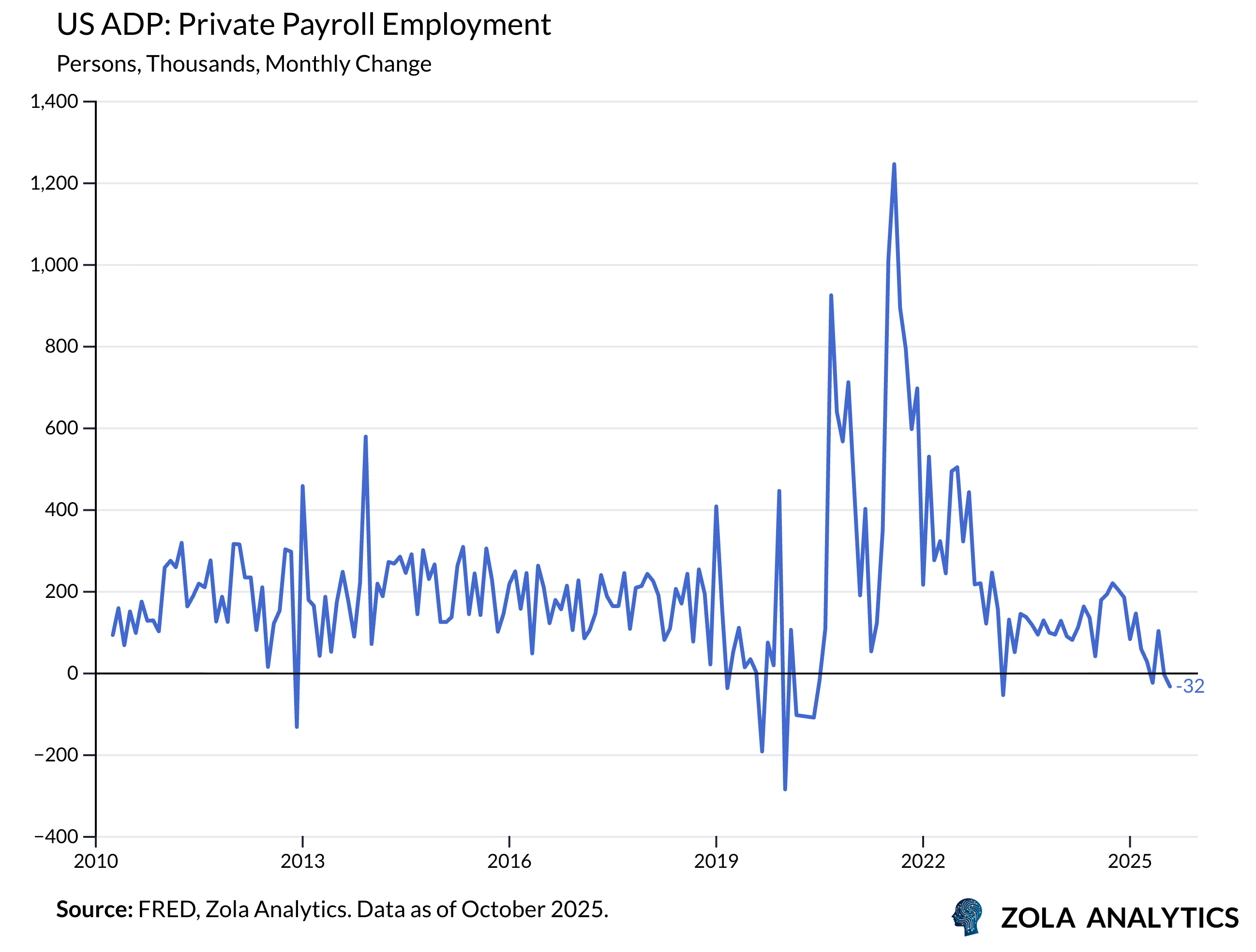

Private payroll data add to the picture, though with important caveats. September’s ADP report showed a 32k decline in private employment, mostly reflecting benchmarking to the Quarterly Census of Employment and Wages, which dragged the headline lower. Beneath that adjustment, the pattern was familiar: education and healthcare continued to add jobs, while the broader services sector softened and goods-producing industries contracted modestly, led by construction.

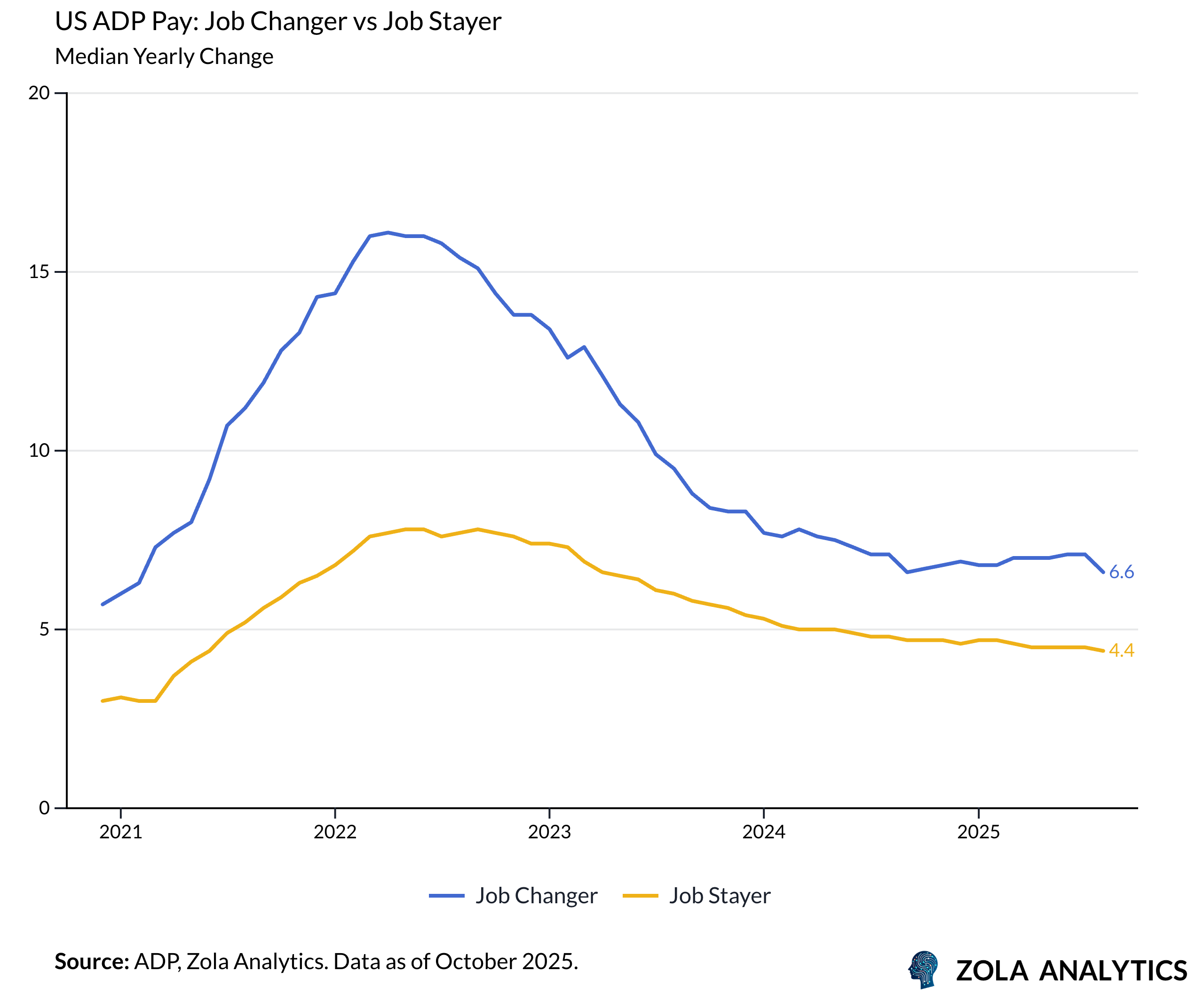

Wages continue to come in resilient. Median pay for job stayers is rising at about 4.5% YoY, slower than in 2022 but still enough to sustain household consumption. But wage-sensitive service categories are already showing signs of easing, consistent with weaker hiring momentum.

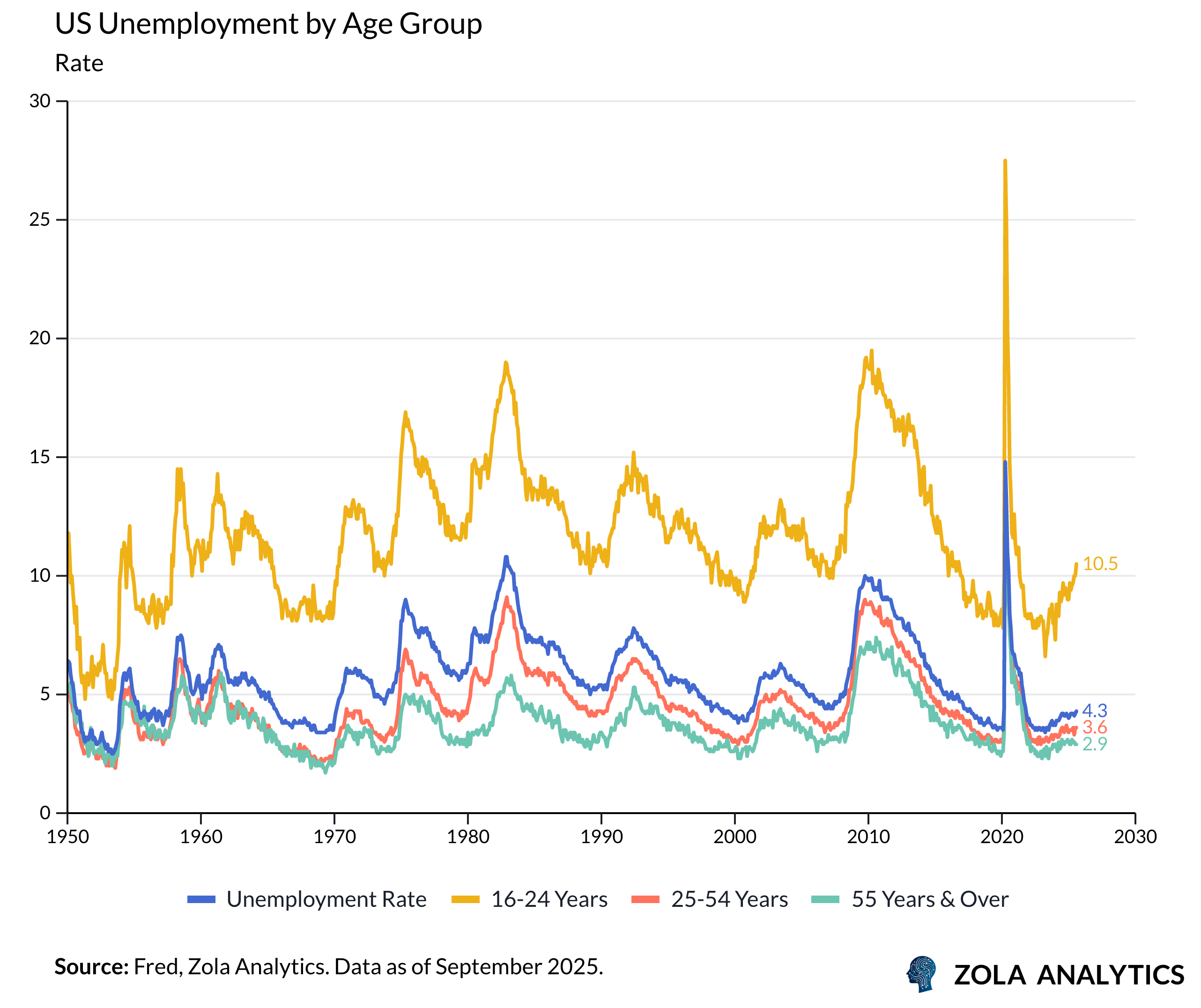

Employment has stalled most sharply among younger workers, especially those aged 16–24. Older cohorts are holding up better, but household confidence among the 25–54 group has fallen to levels that in past cycles preceded recession. This mix hints at both generational strain and broader caution.

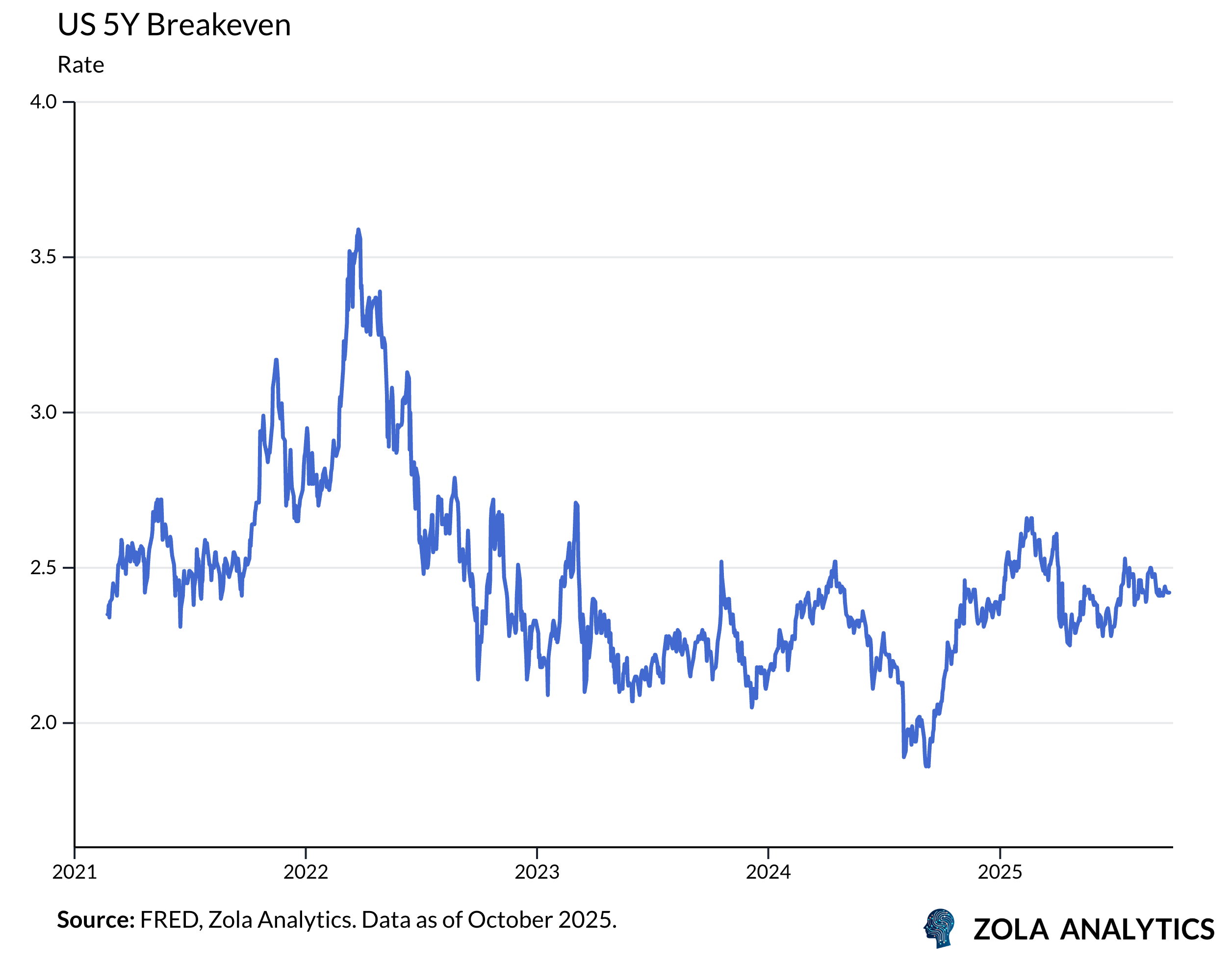

For the Federal Reserve, meeting on 28–29 October, the issue is no longer a missing data point but the balance of risks. Inflation has not returned to 2%, yet at 2.5–3.0% it sits close enough for several officials to call it “good enough” to pivot. Markets have moved with them. Ten-year breakeven inflation has slipped from around 2.7% earlier in the year to roughly 2.3%. Despite the decline, expectations remain well anchored. What matters most now is not a single payroll release, but the steady accumulation of labour-market slack. This signal is harder to revise away, and more difficult for the Fed to ignore.

Sign up to receive the Zola Global Macro Chartbook every week: https://www.zolaanalytics.com/insights?signUp

Disclaimer: Zola Analytics provides this material for informational and entertainment purposes only. It does not constitute investment advice.