Published July 9th 2025

Milei's Chainsaw: Breaking Argentina’s Inflationary Past

Javier Milei's first year came with a dramatic fiscal adjustment for Argentina. Annual inflation went from 211% to 47% by April 2025. This crisis management mirrors Argentina’s repeating cycle: the convertibility plan broke inflation in the 1990s but ended in collapse by 2001; the Kirchner era ended in crisis by 2015; and Macri’s orthodox policies unraveled by 2019. Each episode showed how short-lived victories often succumbed to the country’s structural weaknesses. Each cycle reflects the same institutional weaknesses: government overspending financed by money printing, i.e., seignorage financing. Milei's radical "chainsaw" approach aims to finally break this vicious cycle.

Painful Adjustments at Home

Since December 2017, annual inflation has been above 20% per year. By imposing a cash-based fiscal rule and capping the broad monetary base, Milei reduced seigniorage financing from 3% to around 0% of GDP. This represents a structural break which targets the root cause of previous inflation-management failures, but the sustainability test lies ahead.

Recent economic data shows this adjustment has not only stabilised inflation but has also led to an earlier-than-expected rebound: Argentina’s economic activity rose 1.9% month-on-month in April and 7.7% year-on-year, exceeding expectations and more than recovering March’s decline. This rebound followed the signing of a new USD 20 billion IMF agreement on April 11, which eased currency and capital controls, supporting market confidence.

Milei's fiscal reduction is notable, but is also concentrated in politically sensitive areas. His "chainsaw" to spending reduced public jobs and slashed subsidies for energy, transport, and utilities; with these cuts, expenditure decreased from 38% to 31% of GDP. The economic and social costs are substantial, but the fiscal transformation is undeniable.

This social cost was swift and severe. Along with a reduction in public jobs, unemployment rose by 1.8 percentage points, diverging from the regional average. Poverty spiked to 53% mid-year before easing to 38% by end of 2024, yet still above the regional average. As for salaries, they have outpaced inflation in the last year by 30 percentage points, but are still adjusting to past losses and remain lower than pre-crisis levels.

Markets and Investors Take Note

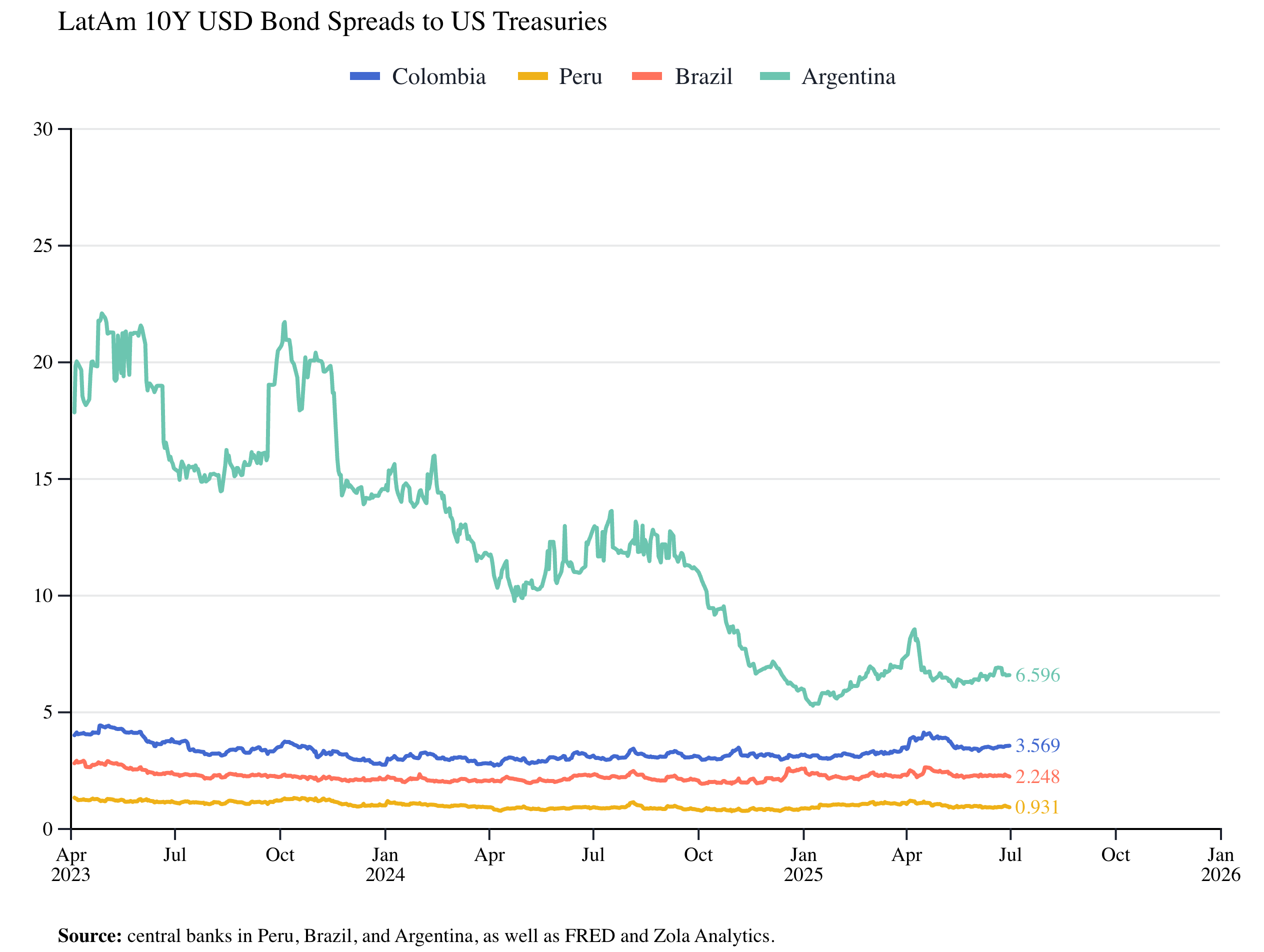

The positive surprise in April GDP, combined with the IMF financing package, strengthened perceptions that Milei’s stabilisation effort might succeed where past plans failed. Markets have signalled strong confidence: Argentine bond spreads have decreased from 1900 to 890bps. while regional peers deteriorated – a significant relative performance that reflects internal policies rather than global conditions. Nevertheless, spreads still remain notably above others in the region. This mirrors Macri's early success, when spreads similarly reduced before external pressures forced policy reversal by 2018. There is one key difference: Milei eliminated the fiscal dominance of monetary policy that Macri did not touch.

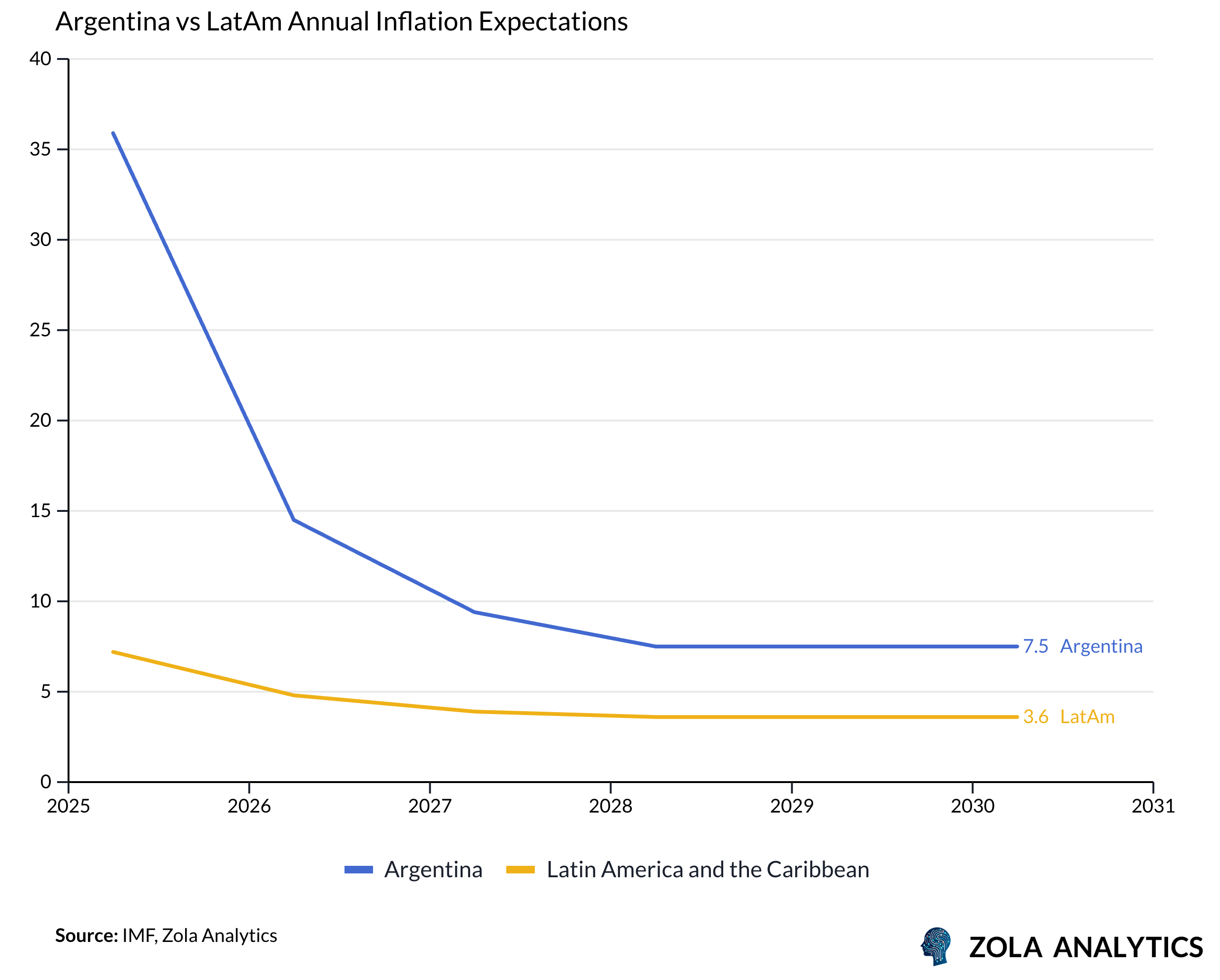

Along with this investor confidence, the market is expecting that inflation will go down to a single digit by 2027. This suggests that investors believe this stabilisation attempt differs from previous failures; yet, it is still early on to affirm that there won’t be a backtrack.

Capital Flows and Peso Stability

Domestic confidence mirrors market sentiment. Milei's “blanqueo”, a regularisation program, brought USD 18 billion dollars cash into the banking system – more than doubling Macri's previous record of $7 billion. This unprecedented capital repatriation has led Milei to launch another regularisation program.

The IMF agreement signed in April included partial lifting of currency and capital restrictions, providing additional liquidity and reassuring investors without destabilizing the currency.. Having more US dollars in the financial system, along with the removal of official currency exchange buying limits, resulted in a relatively stable Peso. The US dollar exchange rate has stayed in the bottom half of the no intervention bound established by the Central Bank, showing optimistic signs. However, the currency stability that markets celebrate creates new risks. With a stable Peso and still high levels of inflation, Argentina has become one of the world's most expensive countries. The Big Mac index shows severe overvaluation, which has decreased tourism levels to a record low deficit of 5.1 million – more Argentines traveling abroad than foreigners visiting. This competitiveness crisis with other countries threatens sustainability and some economists believe that a devaluation is imminent – Milei denies it.

Political Backing and Challenges Ahead

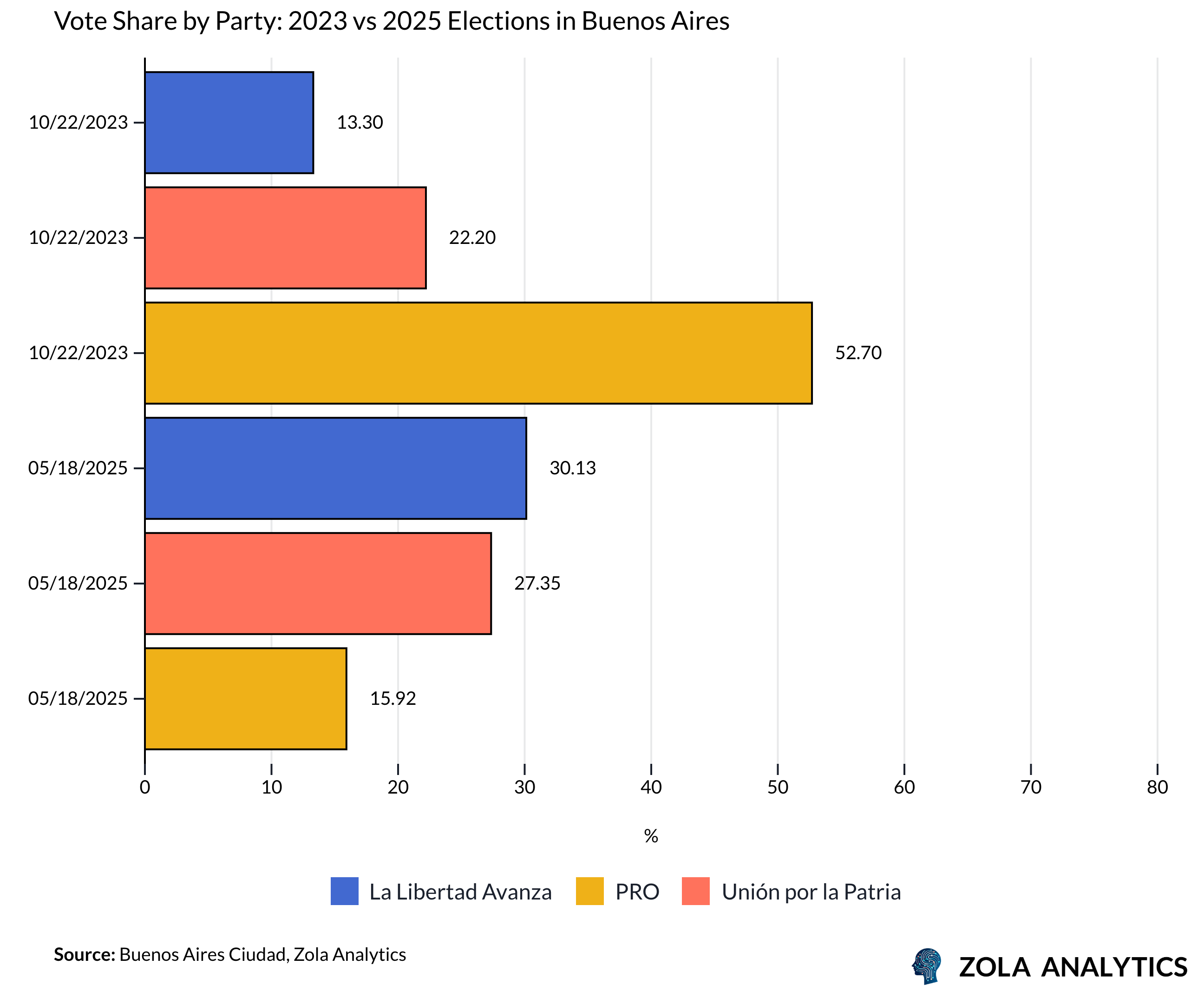

Even after aggressive cuts, the president’s political image remains strong but there are increasing pressures. His party doubled its Buenos Aires vote share to 30% in recent midterms, leaving the previously dominant PRO party in third place and ending their 11 election winning streak. Despite low turnout, this electoral success provides political capital for continued deep and drastic adjustments, but the overvaluation dilemma intensifies as national midterms approach.

This win is a vote of confidence from the Argentine electorate, particularly for Milei’s economic achievements so far. He still has support, but Milei should beware of the high cost of his actions and look at long-term continuity rather than one-off measures.

The second half of 2025 brings about competing risks. An overvalued Peso could continue sinking tourism and decrease competitiveness in exports, while devaluation could increase inflation expectations. This is a costly choice ahead of national midterm elections, and one which historically pressured policy reversals.

A Fragile Opportunity

April’s strong data suggests that Milei’s early stabilisation is delivering immediate momentum, but unresolved peso overvaluation and structural vulnerabilities mean the risk of a renewed crisis remains if underlying imbalances persist. Whether Milei can break Argentina’s cycle with his chainsaw depends on navigating this impossible trade-off while maintaining political support through sustained austerity. His initial gains have bought time, but the true test will be sustaining investor and social confidence if growth momentum falters or external shocks arise.