Published June 10th 2025

The ECB’s 25bp Cut: A Pivot or a Pause?

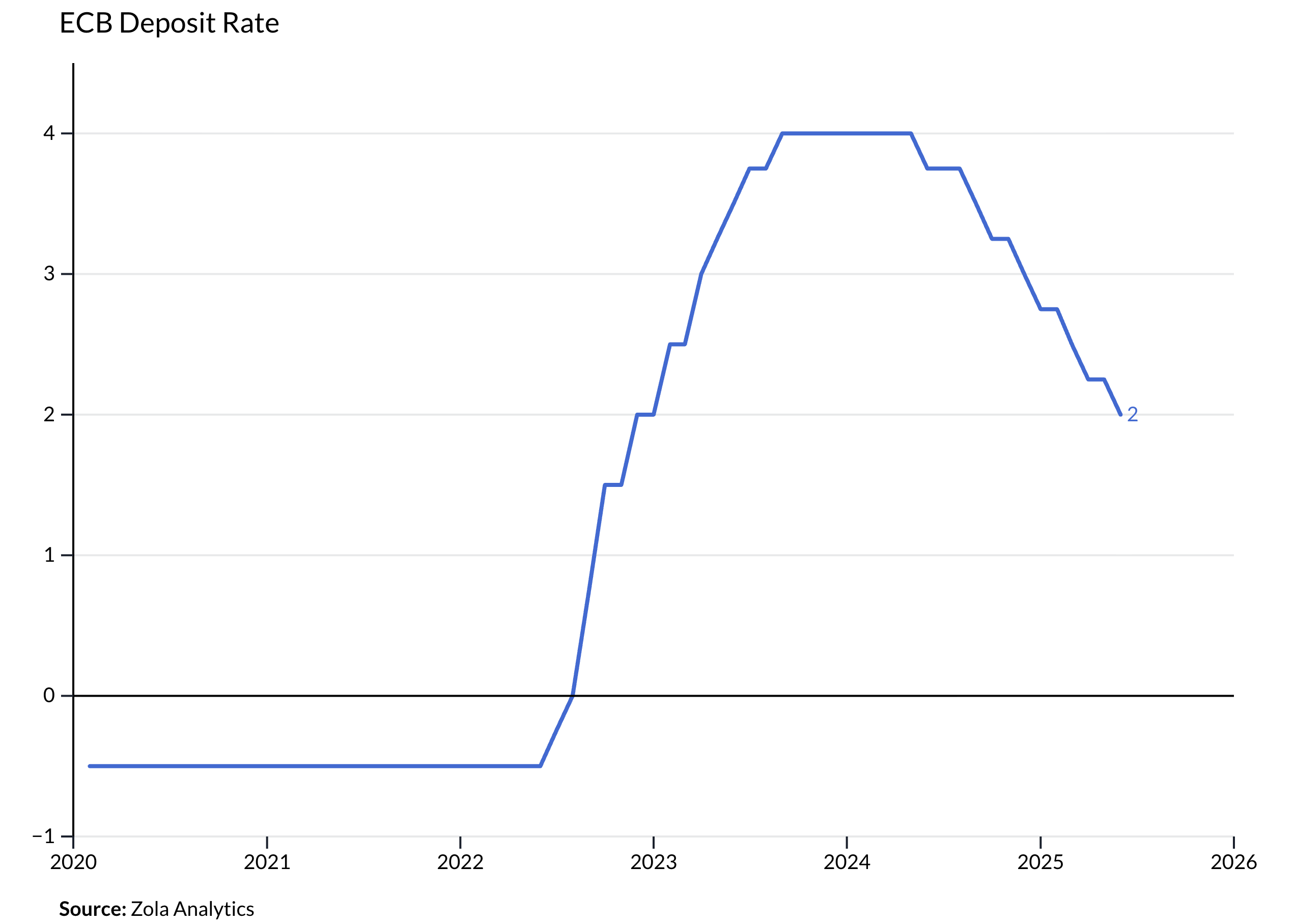

On 5 June, the European Central Bank delivered a widely anticipated 25 basis point cut, bringing the deposit rate down to 2.0%. This marks the eighth cut in the current cycle, and while it represents a symbolic halving from its peak of 4.0%, the ECB stopped short of declaring victory or signalling an end to the easing process.

The question now facing markets is whether this move is the last of the cycle or simply a pause dictated by prevailing uncertainties.

Cautious Optimism

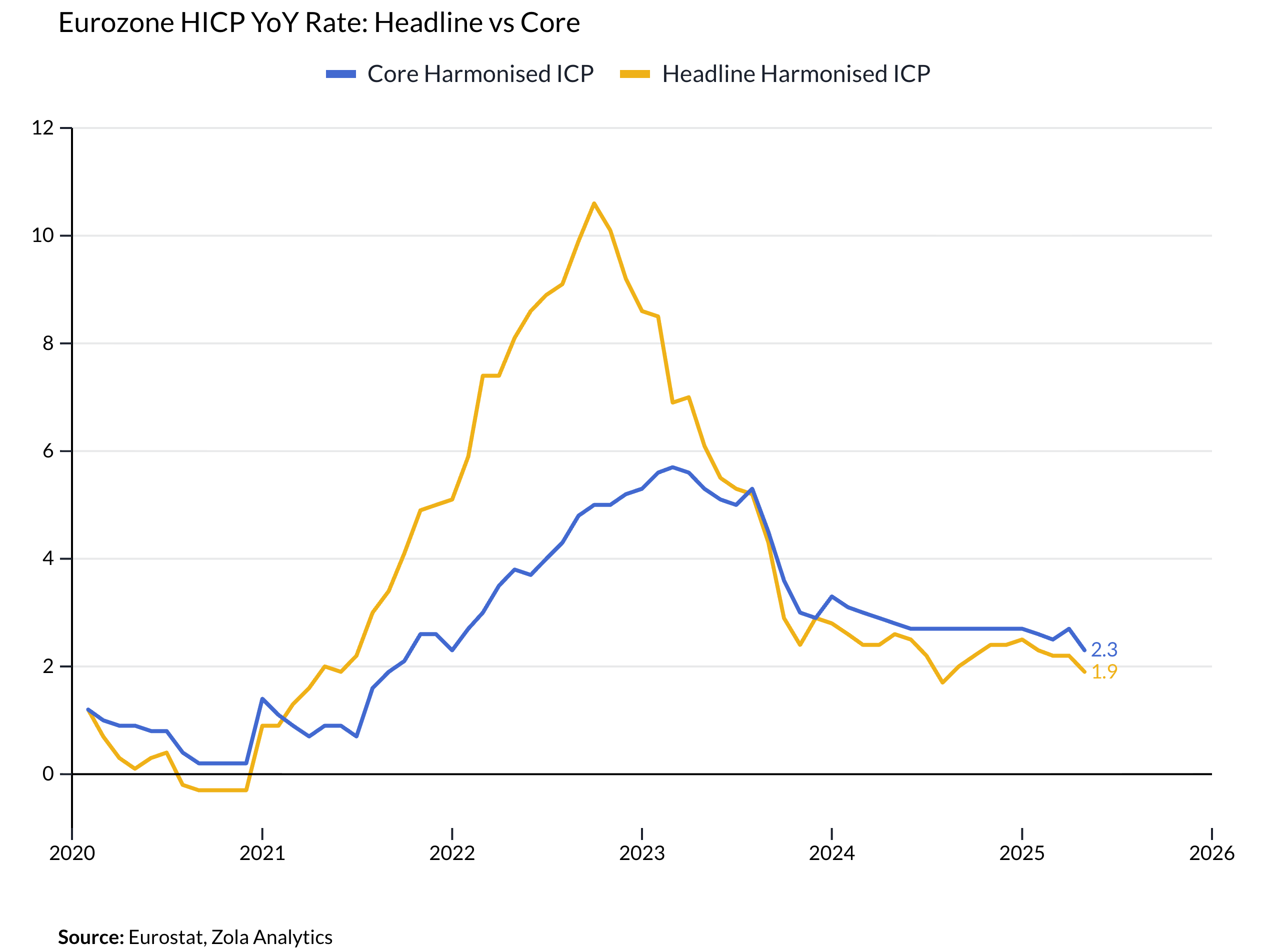

ECB President Christine Lagarde acknowledged that the euro area may be nearing the end of its monetary policy adjustment, but she refrained from offering definitive guidance. The revised staff forecasts show headline inflation falling to 2.0% this year and dipping to 1.6% in 2026, largely thanks to a stronger euro and significantly lower energy prices. However, core inflation remains more persistent, staying above 1.9% through 2027.

This divergence between headline and core measures highlights the ECB’s dilemma: inflation is moderating, but the structural components are proving stickier than ideal. The signal is clear—further easing may not be justified unless inflation convincingly falls below target.

A Global Context: Trade and Tariffs

Adding to the complexity is the external environment. The ECB’s models now incorporate scenarios with heightened global trade tensions, particularly from a US tariff regime shift. In the more severe scenario, inflation is expected to undershoot the 2% target through 2026 and 2027.

This reinforces the view that tariff-driven disinflation—through weaker demand and squeezed corporate margins—can reduce the need for central banks to provide additional monetary support. But it also introduces fresh uncertainty, especially as policymakers must balance risks of undershooting inflation against the potential for future price pressures from supply chain fragmentation and increased defence and infrastructure spending.

Market Response and Strategic Positioning

Markets reacted swiftly. EUR/USD rose towards 1.15 on the back of Lagarde’s comments about approaching the end of the policy cycle, while bond yield curves responded with renewed flattening. The lack of clear forward guidance kept speculation alive, particularly regarding the July meeting.

From a strategic standpoint, the ECB is treading a delicate path. Cutting too aggressively could trigger euro appreciation—especially if the moves are seen as front-loaded—and lead to capital outflows, particularly if other major central banks remain on hold. But pausing too early could leave the eurozone vulnerable to stagnation if global demand continues to falter under the weight of tariffs and uncertainty.