Published June 11th 2025

May US CPI: A Pre-Covid Vibe — For Now

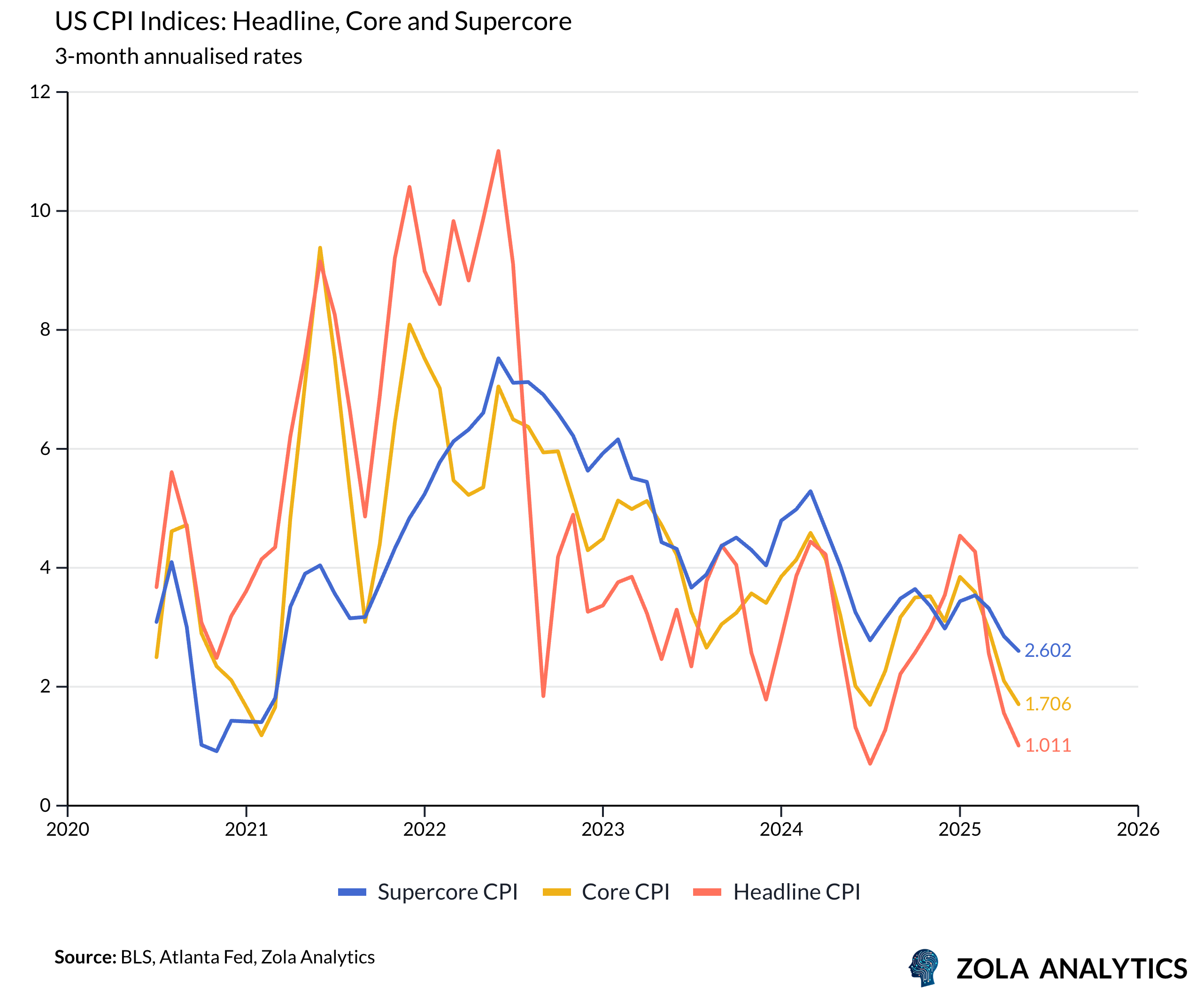

The May 2025 US Consumer Price Index (CPI) report delivered a rare and welcome surprise: inflation appears to be behaving itself. Headline CPI rose just 0.1% month-over-month, versus an expected 0.2%, and core CPI matched this softness at 0.1%, well below the 0.3% consensus forecast. Even more notably, the "supercore" component—a measure of sticky services inflation closely watched by the Federal Reserve—was up only 0.06%.

There was no evidence of passthrough in goods prices, despite expectations that recent tariff hikes would begin to bite. This suggests that any tariff-related cost pressures have yet to filter through to consumers. In the services sector, inflation was subdued as well, with continued softness in shelter costs and notable declines in transportation prices, particularly airfares.

Together, these developments make this CPI print resemble the kind of inflation data last seen before the pandemic. This softness confirms broader market expectations that consumer hesitation, downward rigidity in pricing, and a subdued labour market would suppress price pressures. Importantly, there are still warnings that the full inflationary impact of tariffs has yet to feed through—a concern tied to the delayed pass-through effects of recent trade policy shifts.

Despite these caveats, the immediate implication of May's print is clear: inflationary pressures are moderating. Market reaction was swift, with expectations of a Fed rate cut by September gaining traction. Yet, the Federal Reserve is unlikely to pivot quickly. Policymakers are well aware that tariff-related inflation may still surface in the coming months, and that one soft print does not constitute a trend.

The Fed’s current stance is one of data-dependent caution. It will likely hold rates steady through the summer, watching for consistent evidence that inflation is durably converging with its 2% target. If upcoming CPI reports corroborate May’s benign tone, a dovish shift could materialise by early autumn.

In sum, the May CPI report is a breath of fresh air for markets and policymakers alike. But it is only one chapter in a longer story—a story still complicated by geopolitical shocks, supply constraints, and the uncertain lag of tariff effects. For now, at least, the inflation genie seems back in the bottle, though risk-off moves can explode if the calm proves short-lived.