Published 31th October 2025

9 minute read

One Last Tango

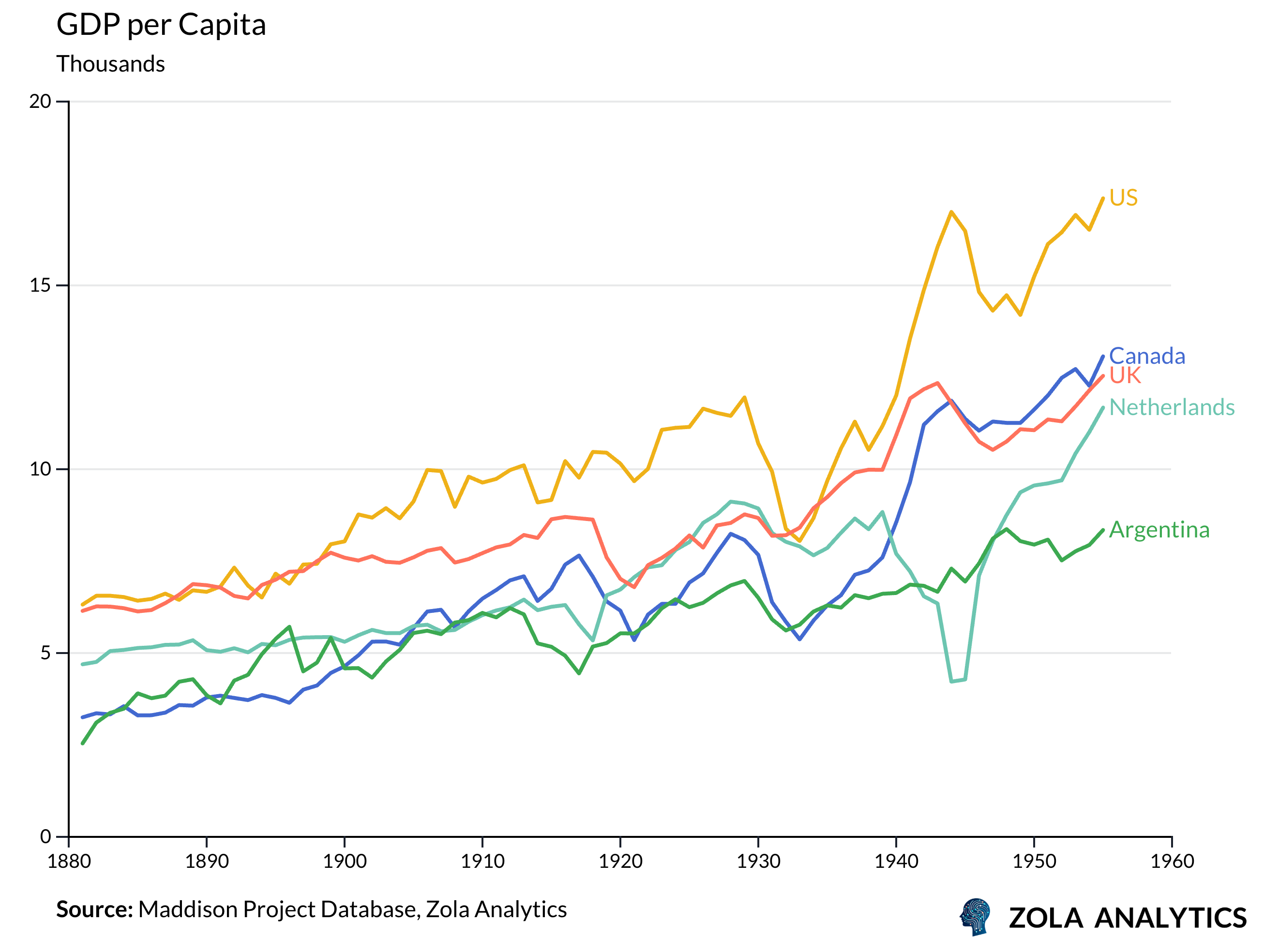

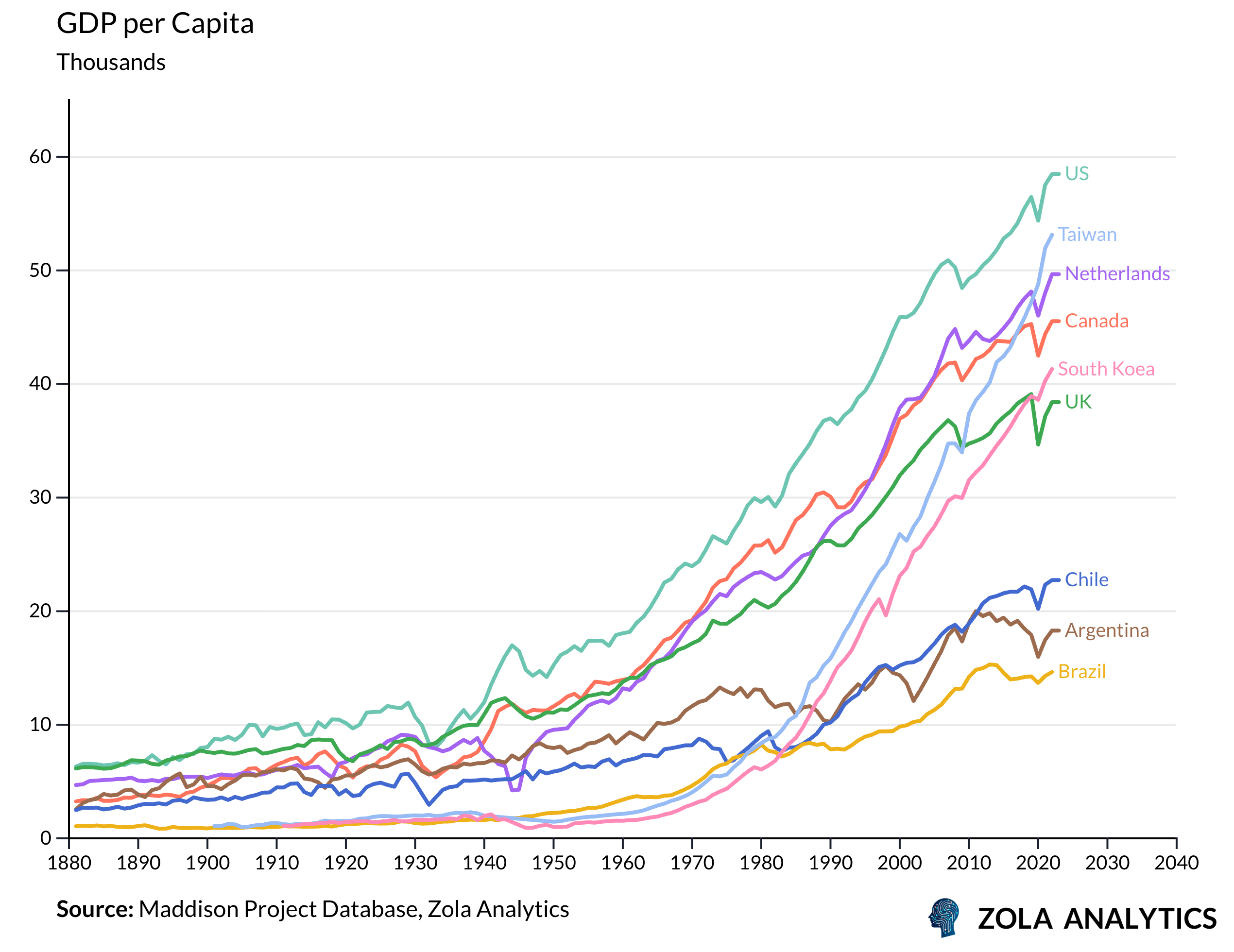

In the milongas of Buenos Aires, elderly dancers sometimes speak wistfully of tango’s golden age, when the world’s finest orchestras filled grand ballrooms and Argentina’s cultural influence rivalled Paris or New York. The nation’s economy has traced a similar arc: from Belle Époque splendor to prolonged decline, punctuated by brief, passionate revivals that never quite recapture past glory. The country that entered the 20th century among the world's ten richest nations, wealthier than France, Germany, or Japan, has spent the subsequent decades cycling through familiar steps of crisis and recovery.

Like a couple locked in tango's abrazo, Argentina remains caught between opposing forces: the impulse toward free markets and the pull of state intervention, fiscal orthodoxy and populist spending, global integration and economic nationalism. As Javier Milei's government attempts yet another dramatic pivot, slashing the state and embracing radical liberalisation, the question remains whether Argentina can finally break this exhausting cycle, or whether the dance between boom and bust has become too deeply ingrained to escape.

The Age of Promise

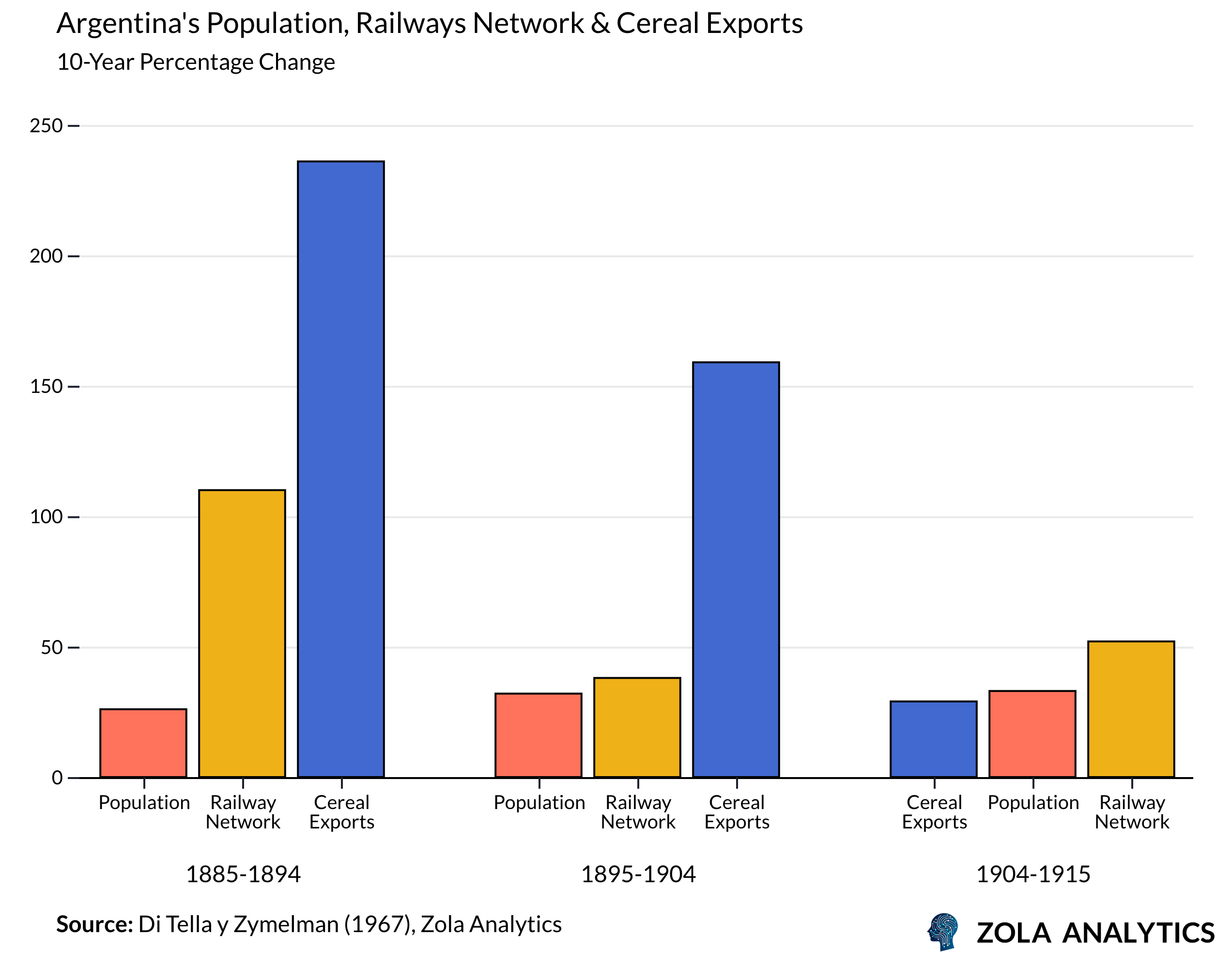

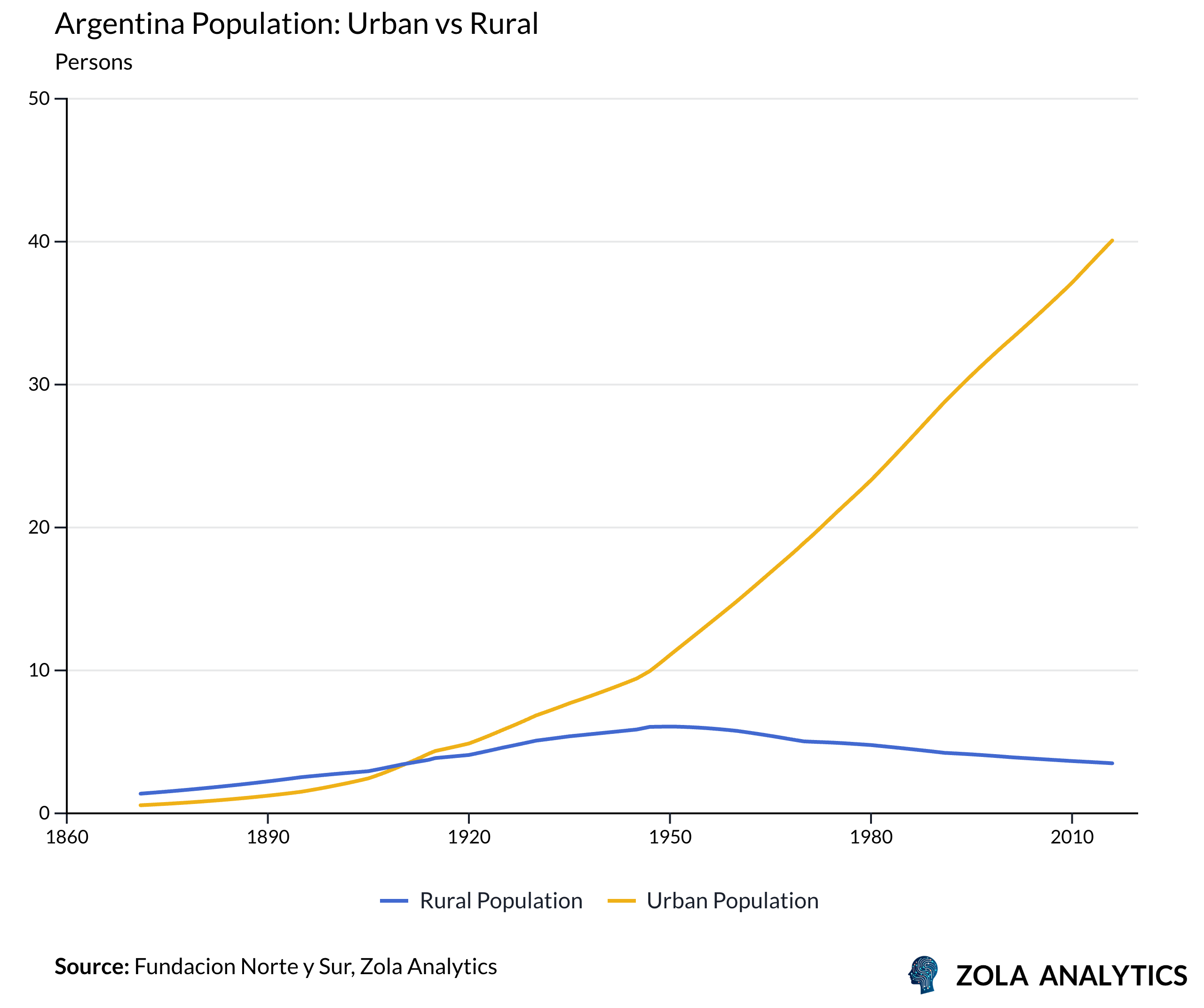

To understand how far Argentina has fallen, one must first recall how high it once stood. The Belle Époque decades between 1880 and 1913 was a period of confidence and expansion when the country stood among the world’s most prosperous nations. British capital financed the railways, ports, and stockyards that transformed the Pampas into one of the most productive agricultural regions on earth. Immigrants from across Europe arrived in search of opportunity, helping turn Buenos Aires into a modern metropolis of boulevards, parks, and electric trams.

Exports of beef, grain, and wool flowed to European markets, while real wages and literacy soared. By 1908, Argentina had overtaken Canada and the Netherlands in income per head and stood as Latin America’s undisputed leader.

First Fall

The First World War marked a turning point, exposing how dependent Argentina’s prosperity had become on external forces. With Britain drawn into conflict and global trade routes disrupted, capital inflows collapsed almost overnight. The country’s railways, ports, and ranches were suddenly starved of credit and export demand. The opening of the Panama Canal further diverted maritime traffic away from the South Atlantic, compounding Argentina’s isolation.

The deeper vulnerability was structural. Argentina’s success had rested on a narrow export base and foreign investment, not on industrial capability or technological innovation. When world demand for its agricultural goods faltered, there was little else to fall back on.

Political tensions grew as the benefits of earlier growth were unevenly distributed between landowners and workers. By the late 1920s, external fragility had converged with mounting domestic strain. The Great Depression then delivered the final blow, triggering a collapse in commodity prices, widespread bankruptcies, and a severe contraction in fiscal revenues. In 1930, the military overthrew the elected government, ending half a century of liberal democracy.

Building Walls

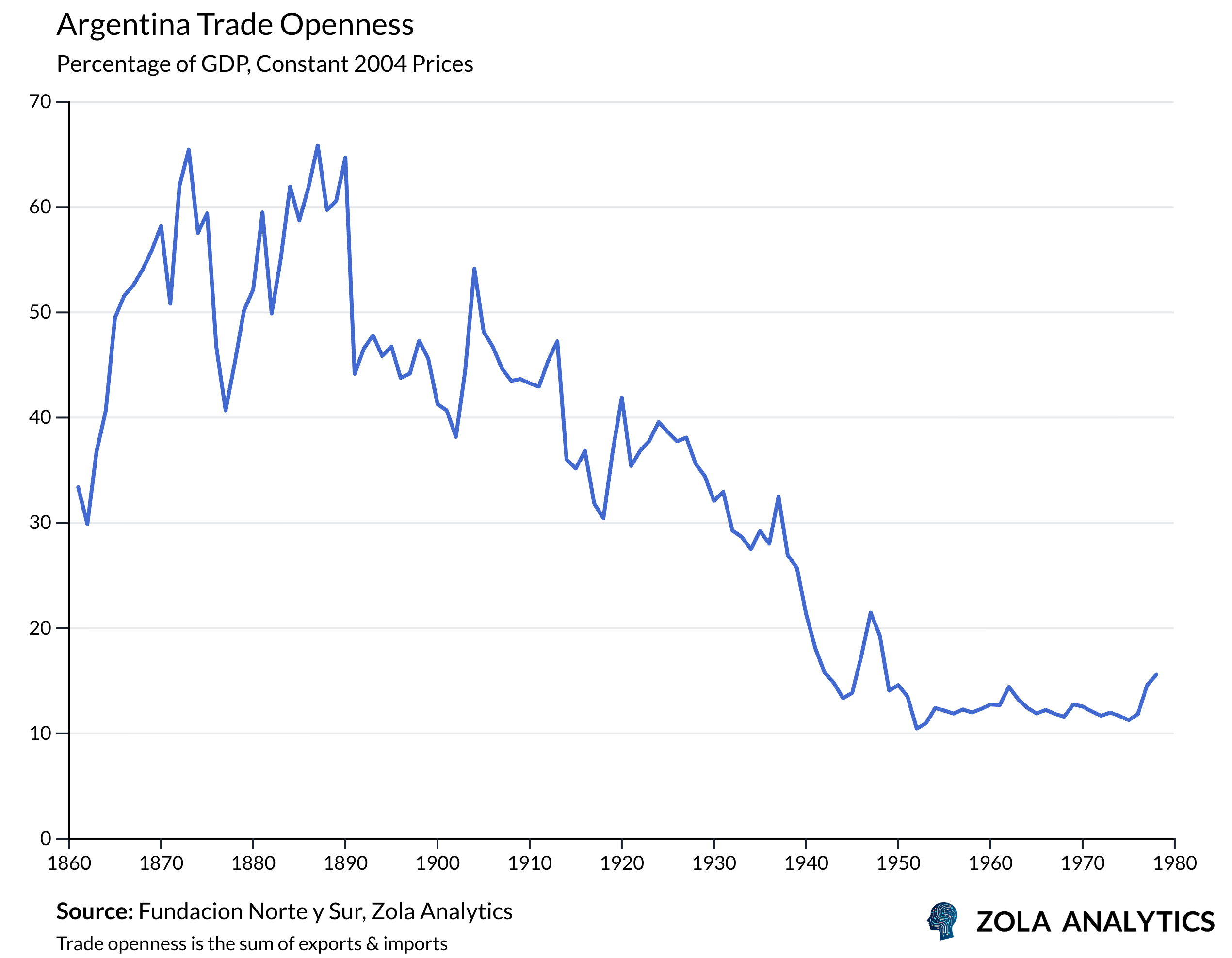

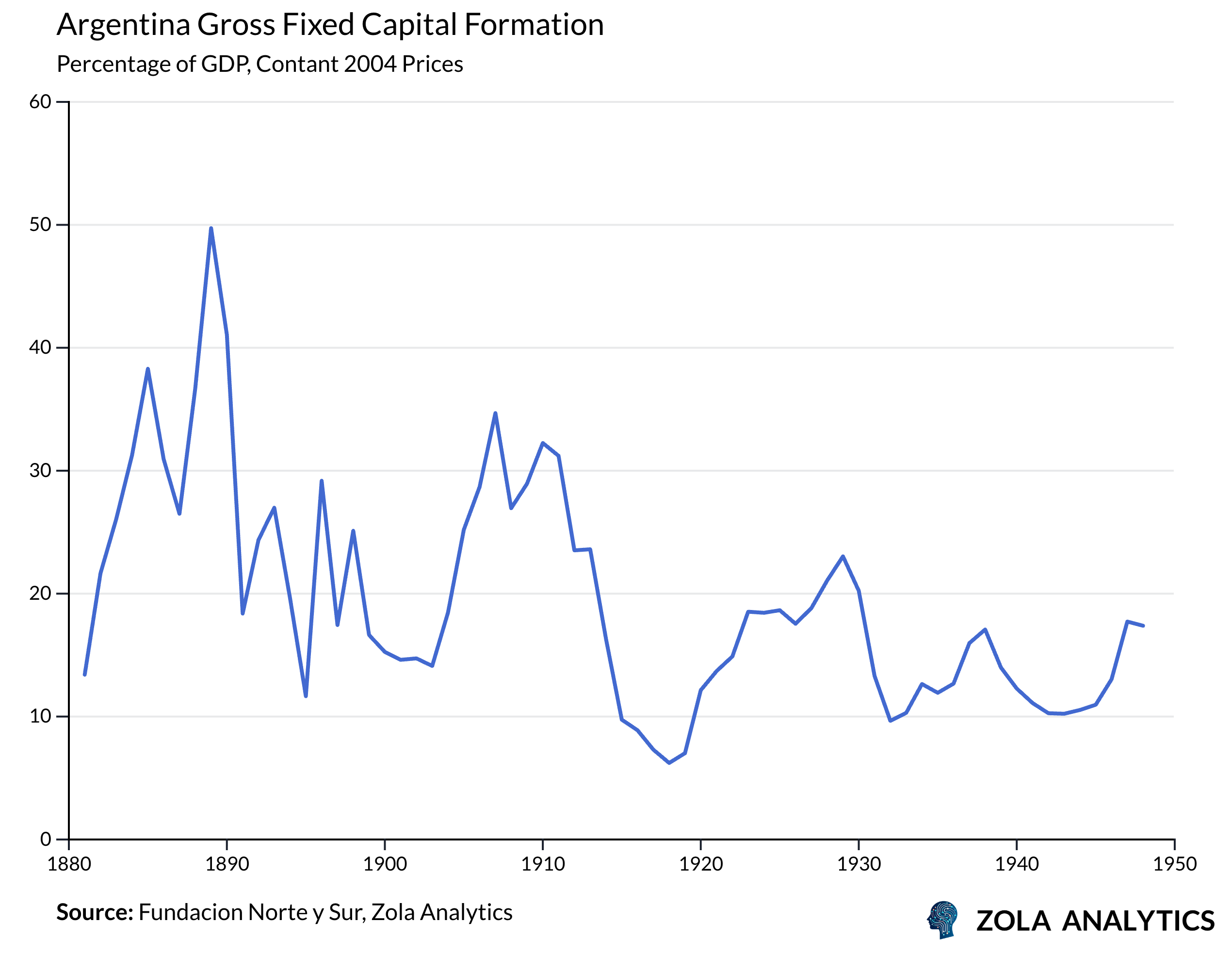

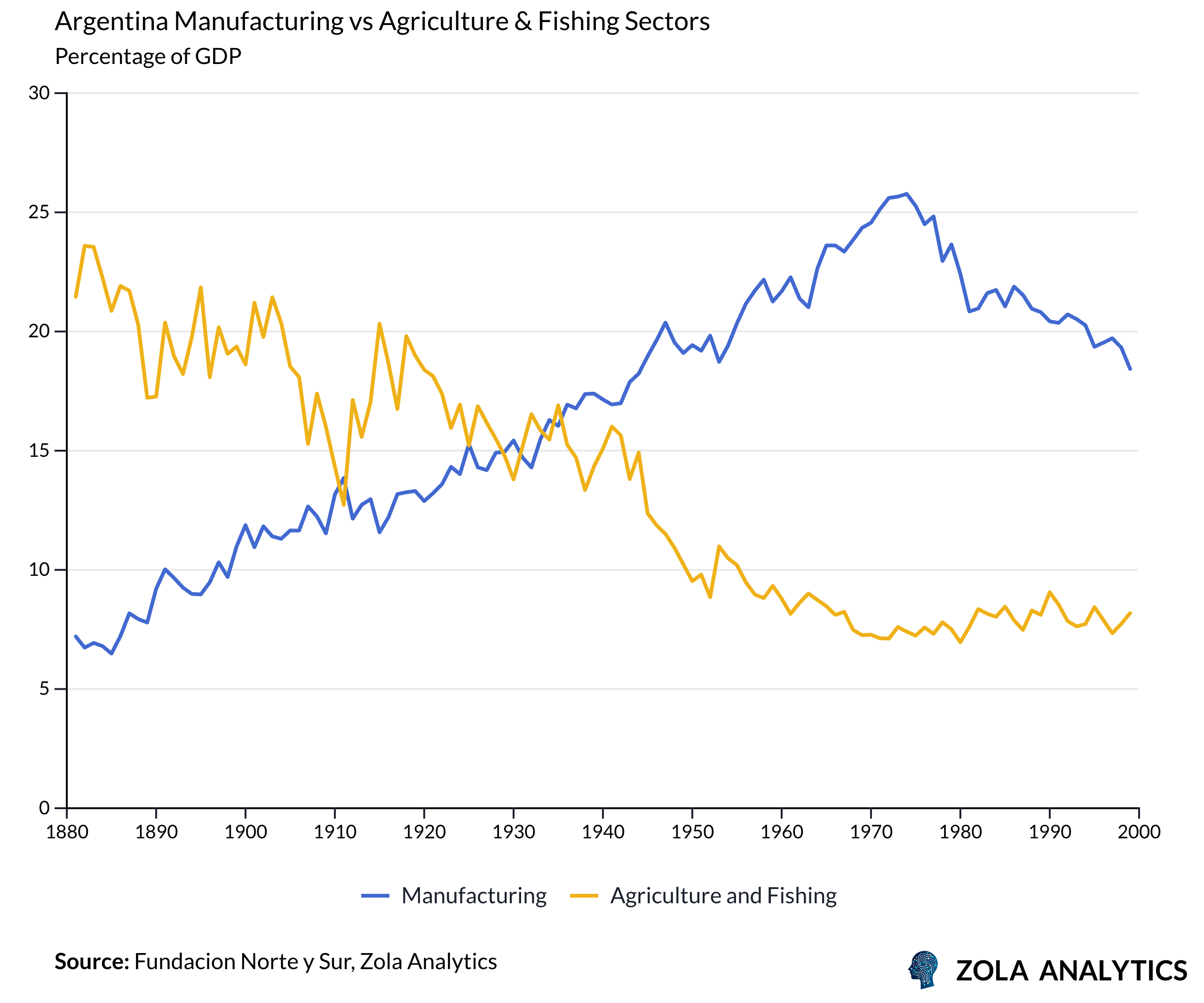

The new regime replaced export-led growth with import substitution industrialisation, seeking self-sufficiency by closing markets, nationalising key industries, and erecting high tariff walls. Initially, industrial output expanded and infrastructure projects flourished.

President Juan Perón’s government in the 1940s–50s pursued social justice through wage increases, labour protections, and social security expansion. Living standards rose, but so did fiscal deficits and inflation.

ver time, import substitution revealed its weaknesses. Protected domestic firms grew inefficient, corruption became entrenched, and the economy’s competitive edge vanished. Import barriers limited access to capital goods and technology, constraining productivity and deterring long-term investment.

By prioritising state control and inward production, Argentina undercut its most dynamic sector, agriculture, while urban migration swelled unproductive manufacturing hubs.

A Republic in Ruins

By the 1970s, stagnation was entrenched: output faltered, inflation accelerated, and repeated military coups deepened institutional decay.

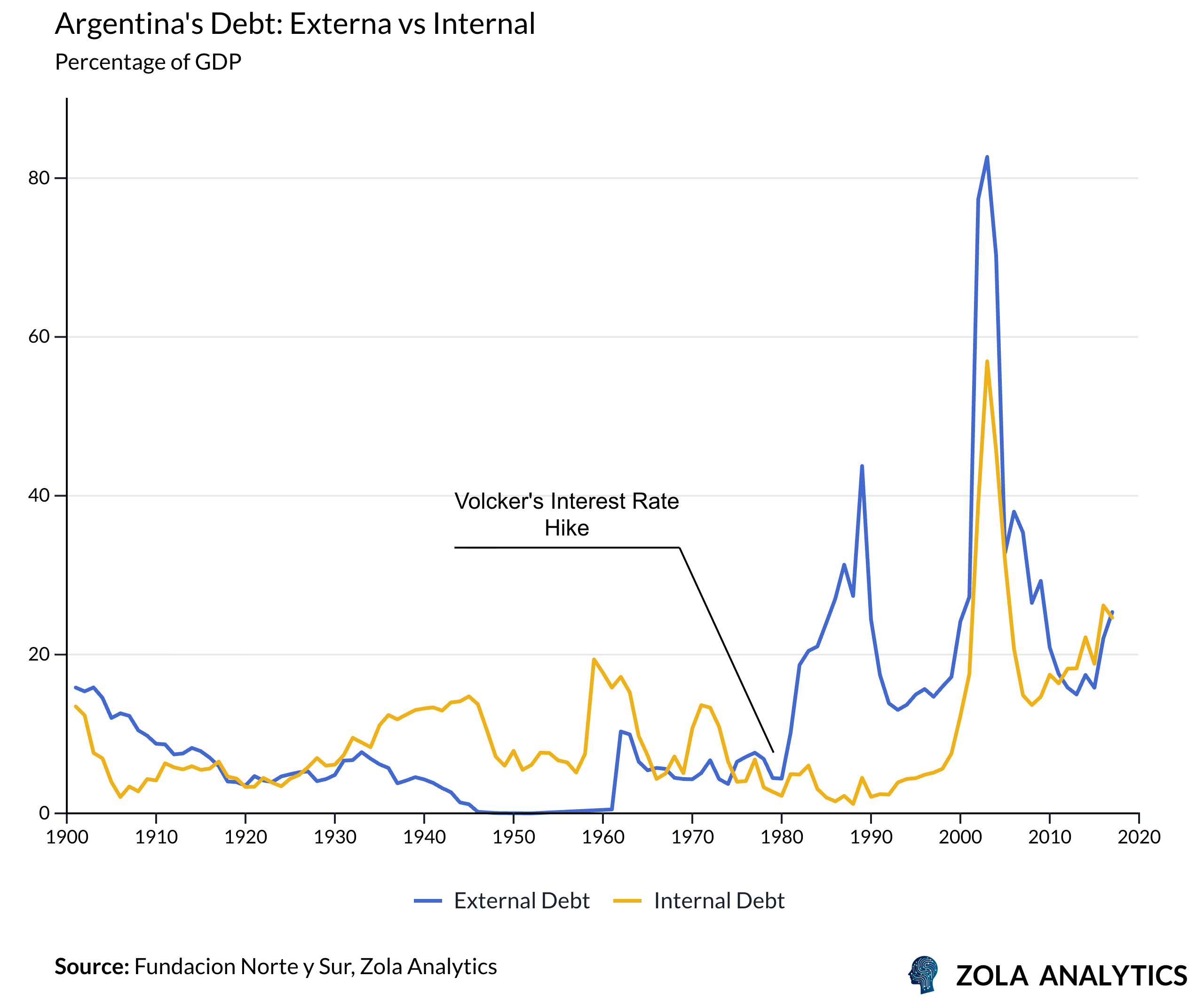

When policymakers attempted to liberalise trade in the 1970s, Argentine manufacturers could not survive in open markets. Industries that had grown behind tariff walls proved incapable of competing abroad. External borrowing soared, capital fled, and repeated devaluations destroyed purchasing power, erasing decades of progress.

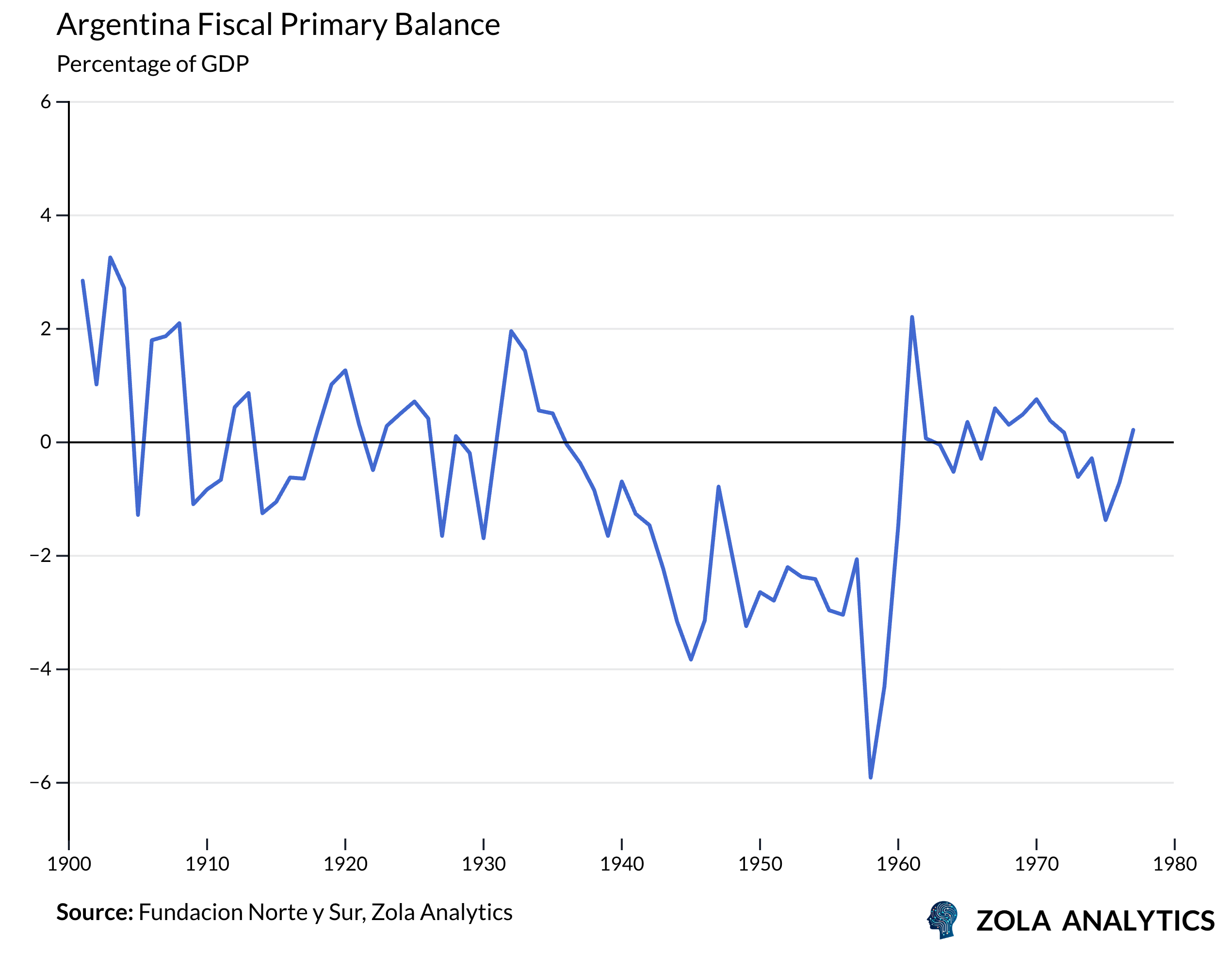

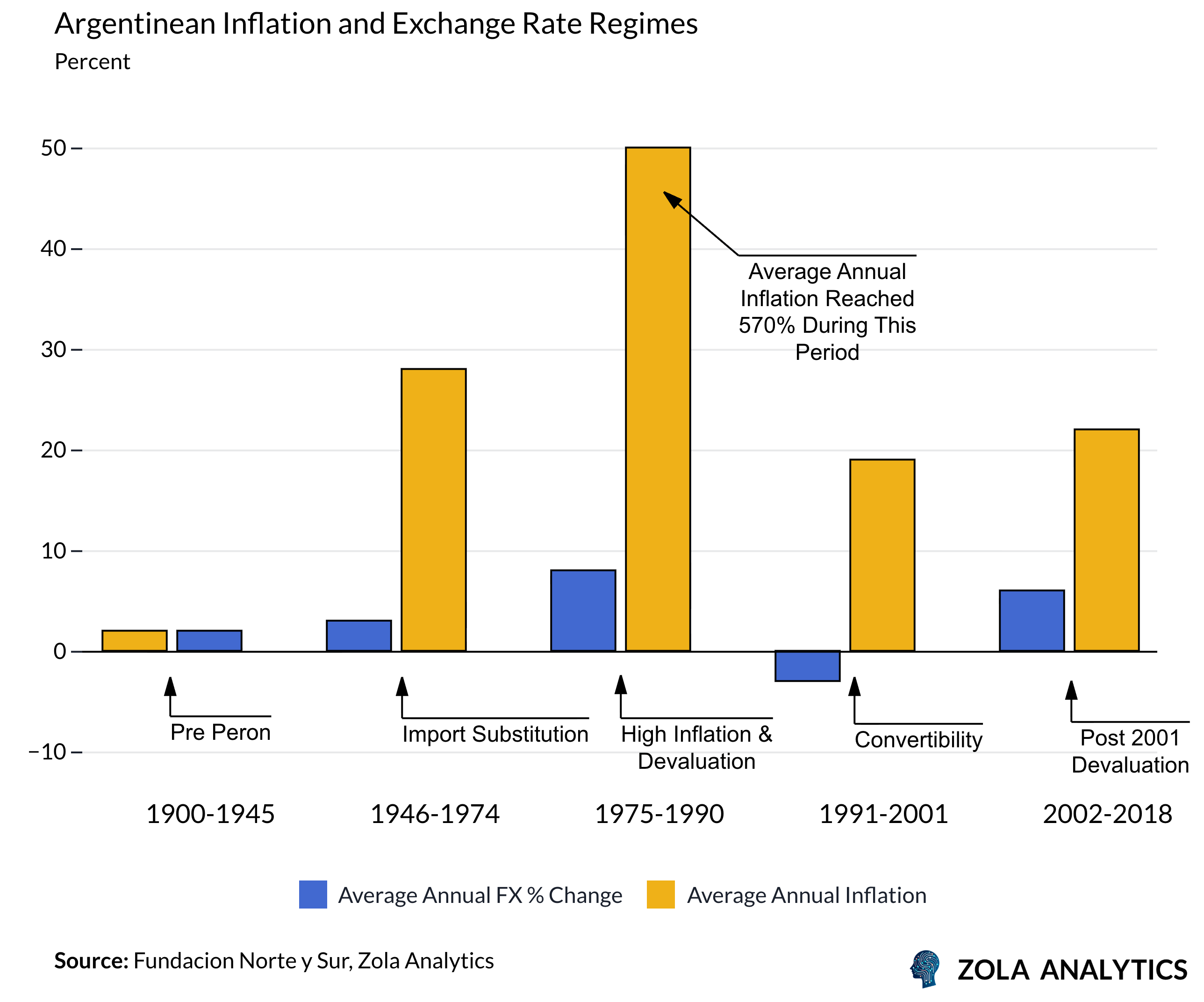

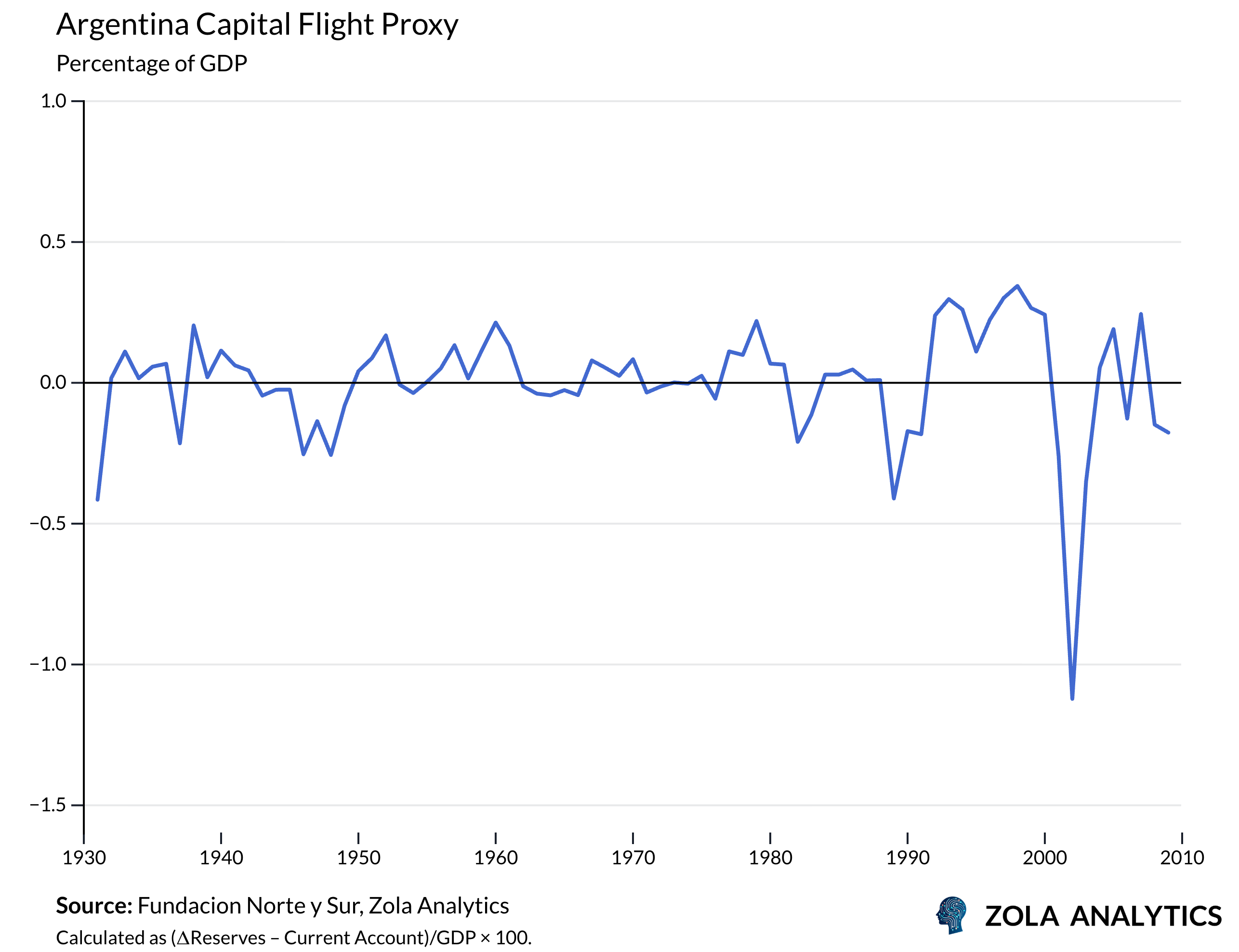

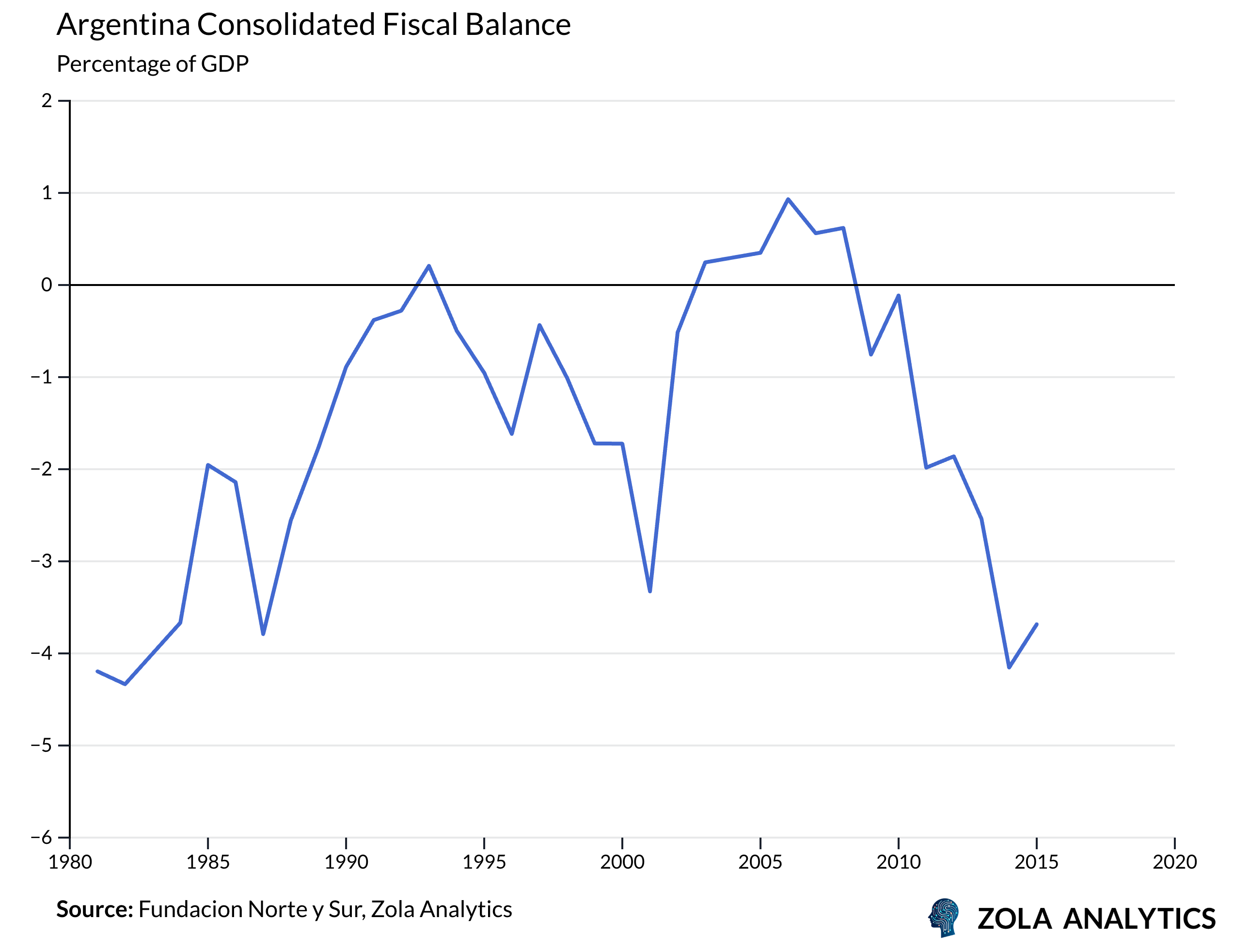

External debt rose from about 3.6% of GDP in 1974 to 44% by 1989. Easy foreign credit in the late 1970s turned disastrous after the Volcker tightening, which sent global interest rates and the dollar sharply higher. Servicing costs soared, capital inflows reversed, and the peso collapsed. As the government absorbed private dollar debts, money creation accelerated to cover fiscal shortfalls, setting off a spiral of inflation, devaluation, and capital flight that culminated in the hyperinflation of the late 1980s.

Political volatility reached extremes: thirteen presidents and twenty-one economy ministers in less than two decades. By the late 1980s, the state’s capacity to govern the economy had effectively disintegrated. Inflation surged into the five-digits, wiping out savings and wages alike. The 1989 riots, triggered by food shortages and collapsing confidence, symbolised the complete breakdown of the state’s economic authority. Argentina, once a model of prosperity, had become the “sick man” of Latin America.

Stability at Any Cost

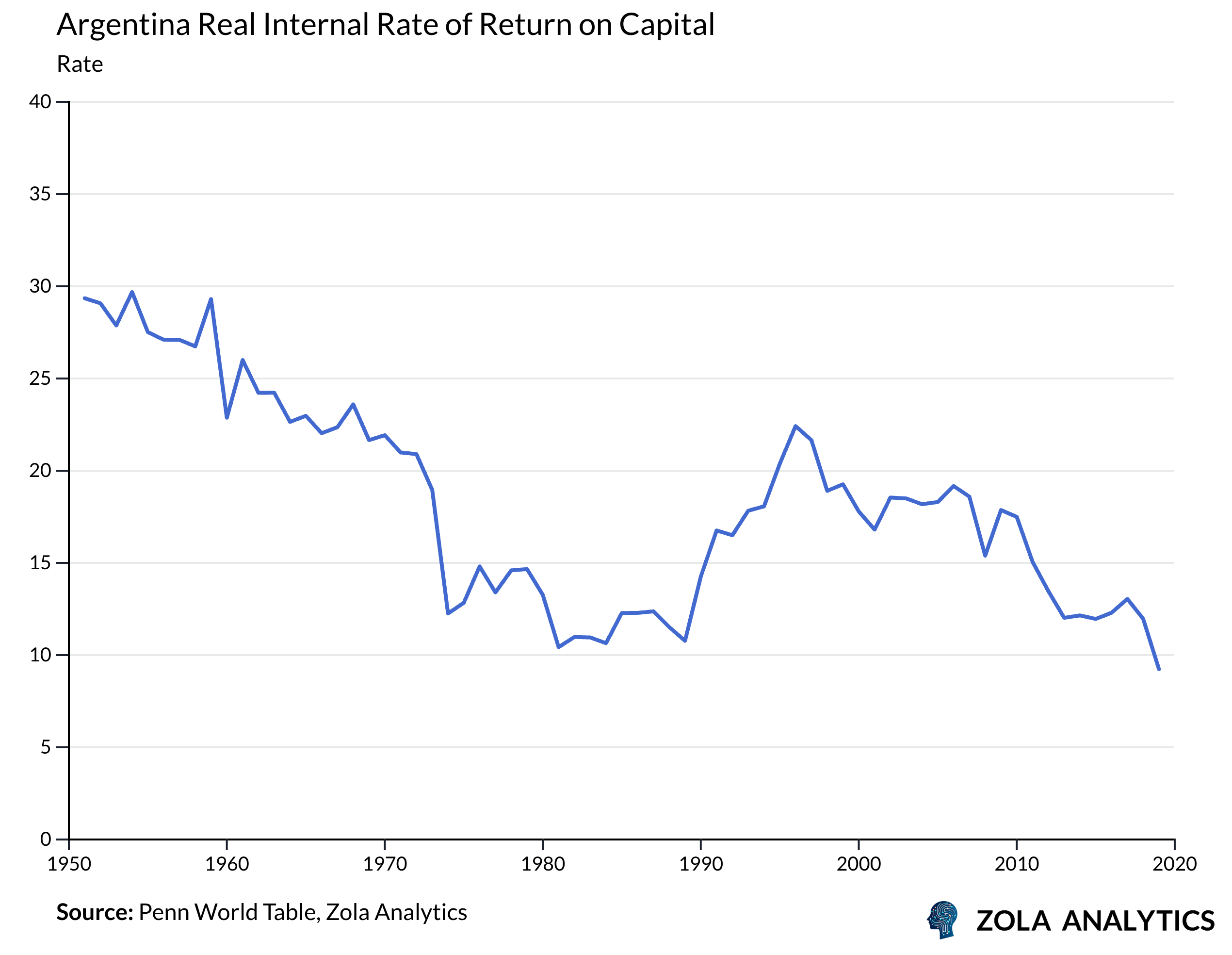

In response, the government introduced a currency board, pegging the peso one-to-one with the US dollar. Inflation collapsed, investment returned, and confidence briefly recovered. But the fix came at a high price: the loss of monetary flexibility left Argentina unable to respond to recession through devaluation. After a series of external shocks during the EM crises of the 1990s, the fragility of the regime was exposed. As pressures mounted, capital flight and bank runs culminated in the 2001 default. The peso collapsed, GDP fell by 20%, unemployment exceeded 25%, and more than half the population fell below the poverty line.

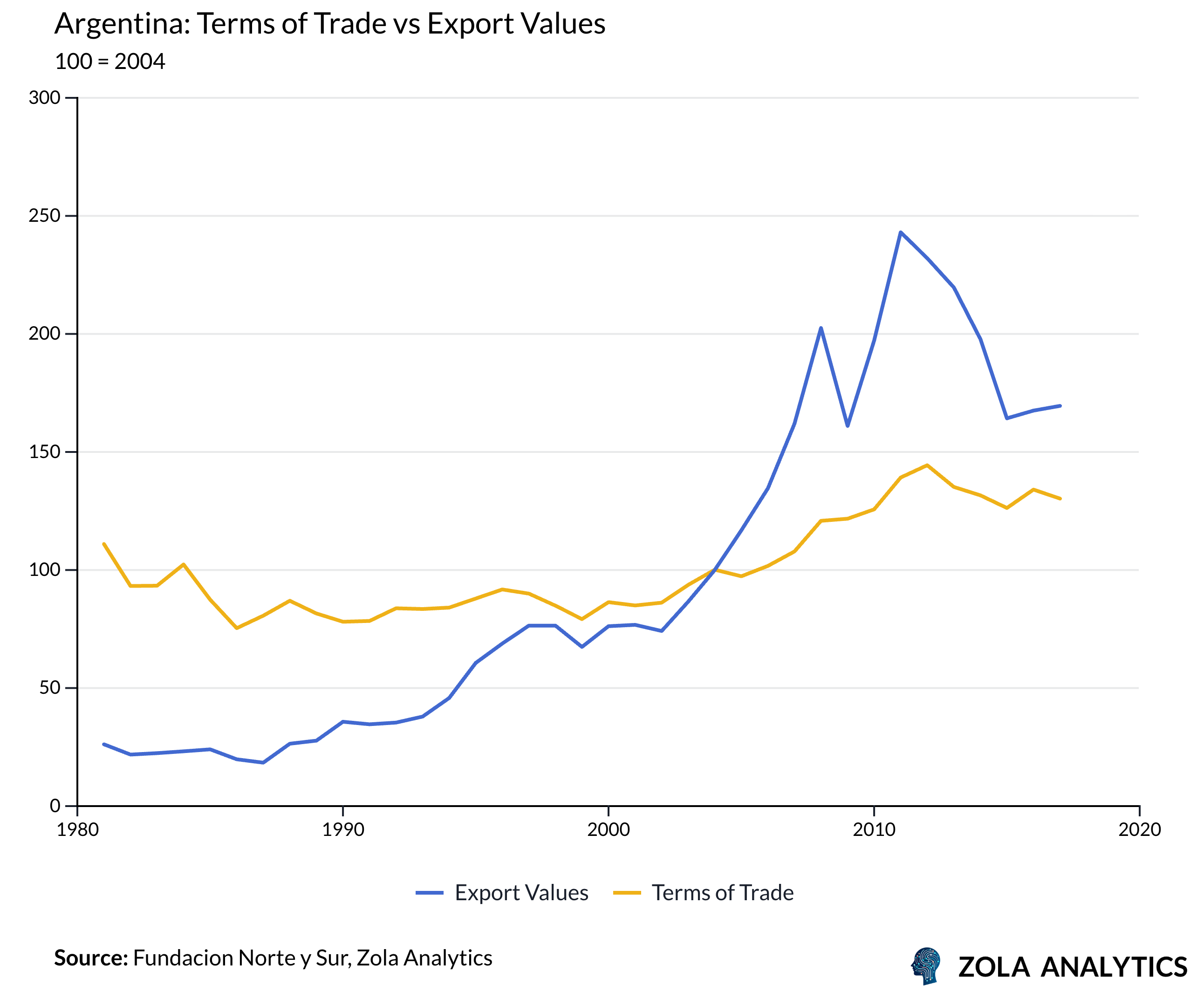

Luckily for Argentina, the global environment turned remarkably favourable in the early 2000s. China’s accession to the World Trade Organisation in 2001 unleashed a surge in demand for food, energy, and raw materials, lifting world prices for soy, maize, and other key Argentine exports. The peso’s steep devaluation amplified these gains, restoring competitiveness and generating a powerful trade surplus.

Yet instead of consolidating the fiscal base and broadening the productive structure, policy channelled the windfall into current spending and social transfers rather than investment.

By the mid-2010s, Argentina’s economy displayed chronic middle income stagnation, marked by weak productivity, shallow capital markets, poor export competitiveness, and persistent inflation. Living standards sustained political expectations but not growth, as social spending crowded out investment and infrastructure renewal.

A Leap of Faith

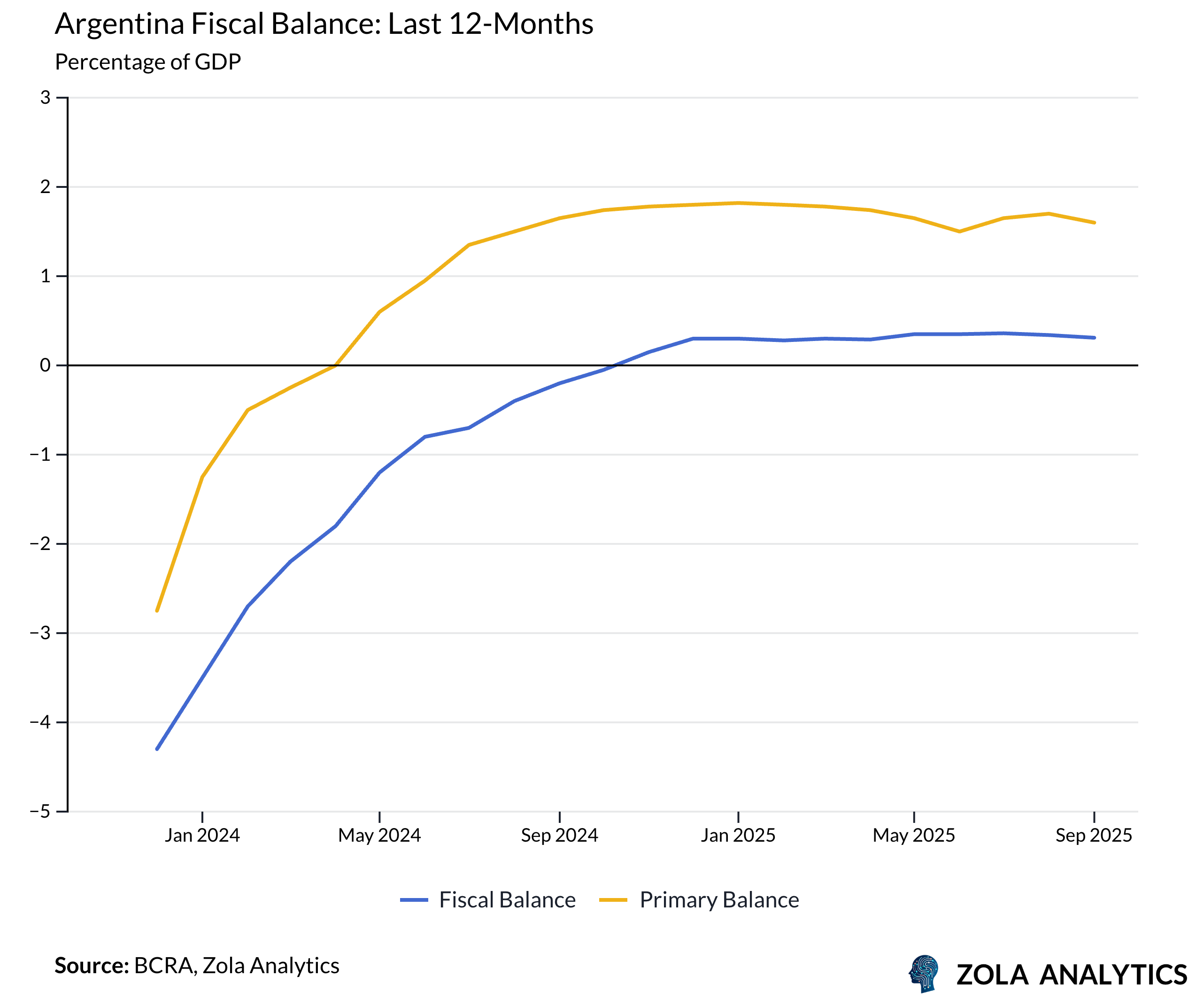

The reforms of the early 2020s mark not just another attempt to end Argentina’s long cycle of instability, but a radical break from the past. Javier Milei’s government has moved with unprecedented speed, slashing state spending, dismantling currency controls, and pushing through liberalizations that previous administrations only dared to whisper about.

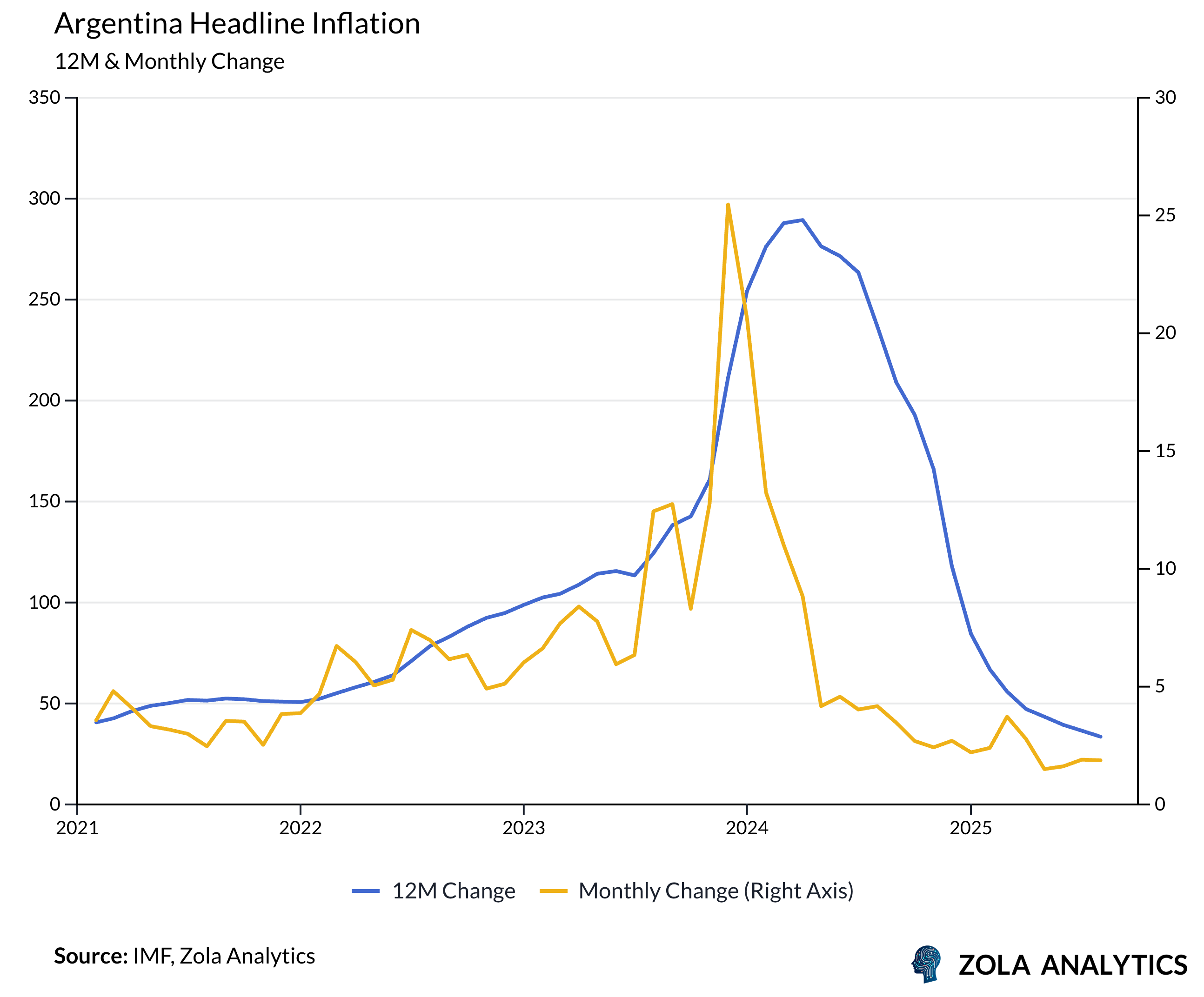

The results are now visible: inflation has plummeted from its vertiginous heights, and international confidence is returning with a cautious but palpable optimism. Yet for all the boldness of Milei’s approach, the question lingers: can Argentina finally escape the exhausting dance between boom and bust, or is this just another pivot doomed to repeat history?

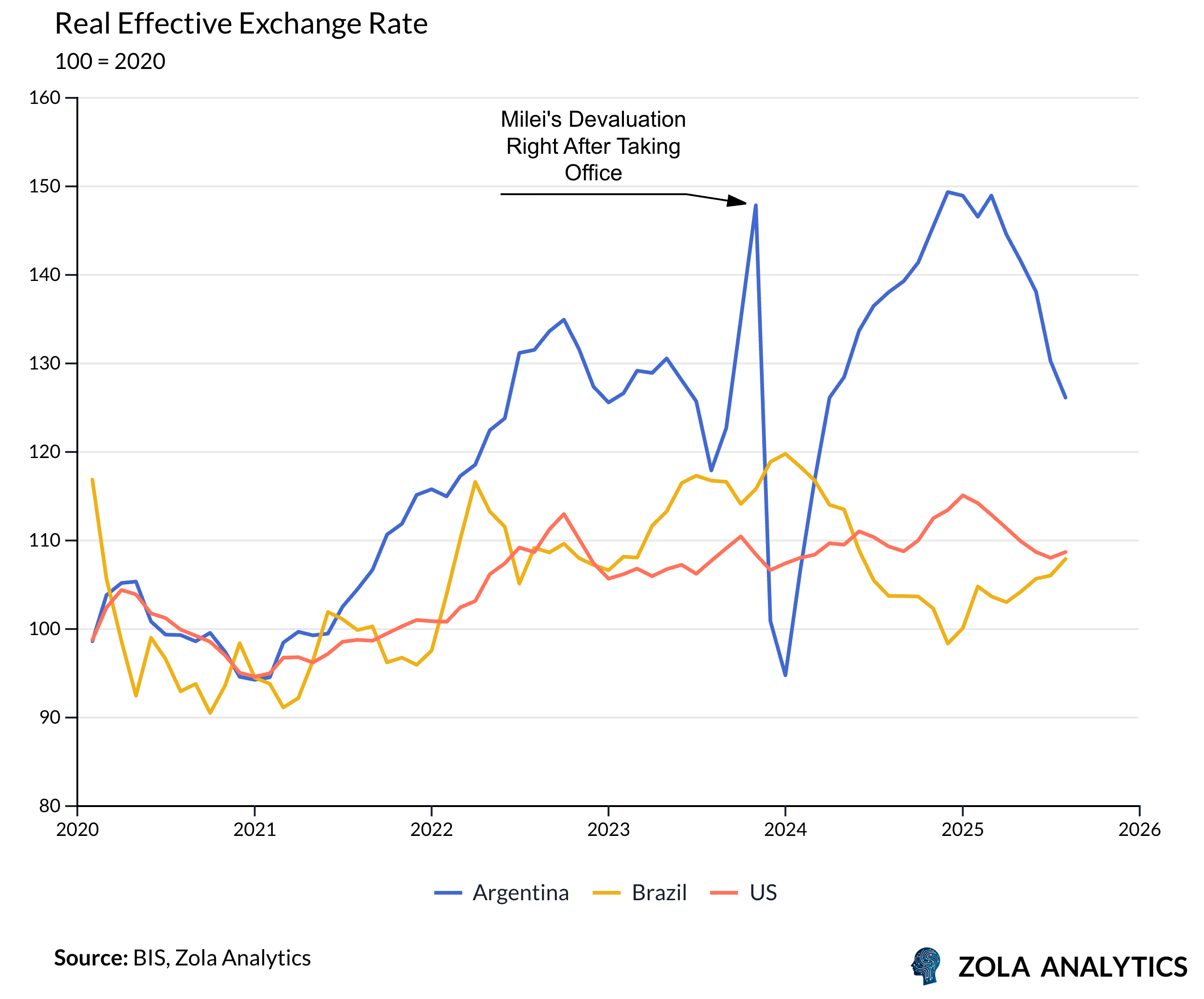

Milei’s project is unlike anything Argentina has seen in decades. It is not merely about balancing the books but about dismantling the economic and political structures that have trapped the country in decline. The agenda is sweeping: liberalizing labor and energy markets, gutting regulations, simplifying taxes, and, most controversially, redefining the role of the peso itself. Even after the sharp devaluation at the start of his mandate in late 2023, the crawling peg failed to keep pace with inflation, causing the real effective exchange rate to become as overvalued as when he took office.

A sudden move to a free float risks reigniting inflation and sparking a stampede into dollars, as Argentines, deeply conditioned to distrust their currency, seek refuge in greenbacks. A managed float, more closely aligned with inflation and market realities, may offer a more pragmatic path, allowing the peso to adjust gradually without succumbing to speculative pressure or losing competitiveness.

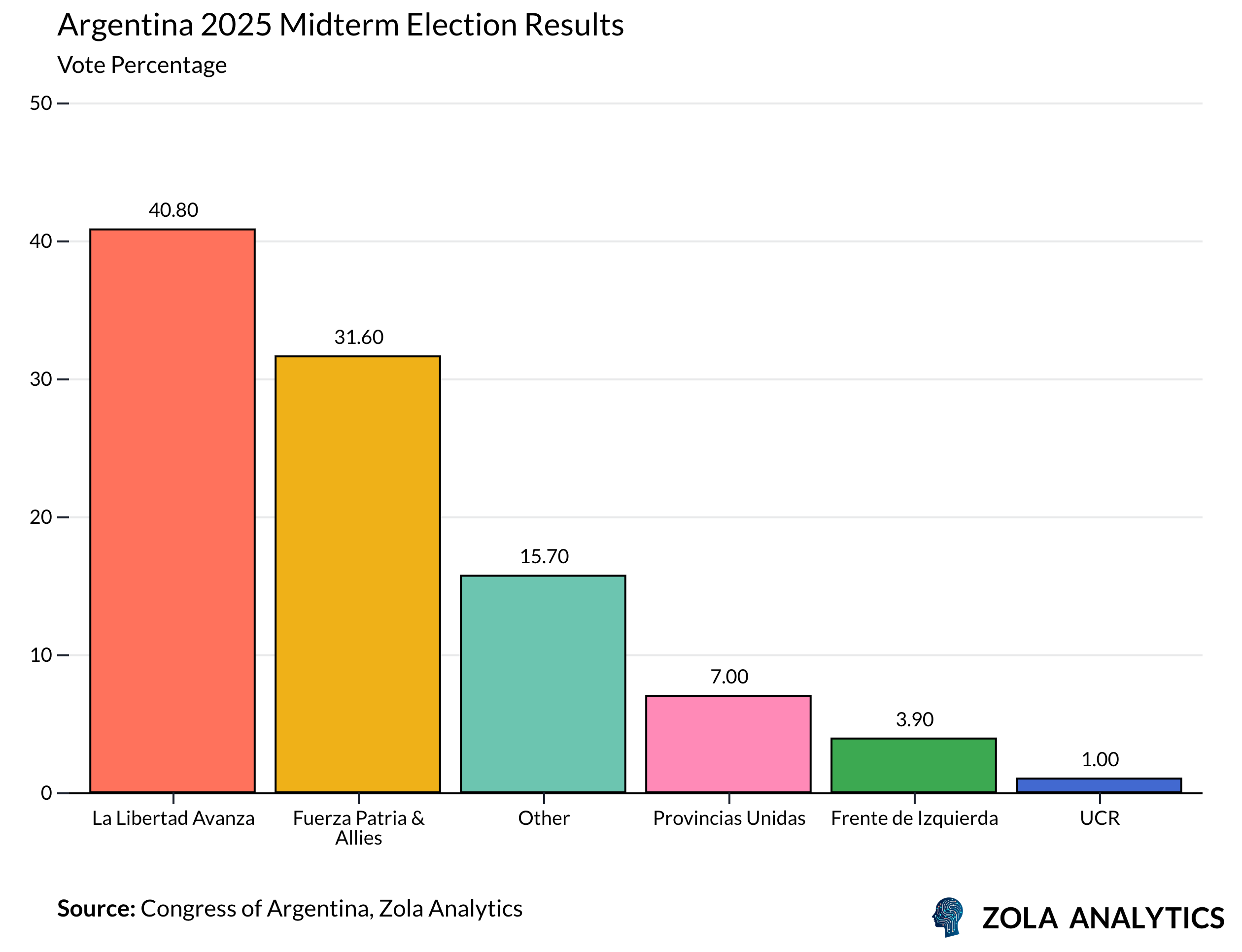

The midterm election results have strengthened Milei’s hand. His libertarian coalition, La Libertad Avanza, secured more than 40% of the national vote, giving them the political leverage to negotiate alliances with moderate provincial blocs, widening the path for legislative progress and deepening reform.

Success now hinges on three factors. The first is a credible monetary anchor, whether a crawling peg or a dirty float, that balances flexibility with stability. The second is rapid progress on liability management, ideally with US Treasury backing, to reduce the risk premium on peso-denominated debt. The third is visible improvement in living standards, to convince Argentines that the state can deliver more than just austerity.

Borges wrote that “every nation imagines itself; Argentina perhaps imagines itself more than most.” If Milei’s government succeeds in converting its mandate into enduring reform, Argentina may at last begin to move beyond its long cycle of imagination and disappointment. If not, the tango of boom and bust will play on, and the peso’s latest devaluation will be just another verse in a song Argentines know all too well. This is Argentina’s best chance in a generation. The question is whether Milei can make it count.

Sign up to receive the Zola Global Macro Chartbook every week: https://www.zolaanalytics.com/insights?signUp