Published August 4th 2025

10-min read

A Faustian Bargain

In the annals of transatlantic relations, some moments reveal more than others. Last week's trade negotiations exposed a fundamental truth: when security meets sovereignty, the former invariably wins. What follows is an assessment of the price paid and the precedent set.

Who Do I Call If I Want To Speak To Europe

Jacques Delors once declared that Europe’s credibility in trade negotiations lies in Europe’s “ability to speak with a single voice and act in concert.” If true, Europe’s credibility took a sizeable dent last week as President von der Leyen travelled to Turnberry to kowtow before Donald Trump. France’s Prime Minister François Bayrou declared it “a sombre day when an alliance of free peoples…resigns itself to submission.”

Deep divisions between European member states weakened their bargaining position. France and Spain argued against capitulation but Germany and Italy favoured a fast deal; with Germany’s Chancellor arguing that “it’s better to act quickly and simply than slowly and in a highly complicated way.” In the end, Europe’s leaders decided that this was a battle not worth fighting. Instead, they have gambled that giving Trump a win on trade will keep the US engaged in Ukraine.

Such meek resignation has a cost. With no champions to defend it, the rules-based international order that undergirds European prosperity will wither away. The global trading system continues to fracture as the WTO's foundational Most-Favoured-Nation (MFN) principle, which ensures trade concessions offered to one partner must extend to all, faces increasing irrelevance. Major economies now pivot toward bilateral deals rooted in leverage, not law. It may be that Europe is simply too dependent on US security to resist Washington’s demands, but dependency is not destiny. The EU still presides over a EUR 17 trillion single market, the planet’s largest capital pool outside the United States, and a potent arsenal of regulatory instruments. By coupling those assets with coalitions, from Japan and Canada to Mercosur hold-outs, Brussels could have applied calibrated counter-pressure. Europe chose conciliation; it did not have to.

The Art Of The Possible

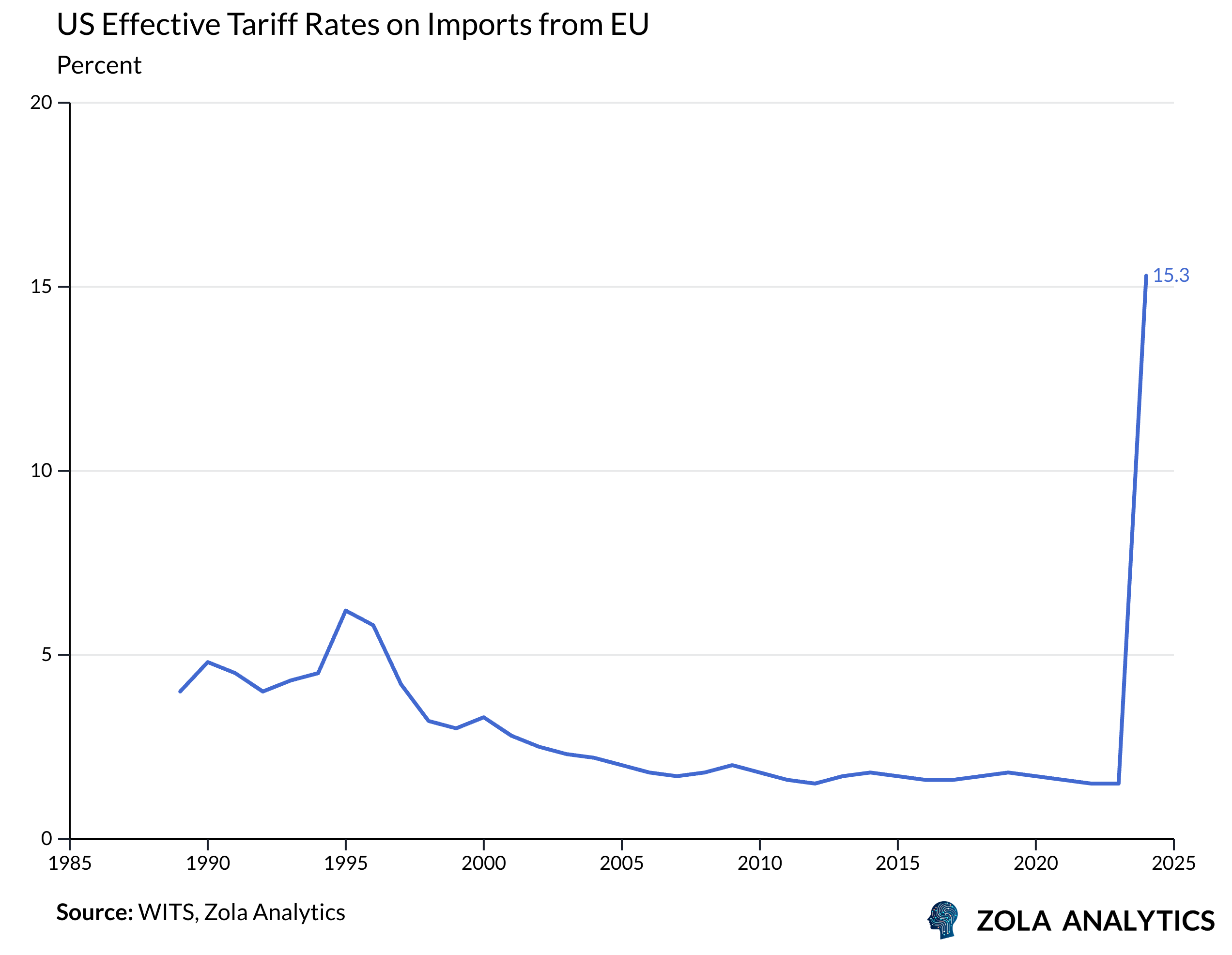

So what’s in the deal? Both camps spun it as a win: the US emphasised binding tariffs and investment pledges while the EU highlighted exemptions covering about 10% of goods, including aircraft parts, chemicals, generics, and natural resources.

Core Deal Components:

15% Flat Tariff: Applies to the vast majority of EU exports to the US, including automobiles and pharmaceuticals—down from threatened 30% but above the 10% markets had hoped for.

50% Metals Tariff: Steel and aluminum face punitive rates, though with unspecified quotas for relief (these represent only 1.5% of EU-US trade)

~10% Exemptions: Aircraft parts, select chemicals, generic drugs, and natural resources escape tariffs entirely—with EU promising to negotiate additional carve-outs over time

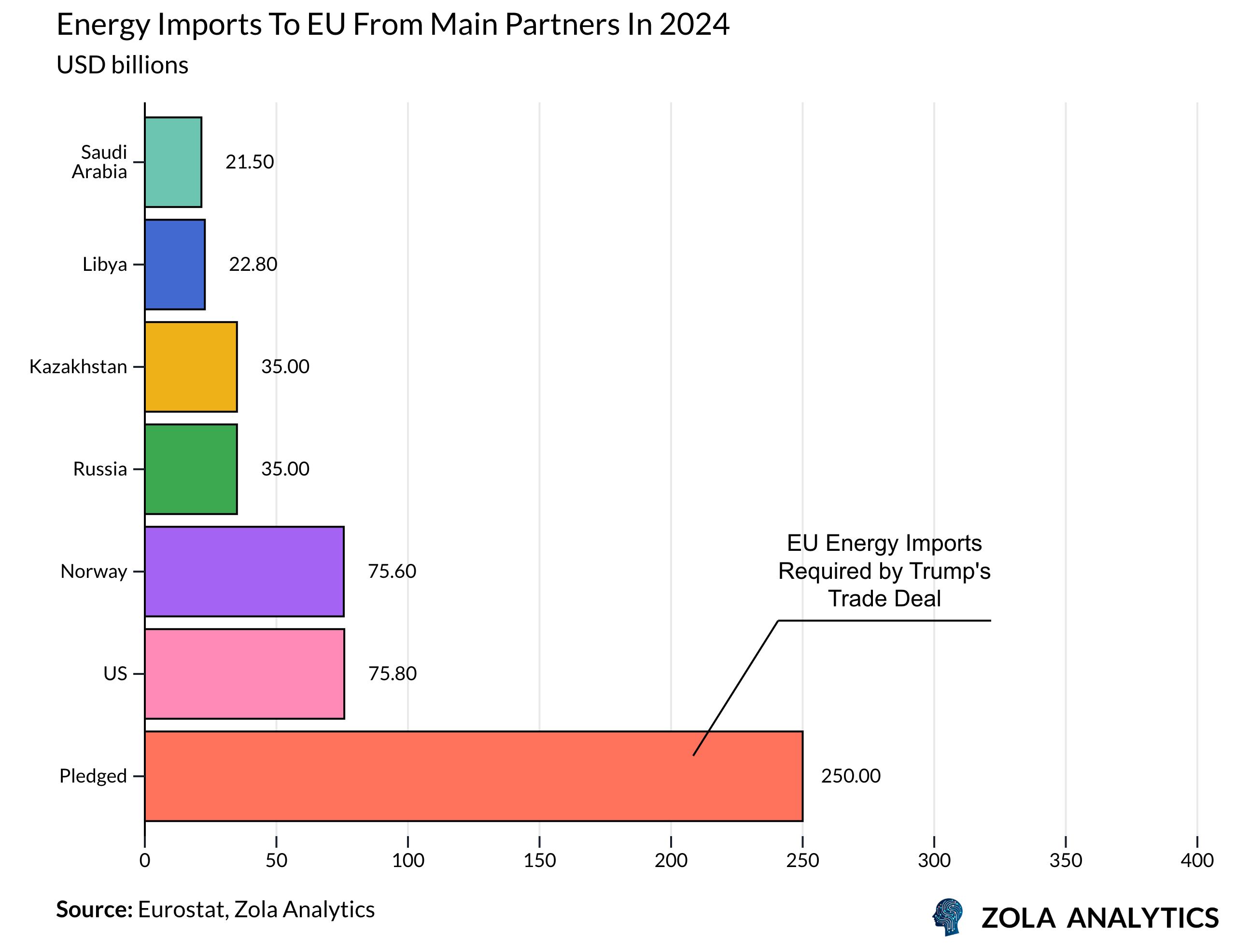

Energy & Investment Pledges: Europe commits to USD 750 billion in US energy purchases over three years and USD 600 billion in investment by 2029, figures that stretch credibility given physical and financial constraints.

View Chart in Zola Analytics

These pledges lack credibility. For one, the promised energy imports far exceed Europe’s import capacity.

The real question isn't whether Europe can absorb 15% tariffs, it is whether this rate will be a ceiling or a floor for future demands. By accepting asymmetric terms to preserve stability, Europe has demonstrated what can happen when security trumps sovereignty. Markets seeking certainty may be satisfied in the short run, but the tensions inherent in this deal will play out for years to come.

Tariff Pass-Through to US Consumers

The pass-through of tariffs to US consumer prices is a complex and lengthy process. Firm margins will first absorb costs before prices rise at the retail level. GM and Ford alone absorbed USD 1.9 billion in tariff-related costs last quarter. But this cushioning has limits. Firms are now flagging weaker earnings as profitability deteriorates, and with threatened tariffs now crystallising into deals, the pressure to raise prices is mounting.

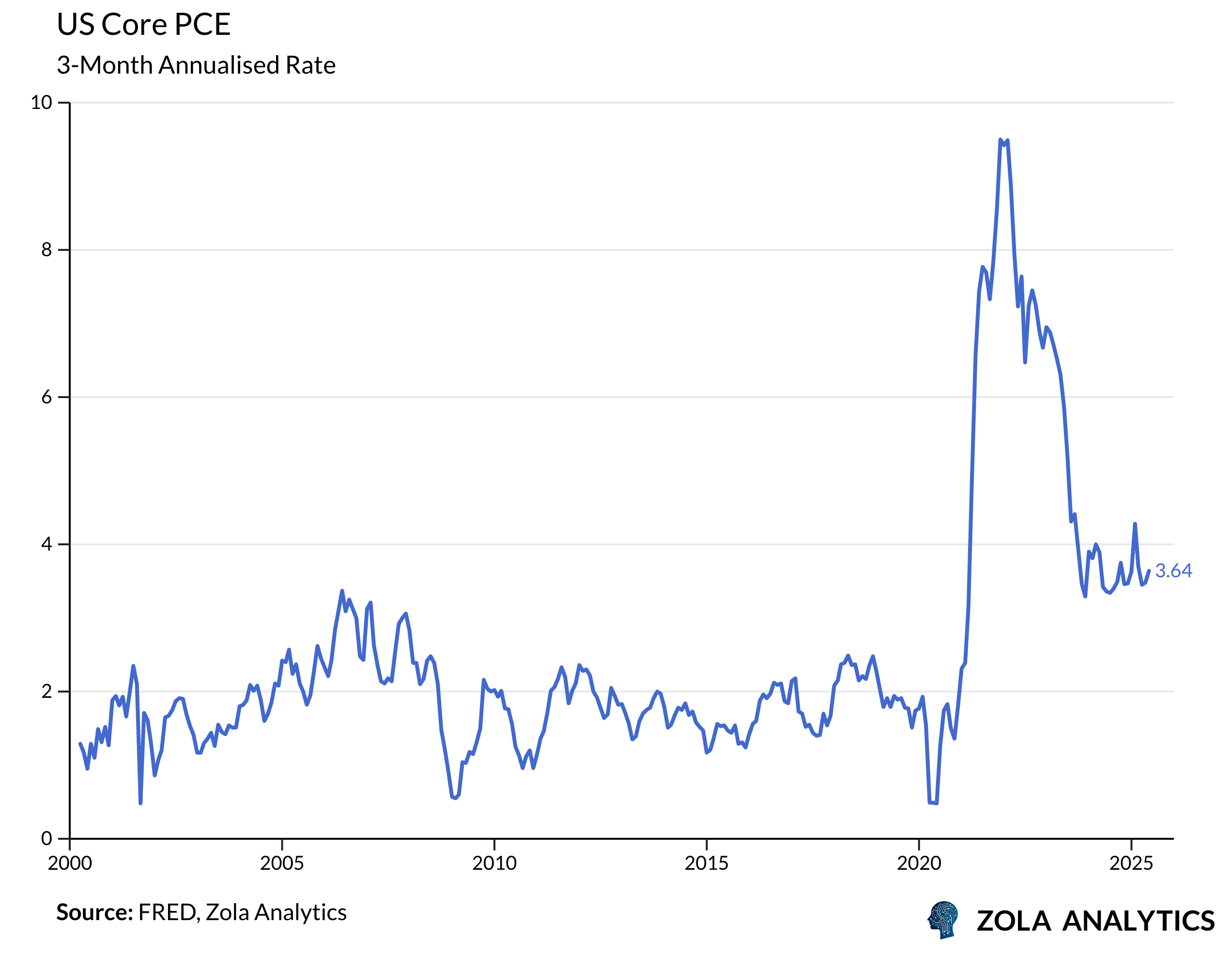

Fed Chair Powell has already cited tariffs as a contributing factor behind the recent uptick, while earlier inventory front-loading masked the full extent of pass-through. Last week’s PCE report showed three-month annualised core inflation rate has accelerated to 3.6%, suggesting the lagged effects of previously implemented tariffs are taking hold. With the Fed worried about the impact of headline inflation on consumer inflation expectations and the labour market suggesting weakness, the FOMC now faces a significant policy dilemma.

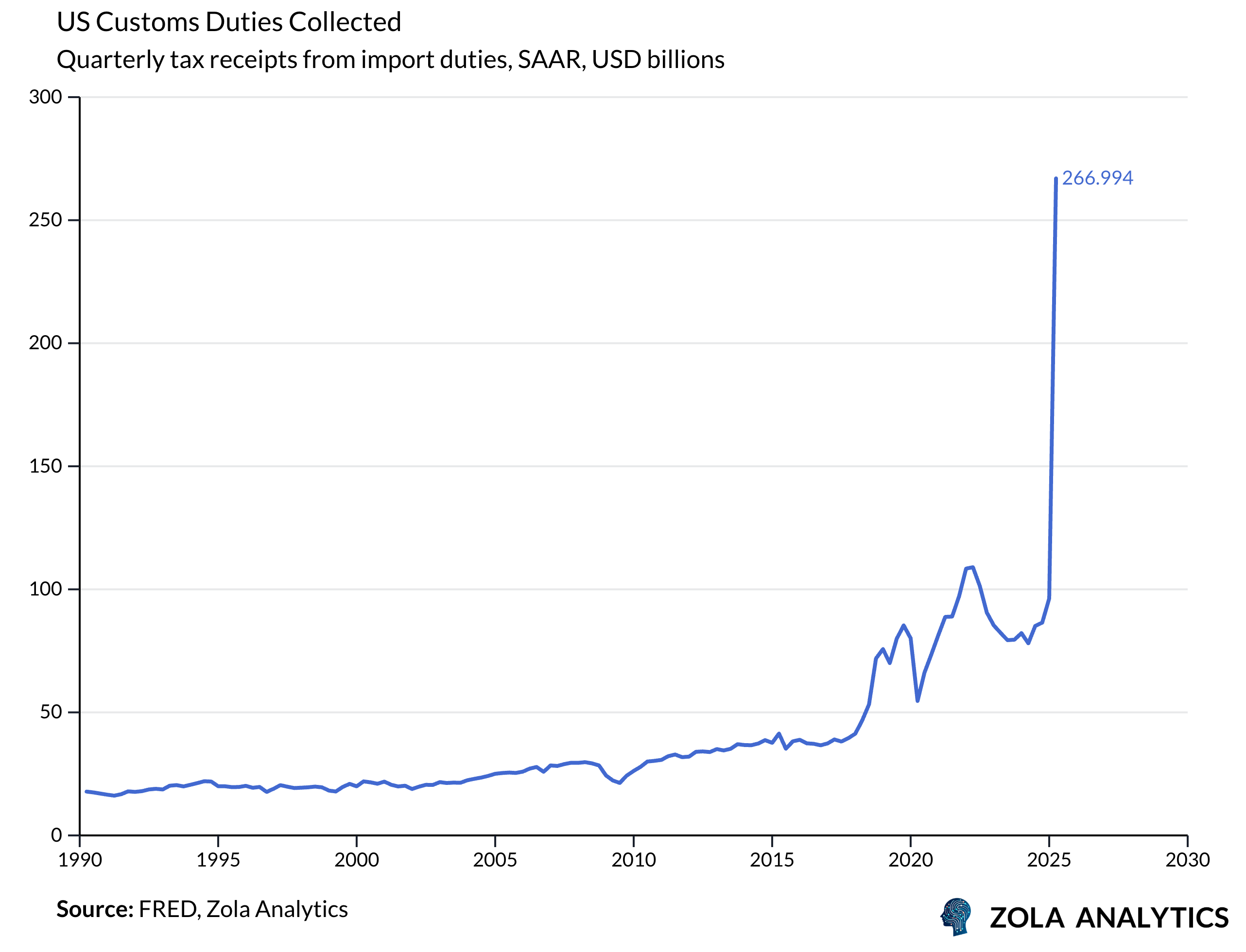

Moreover, policy uncertainty has begun to weigh on business investment and hiring, suggesting second-round effects are forming. Chart signals such as rising customs revenue collected, firming PCE inflation, and a temporary dip in consumer inflation expectations all suggest that while early signs are materialising, the full inflationary consequences of tariffs are still working their way through the system.

Market Fallout: What’s Priced, What’s Not

Equities: Momentum is holding for now. With 63% of S&P 500 companies reporting, 79% have beaten earnings expectations. Yet this strength is concentrated: the Magnificent 7 continue to dominate earnings growth, while the broader market lags. Despite upbeat beats, forward guidance is more cautious, with a pickup in margin compression talk and weaker sales breadth. The full-year EPS forecast for 2025 remains optimistic at +9.5%, and 2026 forecasts suggest 13.6% growth, ambitious given tightening financial conditions and late-cycle risks. Sentiment remains bullish and volatility is underpriced, but any earnings stumble or macro surprise could prompt a sharp repricing.

Bonds: Market rate cut expectations clash with persistent inflation realities. Tariff impacts are feeding through to goods prices, with supercore CPI elevated and Fed policy constrained. The labour puzzle deepens - payrolls averaging just 35k versus 60-80k breakeven needs, suggesting growth has halved, yet wage pressures persist amid tighter labour supply from immigration limits. Treasury supply surges through 2026 as QT unwinds, pressuring intermediate maturities and term premia. Long-end supply pressures persist, with Jackson Hole (Aug. 21-23) potentially providing the true rate signal, until then, expect curve whipsaws and fragile term premium anchoring. European markets face similar constraints: ECB holds at 2% with minimal easing priced, while UK gilts struggle under fiscal pressures despite rate cut expectations.

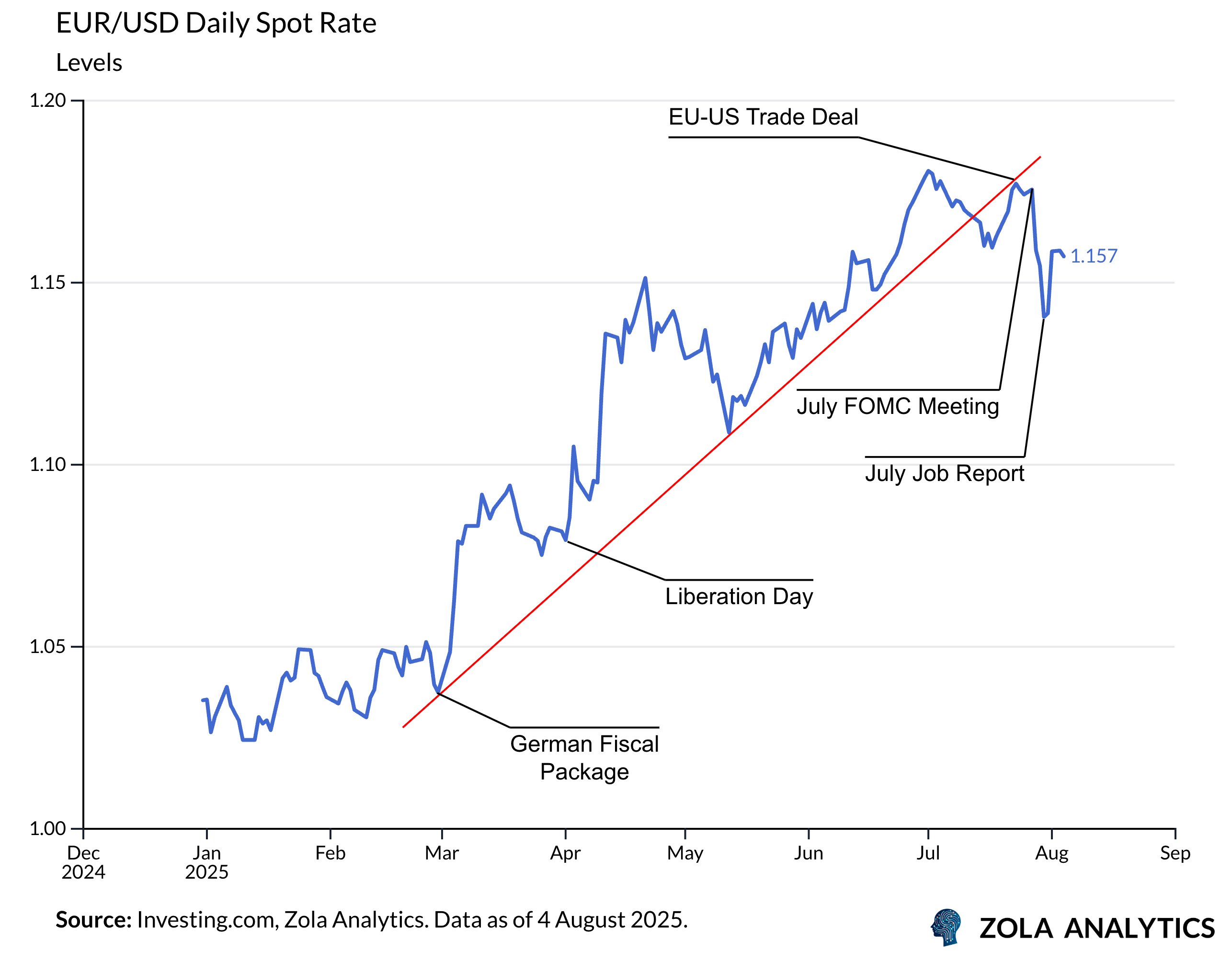

FX: The dollar bounce appears tactical rather than structural, driven by positioning and Fed repricing. Despite near-term DXY resilience from delayed cuts and haven flows, a softening bias is emerging. Real rate differentials should compress as inflation rises and growth slows, favouring selective dollar shorts, such as USD/JPY and USD/CHF.

Commodities & Crypto: A surprise 50% copper tariff triggered a 19% crash in futures, underlining how vulnerable markets remain to political noise. Gold remains supported as a hedge against monetary drift and geopolitical friction. Bitcoin echoed equities, selling off post-FOMC before rebounding, thriving on dysfunction narratives and dollar weakness expectations.

Bank of England meeting

The BoE meets Thursday, with a 25bp cut fully priced. After last month’s pause, this would continue the hold–cut–hold rhythm.

Policy remains restrictive at 4.25%, but mixed signals persist: inflation is sticky, yet growth has stalled and payrolls are shrinking. The focus will be on updated forecasts and any hints of another cut this year.

Fed Succession Watch

With Governor Kugler’s surprise resignation, attention now turns to her replacement. Despite claims of a split with Powell, Kugler’s latest remarks echoed FOMC consensus. What matters more now is who fills the seat—and whether the nominee tilts dovish, hawkish, or political. The next Fed speaker to watch is Bostic (Thursday), though the more pressing risk may come from the White House, not the Committee.

Tariff Deadline

The 7 August deadline looms for US trading partners to secure bilateral terms or face new “reciprocal” tariffs. While several countries have already struck deals, including Japan, the UK, and the EU, others remain exposed.

Russian Roulette

Friday marks the deadline set by President Trump for Russia and Ukraine to strike a ceasefire. While framed as a push for peace, the threat of new sanctions underscores the leverage-based strategy. Moscow shows little sign of relenting, with recent battlefield gains reinforcing its position. US envoy Steve Witkoff is expected in Moscow midweek in a last-minute diplomatic push.

Sign up to receive the Zola Global Macro Chartbook every week: https://www.zolaanalytics.com/insights?signUp