Published 5th September

8 minute read

The Brittle Map of Globalisation

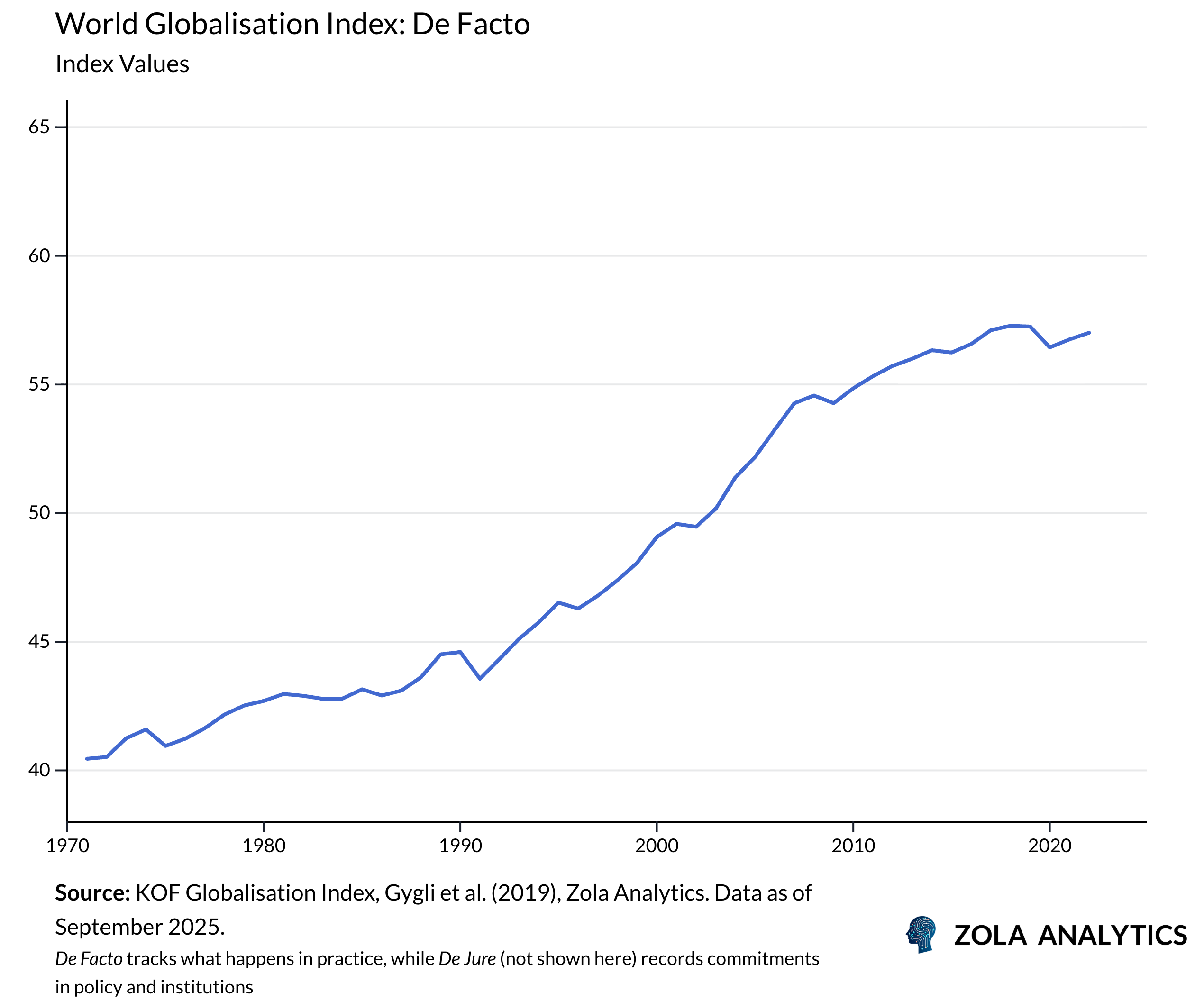

When the Doha Development Round opened in 2001, it seemed to confirm what many believed: that globalisation had entered an irreversible phase of expansion. The Cold War had ended, democracy was spreading, and market liberalisation promised to extend prosperity more widely than ever. Barriers were falling, capital was moving freely, and trade volumes swelled. Globalisation was destiny. Two decades later, the world looks very different. What seemed like solid foundations have proved brittle: hairline fractures have deepened into structural fissures, revealing the global system as more fragile than it first appeared.

The Inevitable Peak

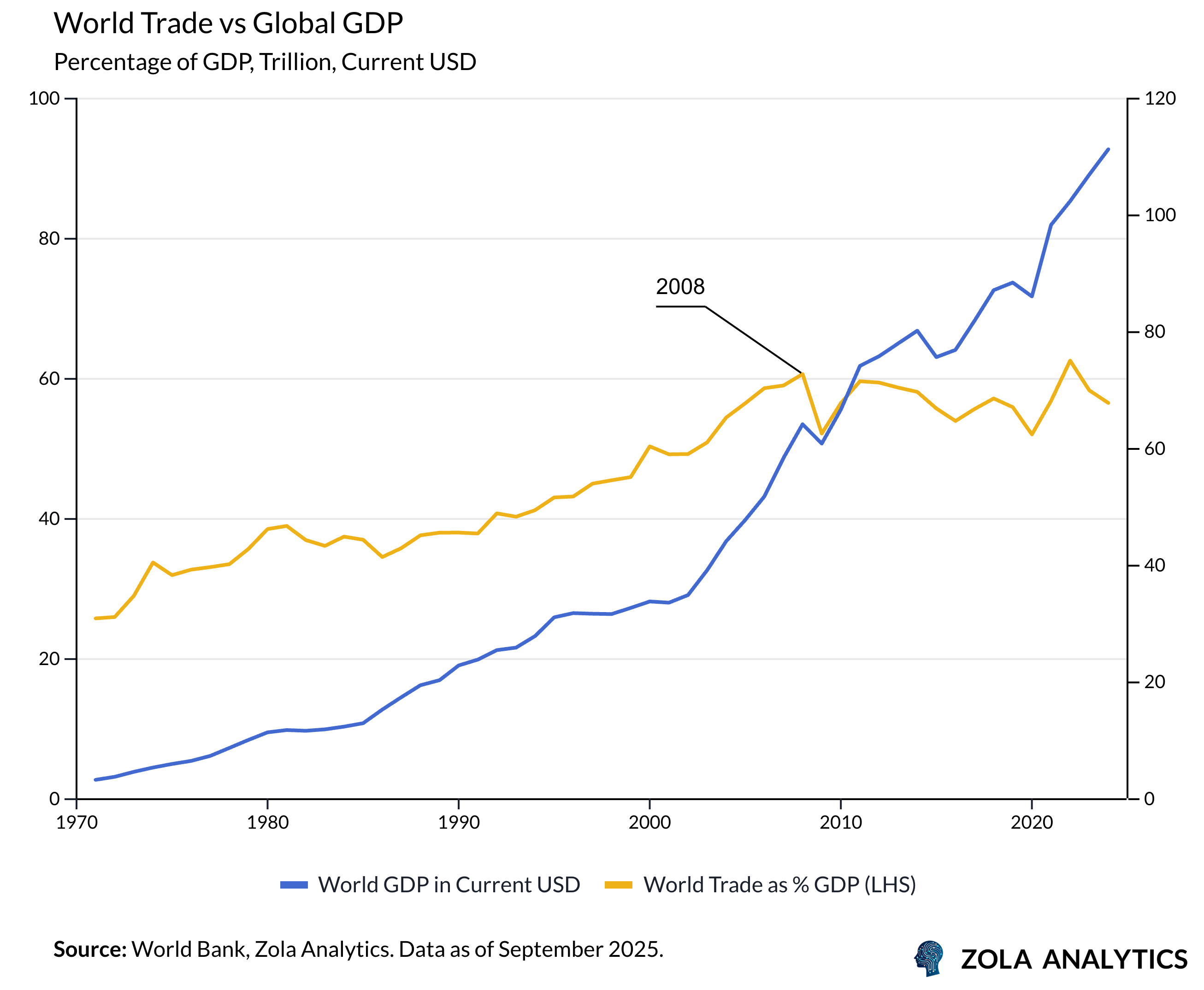

The high-water mark of global trade came just before the global financial crisis. By 2008, world trade had nearly doubled as a share of global GDP compared with the mid-1980s. This surge was fueled by one-off forces: the ICT revolution lowered coordination costs; liberalisation removed barriers; faster transport compressed distance; and the entry of vast new labour pools held down prices.

Such momentum could not last. Digital networks can only spread once. Tariff cuts reach their floor. Labour costs rise as economies develop. Investment faltered after 2008, and politics piled on new barriers. Ratios such as trade to GDP cannot rise without limit. The golden age of 1986–2008 carried within it the seeds of its slowdown. What looked like an endless climb proved to be a summit.

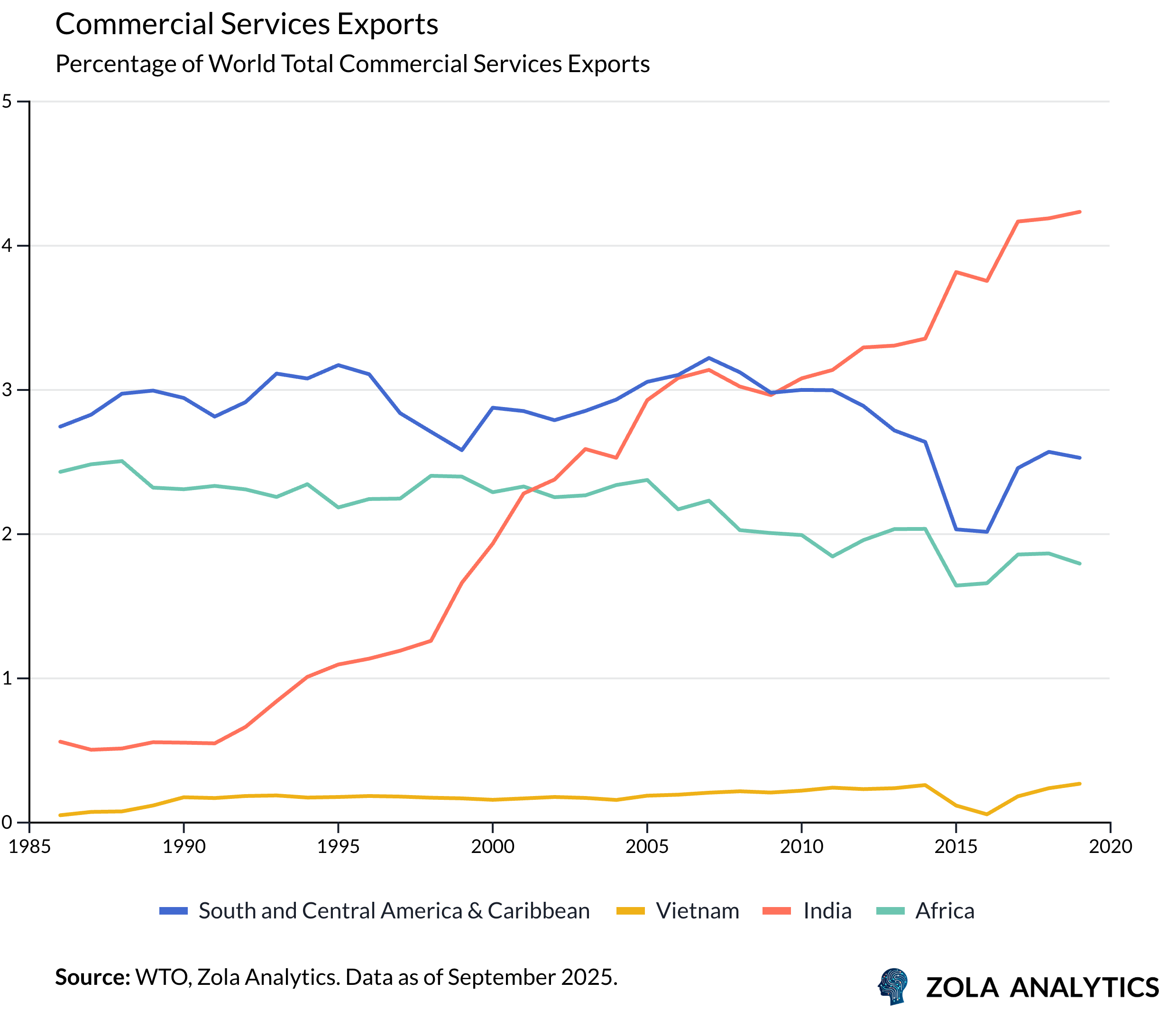

Bridges and Blocs

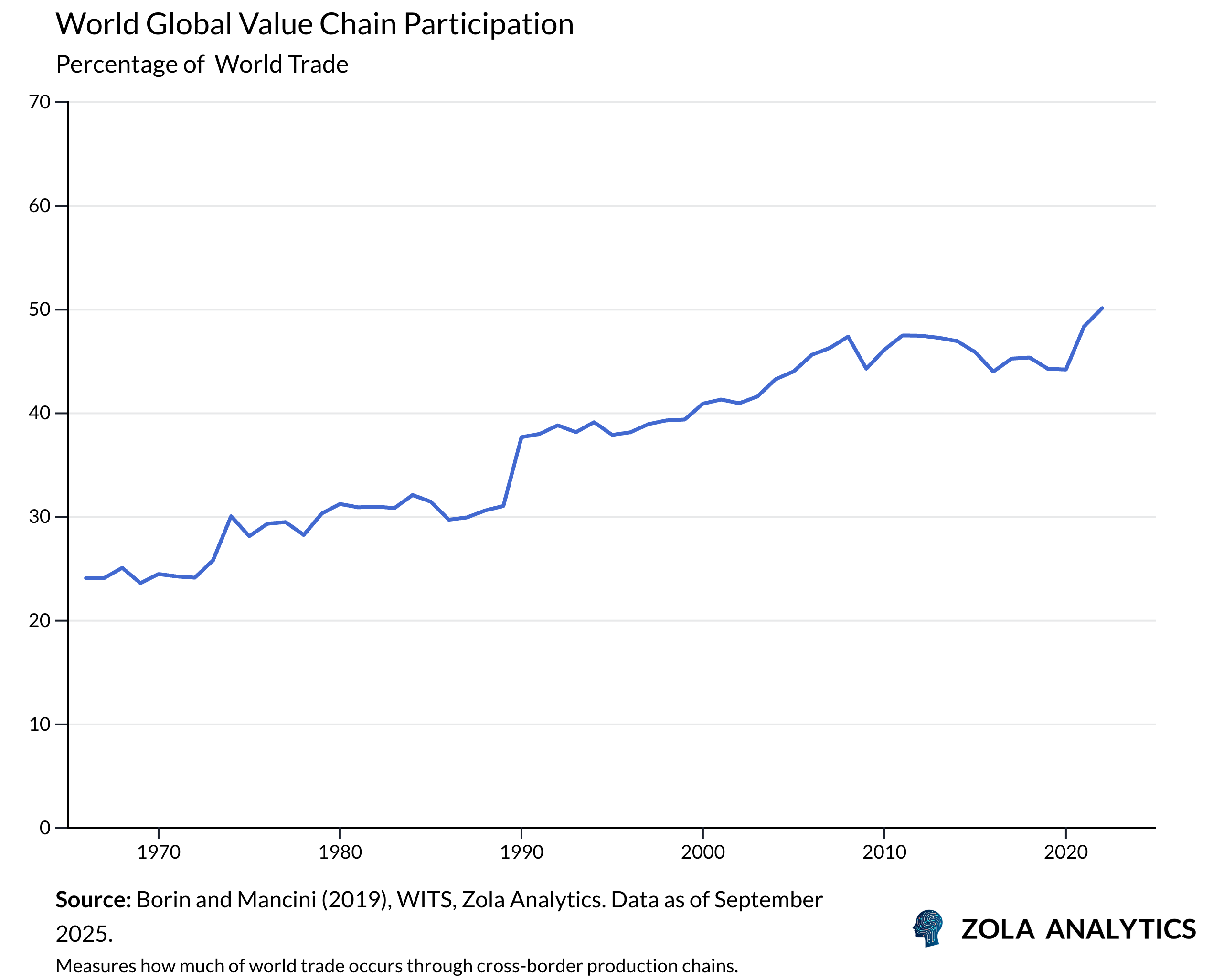

On this plateau, the structure of globalisation has changed. Goods trade has slowed, but services such as finance, digital platforms, and professional work continue to expand across borders. Services are less exposed to tariffs, travel through digital networks rather than ports, and often operate on multinational platforms. This shift has helped cushion the overall slowdown.

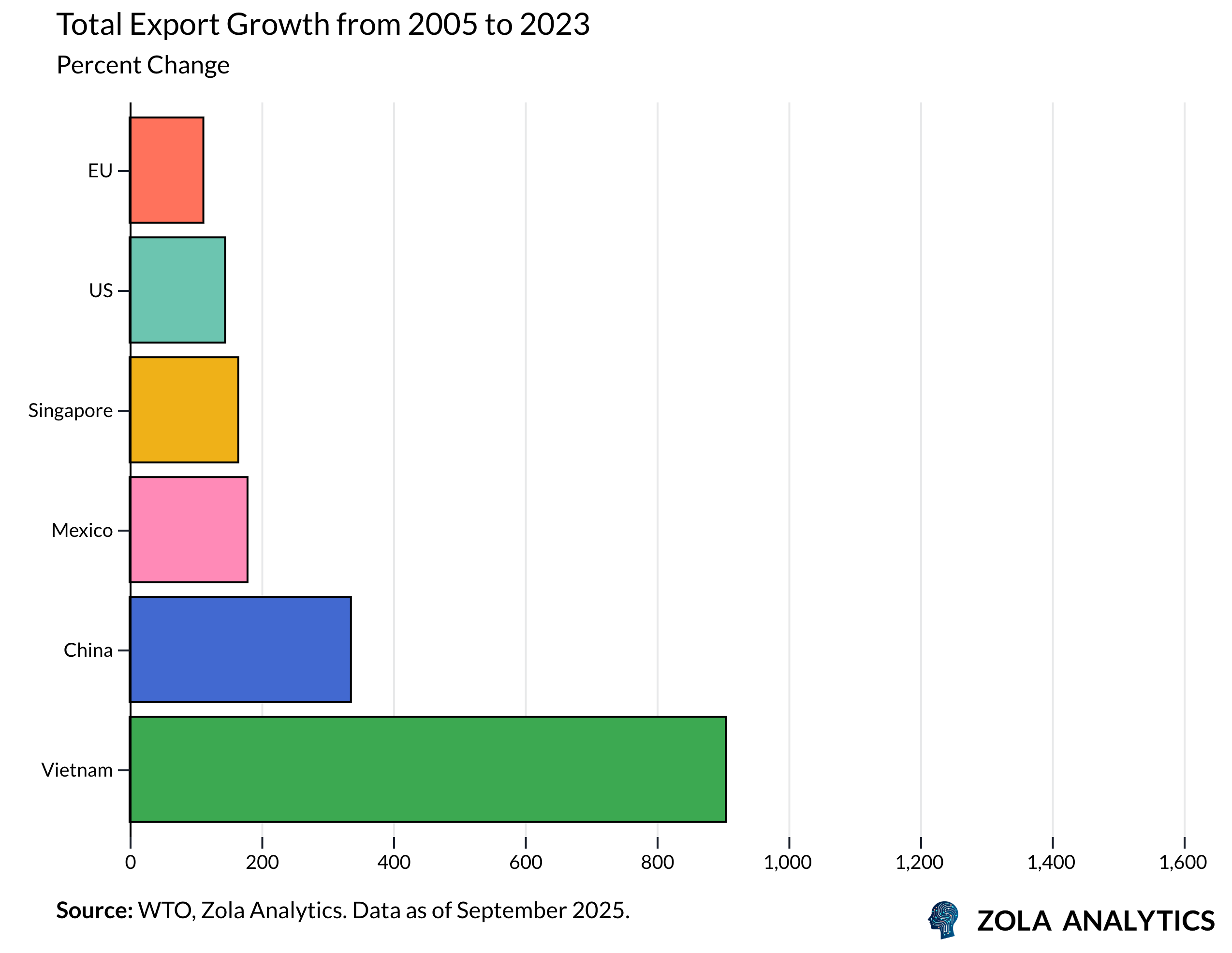

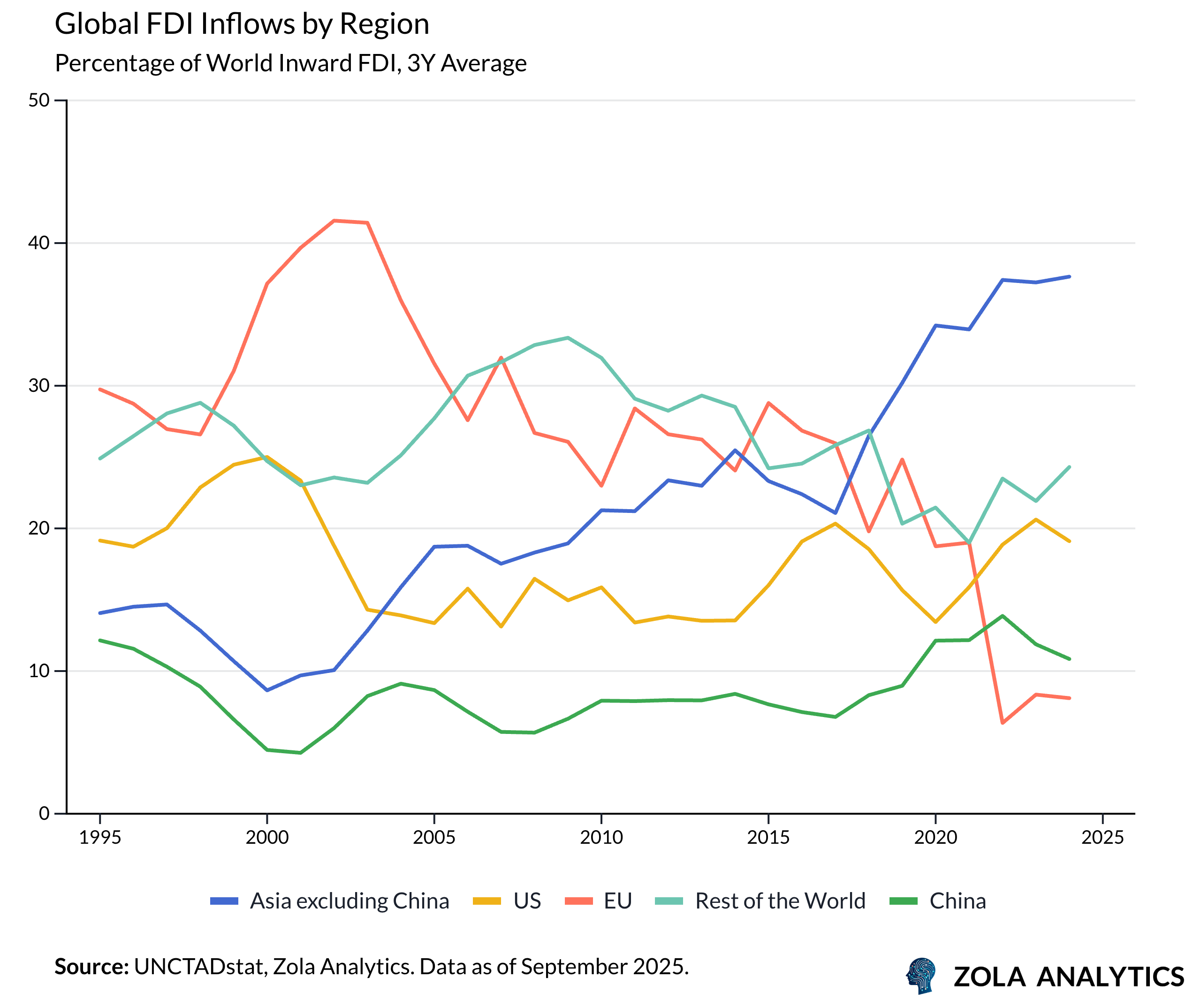

At the same time, supply chains have been redirected through intermediary economies such as Vietnam, Mexico, and Singapore. These economies have become critical connectors, keeping commerce flowing between rival blocs, but often at higher cost and with lower capacity. Asia remains the core of the global economy, though with mixed outcomes: China has advanced technologically and become a capital exporter; Taiwan and Korea remain central to semiconductors but face greater geopolitical exposure; Southeast Asia has gained importance as a hub. Europe has lost ground due to energy shocks and policy hesitation. The US has held position, but largely by absorbing China’s trade surplus. Integration persists but unevenly, with weaker regions bearing the greatest strain.

Directed Capital

Capital flows have changed as much in kind as in scale. The wave of greenfield projects that once expanded productive capacity has ebbed since 2008, replaced by mergers and portfolio flows. Liquidity is abundant, but productive investment is thin. Global greenfield inflows remain less than half their pre-2008 levels, underlining the structural break.

Policy now plays as large a role as markets. Subsidies, tariffs, and security rules increasingly determine where capital goes. Southeast Asia has gained, Europe has lost ground outside finance, and the US depends on foreign savings even as it pursues self-sufficiency. This reconfiguration leaves the system more volatile and less growth-oriented. Capital is abundant, but its foundations are weak.

Resilience Over Efficiency

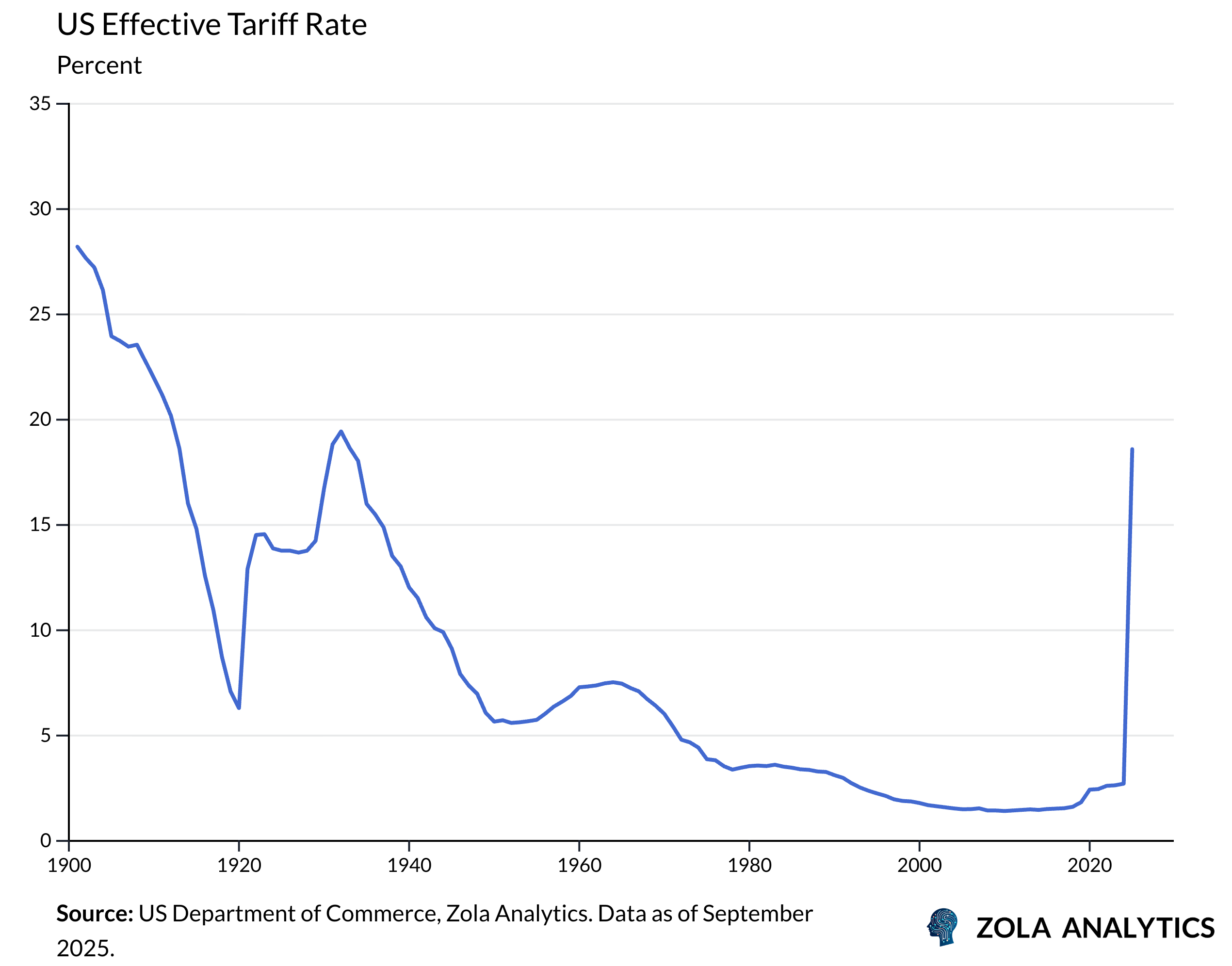

The pandemic revealed how fragile long supply chains could be. What looked efficient in normal times proved brittle under stress, as shortages of masks, medicines, and semiconductors cascaded through the system. For many governments, the COVID experience turned resilience from a slogan into a priority, and prompted a retreat from the liberal principles that had underpinned decades of open trade.

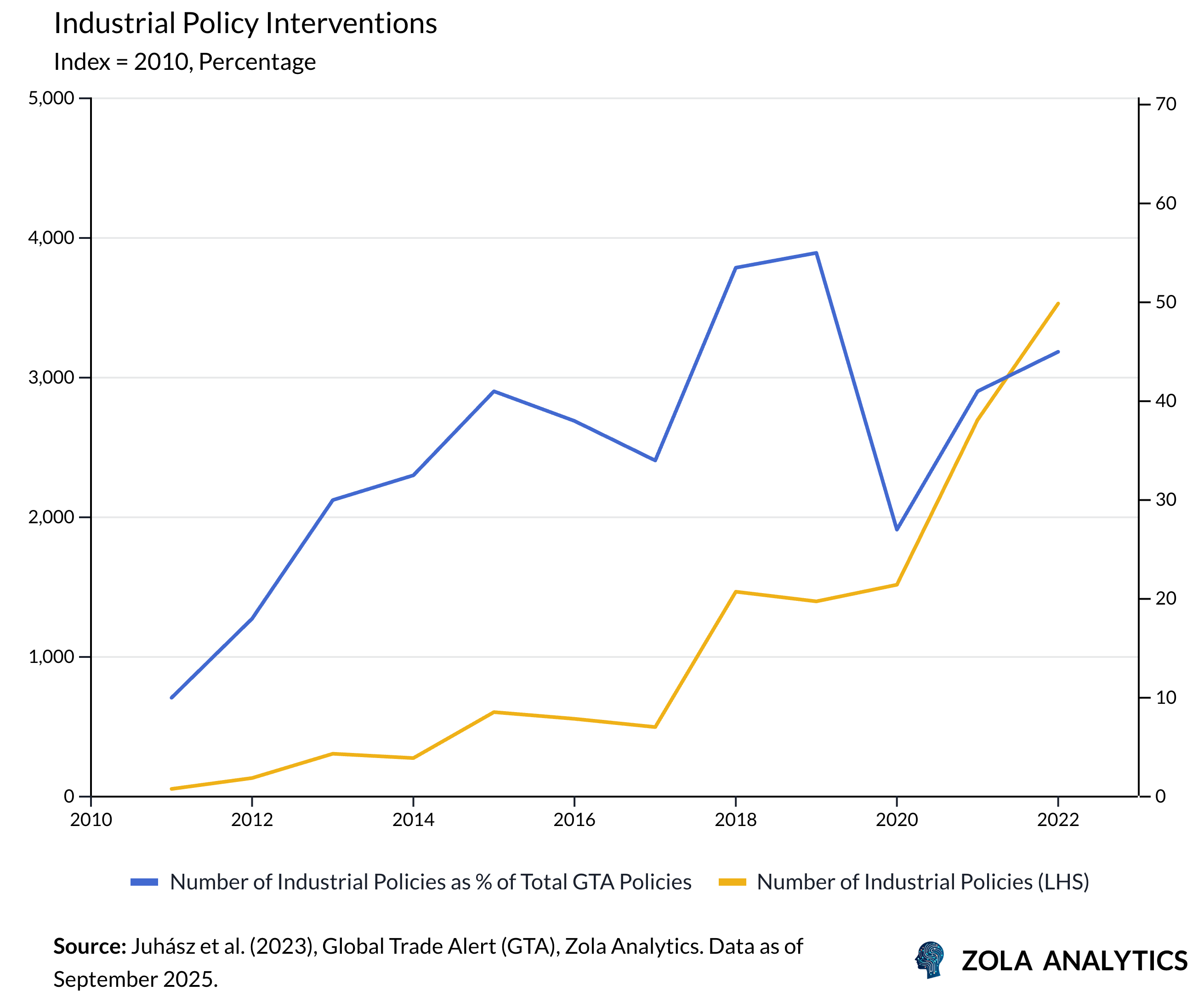

Policy has since adjusted to this new reality. The dominant language is resilience, security, and industrial strategy. Tariffs remain in place, subsidies have multiplied, and coordination even among allies has weakened.

The shift is visible across major economies. The US Inflation Reduction Act ties subsidies to domestic content, creating friction with partners. Europe’s Carbon Border Adjustment Mechanism adds climate-linked costs to imports. Japan’s reshoring incentives reduce dependence on China but raise costs for domestic firms. Disputes within blocs, from clean-energy credits to steel mergers, show how quickly common agendas fragment under pressure. At the frontier of geoeconomics, control over strategic sectors such as semiconductors, batteries, and critical minerals has become as important as tariffs or quotas. Chips are treated not as commodities but as levers of security and influence.

The macroeconomic cost is clear. Efficiency has been traded for resilience. Supply chains are more secure but also more expensive, embedding structural inflation into the global system. Integration endures, but its dividends are weaker.

The Shorter Ladder

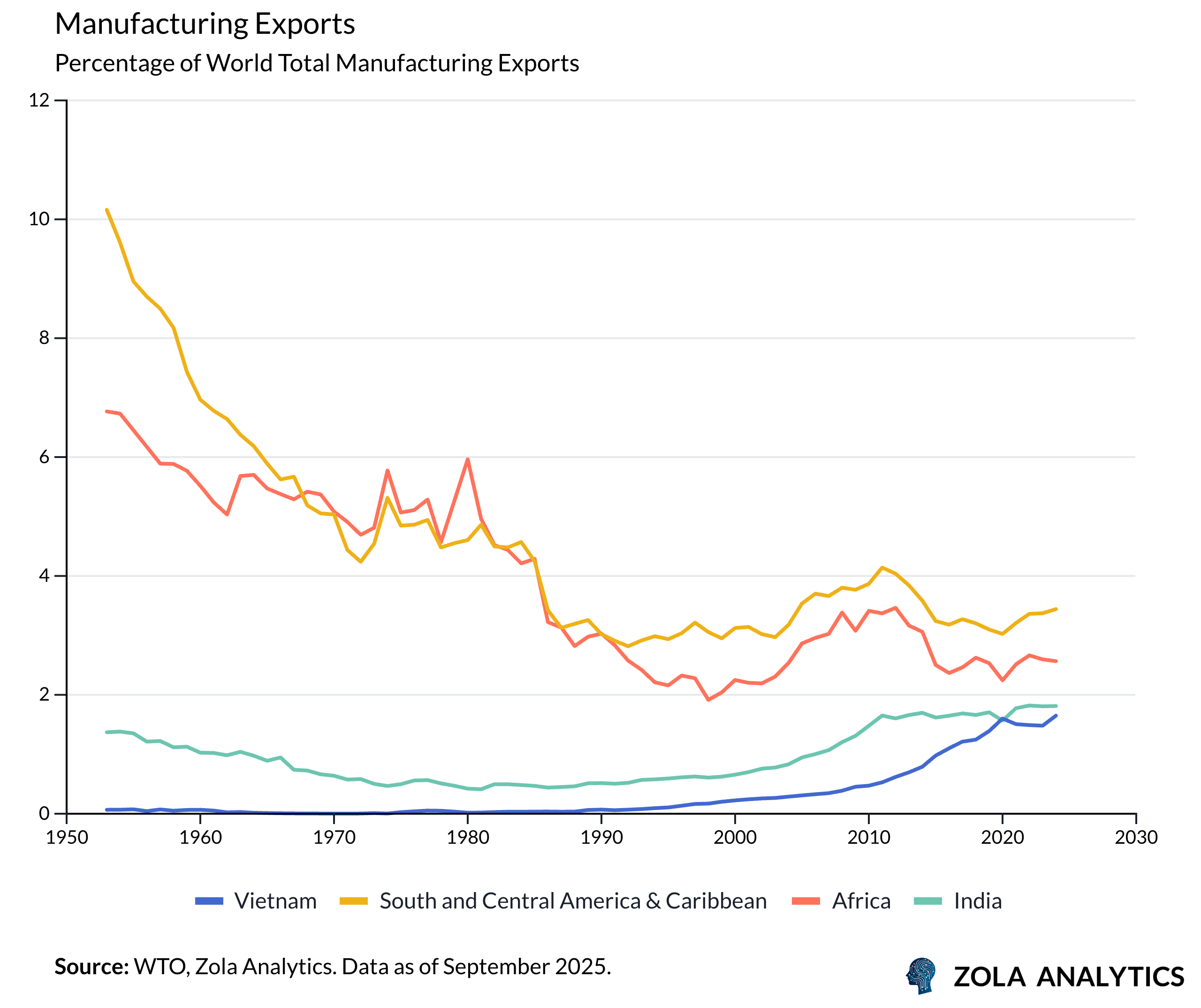

For emerging economies, this reconfiguration is a mixed blessing. Export-oriented manufacturing once provided a reliable ladder to growth. Today, that route is harder: rich markets are less open, supply chains are more regional, and automation has reduced the scope for labour-intensive industry.

India illustrates the challenge. Despite abundant labour, it has struggled to build the large-scale industrial base that once absorbed workers in East Asia. Diversification has begun, but without sustained manufacturing exports, the task of creating jobs at scale remains acute. Vietnam shows the other side: it has gained in electronics and textiles as firms divert supply chains away from China. Yet its success highlights limits as well as opportunities — it can only capture a fraction of the space once occupied by China’s vast export machine.

Beyond Asia, Africa and Latin America risk being bypassed altogether. Still reliant on commodities, they have captured little of the redirected investment. The convergence model that once drew countries upward is narrowing, and large parts of the global South face

Living with Fragility

Globalisation delivered a generation of cheap goods and rapid growth. Its slowing means higher costs, sharper rivalries, and fewer easy paths to prosperity. Yet it has not collapsed. Volumes remain high. Services are resilient. Connectors keep trade alive.

What remains is resilient in scale but brittle in form — enduring, yet reconfigured under political and security pressures. The global economy is no longer a clear pane reflecting a single order; it is a brittle map, its surface traced with fissures and resting on unstable foundations.

The next phase will test whether resilience can outweigh fragmentation. Services and connectors may provide enough joins to hold the system together. But if political stress deepens, today’s plateau could harden into tomorrow’s decline.

Sign up to receive the Zola Global Macro Chartbook every week: https://www.zolaanalytics.com/insights?signUp