Published June 16th 2026

10 minute read

Royal Rush

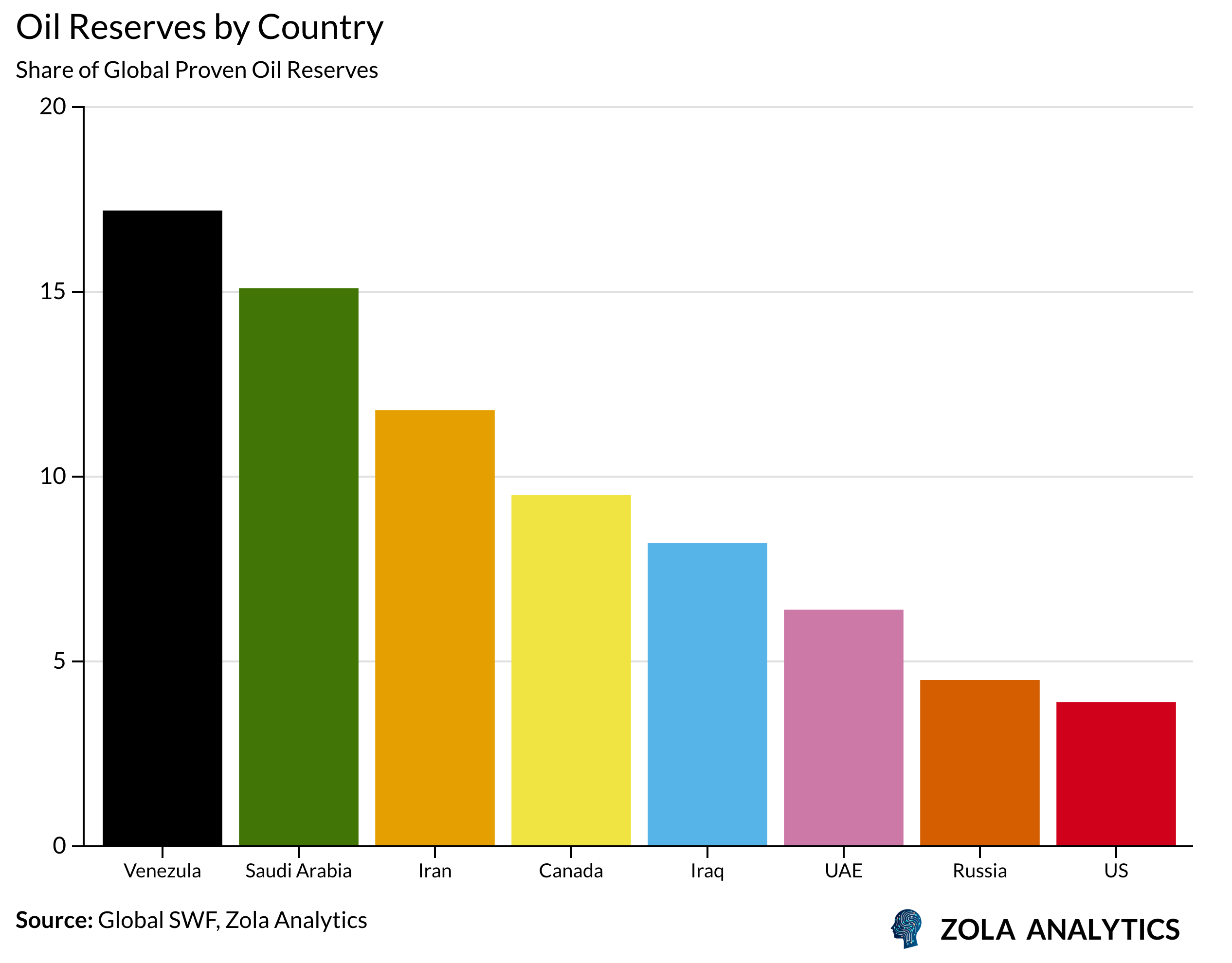

Saudi Arabia holds an enviable position in global energy markets: 300 billion barrels in proven reserves, the world’s lowest production costs, and sufficient spare capacity to move markets at a whim. Even aggressive energy transition scenarios project Saudi to be the last producer standing when global oil demand finally peaks. Yet the Kingdom is racing to restructure its entire economy away from oil dependence within fifteen years.

This is the core paradox of Vision 2030. While Saudi is a resource superpower, it has recognised that its greatest asset must be replaced before it is overwhelmed by structural pressures. This week’s Zola Chartbook aims at understanding this urgency, which requires looking past the narrative of energy transition to uncover the structural realities behind the insecurities of Saudi’s leaders.

New Prince, New Plan?

Despite holding substantial reserves, the Kingdom has long recognised that its oil is finite. Its first development plan in 1970, already identified diversification away from oil dependence as a core objective. Successive governments have pursued this agenda through multiple development plans, each promising to build alternative revenue streams and sources of private sector employment.

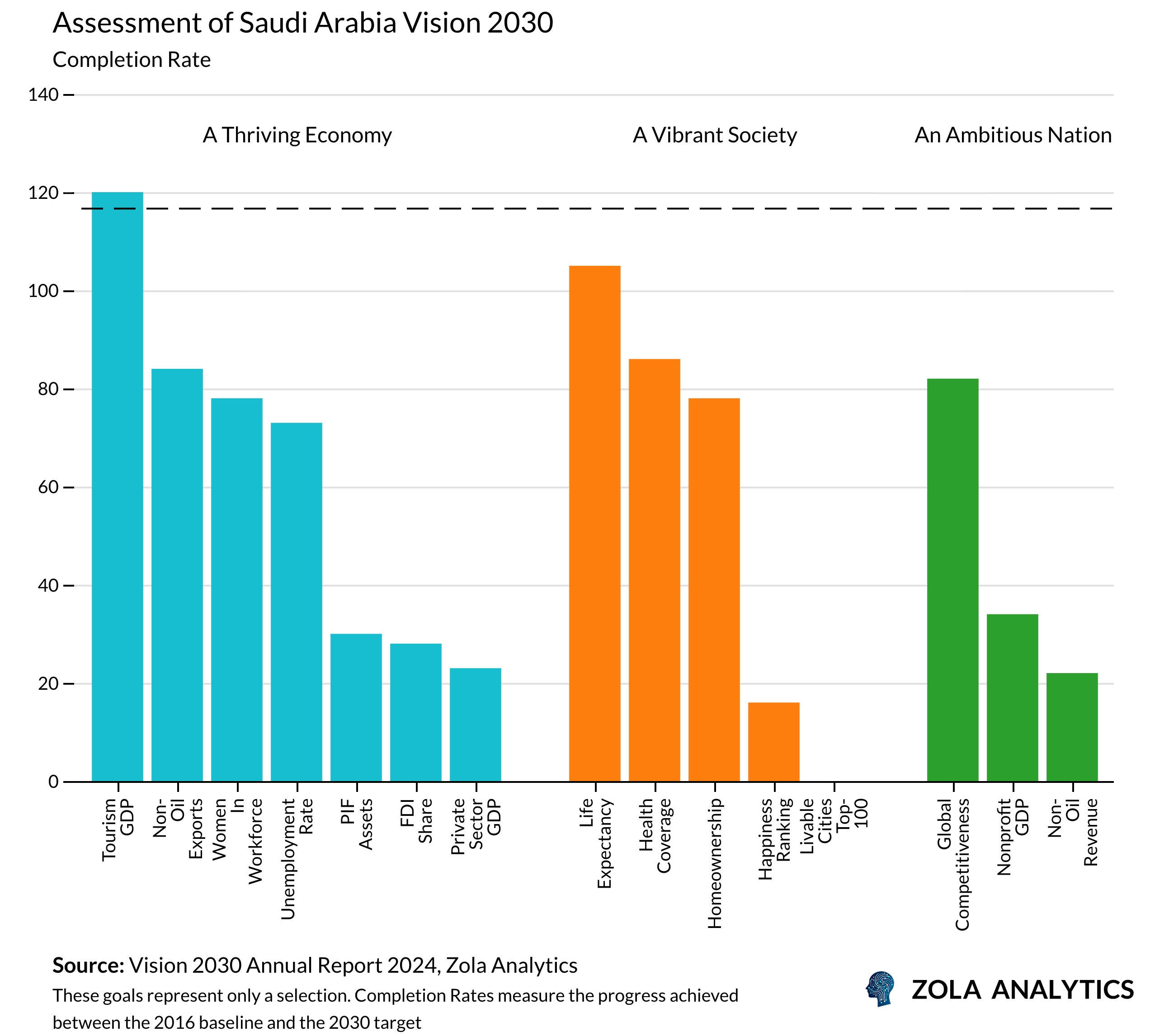

Vision 2030, launched in 2016 by Crown Prince Mohammed bin Salman, represents the latest and most ambitious attempt. What distinguishes it from previous plans is its ambition reflecting not only confidence, but also recognition of the depth of underlying structural weaknesses.

Yet nearly a decade in, the results are mixed. While some objectives, particularly in labour market reforms, have seen substantial progress, the most critical diversification targets remain far behind schedule. Private sector and SME contributions to GDP have barely moved, foreign direct investment flows are well below targets, and youth unemployment among Saudi nationals remains elevated.

The Kingdom’s Twin Distortions

Saudi’s diversification challenge reflects a pair of structural distortions that have resisted reform for half a century.

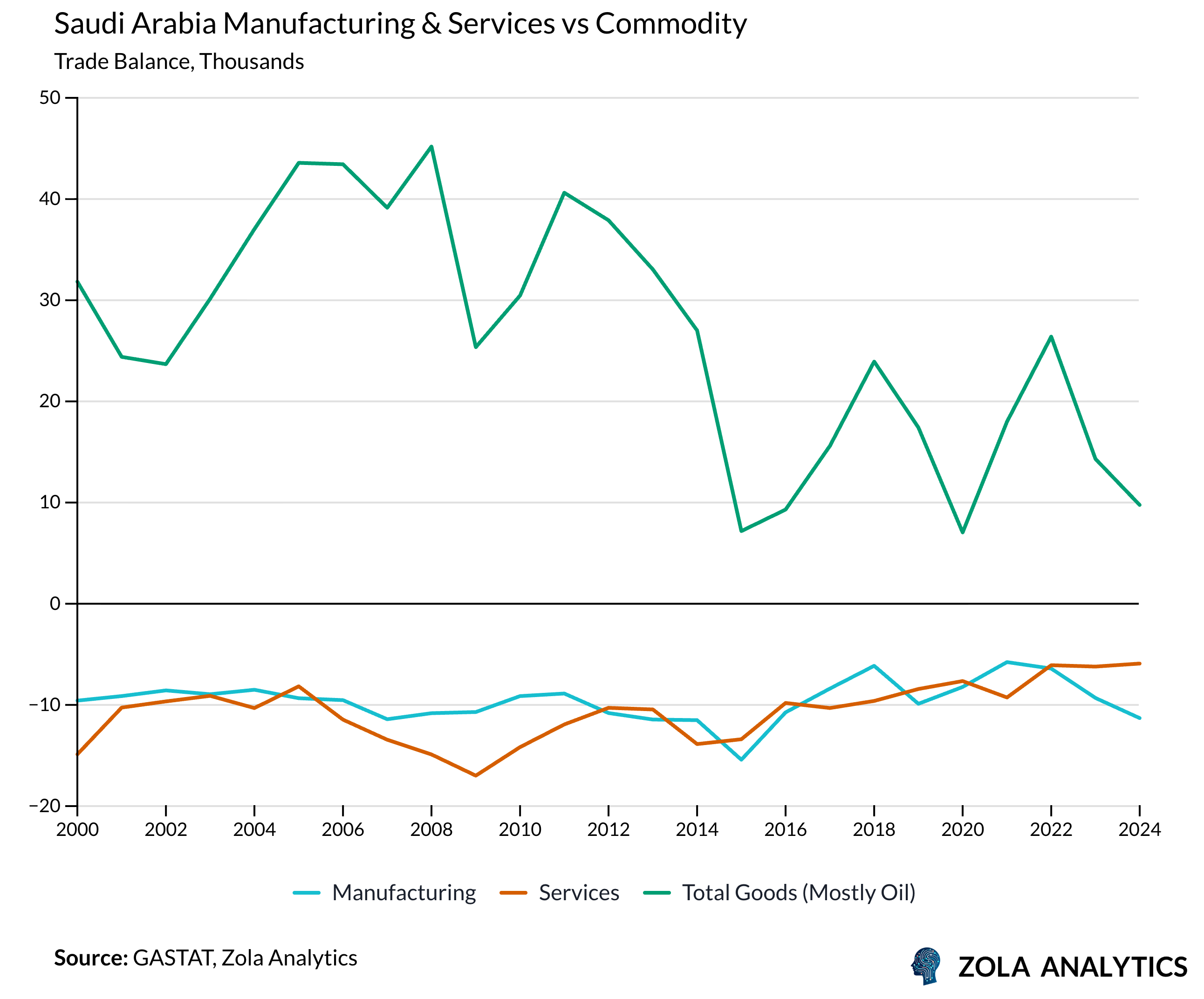

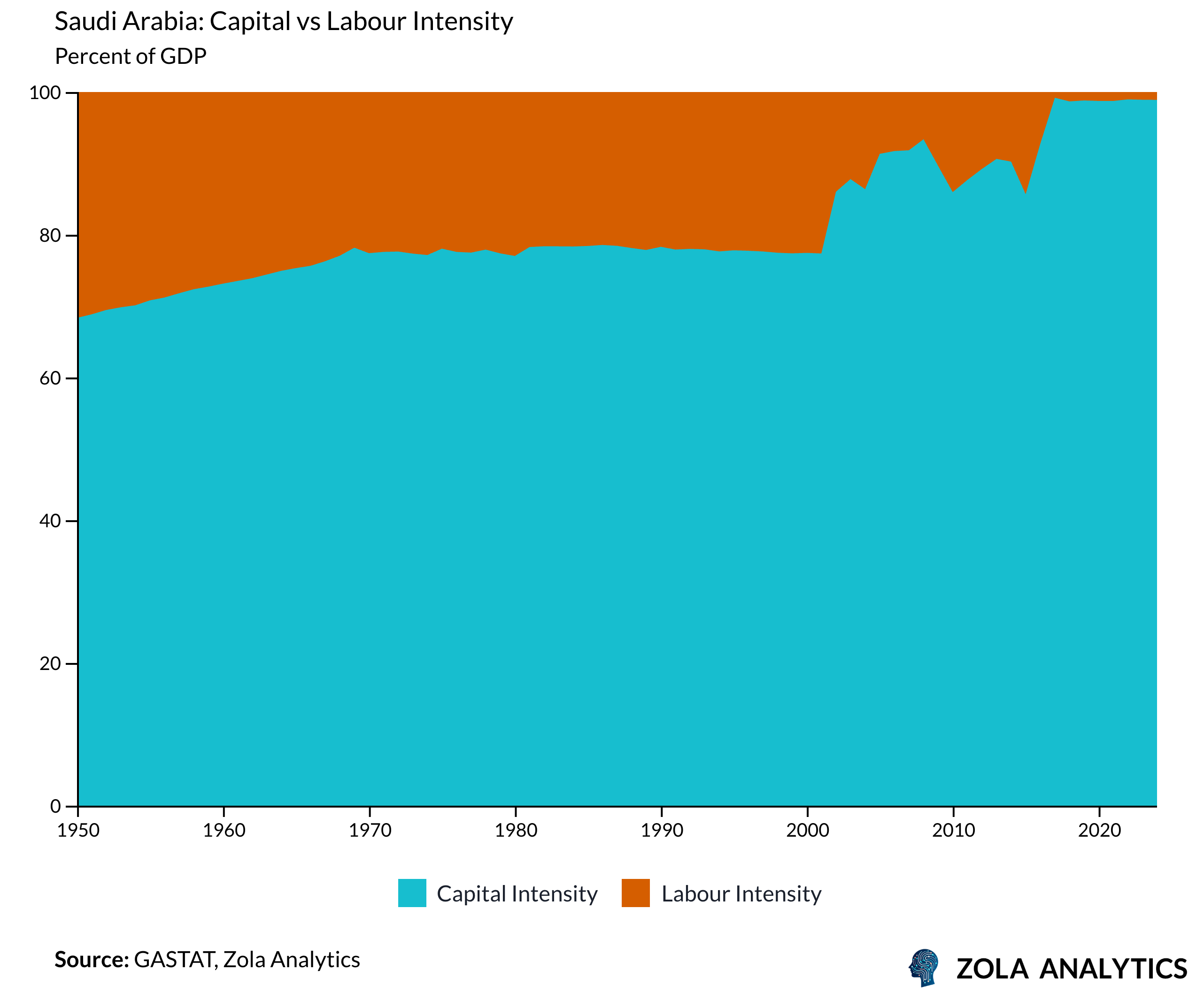

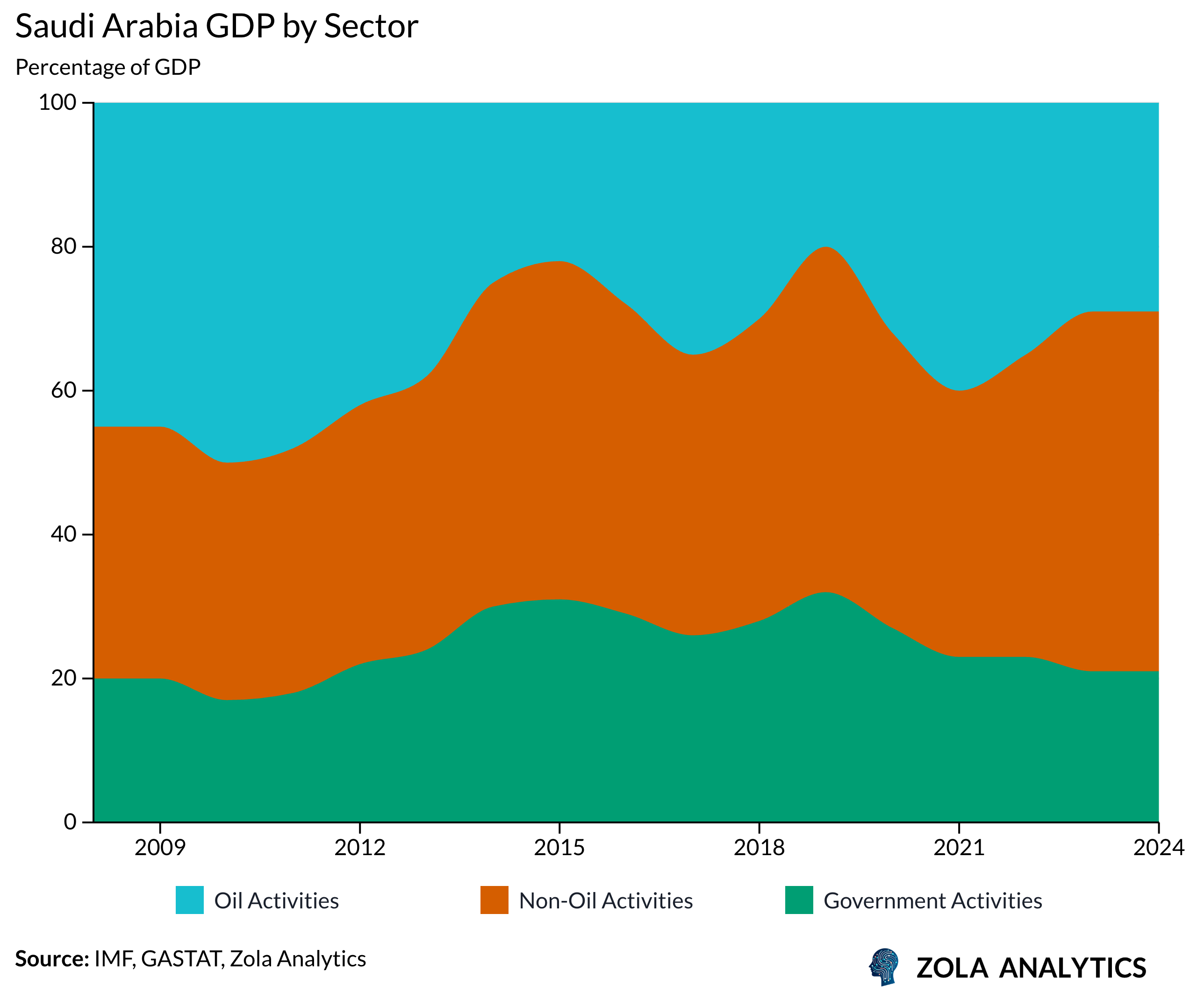

Saudi Arabia has long suffered from a severe form of Dutch Disease. Oil wealth inflates domestic costs, eroding price competitiveness in tradable sectors and entrenching an economy tilted toward non-tradables that rise and fall with government spending. These "spending effects" are visible throughout the economy in non-tradable sectors dependent on continued oil income. Construction, retail trade, and hospitality have thrived on distributed oil revenues.

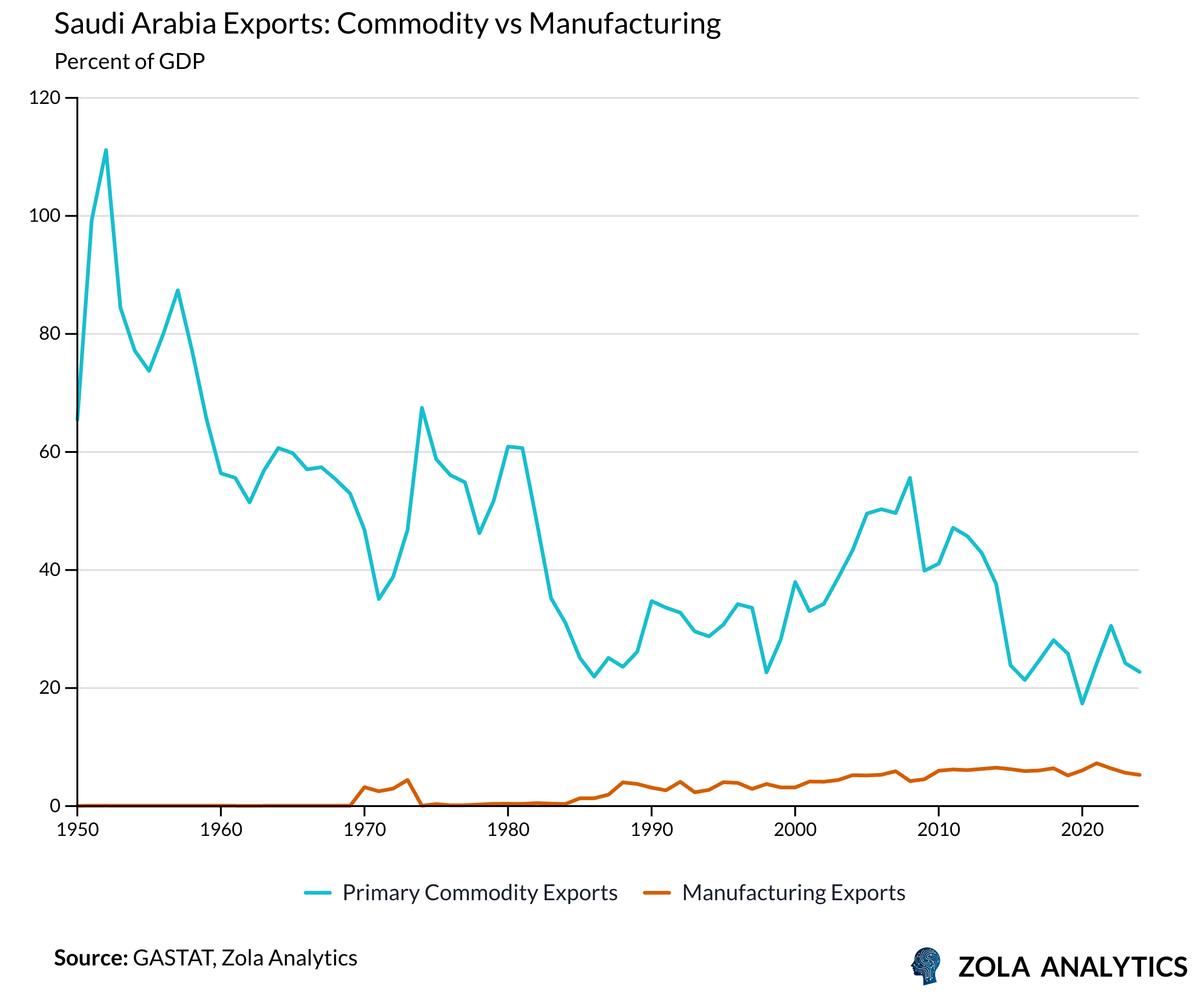

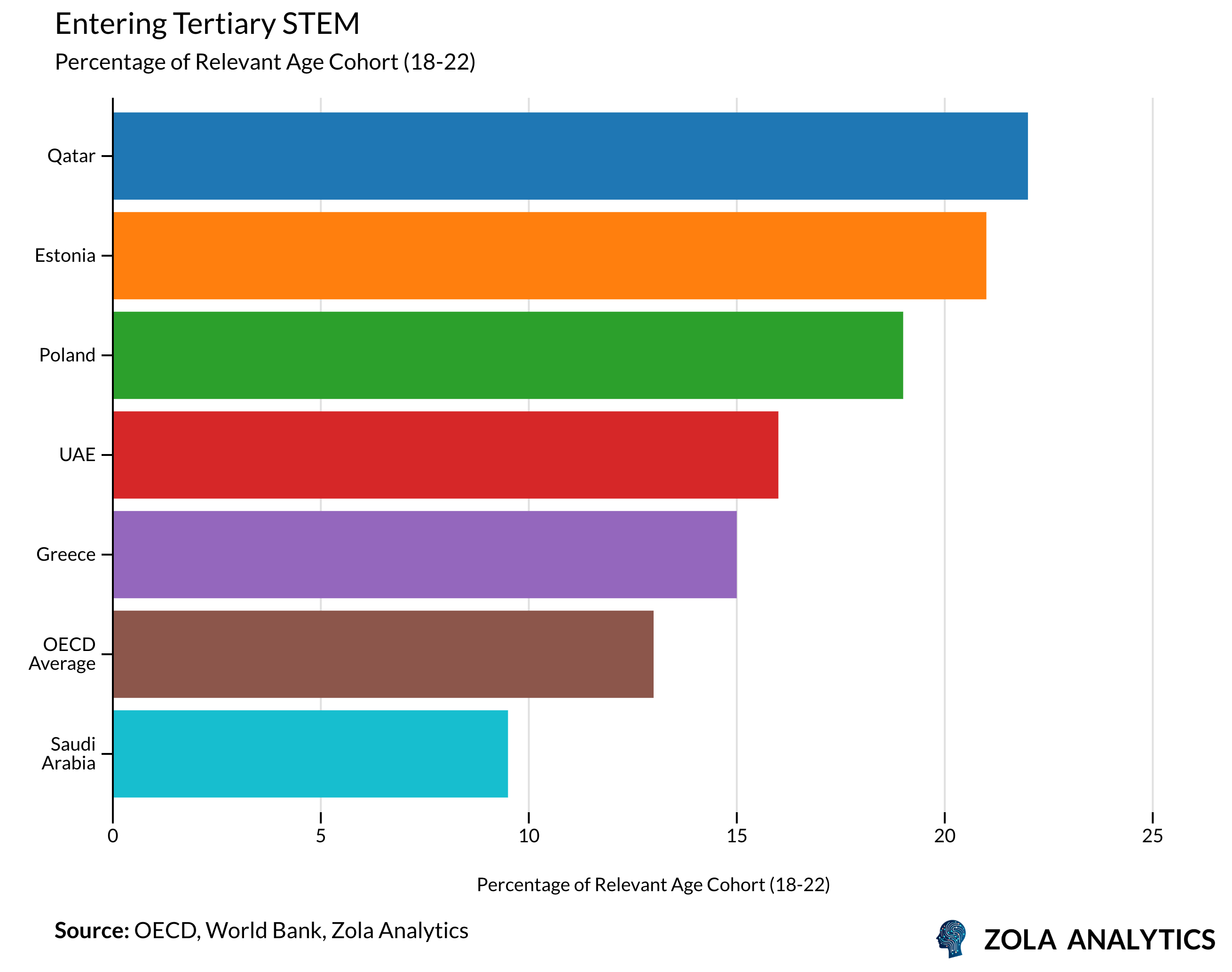

Meanwhile, manufacturing (excluding petroleum refining) represents just 9% of GDP. Whilst non-oil output now makes up half the economy, less than a quarter of this production is exported, far below the 2030 target of 50%. The sectors of the economy growing the fastest are not in diversifying sectors, suggesting little progress is being made to reduce dependence on the old economic model.

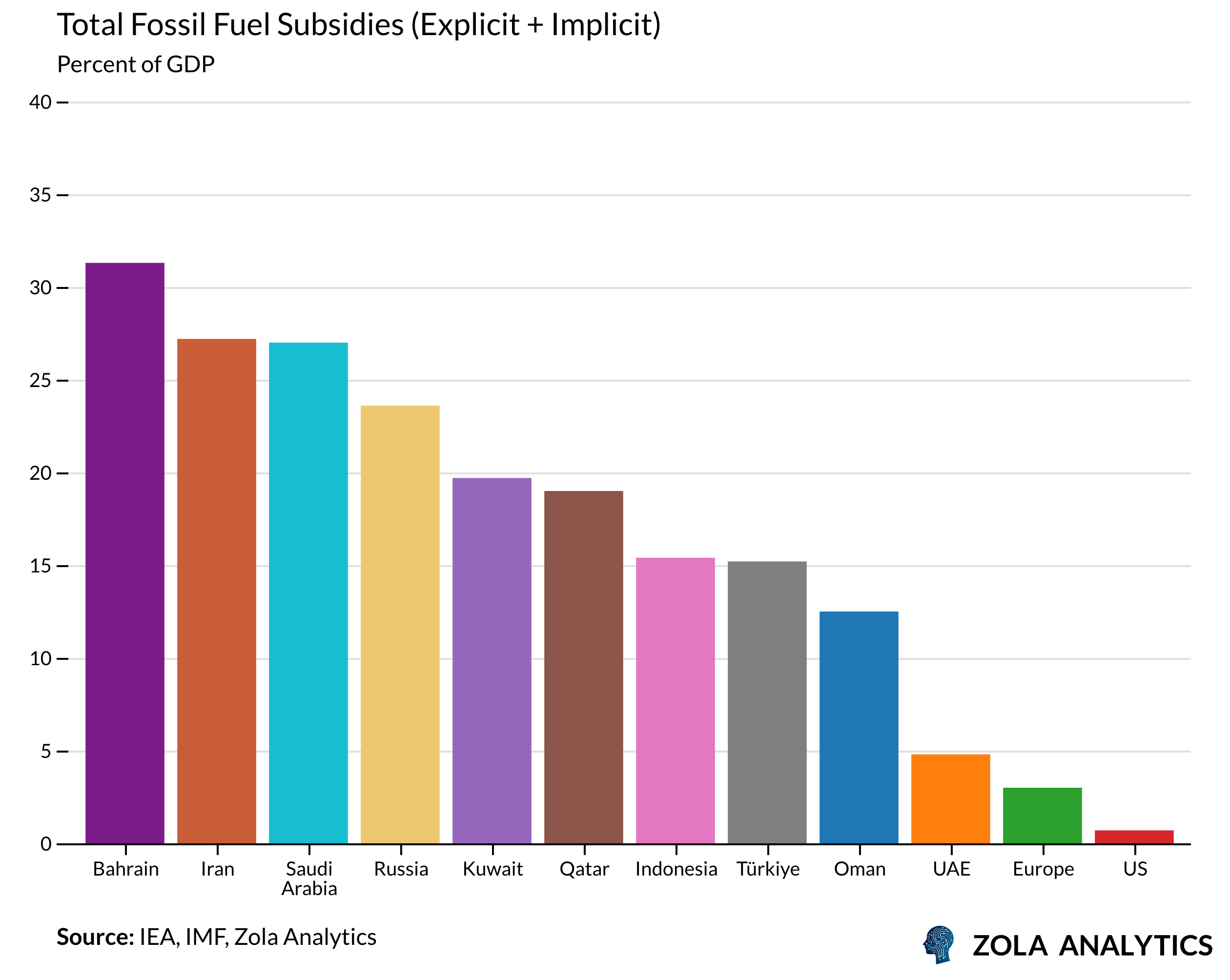

Energy subsidies compound the problem. Saudi Arabia remains the highest per capita spender on subsidies among G20 nations at USD 6,996 per person.

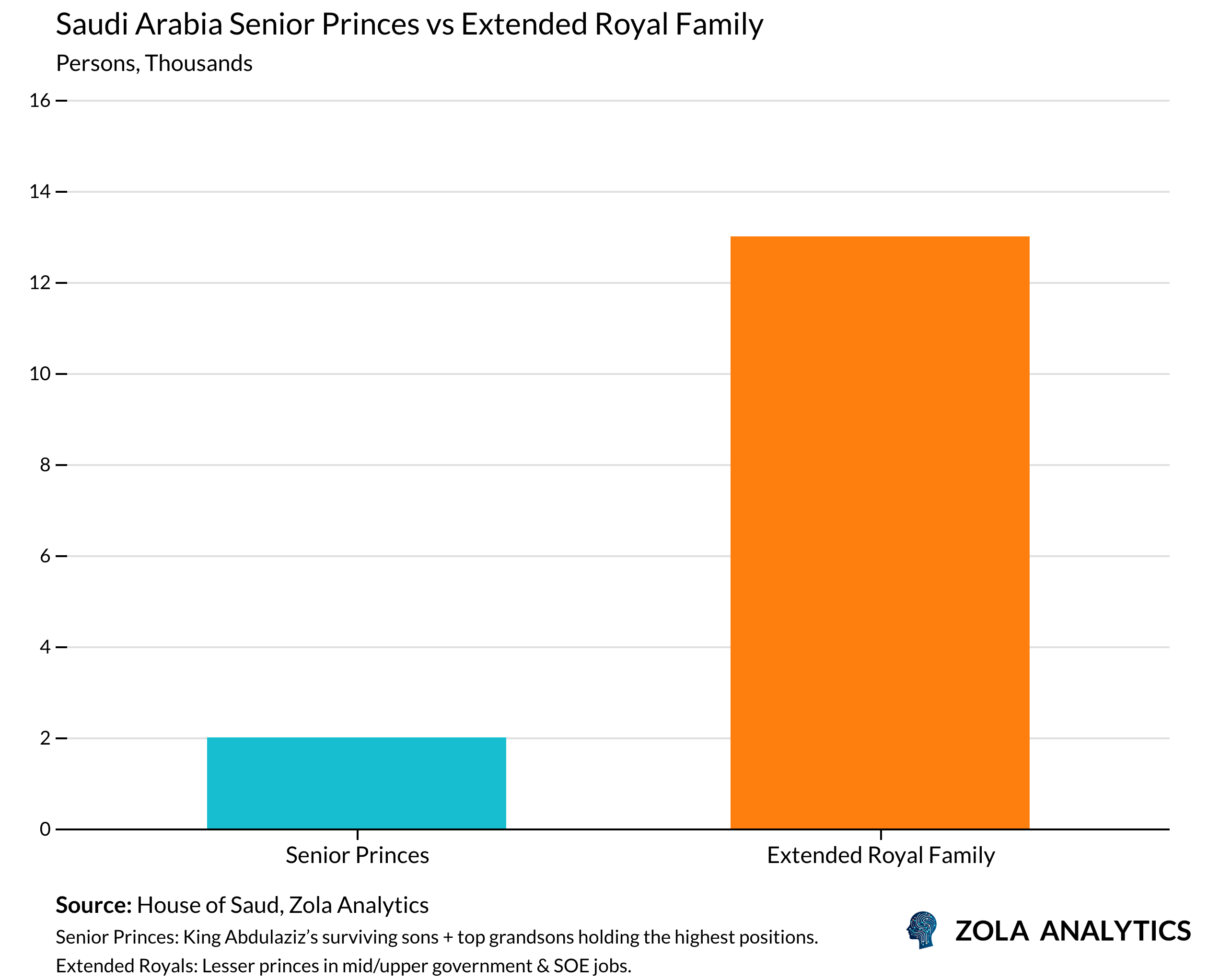

The structural constraints are not only economic, but also social. Approximately 15,000 members of the extended royal family hold positions throughout the Saudi government and state enterprises. Of these, roughly 13,000 are not independently wealthy but instead depend on these positions for income and status. Jobs are allocated through lineage networks, a pattern that destroys meritocratic incentives and degrades the quality of decision making.

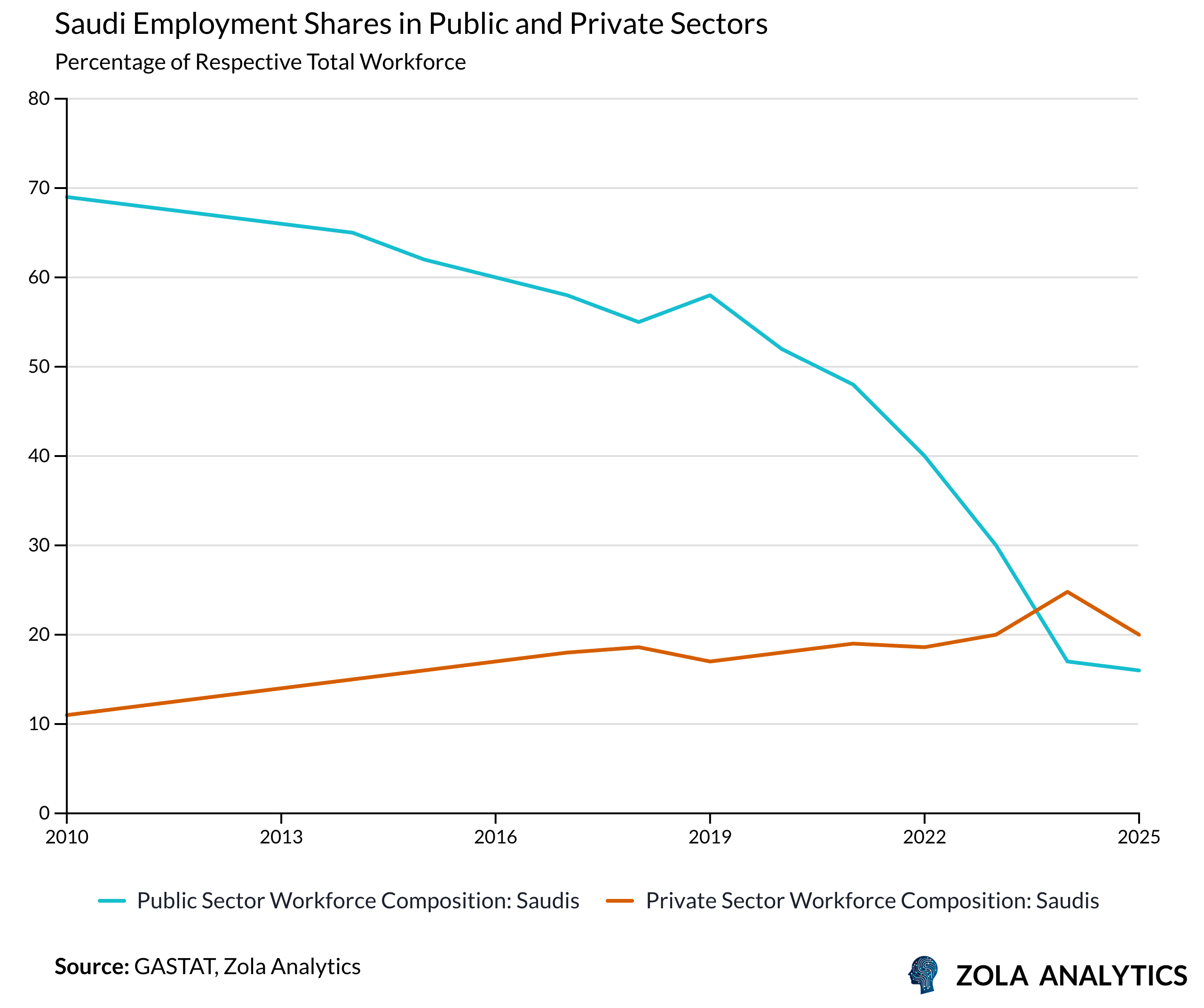

The labour market reflects these distortions. Saudis occupy comfortable public sector roles financed by oil revenues, while the majority of the private sector workforce is composed of foreign workers. Saudis tend to view these roles as beneath them. "Saudisation" policies that mandate replacing foreign workers with nationals confront not only skills mismatches but status-driven resistance.

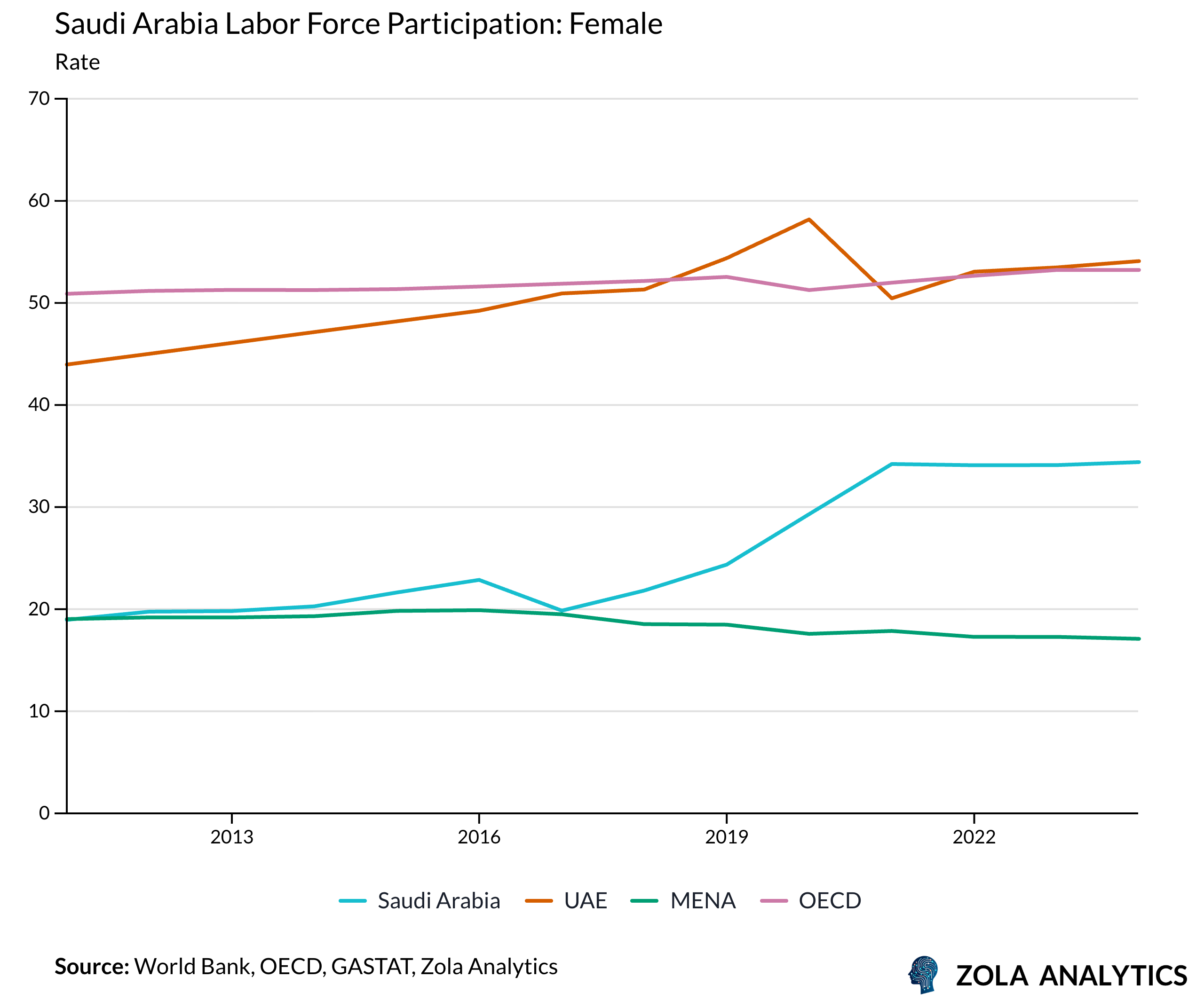

On the other hand, Vision 2030's labour market reforms have produced measurable progress. Overall unemployment has dropped from 12% to 7%. Female labour force participation has surged from 23% to 36%, a dramatic social shift in a society where women's economic participation was severely restricted.

These gains demonstrate that policy can move entrenched structures. The question is whether this momentum can be sustained as more difficult reforms such as skill development, private sector competitiveness, and meritocratic hiring remain incomplete.

What’s The Rush?

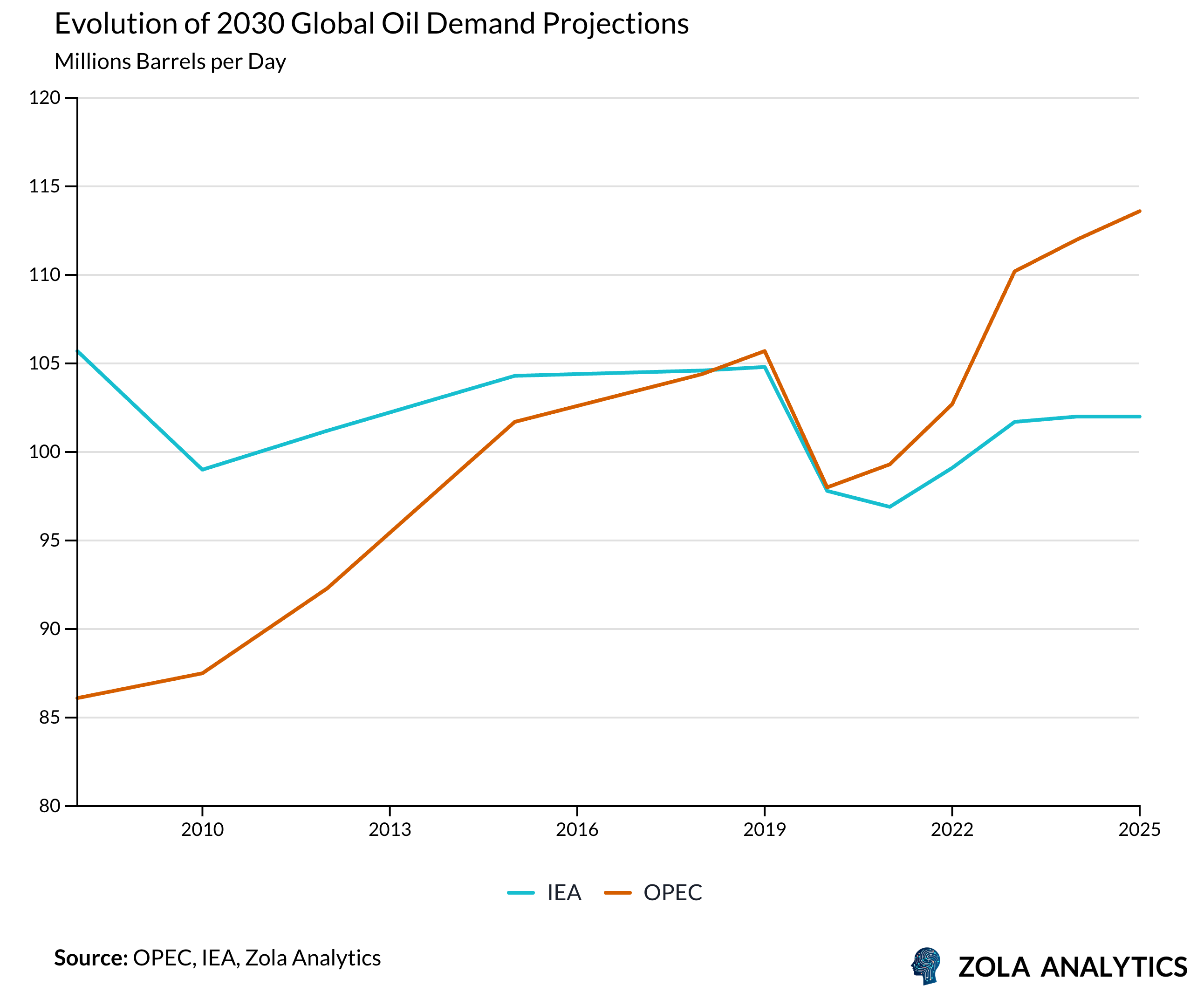

Vision 2030 is frequently framed as a response to projections that oil demand is in structural decline. Yet this explanation alone does not withstand scrutiny. The IEA projects oil demand peaking before 2030, while OPEC sees demand rising through 2050. Whoever is right, reality likely involves a protracted plateau rather than sharp decline.

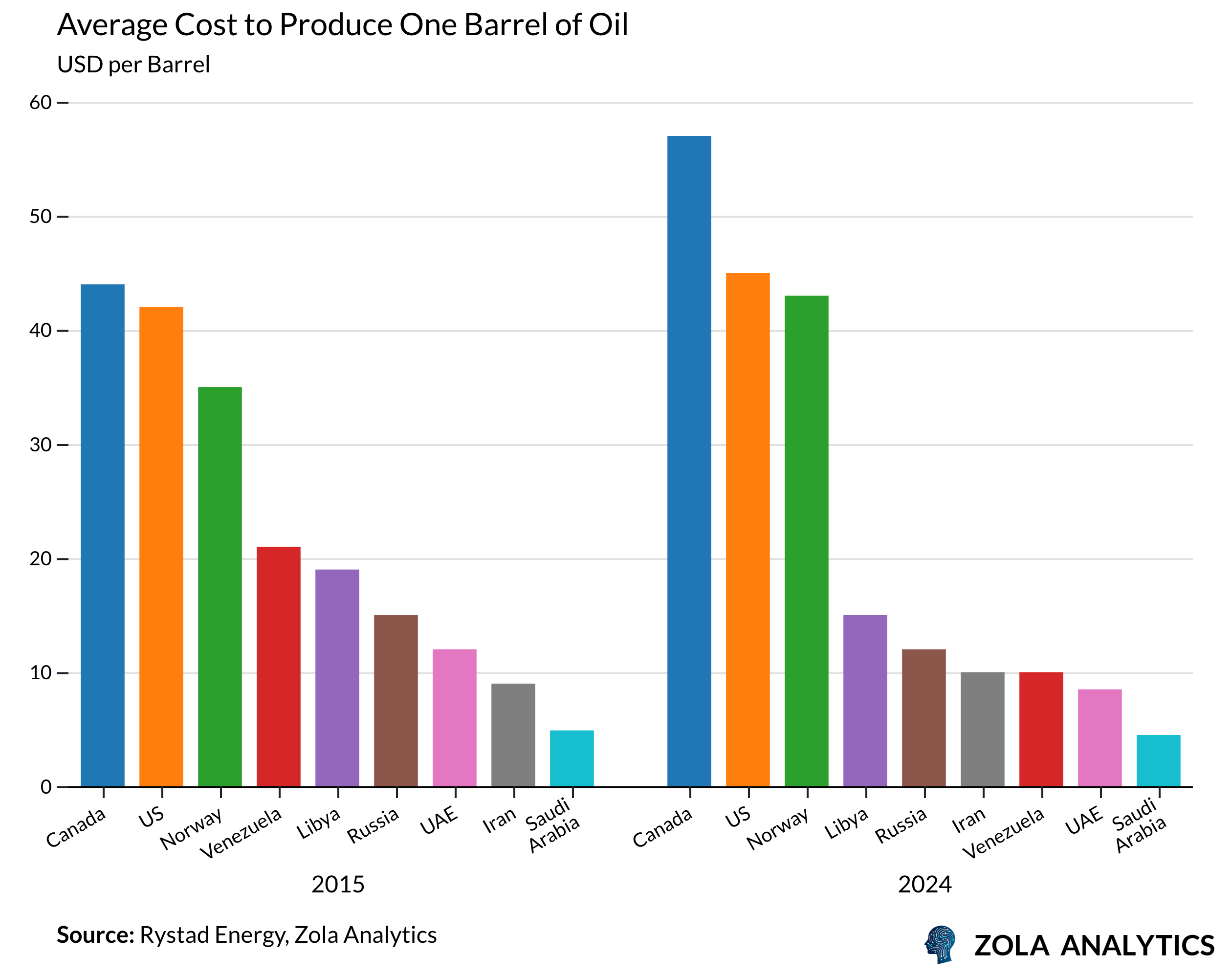

More importantly, Saudi's cost position means the Kingdom will continue producing profitably long after marginal producers shut down. When your lifting costs are USD 3 per barrel, you can tolerate substantial price volatility.

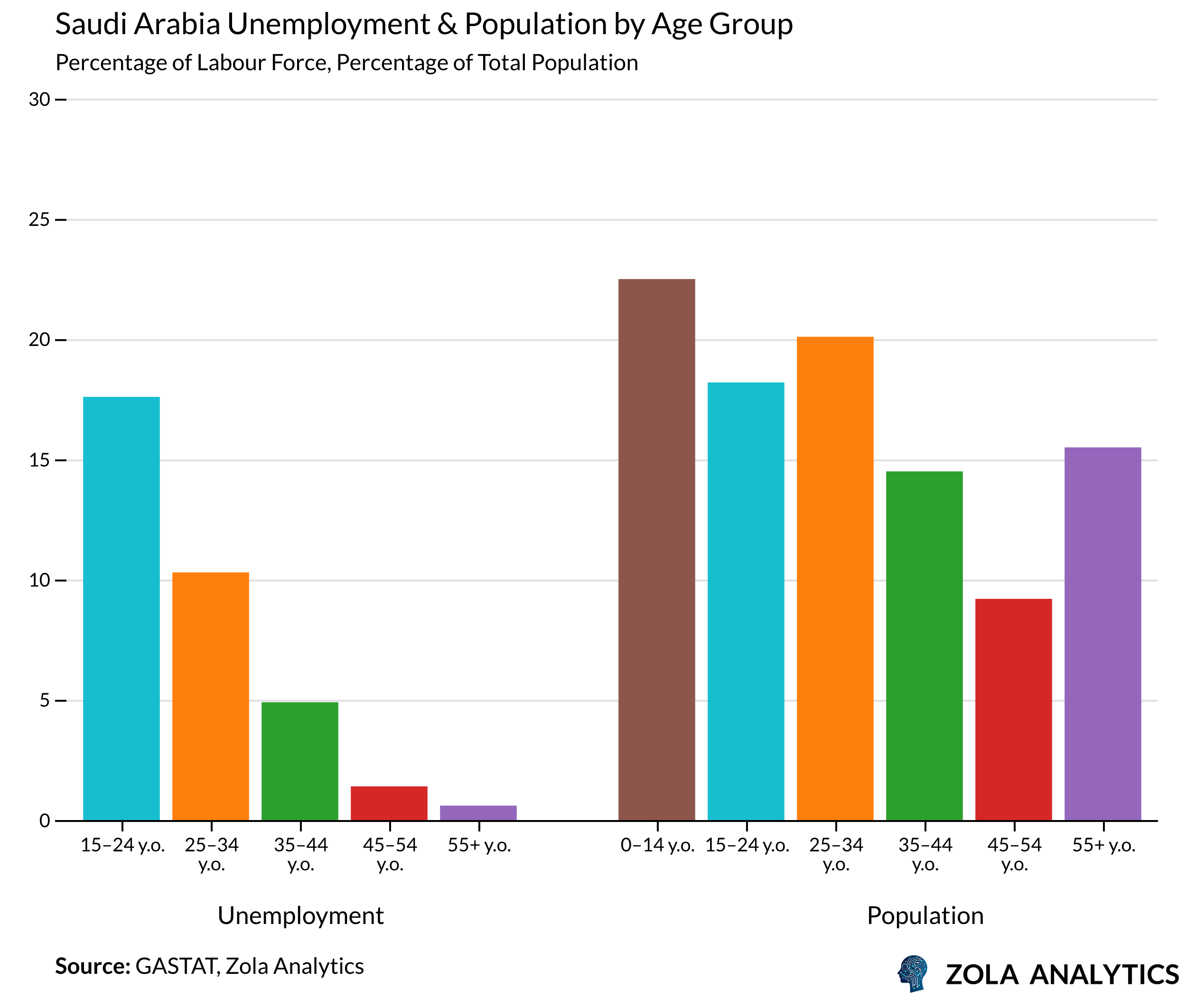

The actual drivers of urgency are older and more fundamental. Over 70% of Saudis are under 35, with youth unemployment at 17.6%. The oil sector, despite dominating government revenue, employs relatively few workers.

Therefore, the public sector jobs can't absorb the wave of graduates entering the labour market annually.

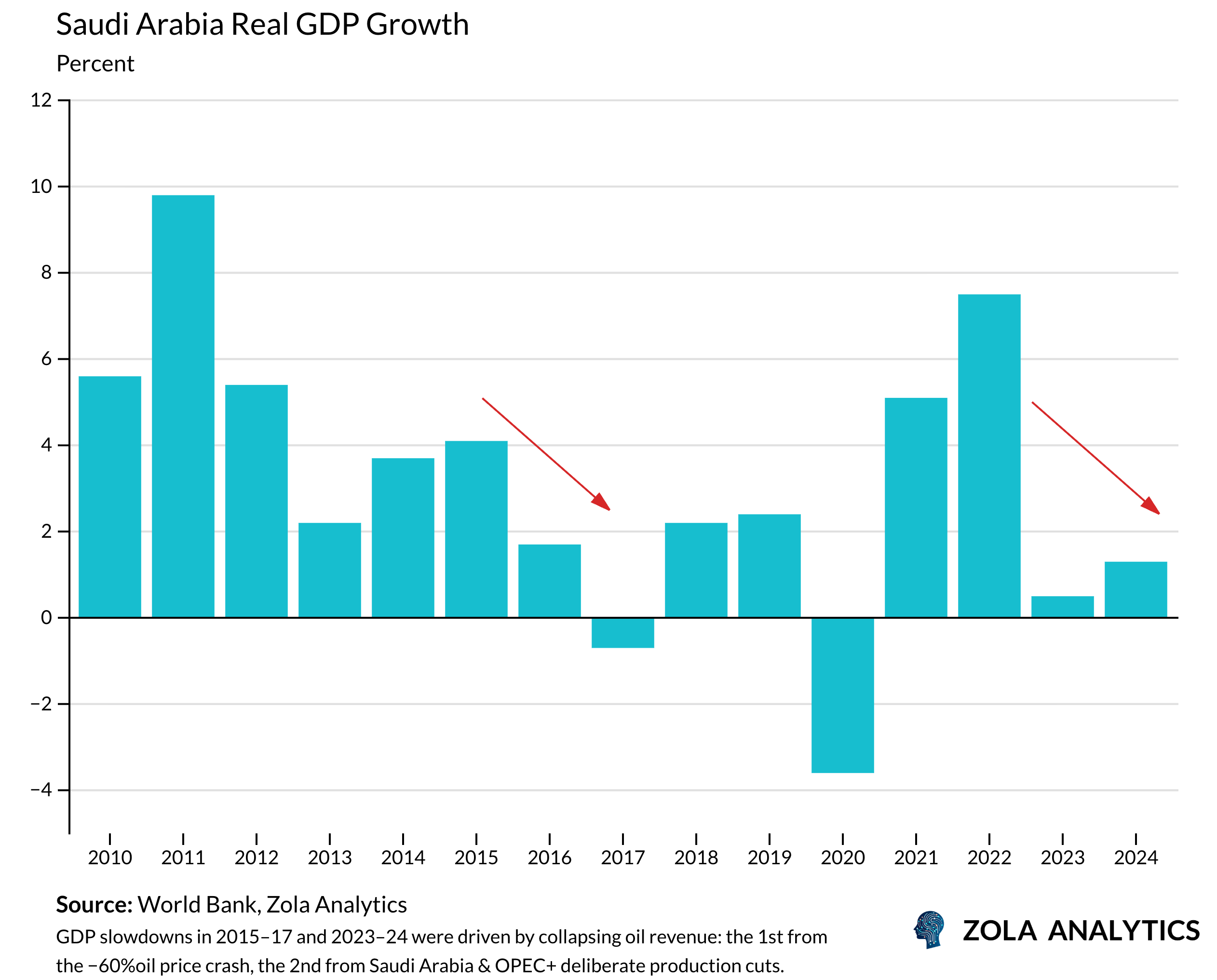

When Brent crude collapsed from USD 110 in 2014 to USD 30 in 2016, Saudi GDP growth slowed sharply in 2014 and turned negative in 2017, revealing how price swings transmit disproportionately into domestic activity because diversification has not progressed at the pace earlier plans envisioned.

Norway offers an instructive contrast. When North Sea oil revenues began flowing in the 1990s, Norway established its sovereign wealth fund and spent decades methodically building alternative income. Patient, generational wealth-building. Saudi Arabia can't replicate that approach because demographic and political pressures demand immediate results.

The Financing Crunch

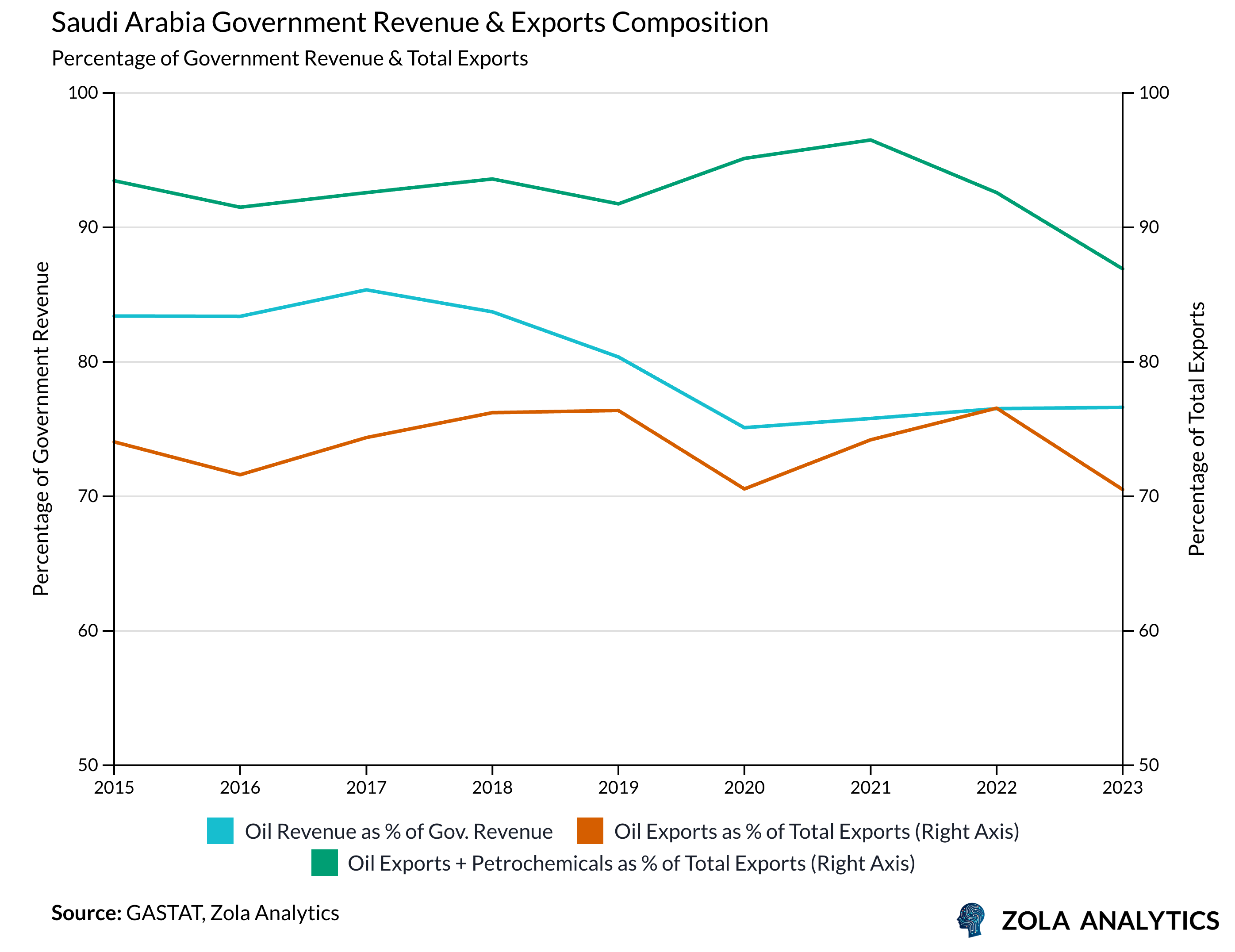

Curing Dutch disease and restructuring the labour market requires sustained investment. But Saudi's fiscal situation is a significant constraint. Diversification must be financed by the oil revenues the Kingdom is trying to move beyond. Oil revenues comprise 77% of government income and 70% of exports.

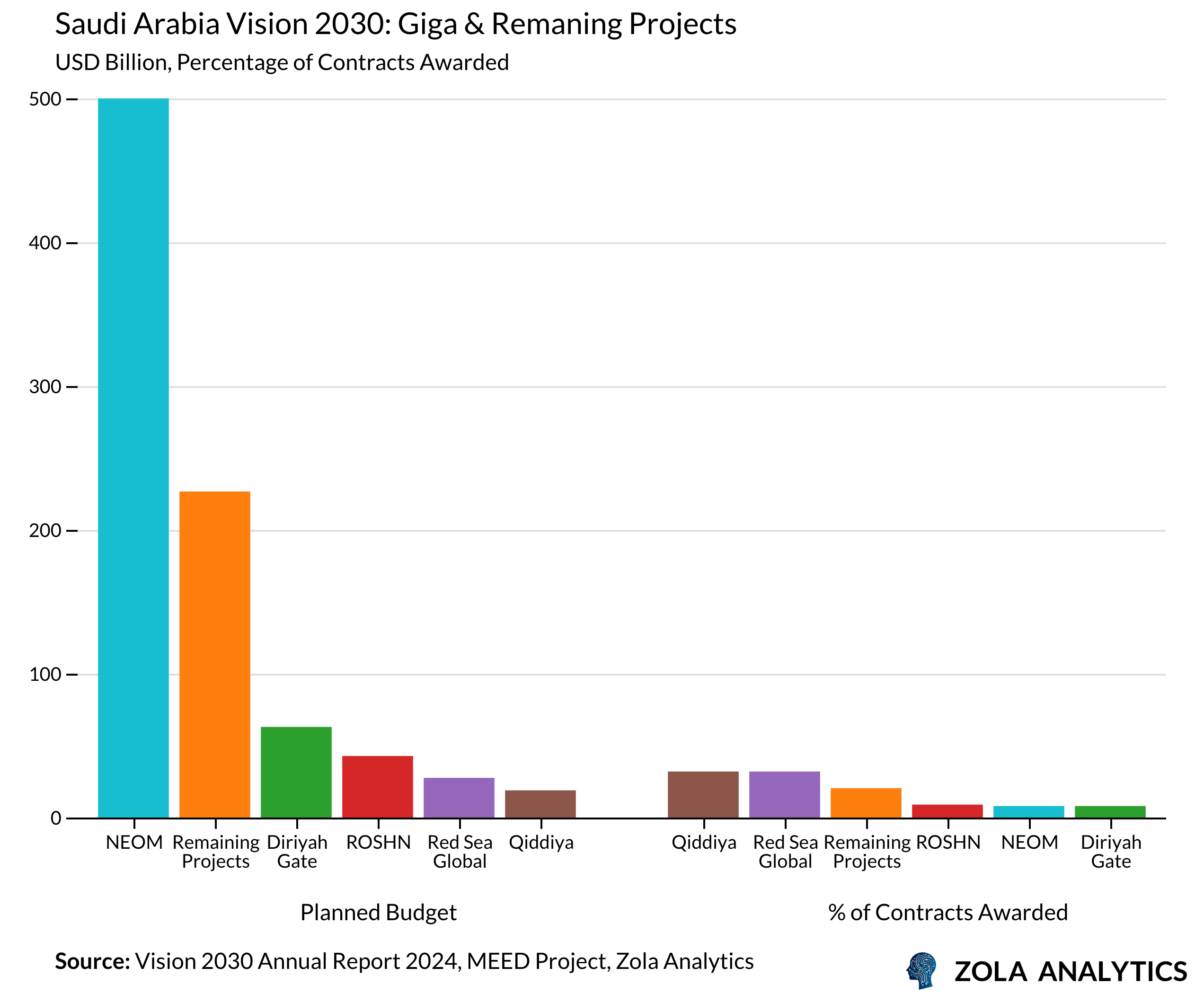

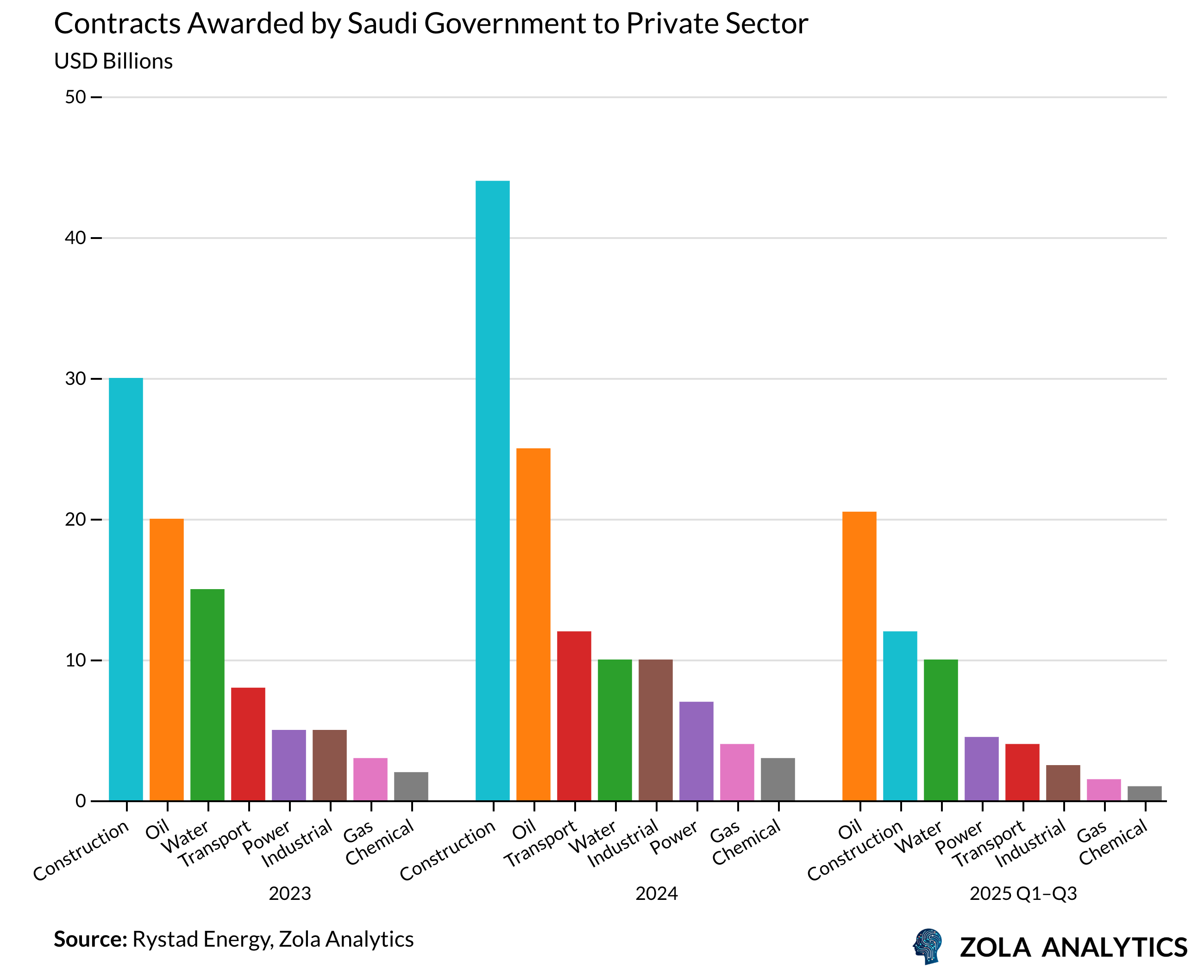

The ‘giga projects’ require investment on a scale that exposes the central tension of the strategy, diversification must be financed by the very revenue base it aims to diminish.

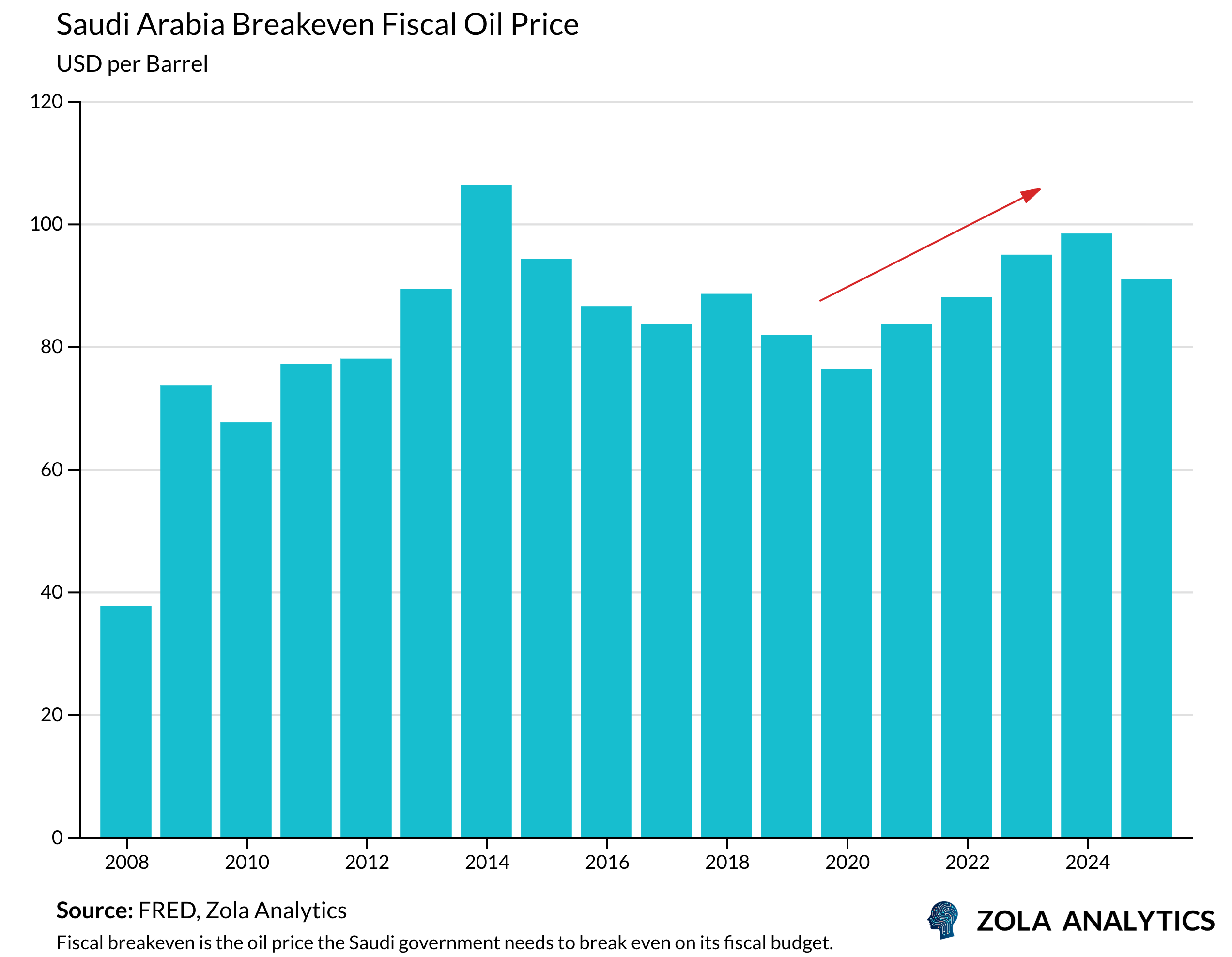

Partly as a result of this massive investment, the Kingdom’s breakeven fiscal oil price has begun to rise.

Initial financing came from the government budget and the kingdom’s sovereign wealth fund (PIF) but OPEC+ production cuts over the past two years have constrained oil revenues precisely when capital demands peaked.

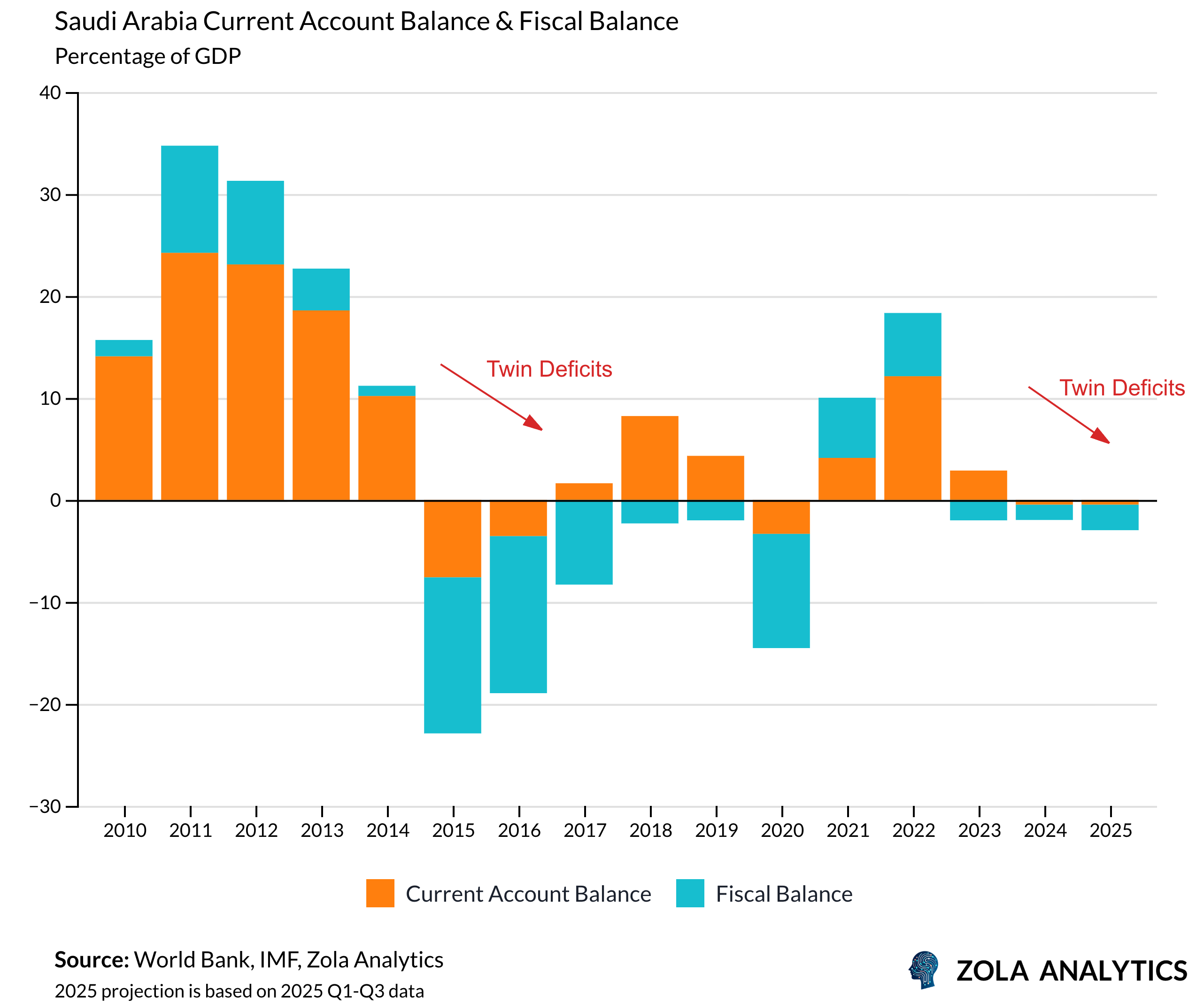

By 2024-2025, financial strain is forcing a strategic pivot. Twin deficits (both fiscal and current account) emerged. Public debt climbed to 30% of GDP. The PIF imposed budget cuts exceeding 20% for 2025. NEOM's signature project, The Line, originally envisioned as a 170-kilometre linear city, has been quietly scaled back, with only 2.4 kilometres targeted for initial completion by 2030.

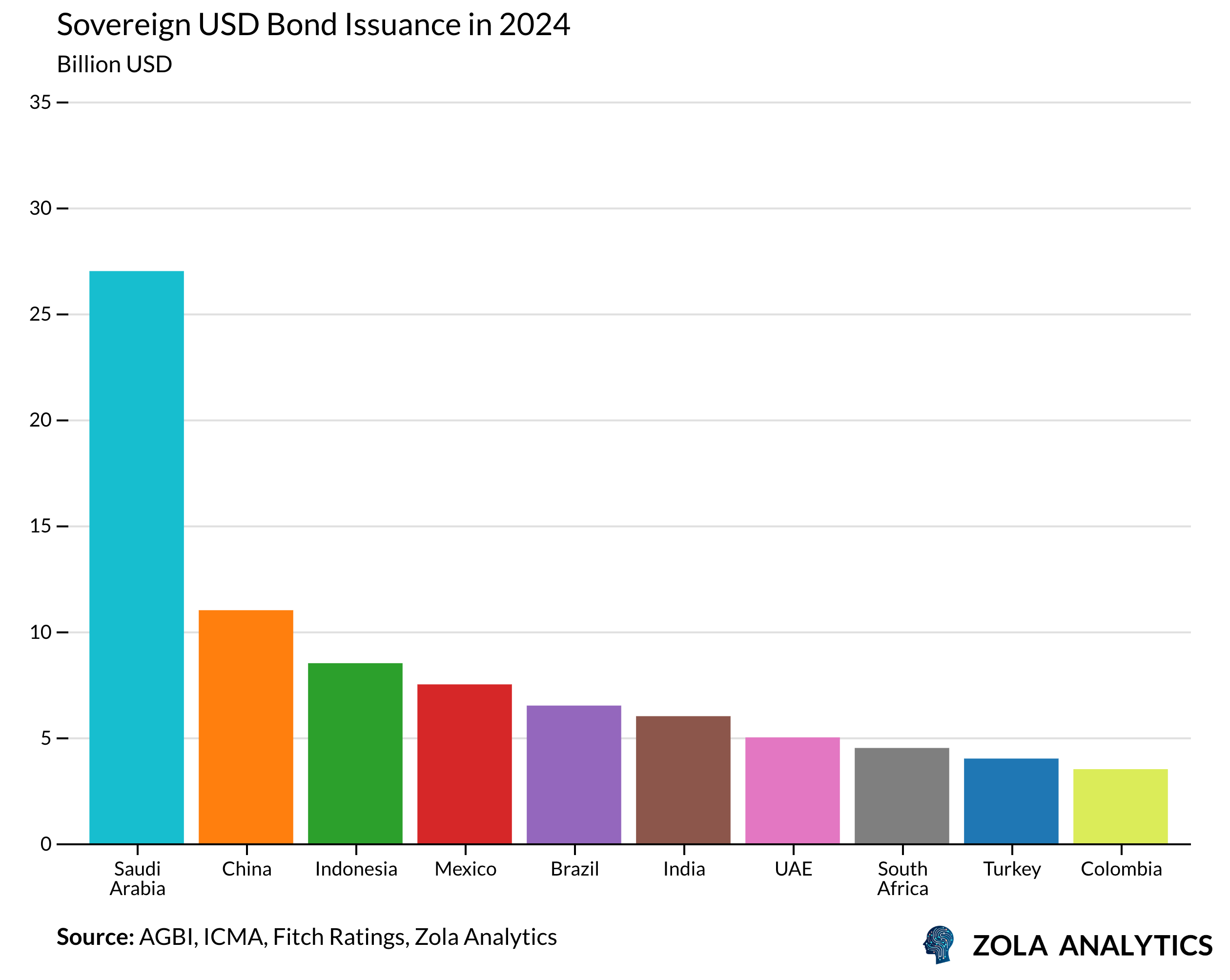

The strategy is shifting from prestige mega-projects to event-driven infrastructure, a recalibration that signals an implicit recognition of funding constraints rather than a thematic reorientation: Riyadh Expo 2030 and FIFA World Cup 2034. These create hard deadlines and defined capital requirements, a marked departure from the open-ended ambition of projects like NEOM. In 2024, Saudi Arabia became the world’s largest EM hard currency bond issuer, overtaking China, as the government increasingly relies on international debt markets to bridge the gap between ambition and oil revenues.

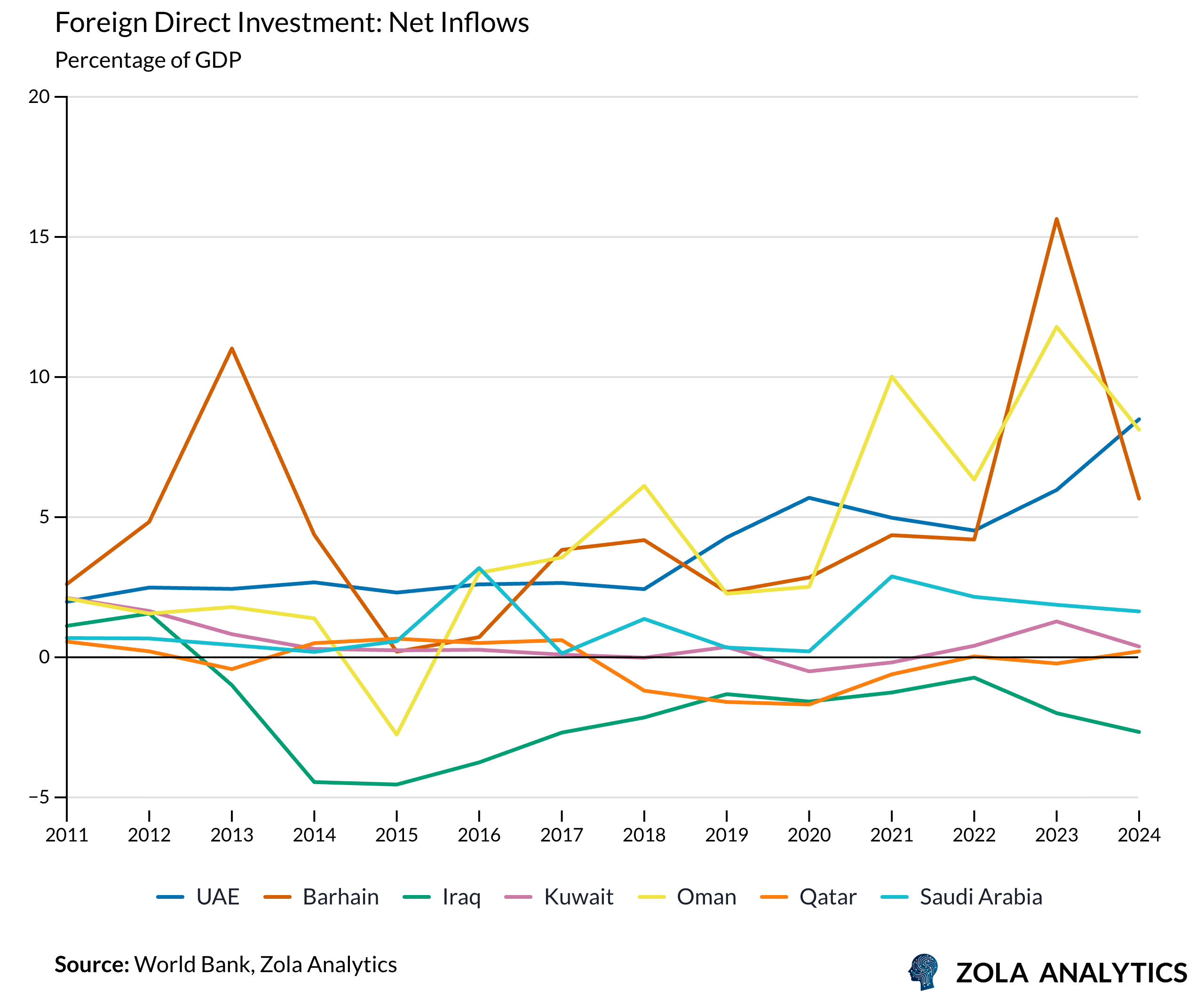

Foreign direct investment outside the oil sector remains disappointingly low at just 1.6% of GDP, far short of the USD 100 billion annual target by 2030. The PIF itself, facing capital constraints, has sought external financing partnerships with Goldman Sachs, BlackRock, and Japanese banks, a telling admission that domestic oil revenues alone can't fund the diversification agenda.

The Verdict

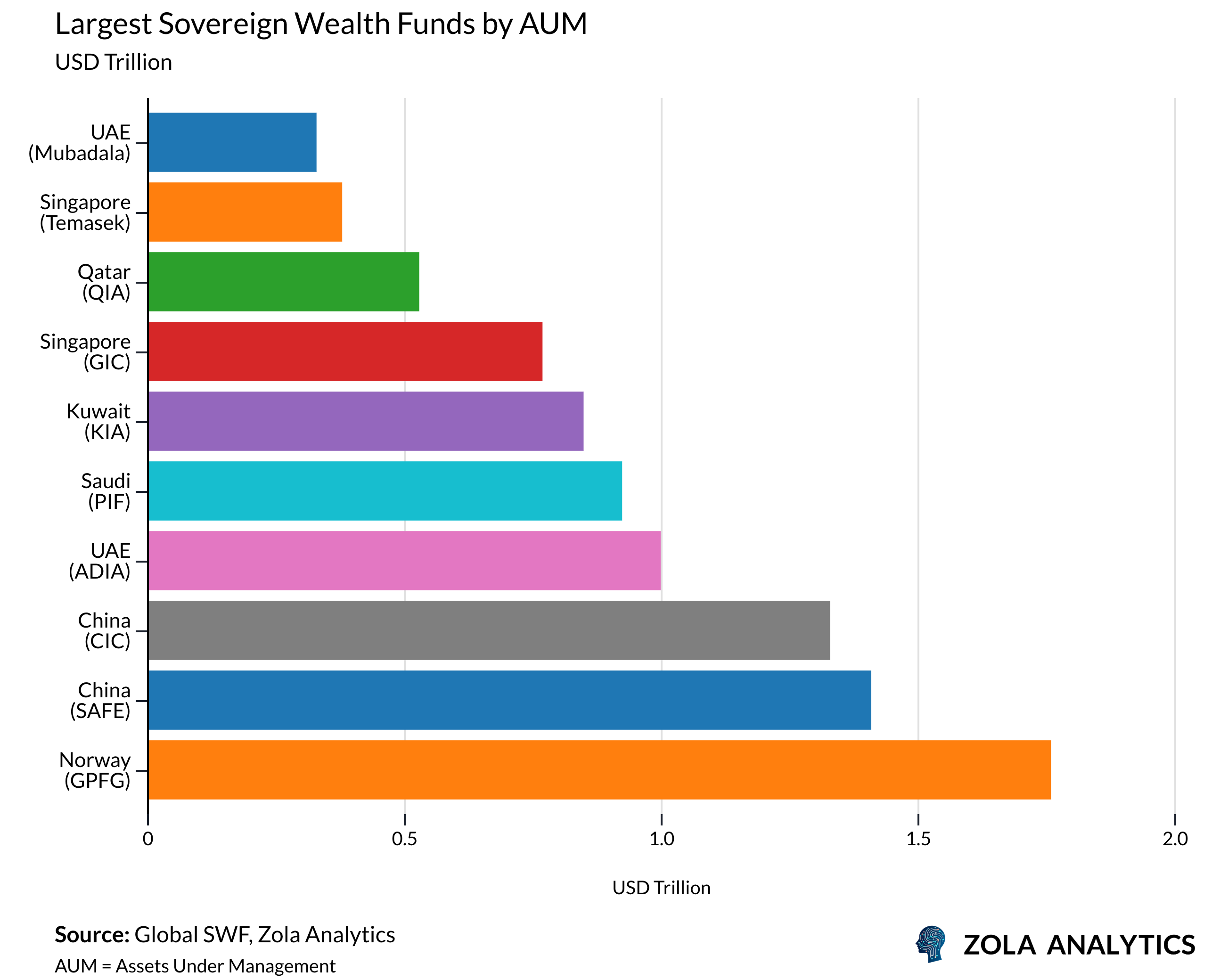

Saudi Arabia’s success depends on how one defines it. Fiscal collapse or social unrest appears unlikely: oil demand will plateau rather than collapse, the PIF holds over USD 900 billion, and political will is strong given that the Crown Prince has staked legitimacy on Vision 2030.

Achieving 50% non-oil exports as a share of non-oil GDP, creating competitive manufacturing sectors, absorbing youth cohorts into productive private sector employment, looks equally unlikely. The obstacles are too deep: competitiveness deficits from decades of Dutch disease, entrenched political interests resistant to reform, skill mismatches that can't be resolved quickly.

The most probable outcome is partial diversification, with reduced but persistent oil dependence, moderate employment growth, and modernisation that preserves political hierarchies. Labour market reforms demonstrate progress, while project delays and financing constraints highlight execution limits.

The crucial question is deployment strategy. The emphasis on mega-projects over productive capacity raises fundamental questions. NEOM is a bet on luxury tourism and tech clusters and it is unclear whether these will generate competitive tradable sectors. A smarter path prioritises manufacturing capacity, technology transfer, education reform, and infrastructure that would sustain tradable goods production.

While Saudi Arabia has scaled back some of its most high-profile Vision 2030 projects, most notably The Line, the Kingdom is simply shifting obsessions. From drawing straight lines in the sand to wiring the desert with fibre and flooding it with hundreds of thousands of Nvidia GPUs. They have just announced a500 MW xAI-Humain data centre, which will be the largest AI compute hub outside the United States. Whilst cheap energy, vast land, and sovereign patience offer significant advantages, this yet again represents the dependence on energy that the leadership is so desperate to break.

Saudi Arabia has vast resources to navigate its challenges, but recent experience shows that success is not a matter of spending money but of conducting unglamorous and difficult reforms. The critical bottlenecks in human capital and decision making capacity, undermine their ability to execute on the reforms themselves and free the economy from its dependence on oil.