Published 10th October 2025

12 minute read

Elements of Power

In 1787, a Swedish army officer and hobbyist chemist discovered a dark rock in Ytterby, near Stockholm. His curiosity piqued by its unusual heavy weight, he sent samples to various chemists for analysis. At the Royal Academy of Turku, a new oxide, named yttria, was discovered in the sample. At the time, discovery of a new oxide was considered equivalent to discovery of a new element so Yttrium became the first identified member of the family we now know as the rare earth elements. The set was completed in 1945 when Promethium was isolated in the products of uranium fission in Oak Ridge, Tennessee. This once obscure family of metals now underpins the world’s most advanced technologies. They have grown from a chemical curiosity into a strategic resource that nations compete fiercely to control.

On Thursday 9th October, Beijing announced a sweeping expansion of export controls on rare earths, tightening further its hold over the global semiconductor supply chain. Markets barely blinked, perhaps taking the view that this is China’s way of creating leverage ahead of Xi’s meeting with Trump at APEC. But if aggressively enforced, this would have profound implications, not only for the semiconductor industry, but also for the global economy.

But what are rare earths? Why are they important? And why should we care that they are now taking center stage in the strategic competition between the US and China? In this week’s edition of Zola Chartbook, we answer these questions.

What are rare earths?

Rare earths are a group of seventeen metallic elements that share similar chemical properties and often occur together in the same mineral deposits. They’re prized not for their shine or rarity, but for their magnetic, luminescent, and catalytic qualities.

Why are rare earths rare?

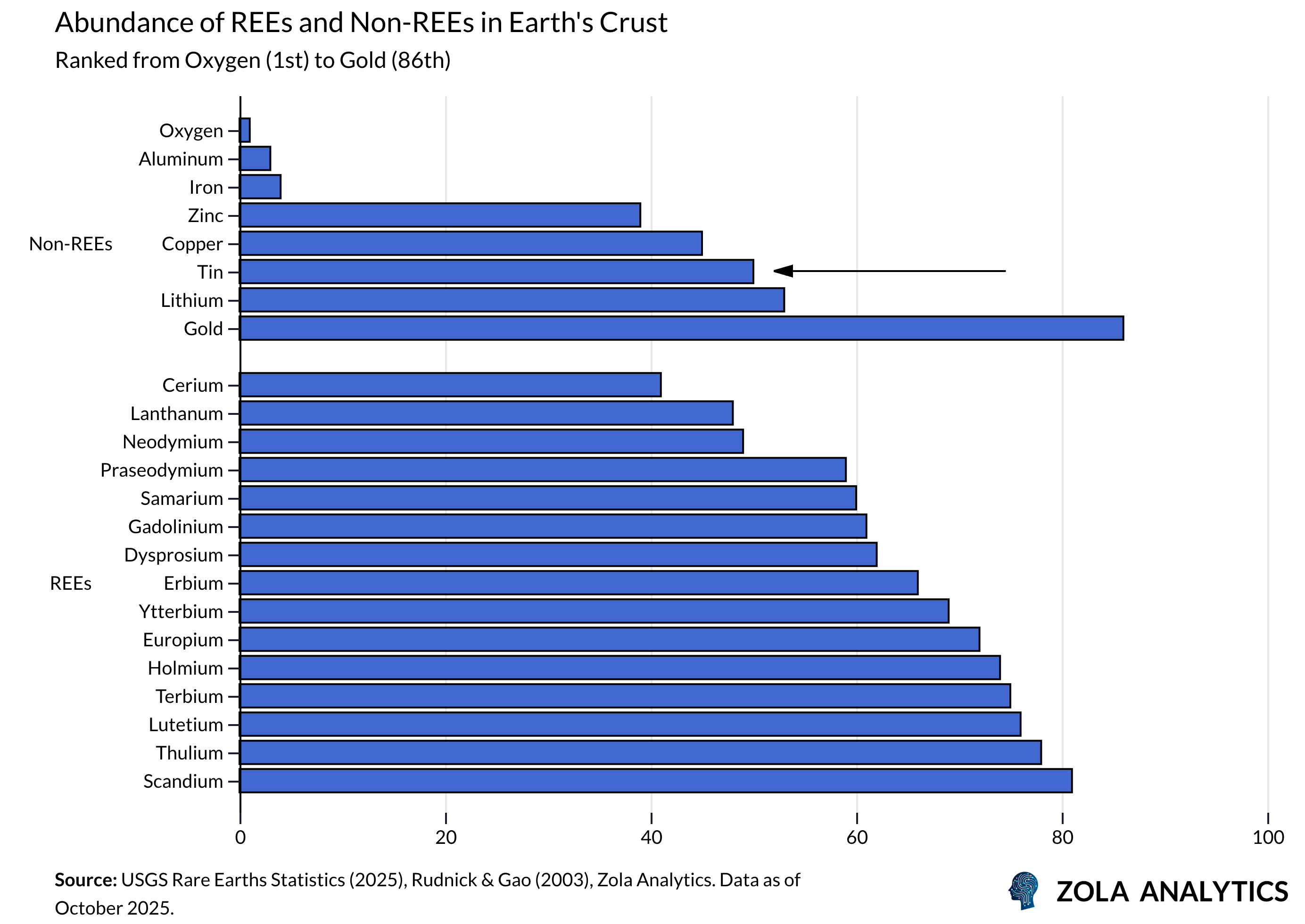

Despite their name, rare earths are not geologically scarce. Cerium, lanthanum, and neodymium are more common in the Earth’s crust than tin (although they seldom occur in concentrated deposits). Because these elements behave so similarly chemically, separating them takes complex, energy-intensive processing. Their rarity lies in the complexity of refining them into usable form.

Why are rare earths important?

Rare earths are essential inputs for the technologies that underpin modern manufacturing, energy, and defence. They are critical to the production of semiconductors, electric vehicles, wind turbines, and advanced imaging systems. Their unique magnetic and conductive properties make them irreplaceable in high-performance components where precision and efficiency are paramount.

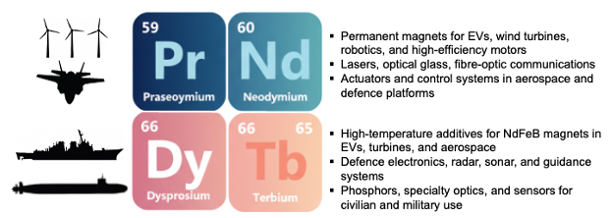

The most important use of rare earths is in permanent magnets, which retain magnetic strength without external power. Neodymium and praseodymium are used in the motors of electric cars, turbines, and industrial robots. Dysprosium and terbium allow these magnets to operate at high temperatures, which is necessary in aerospace, defence, and semiconductor fabrication equipment.

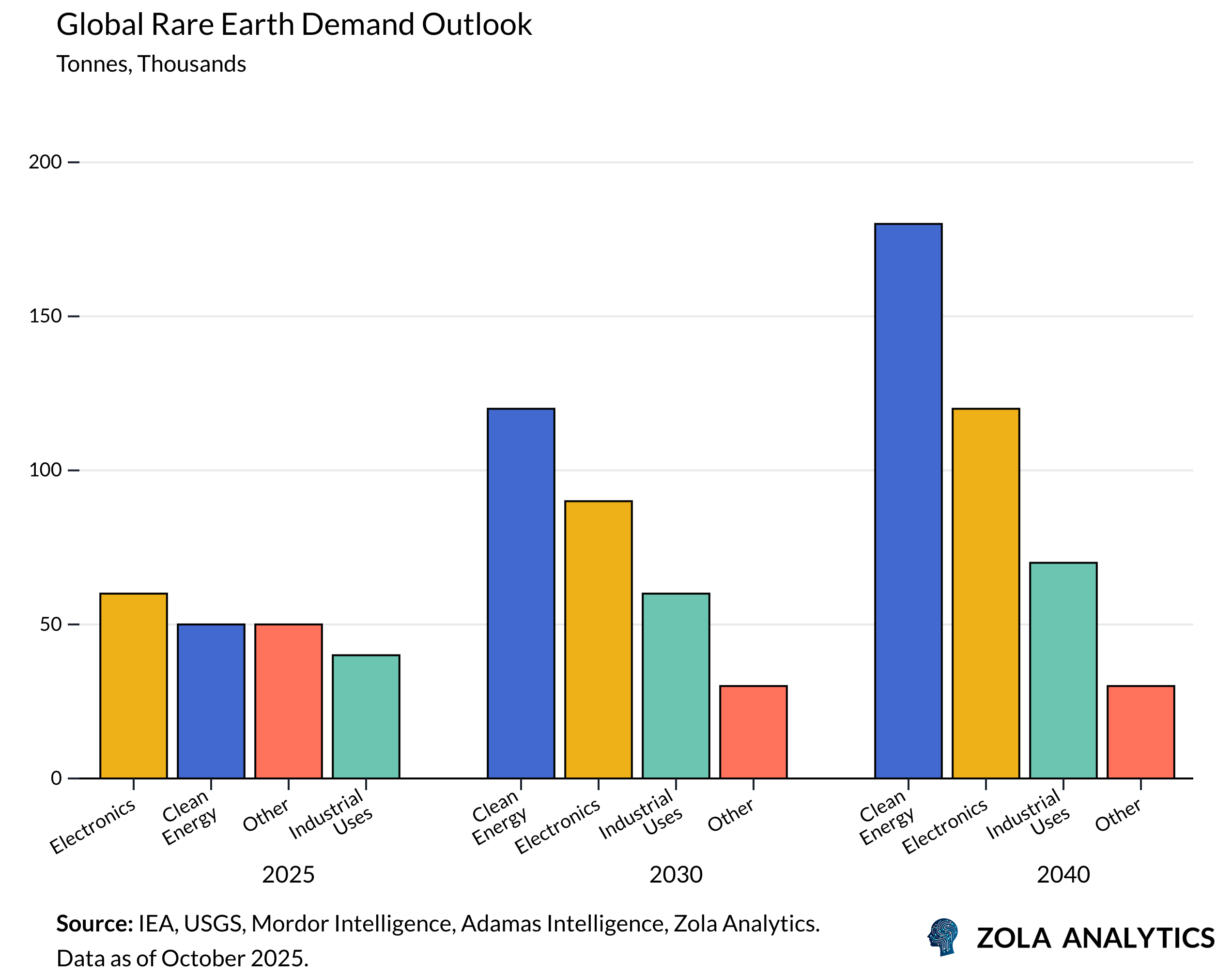

Demand is rising rapidly as the clean energy transition accelerates. In the IEA’s Sustainable Development Scenario, global use of rare earths in clean technologies is projected to triple by 2040, with renewables overtaking electronics as the largest source of demand. Europium, gadolinium, and lanthanum, once used mainly in color displays and medical scanners, are now applied across optics, imaging, and sensor systems. The defence sector is another major consumer: an F-35 fighter jet contains about 400 kilograms of rare earths; a destroyer about 2.5 tonnes; a submarine more than four tonnes.

Together, these applications make rare earths a central input to the global industrial and technological system.

Why does China dominate the rare earth supply chain?

While the Chinese Communist Party often preaches Marxist pieties while practising market capitalism, one part of Leninist doctrine it has never abandoned is the injunction to control the “commanding heights” of the economy. Jiang Zemin later reframed this as grasping the large, letting go of the small; keeping strategic sectors under state control while allowing market forces to operate elsewhere. Few industries illustrate that philosophy more clearly than rare earths.

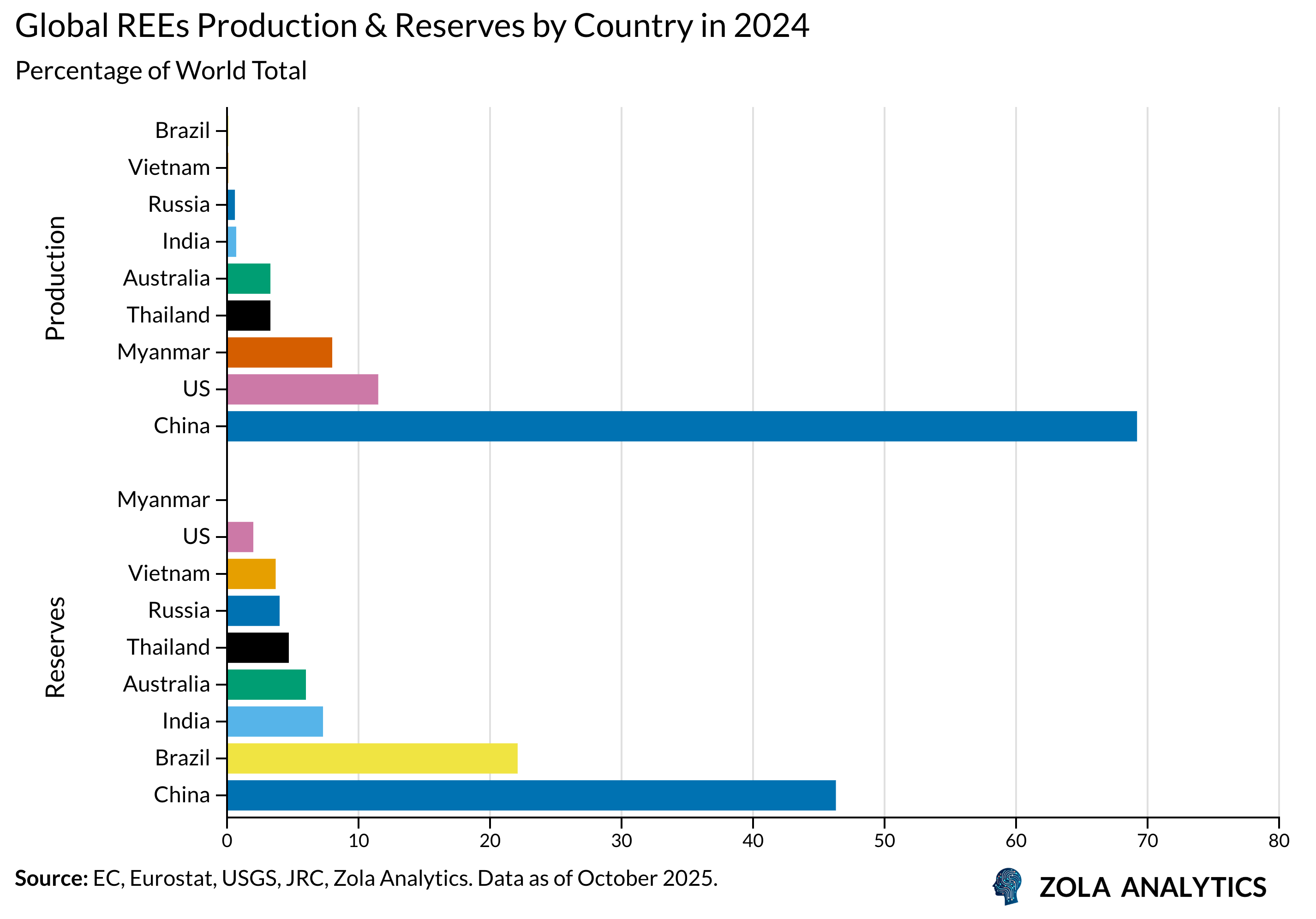

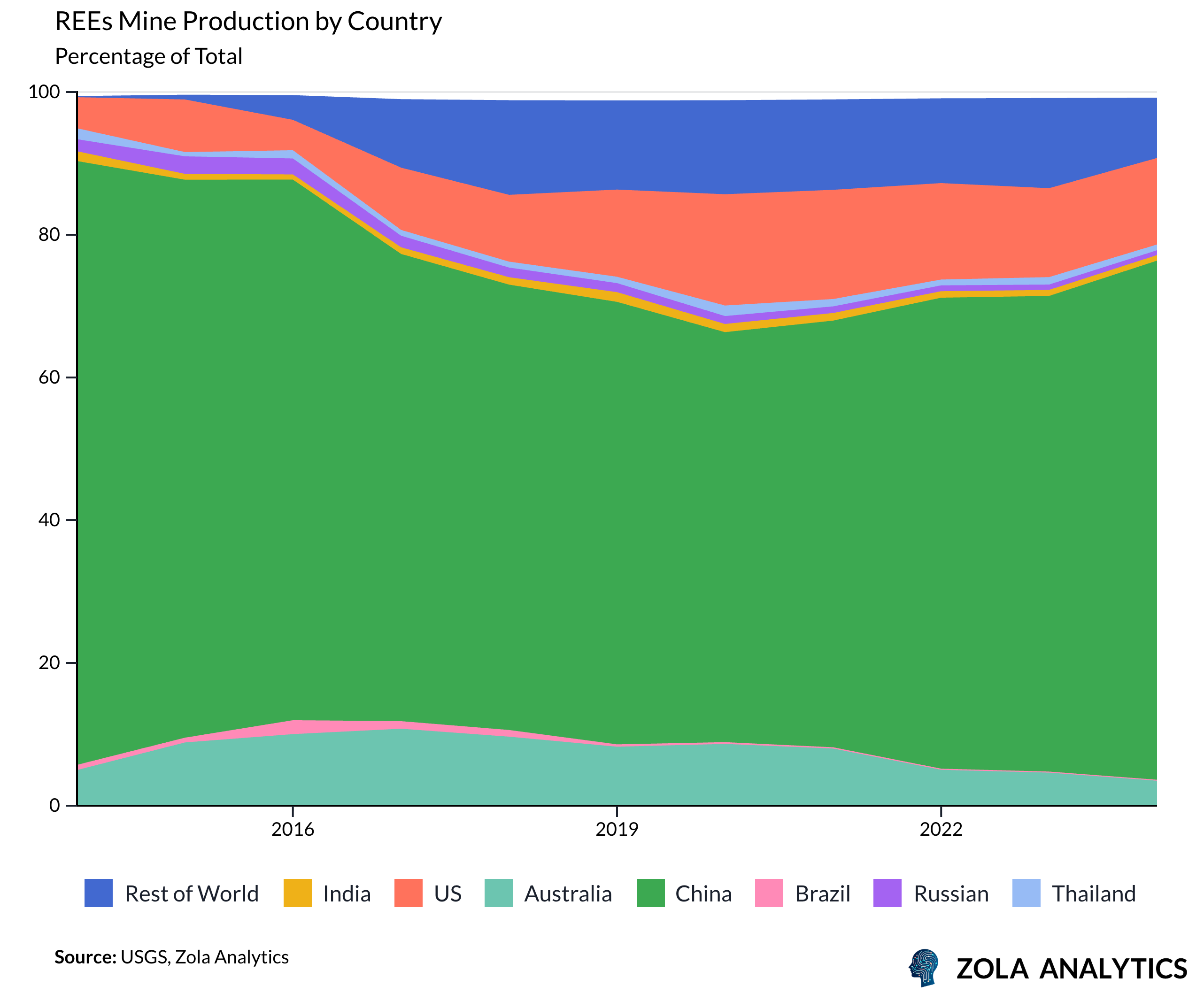

China’s dominance in rare earths is the product of deliberate, long-term industrial planning, not geological advantage. It now accounts for roughly 70% of global mine output and more than 90% of global refining and magnet manufacturing. This dominance extends across extraction, processing, and component production, creating a vertically integrated system that no other economy can match.

The United States once led global supply through the Mountain Pass mine in California, developed during the Manhattan Project and expanded in the decades that followed. Yet environmental regulation, price volatility, and the liberalisation of commodity markets eroded its competitiveness. Beginning in the 1980s, Beijing charted the opposite course. Backed by state subsidies, cheap power, and long-term investment in hydrometallurgy, China built a complete mine-to-magnet chain that gradually absorbed global refining capacity. Today, its advantage is institutional and cumulative, resting on industrial coordination, capital discipline, and policy continuity rather than on resource endowment alone.

What are the geopolitical implications of Chinese dominance?

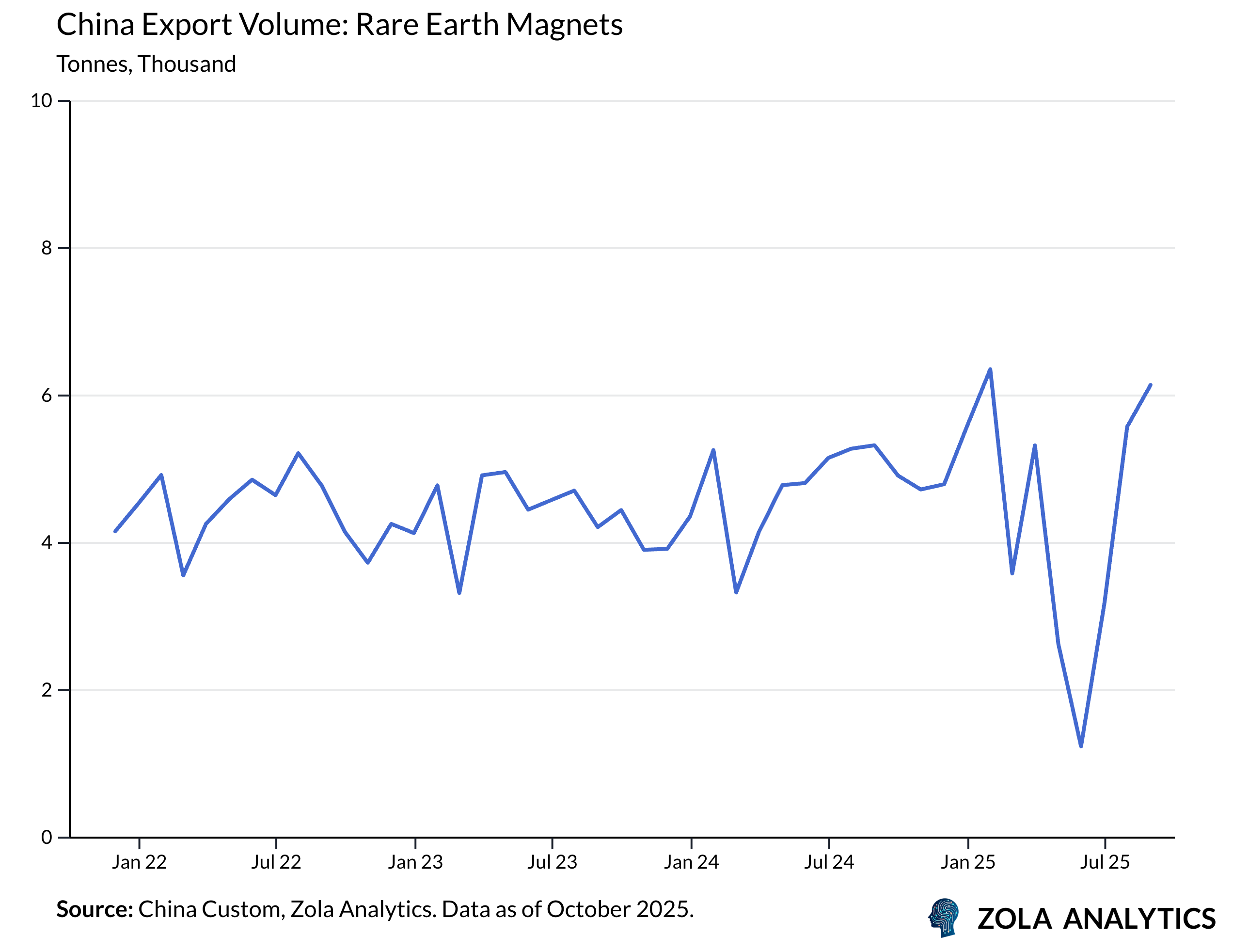

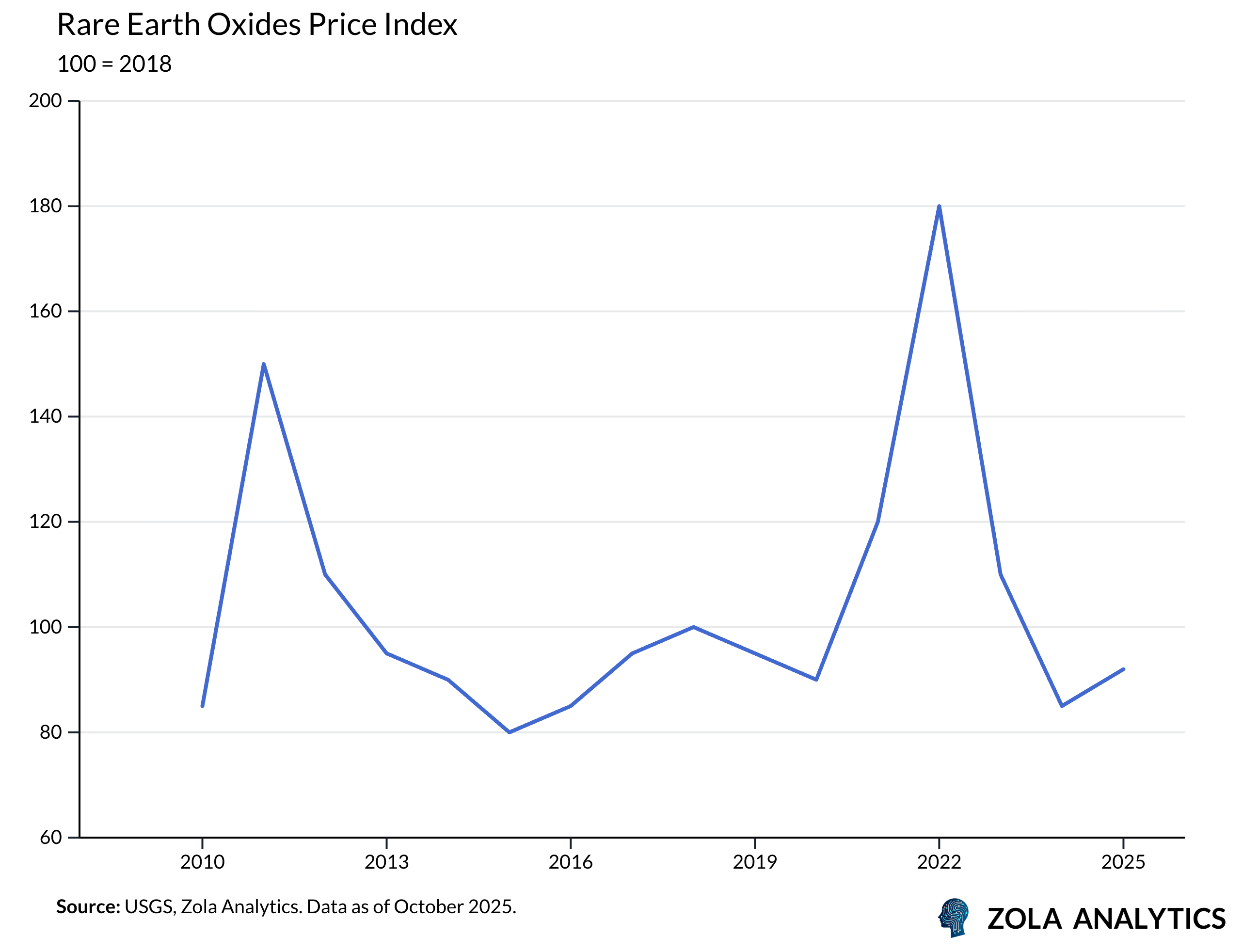

Control of these elements has become one of Beijing’s most effective instruments of economic statecraft. In 2010, during a maritime dispute with Japan, exports were abruptly curtailed, sending global prices soaring and exposing the fragility of downstream supply chains. Fifteen years later, in April 2025, the government imposed new export licensing requirements on seven medium and heavy rare earths, driving up prices for dysprosium and terbium and sharply reducing magnet exports. By October, restrictions were extended to processing technologies and products with defence applications, tightening China’s grip still further.

Officially framed as a countermeasure to US tariffs, these measures form part of a broader grey-zone strategy: exerting economic pressure without a formal embargo. The message was clear. Control over rare earths, indispensable to semiconductors, electric vehicles, renewable energy, and advanced weapons systems, gives Beijing a form of leverage that is quiet but flexible.

What are other countries doing to reduce dependence?

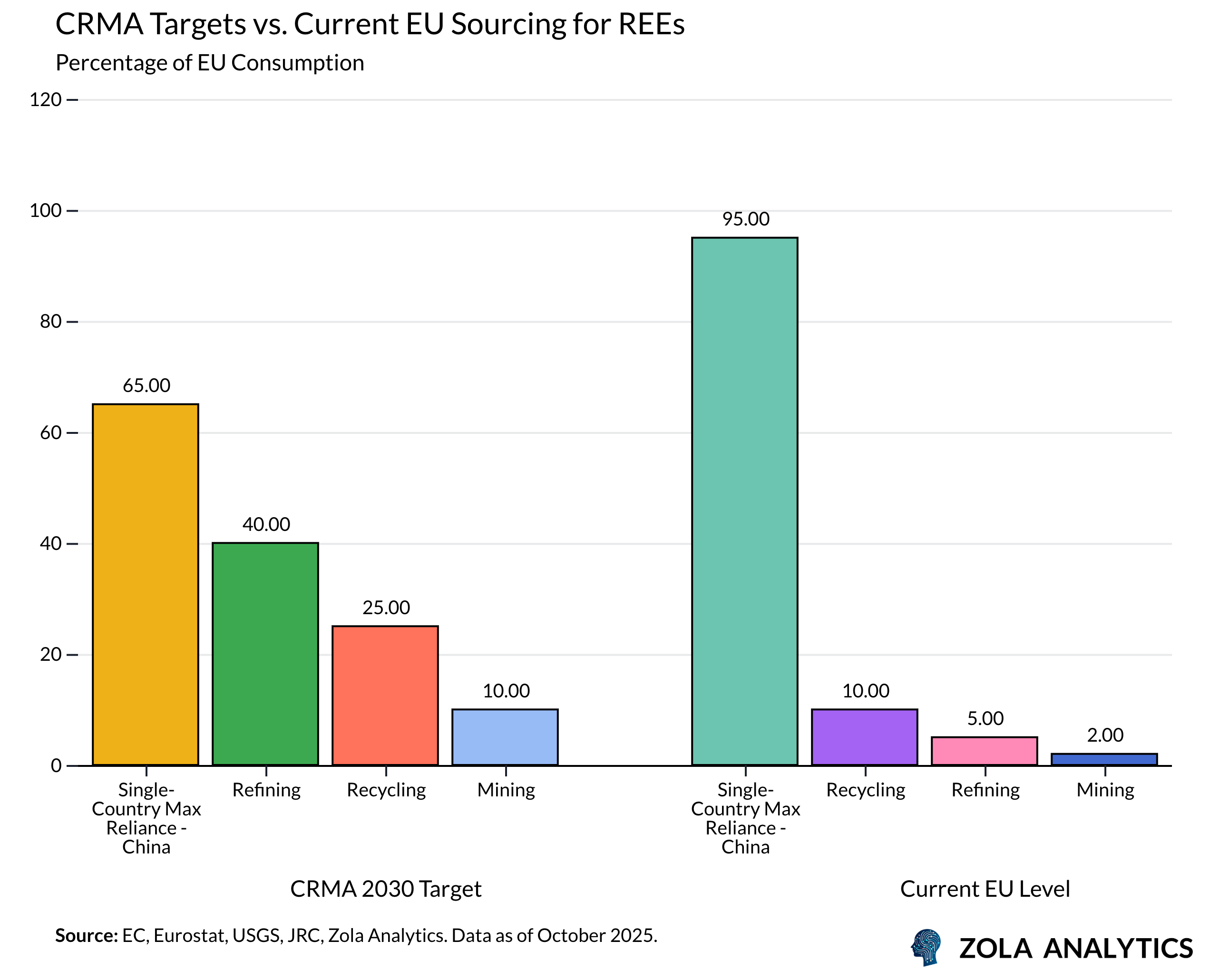

Outside China, efforts to rebuild and diversify supply chains have gained urgency, but progress remains limited relative to the scale of demand. The United States has allocated more than USD 400 million to domestic mining and processing under the Inflation Reduction Act, and a further USD 900 million through defence and energy programs to develop an integrated mine-to-magnet system. The EU’s Critical Raw Materials Act sets binding 2030 targets of 10% domestic mining, 40% processing, and no more than 65% dependence on any single supplier. The Minerals Security Partnership, which brings together the United States, the EU, Japan, and other allies, has committed over USD 1 billion to projects in Africa, Latin America, and Southeast Asia.

Recycling and “friend-shoring” are expanding with public incentives, but both face structural constraints. Feedstock is limited, recovery technologies remain inefficient, and environmental approvals continue to delay new facilities. The result is steady but gradual progress rather than a decisive shift. Still, the coordination of policy, capital, and security objectives represents the first sustained attempt in decades to rebalance a supply chain that has long been shaped by China’s industrial model.

What risks does the rare earth market face?

The global rare earth market remains narrow, volatile, and highly exposed to policy intervention. Prices are set mainly through Chinese spot exchanges, where even small quota changes can trigger sharp swings. In 2024, weakness in battery metals pushed prices lower and discouraged Western investment. Yet any tightening of Chinese export rules can reverse that pattern almost overnight. The result is a market that reacts more to policy than to fundamentals.

The deeper risk is structural dependence. Concentration of supply has become both a strategic and an economic vulnerability. A sustained disruption in heavy rare earths such as dysprosium or terbium would hit advanced manufacturing and clean energy production across major economies. For the United States and its allies, material dependence now carries measurable macroeconomic cost.

The International Energy Agency estimates that prolonged export restrictions could raise the cost of clean energy and semiconductor production by 20-30%. This volatility discourages private investment and leaves Beijing as the market’s stabiliser of last resort. Fragility, once an exception, has become the defining condition of the system.

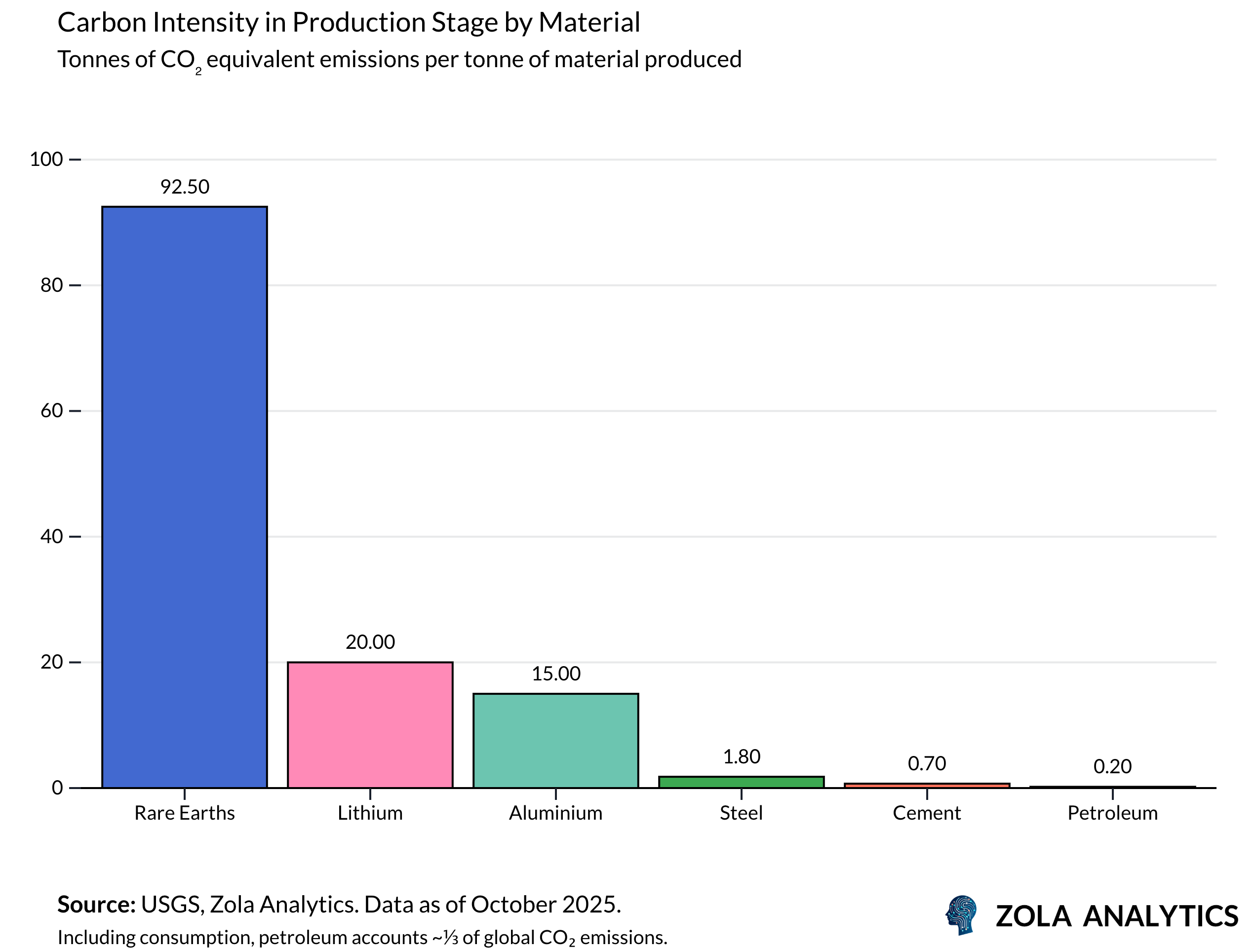

What are the environmental and social costs of rare earths?

The environmental cost of rare earth production remains high and largely unaccounted for. In China, decades of mining and refining have left radioactive tailings and chemical runoff that have contaminated soil and groundwater across parts of Inner Mongolia. Similar impacts are emerging elsewhere. In Southeast Asia, refining along the Mekong basin has produced toxic discharge and widespread deforestation. The result is a steady degradation of ecosystems in regions least able to manage industrial waste.

The social consequences follow the same pattern of imbalance. In the Democratic Republic of Congo, cobalt extraction, closely tied to critical mineral supply chains, has been linked to unsafe working conditions and child labour. Proposals for deep-sea mining present additional risks for fragile marine environments. Once refined and traded, the origin of materials becomes opaque, weakening accountability between producer and consumer. Without stronger certification systems and transparent oversight, the green transition could replicate the same extractive inequalities it is meant to address.

What lies ahead?

China’s export controls could cause major short-term disruption even if they do not alter the long-run balance. Supply is concentrated, so a strict cutoff or heavy licensing regime would quickly raise costs for semiconductors, magnets, and clean energy equipment and could slow production across chip fabs and manufacturing lines. Over time, higher prices and government support will draw new investment, spur recycling, and expand non-Chinese refining capacity. Rare earths can be produced at scale outside China with sufficient capital, predictable permitting, and sustained policy commitment. The challenge is structural rather than geological and solvable over the medium term.

Policymakers should plan for disruption and prepare both resilience and retaliation. Resilience means accelerating allied mine-to-refine projects, shortening approval times, improving recycling, and securing consumable inputs where stockpiles are thin. Retaliation can be selective: tighter export controls on semiconductor equipment and key consumables, targeted tariffs, and restrictions on Chinese access to advanced technology. The most immediate market risk lies in AI and chips. Tighter rare-earth flows could raise costs for packaging and GPUs, slow data centre build-outs, and trigger a pullback in the AI trade. Given high valuations and the weight of technology in global markets, the broader economy would feel the shock. The task now is to limit short-term damage while building a system that can absorb future stress. Over time, supply will prove to be elastic. Rare earths are not so rare after all.

Sign up to receive the Zola Global Macro Chartbook every week: https://www.zolaanalytics.com/insights?signUp