Published July 24st 2025

ECB Pauses After 200bps Cuts

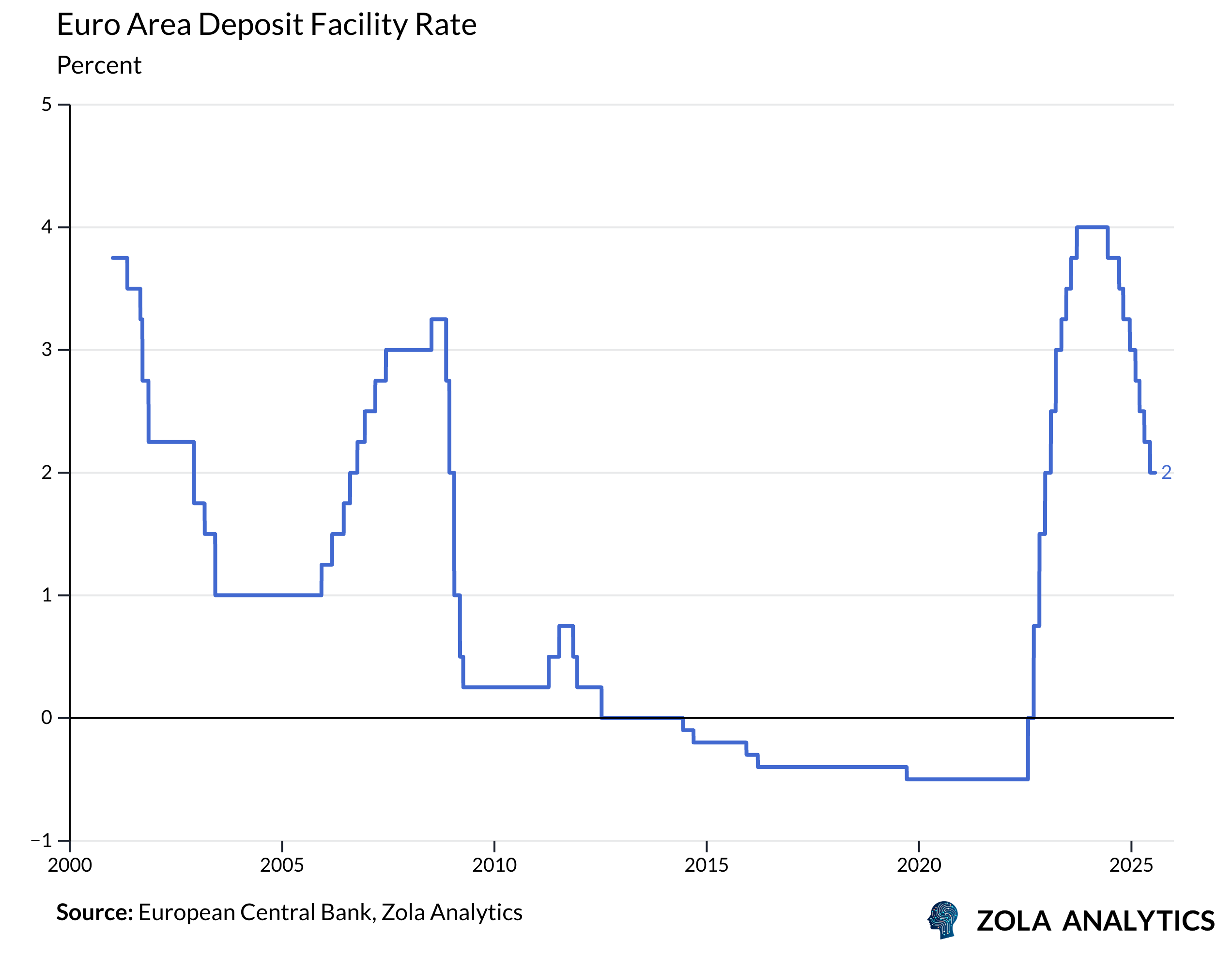

The European Central Bank (ECB) left policy rates unchanged in July, pausing after a cumulative 200 basis points of easing since September 2023. The deposit facility remains at 2.00%, with the main refinancing and marginal lending rates at 2.15% and 2.40%, respectively. The move was widely expected, but the tone of the press conference leaned more hawkish than anticipated, reinforcing the impression that the threshold for further easing has risen.

Why the Pause?

President Christine Lagarde emphasized that the ECB is now “on hold,” adopting language reminiscent of Federal Reserve Chair Jerome Powell’s cautious stance in previous cycles. The central bank’s message was clear: the Governing Council remains data-dependent and meeting-by-meeting, but with policy transmission well underway and inflation near target, there is little urgency to cut further.

The ECB continues to describe the eurozone economy as resilient, supported by strong labor markets and easing financing conditions. Unemployment stands at 6.3%, close to its lowest level since the euro’s introduction. Wage growth is moderating, albeit more slowly than expected, while consumer spending benefits from rising real incomes and robust household balance sheets. Over the medium term, planned fiscal support—particularly Germany’s Q4 stimulus and increased defence spending—should bolster activity.

Inflation and Risks

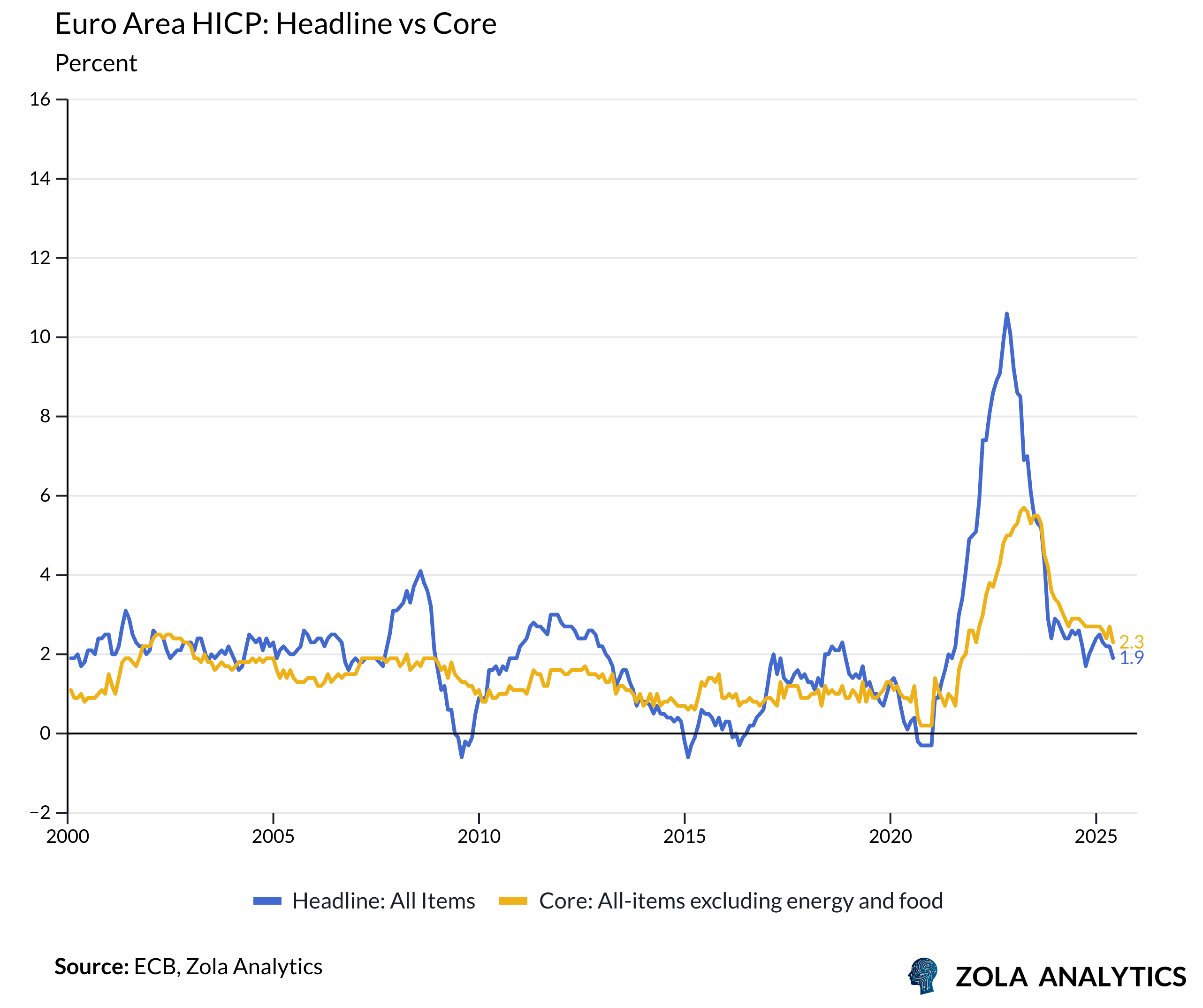

Inflation remains at 2%, with the outlook described as “more uncertain than usual.” Lagarde downplayed concerns about euro appreciation, noting the ECB has no exchange rate target but monitors FX as part of policy transmission. Similarly, a modest undershoot of near-term inflation projections is not considered problematic, as the Governing Council prioritizes the medium-term outlook.

Downside risks remain, however:

Global trade tensions and prospective US tariffs (with negotiations reaching a key deadline on 1 August).

Geopolitical uncertainty, weighing on business investment.

Potential for weaker summer data, particularly on inflation and growth.

September Cut: Still Possible, but Odds Have Shifted

Markets initially priced a strong probability of another 25bp cut in September. Post-meeting, those odds fell from 90% to 74%, with some expectations shifting toward December. The consensus view is that a September cut remains plausible—particularly if incoming data undershoots expectations and US-EU trade talks fail—but the conviction is weakening. Previous ECB projections suggested a terminal rate of 1.75%, which implies some remaining room for maneuver if conditions deteriorate.

By contrast, if tariffs are avoided and fiscal tailwinds strengthen activity into year-end, the ECB could pivot toward a prolonged hold and even revive discussions of policy normalization in 2026. A robust rebound in Germany and stabilization in labor markets could also reintroduce inflationary pressures in late 2025.

Medium-Term Outlook

While the ECB remains squarely focused on downside risks today, policy asymmetry is fading. The era of rapid cuts is over; the next phase is one of optionality. If inflation proves stickier or growth accelerates, markets may begin to price in a hawkish tilt by mid-2026—a notable shift from the dominant easing narrative of recent quarters.

For now, the ECB sits in what Lagarde called a “good place.” Whether that comfort zone survives the summer will depend on the data—and perhaps on geopolitics as much as economics.

Disclaimer: Zola Analytics provides this material for informational and entertainment purposes only. It does not constitute investment advice.