Published 14th November 2025

10 minute read

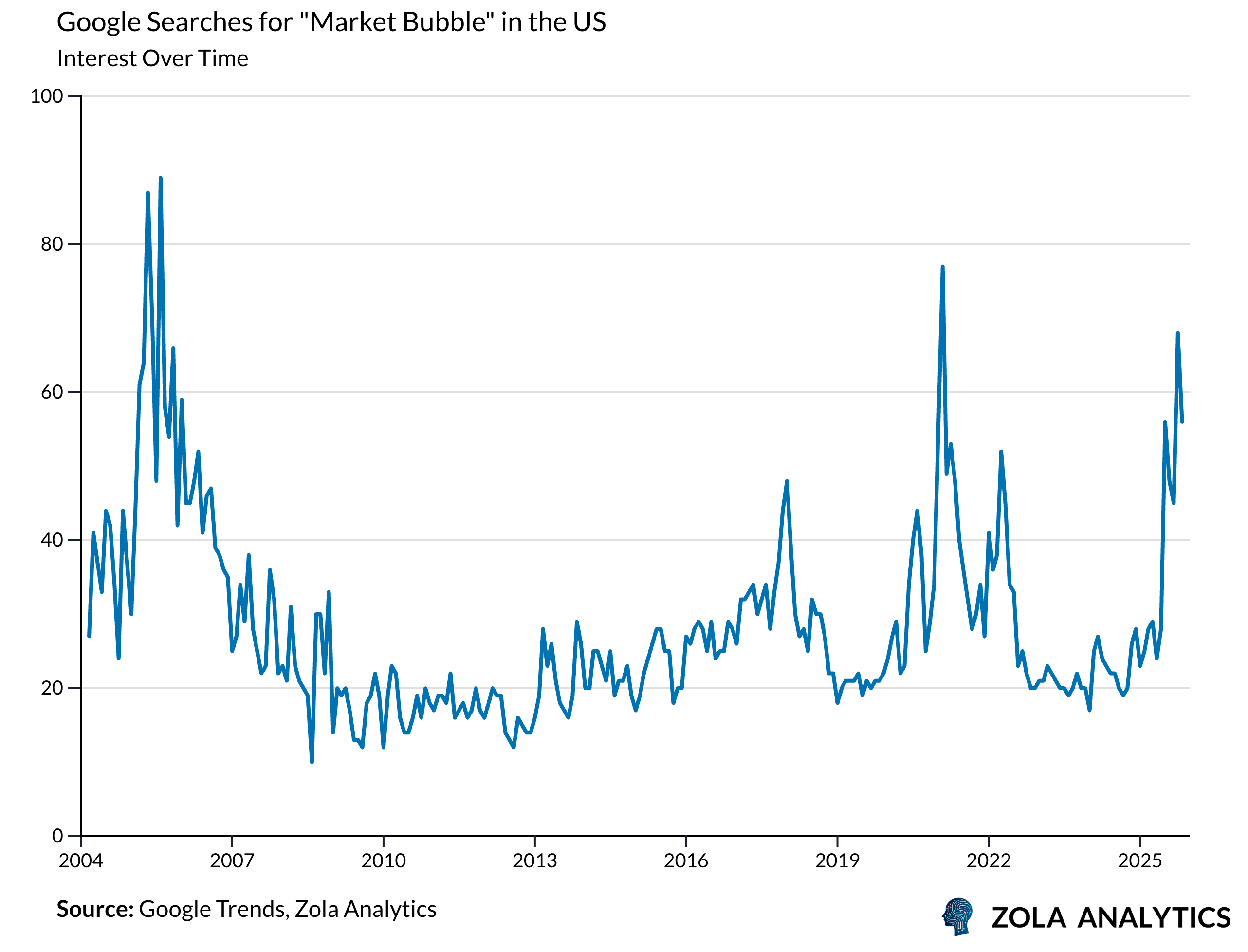

Bubble Diagnostics

Every generation believes it can spot a bubble before it bursts. Today, many warn that AI is the next big bubble, pointing to skyrocketing valuations and frenzied investment in data centers, chips, and cloud infrastructure. While others dismiss the idea entirely, arguing that AI’s transformative potential justifies the hype. So who’s right?

The answer will only be clear in hindsight. But we don’t have to wait to ask whether AI is a bubble. This week’s Zola Chartbook examines historical patterns, valuations, and market behaviour, so we can assess the risks and decide whether today’s enthusiasm is justified or dangerously overblown.

What is a bubble?

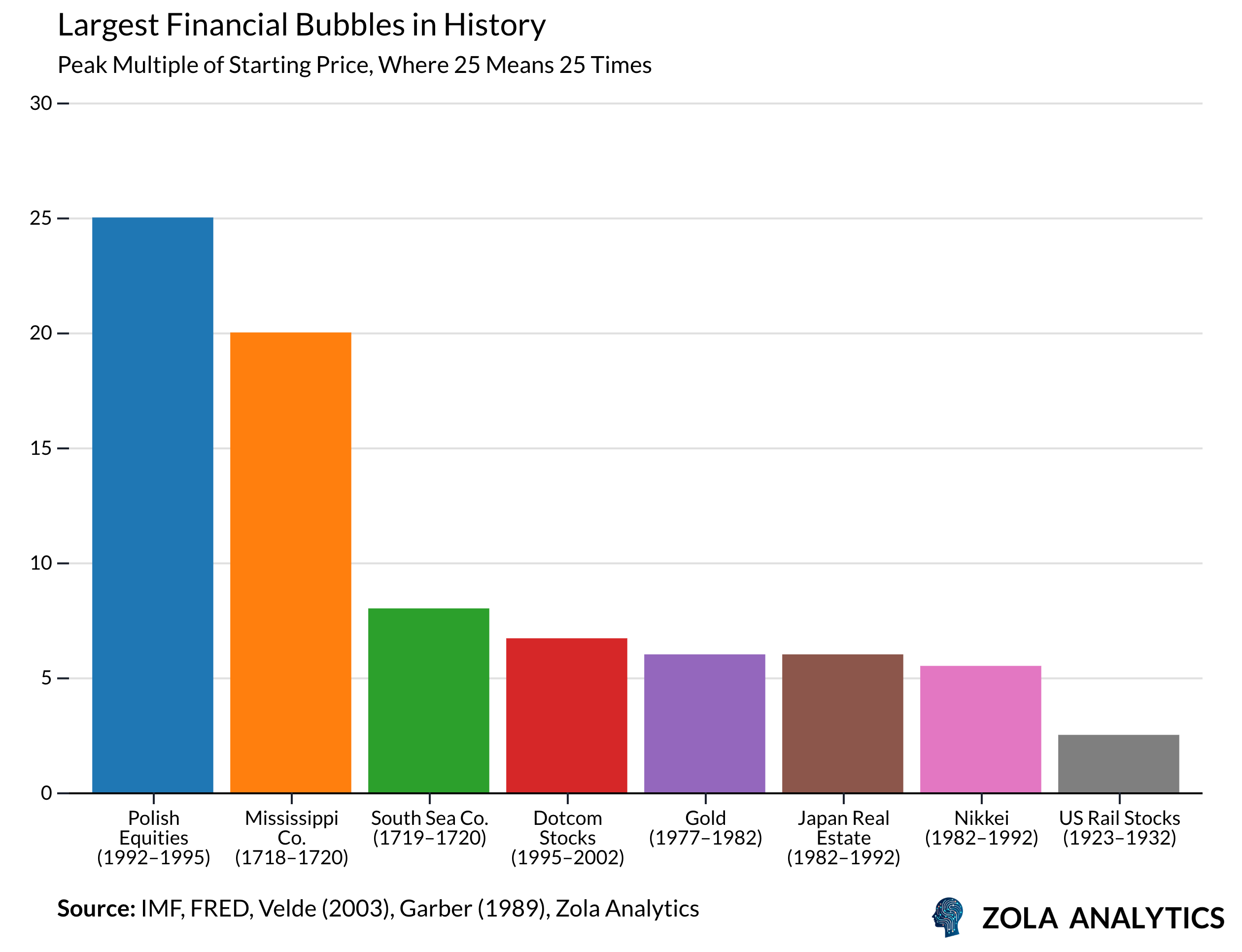

A bubble develops when prices of assets become divorced from their value, in a self-reinforcing cycle of speculation and momentum. It starts with something real: an innovation, a technological leap, or a paradigm shift that promises to change the world and always ends with claims that “this time is different”. The South Sea Company dazzled investors with visions of New World riches in 1720. The railways of the 19th century offered the prospect of revolutionizing transport and commerce. The internet, in the late 1990s promised to reform the global economy. Each of these began as a legitimate breakthrough that held the potential to transform the world.

As prices rise, speculation takes over. Early gains breed confidence, and confidence fuels momentum. Prices diverge from traditional metrics of value. Warnings are dismissed as outdated thinking and the narrative becomes self-sustaining. In the early stages, this optimism is rational. But justified confidence hardens into mania.

AI is no different. It is undoubtedly a transformative technology, and we are only beginning to see its impact from the automation of routine tasks to the acceleration of drug discovery. Yet it too is showing signs of speculative excess. Some signals are flashing red, while others suggest this story is only just beginning.

Priced For Perfection?

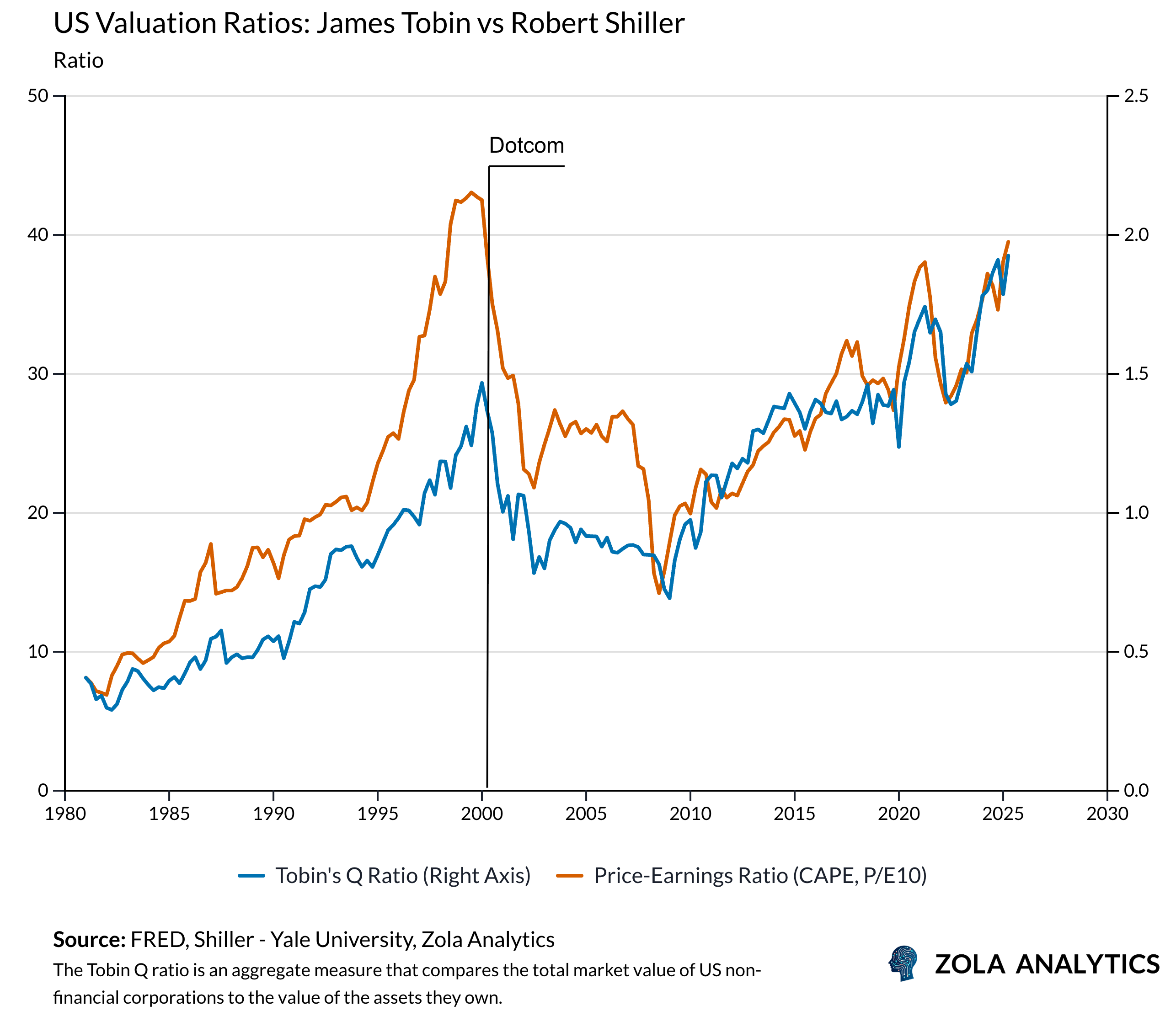

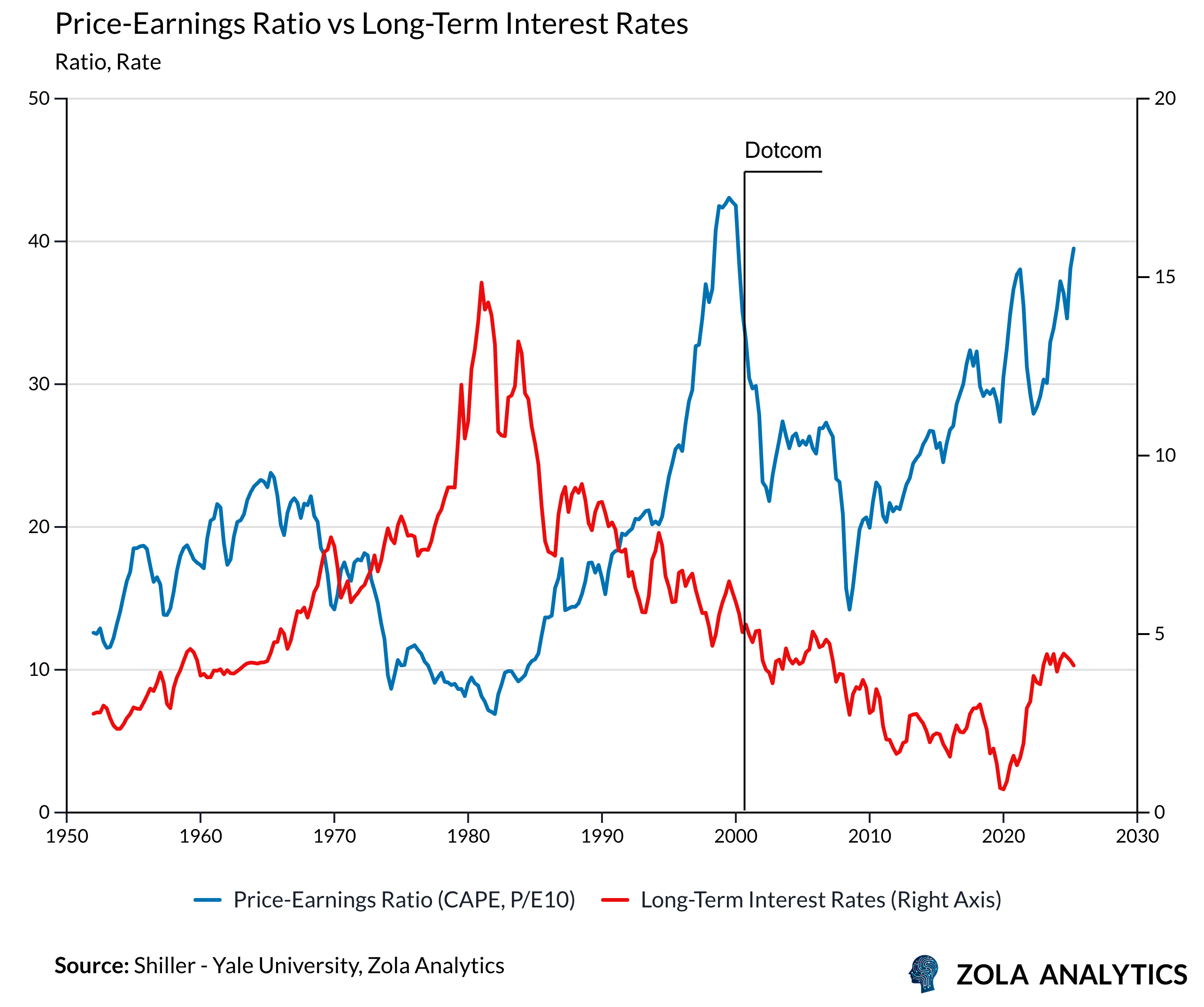

If bubbles represent deviations from fair value, analyzing them requires first establishing how to measure value. When we assess useful measures of valuation, we can see how far expectations have stretched. US equities now trade near the upper end of their historical range. The cyclically adjusted price–earnings ratio has returned to levels last seen during the late 1990s, while Tobin’s Q ratio shows market values well above long run norms. These metrics aren’t yet at the extremes of past bubbles, but they’re close enough to raise eyebrows.

In the context of the broader macro environment, this is even more puzzling. Since 2021, interest rates have climbed sharply, a shift that in theory, should deflate valuations by making future earnings less valuable today. So why hasn’t the market cracked? The answer isn’t straightforward, but a few theories stand out.

High valuations could reflect an extremely positive outlook for corporate profits. We could be witnessing a structural increase in people’s risk appetite. Others would explain that the market sees higher rates as temporary, with traders positioning themselves for rate cuts that could extend the rally. A final explanation would be bubble dynamics, where momentum, narrative, and irrational optimism override the cold maths of valuations.

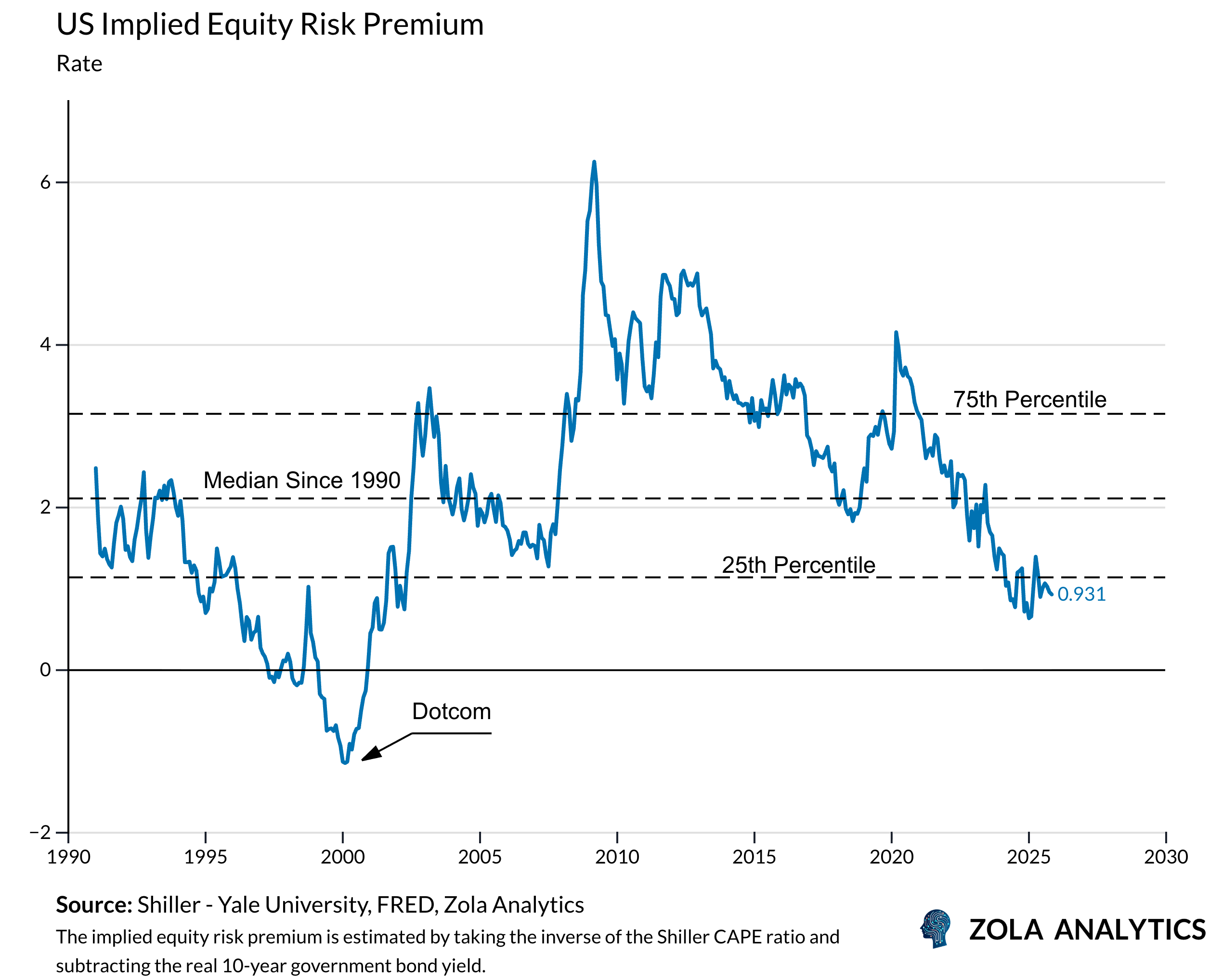

Whatever the explanation, it is clear that the market is pricing-in extreme levels of optimism. The equity risk premium, which is the extra return investors demand for holding stocks instead of safe assets, continues to fall to historically low levels.

Investment Justified?

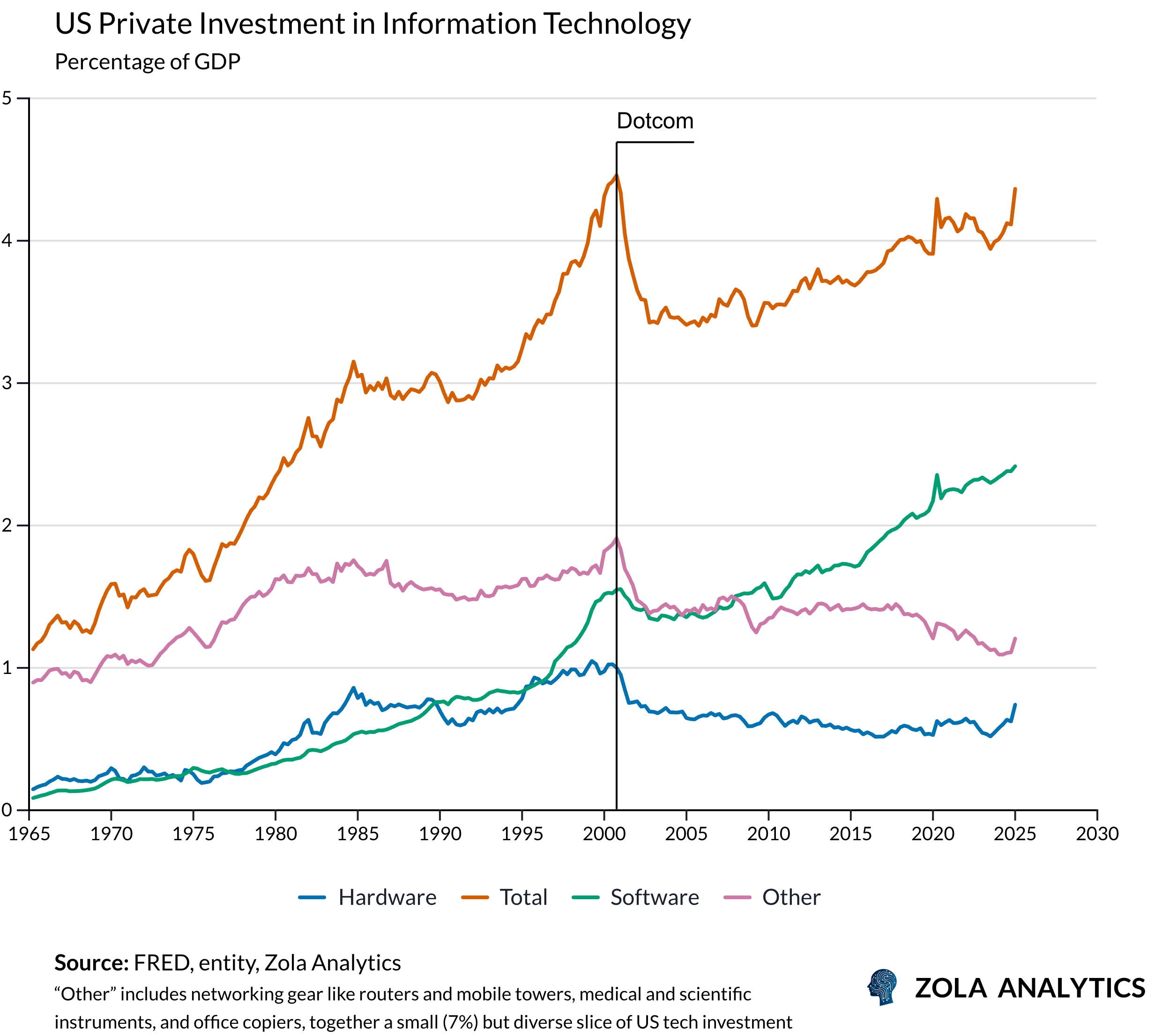

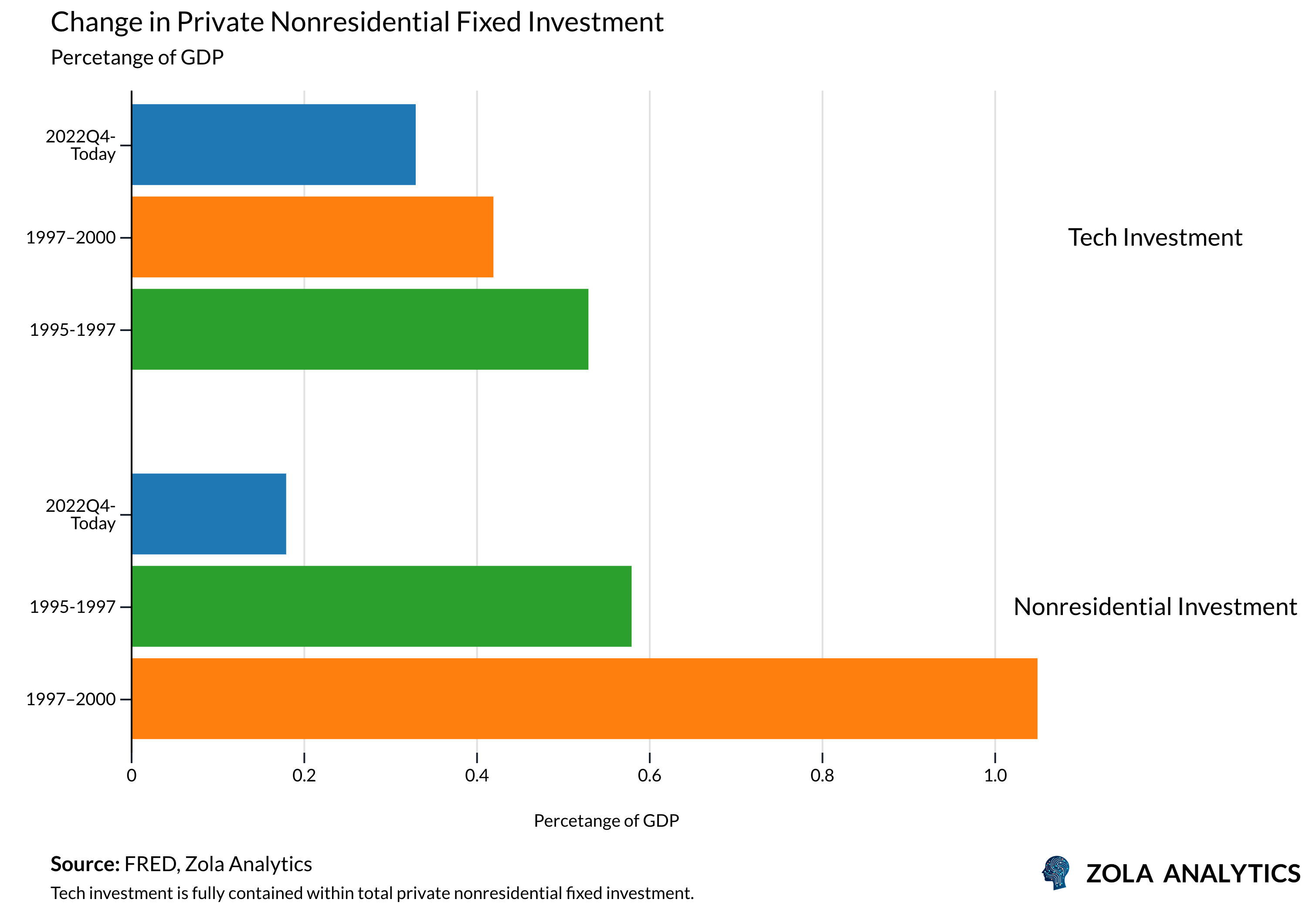

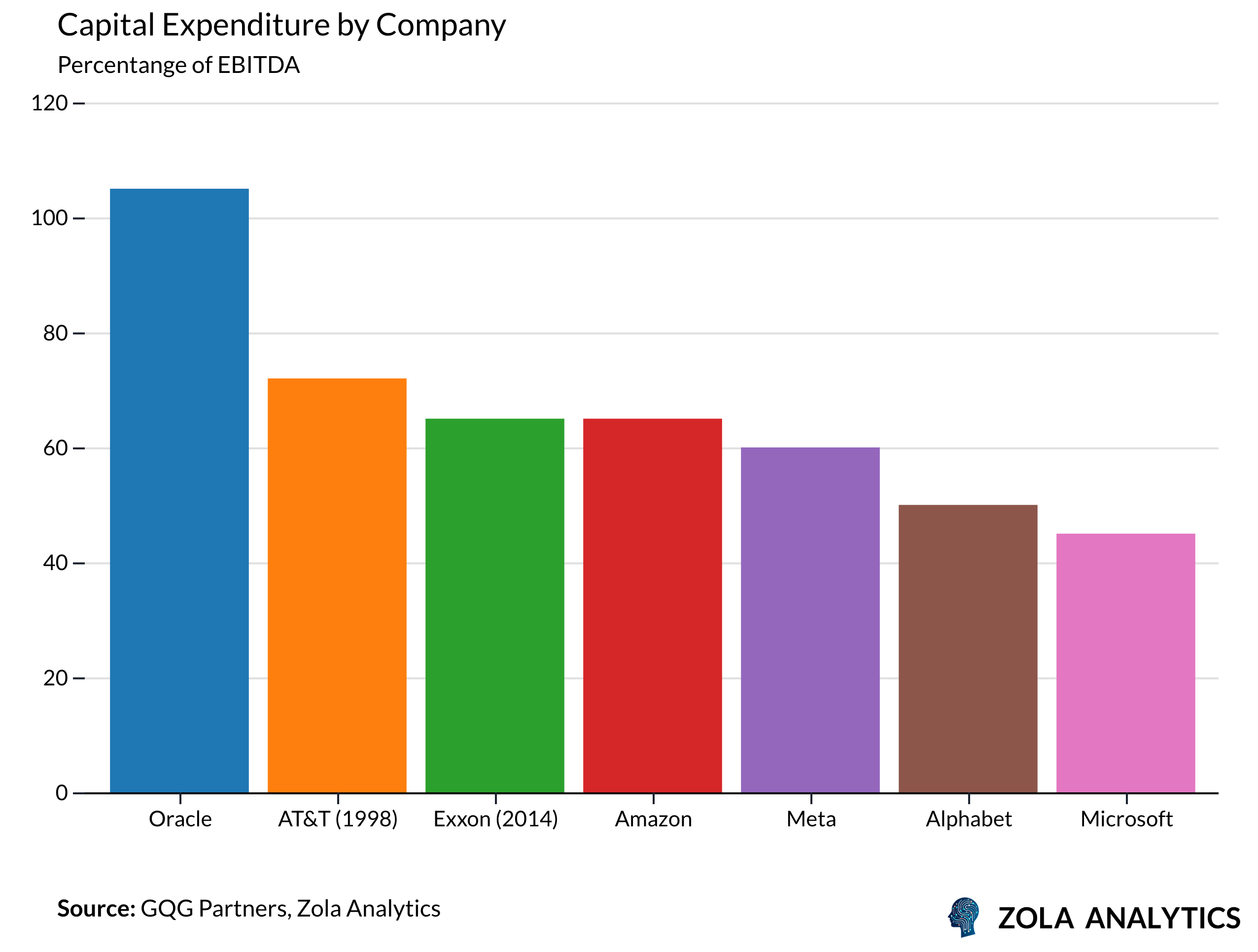

Current AI developments echo earlier episodes of technologically driven investment. Large firms are deploying significant capital into data centres, specialised semiconductors, and cloud infrastructure, albeit this spending still remains below the telecom buildout that defined the late 1990s.

In the late 1990s, investment was broad-based, spanning manufacturing, services and logistics. Today’s boom however, is more concentrated with most of the expansion focused on data infrastructure and semiconductor capacity.

Broad investment cycles tend to generate reinforcement spillovers, making them more resilient to shifts in expected returns. But when investment is concentrated, it becomes less likely that all of these competing investments can generate the required returns that justify their valuation. What would it take for all this spending to actually deliver returns?

AI infrastructure depreciates rapidly. High-end GPUs and data centers can become obsolete in as little as three years, requiring constant reinvestment just to stay competitive. Meanwhile, the commoditisation of AI could erode profitability over time. There’s even a risk that Jevons Paradox will hold, where increased efficiency leads to more demand rather than cost savings, forcing firms to spend even more just to keep up.

A recent MIT study suggests that 95% of organisations deploying generative AI are seeing little to no return on investment. When so much capital is chasing uncertain returns, the risk isn’t just that the boom fizzles, it’s that it leaves behind a graveyard of stranded assets.

While we are not yet in a classic late-stage mania, the signs are concerning. Narrow investment and rapidly depreciating assets indicate that there is a gap between hype and reality. While AI could well become as transformative as electricity, the question isn’t just whether it will work, it’s whether the returns will justify the cost. Right now, the evidence suggests we’re in the midst of gargantuan capital misallocation, where the winners will be few and the path to profitability unlikely for most firms involved.

Late Cycle Behaviour

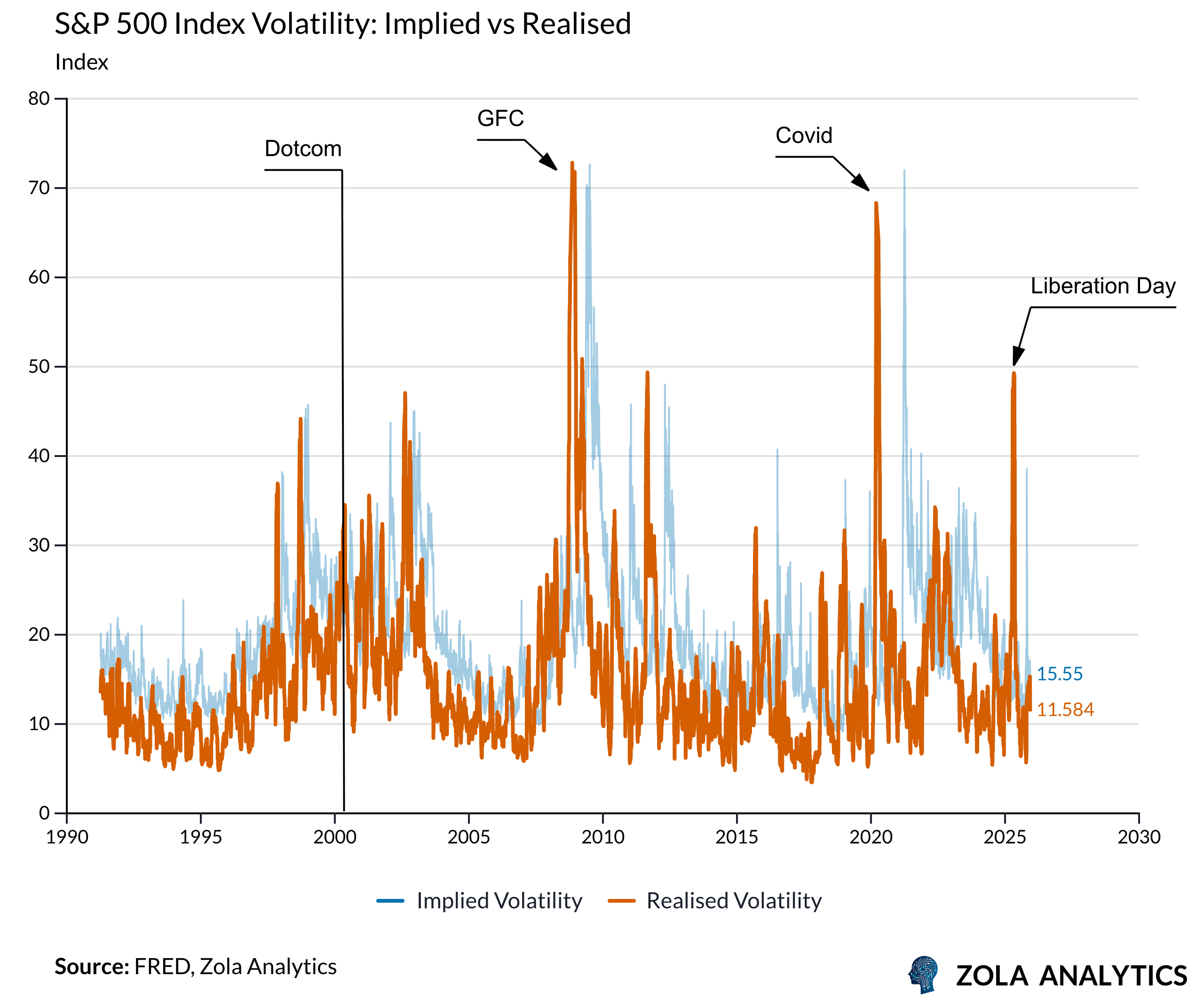

When bubbles begin to pop, volatility starts to rise. Recent behaviour has not followed this template. Despite stretched valuations and pockets of speculative activity, realized volatility has remained low. This could reflect benign conditions, but could also indicate investor complacency. When the market turns, the shock to expectations and the assumptions that underpin both earnings forecasts and collateral structures, will lead to sharp and protracted drawdowns.

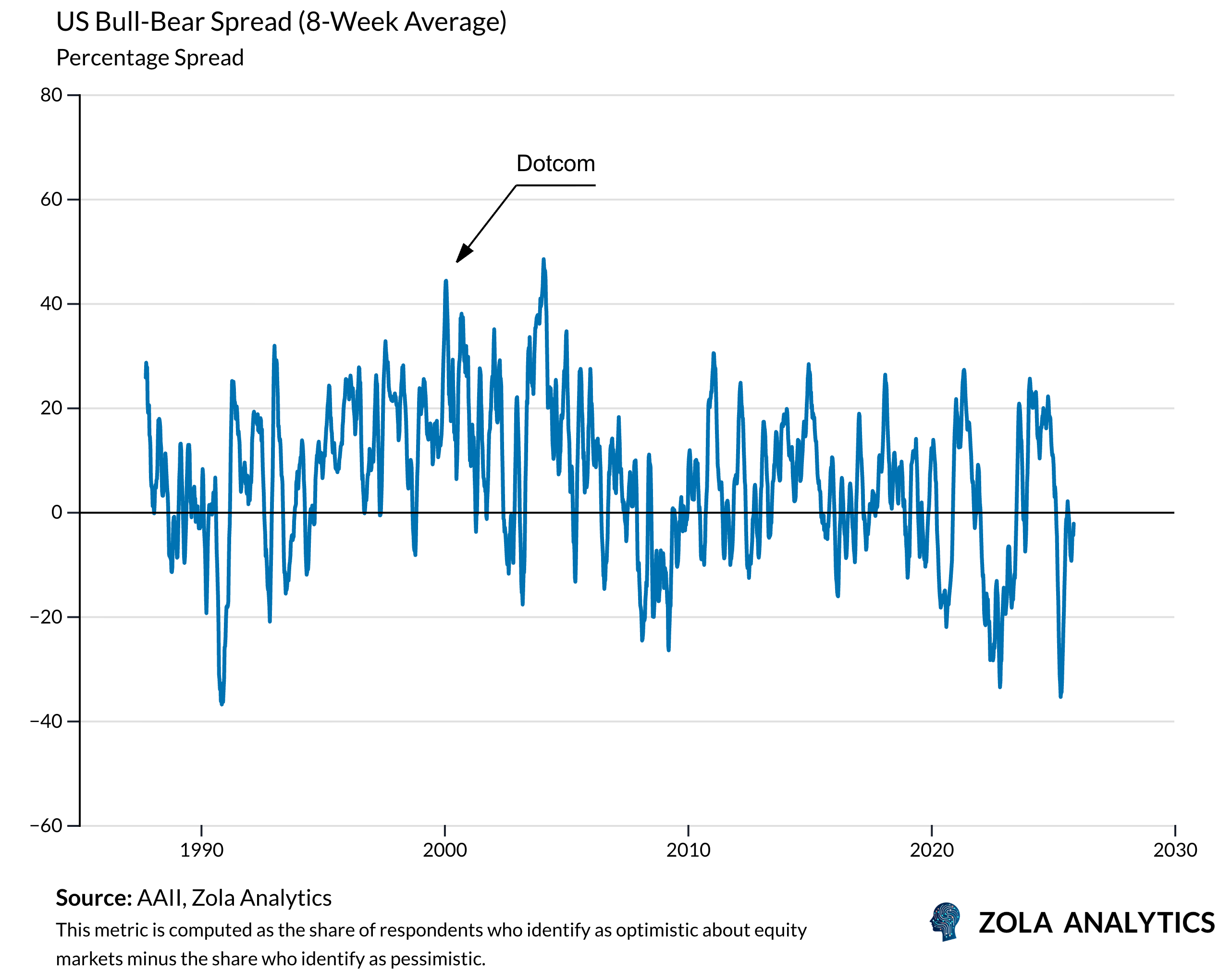

On the other hand, retail investor sentiment as captured by surveys like the AAII bull-bear spread, remains balanced rather than euphoric. While optimism has risen at times, lingering concerns over inflation, fiscal pressures, and interest rates have prevented the one-sided exuberance typical of late-cycle extremes.

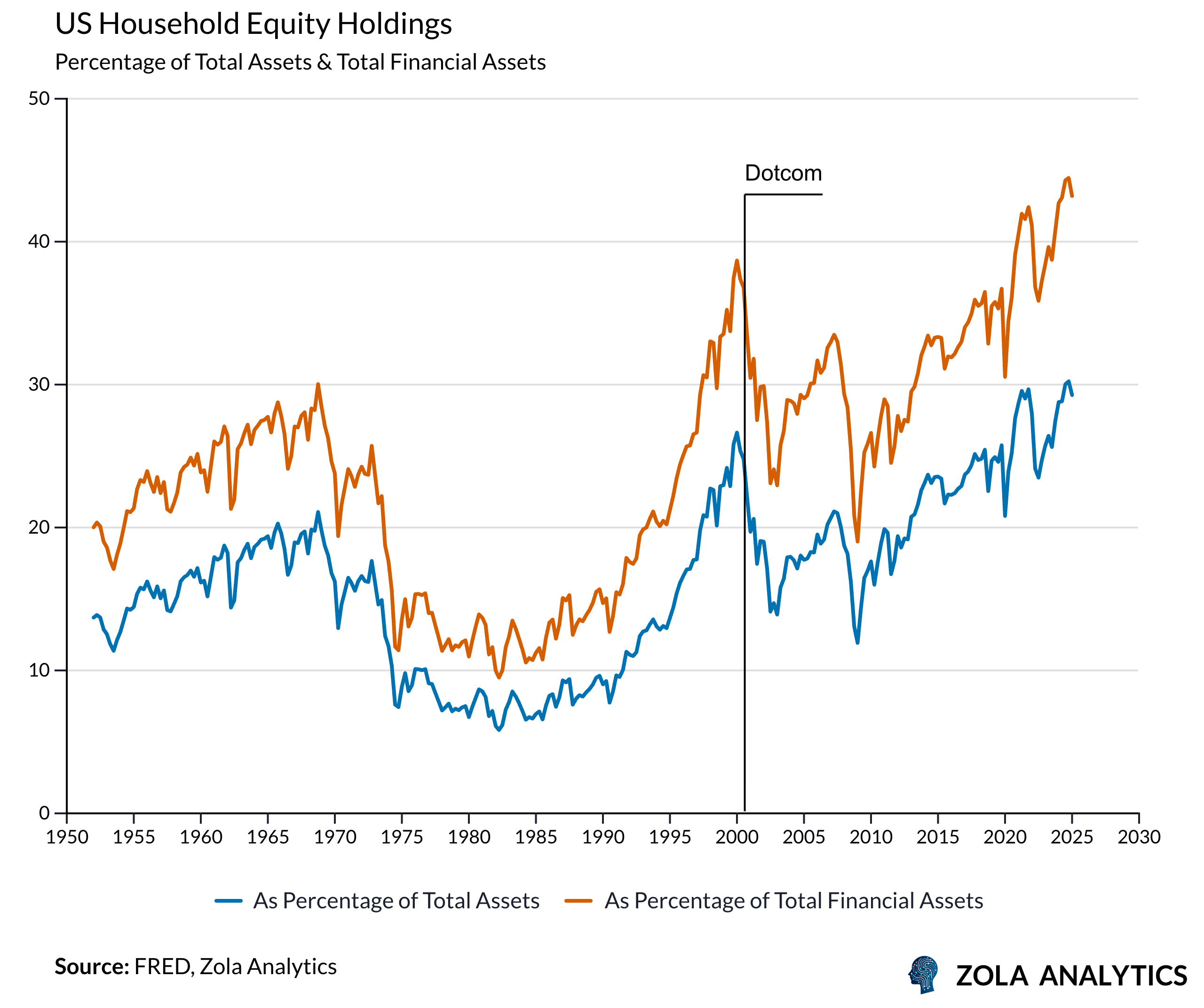

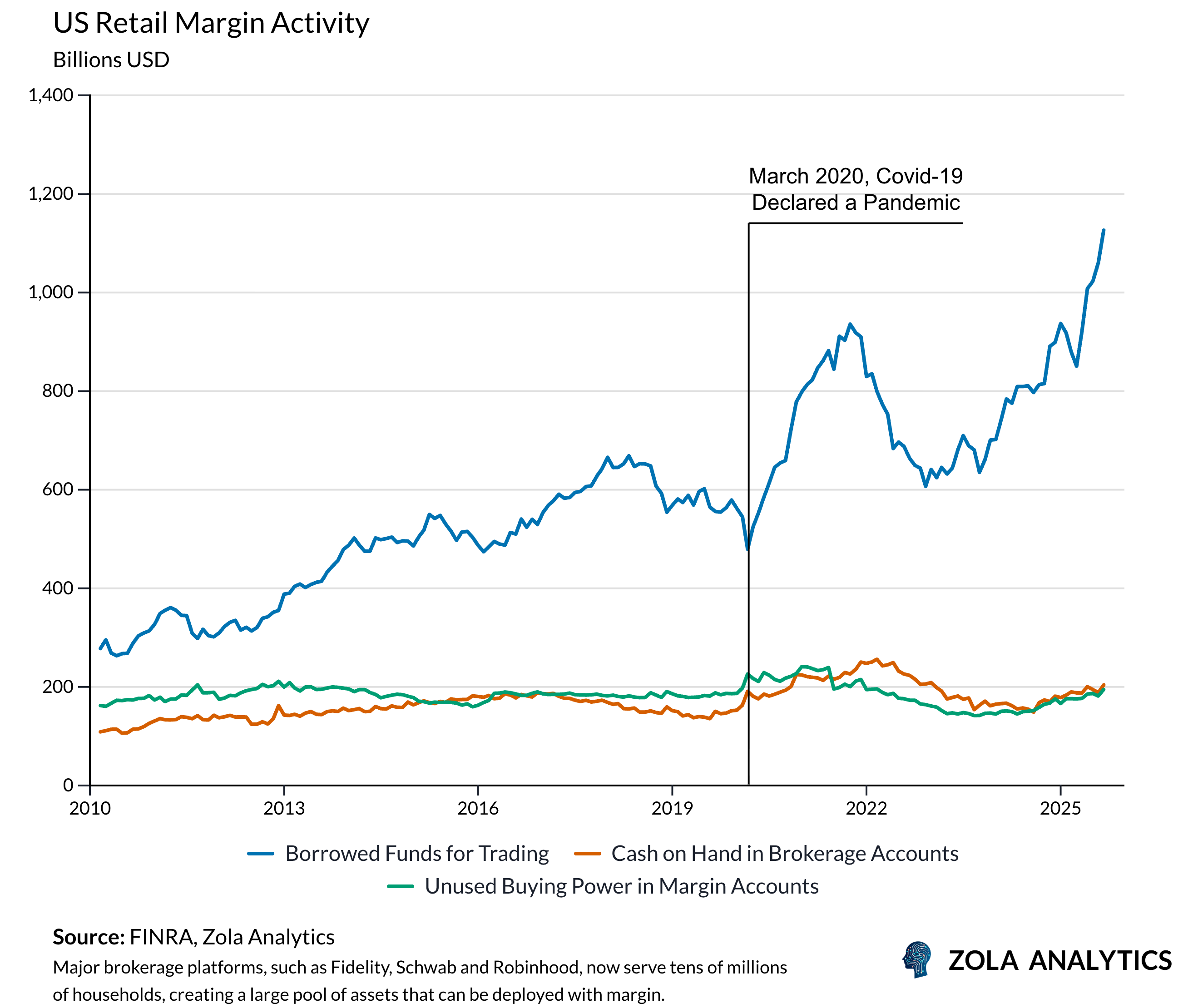

However, this masks a growing fragility. Household equity exposure has climbed toward historical highs, partly due to strong market returns since the pandemic.

Even more concerning is the surge in margin debt which has reached record levels. Many investors, particularly those who entered the market during the post-pandemic rally, have never experienced a severe correction. When a drawdown arrives, thin cash buffers and high leverage could force rapid deleveraging, amplifying the selloff.

Devil’s Advocate

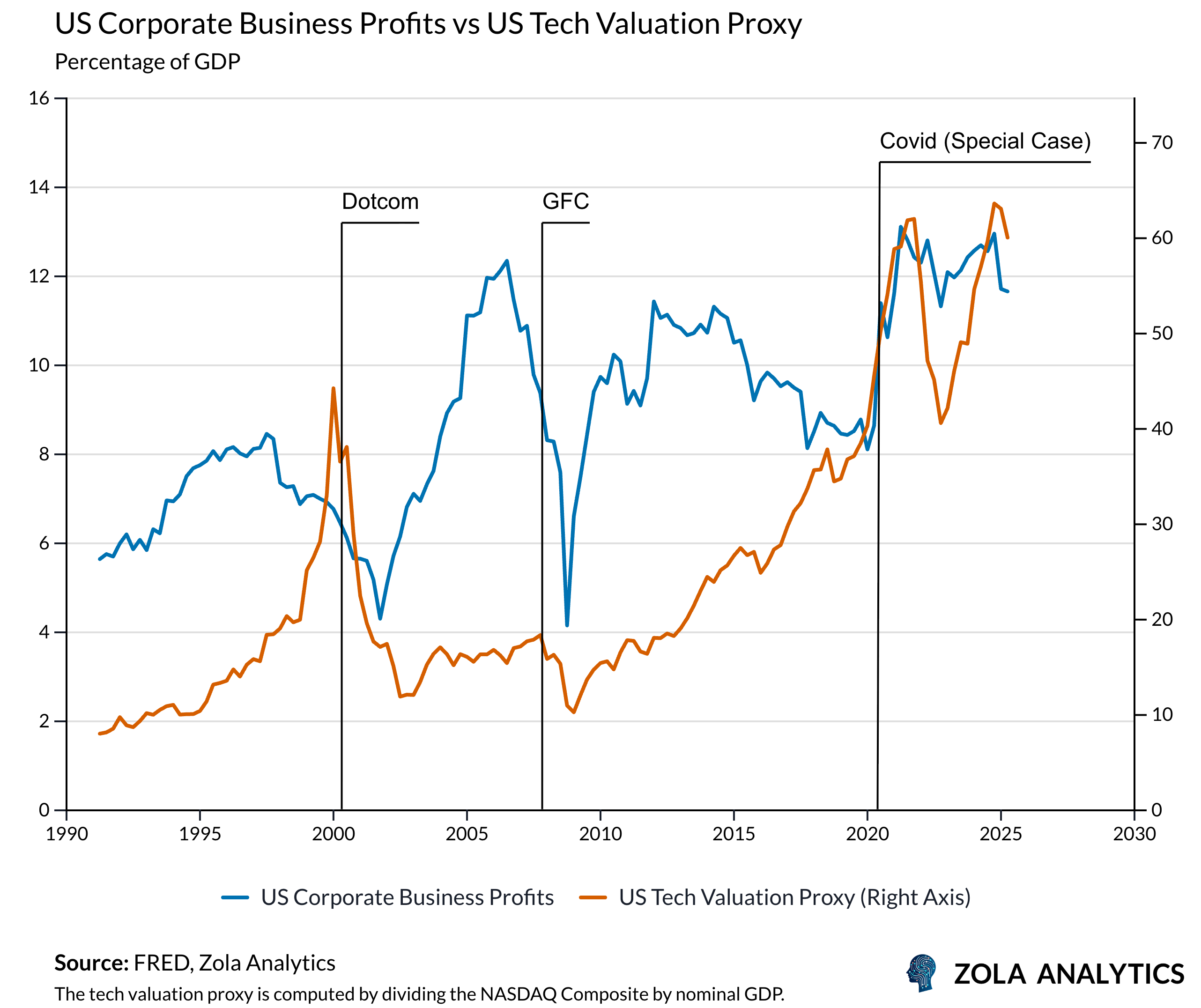

This exuberance showing up in asset prices did not materialise out of thin air. When we observe corporate earnings, they are high relative to the size of the economy, offering a critical layer of support.

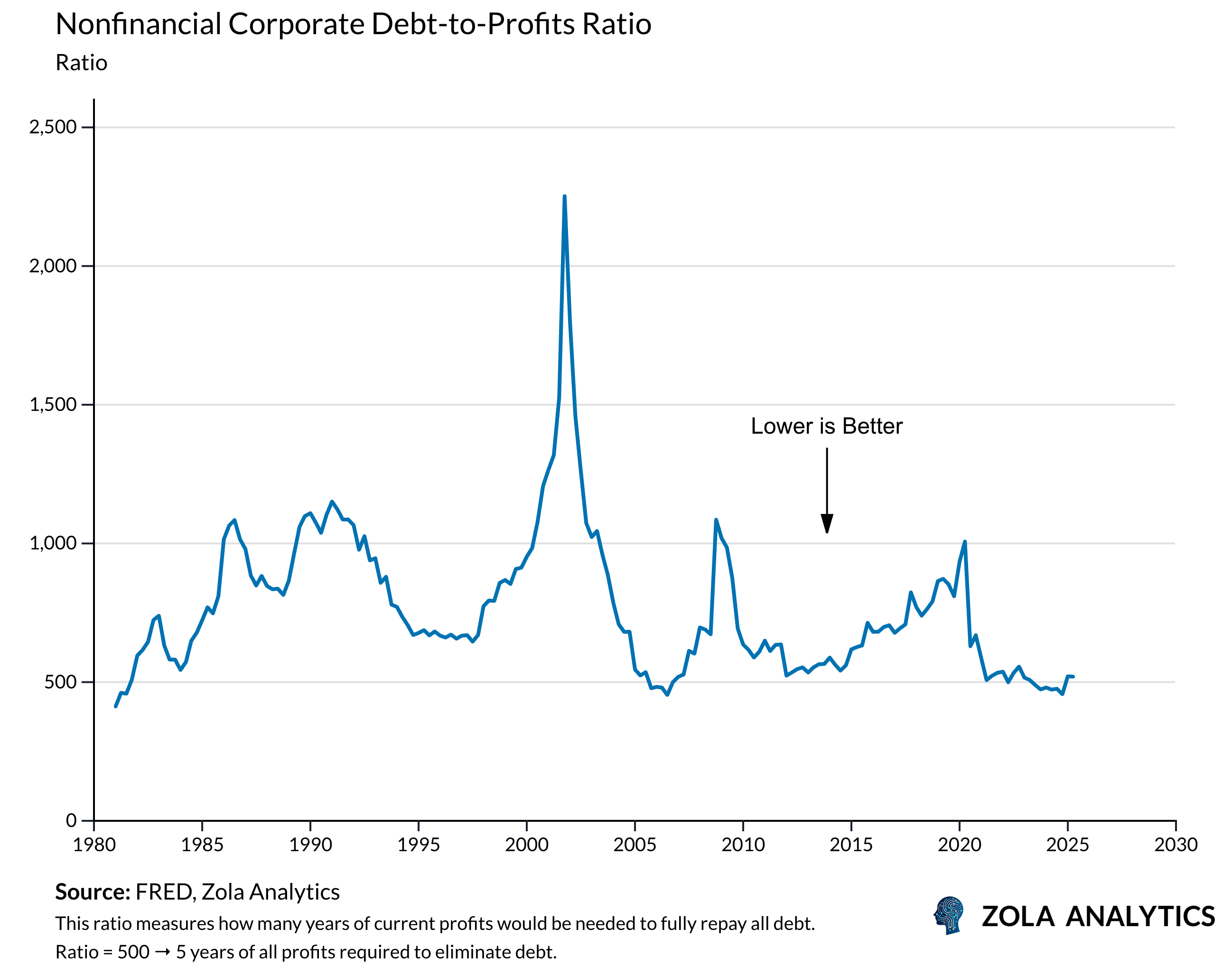

Balance sheets tell a similar story. Debt levels, relative to profits, are modest by historical standards, and companies’ ability to service that debt is strong. This isn’t the financial fragility that characterized past bubbles, where excessive leverage led to collapse. Instead, corporate finances are resilient. Cash reserves are plentiful, default rates are low, and firms have the flexibility to weather potential shocks.

Disguised Stresses

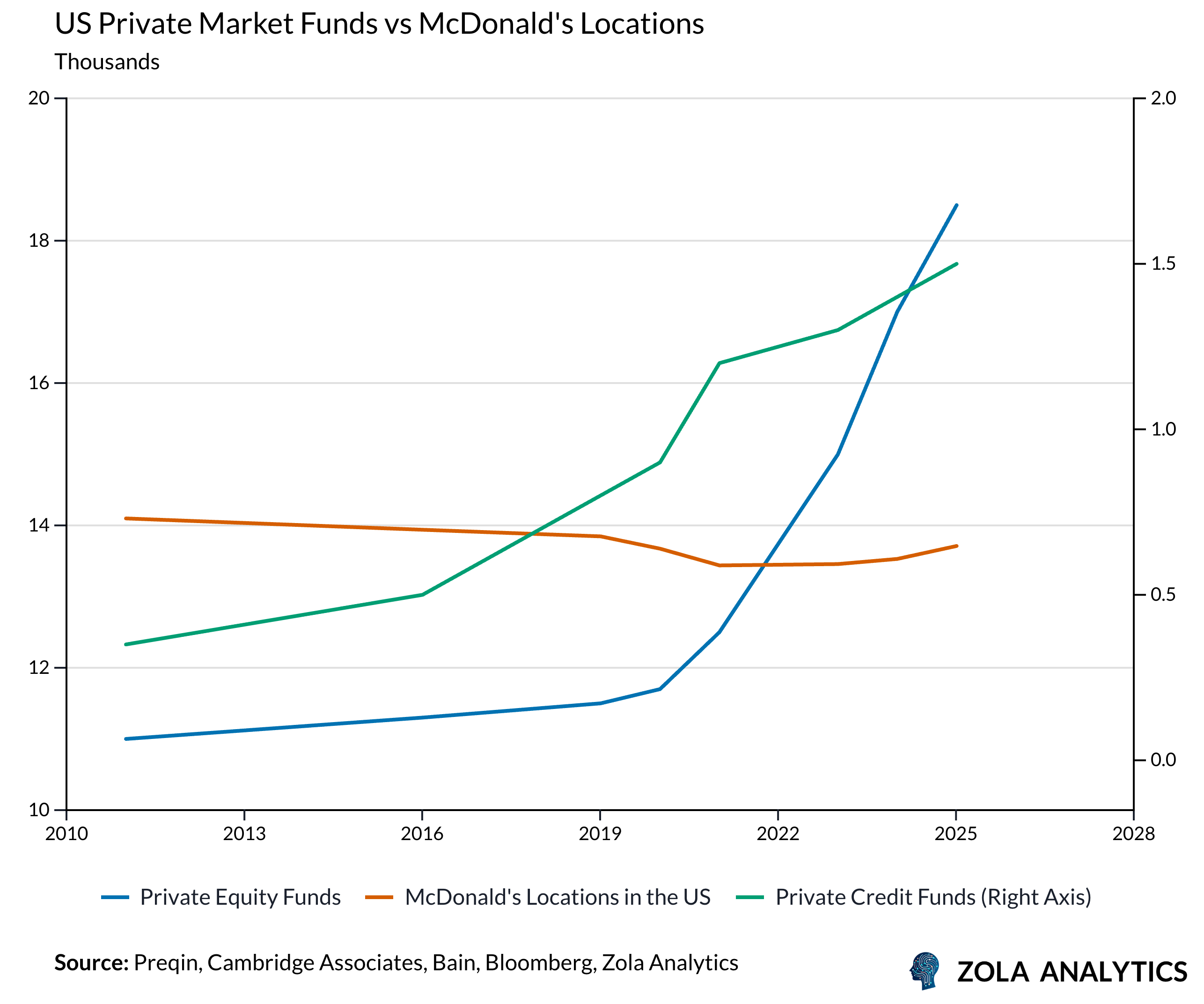

Nonetheless, under the surface there are some more worrying signs, indicative of exuberance. Private markets have expanded rapidly, with increasingly complex investment products reaching a wider retail audience. The growth of private credit is particularly important, given its close ties to the financing needs of the technology sector. These linkages create a channel through which funding shocks can propagate more quickly.

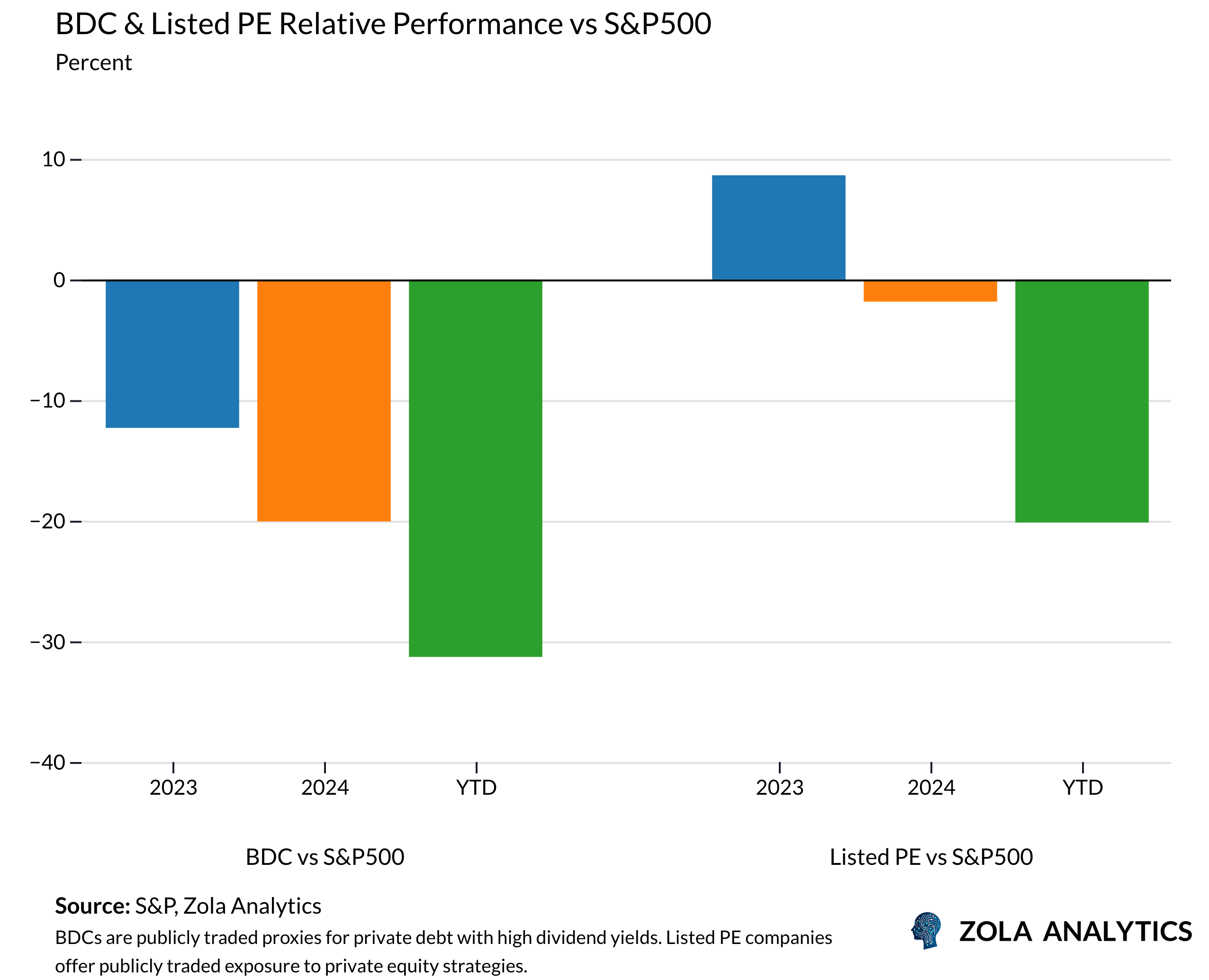

Publicly traded vehicles linked to private strategies offer an early read on these pressures. Business development companies and listed private equity firms have underperformed major equity indices, especially this year, signalling greater sensitivity to higher funding costs and tightening liquidity. Their exposure to leveraged borrowers, valuation marks, and refinancing cycles makes them more responsive to shifts in the investment environment than broad equity benchmarks. As private markets become more entwined with the AI investment cycle, their capacity to transmit shocks across the financial system increases.

Gravity Against Narrative

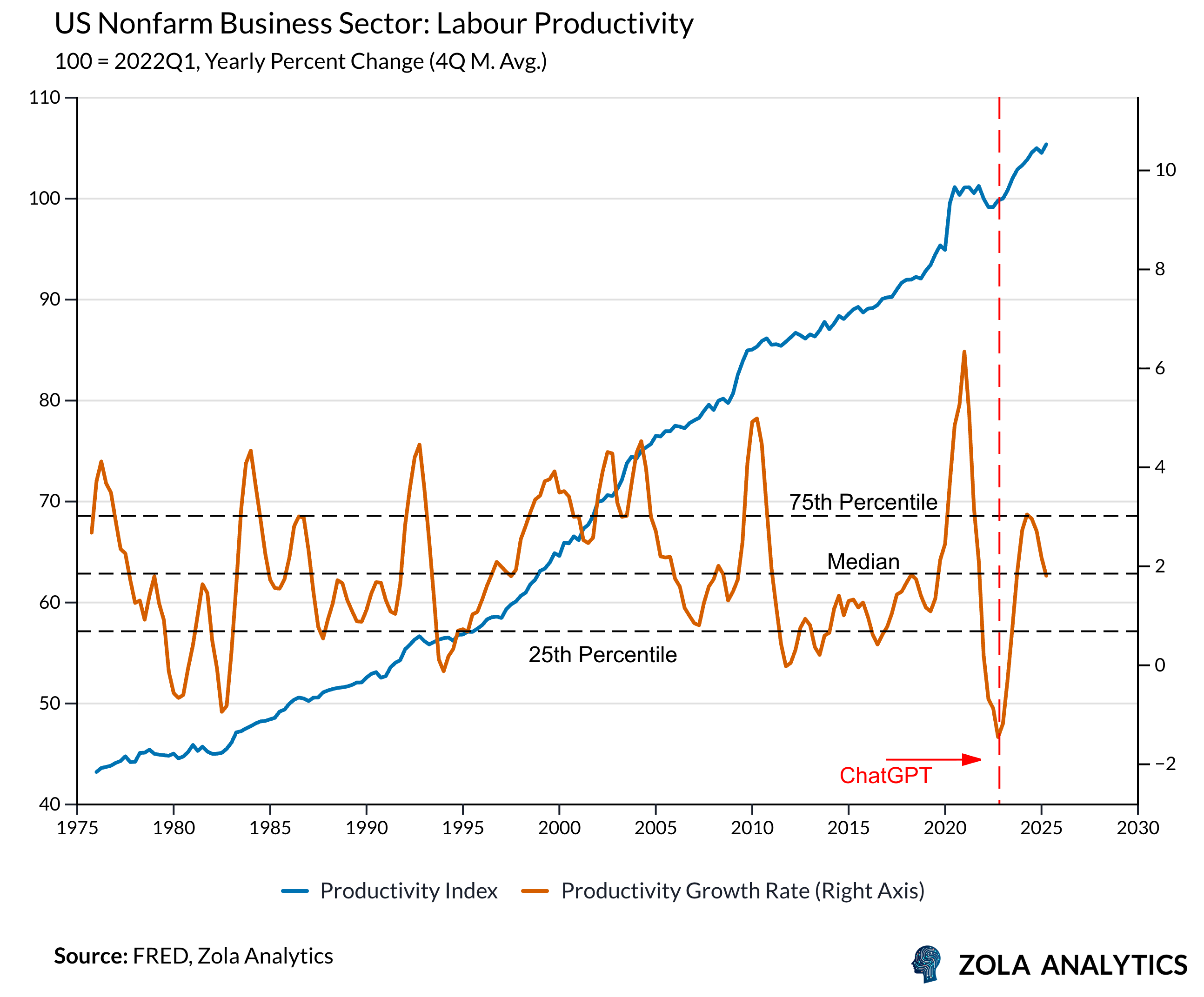

“By 2005 or so, it will become clear that the Internet’s impact on the economy has been no greater than the fax machine’s” — Paul Krugman (1998). In retrospect the remark is laughable, yet the context matters. At the time, productivity data showed little evidence of an internet driven acceleration, commercial applications were still limited, and scepticism rested on a reasonable reading of the facts available.

The same tension appears in today’s discussion of artificial intelligence. The technology carries clear potential to reshape industries, raise efficiency, and support economic growth over the long run. Productivity has improved during the initial phase of adoption, yet the gains sit comfortably within previous cycles and do not point to a structural break. The evidence suggests reinforcement of trend growth rather than the step change implied by the most optimistic valuations.

While the risk of an abrupt reversal is always present, a collapse tomorrow looks unlikely. Earnings remain resilient and the cycle still carries momentum. The real question is how much of the current investment wave will prove economical once outcomes are clearer. That will take time to assess and is more a story for 2026 than for today.

Sign up to receive the Zola Global Macro Chartbook every week: https://www.zolaanalytics.com/insights?signUp