Published July 31st 2025

3-min read

Fed Pushes Back: Holding Steady While Watching Labour

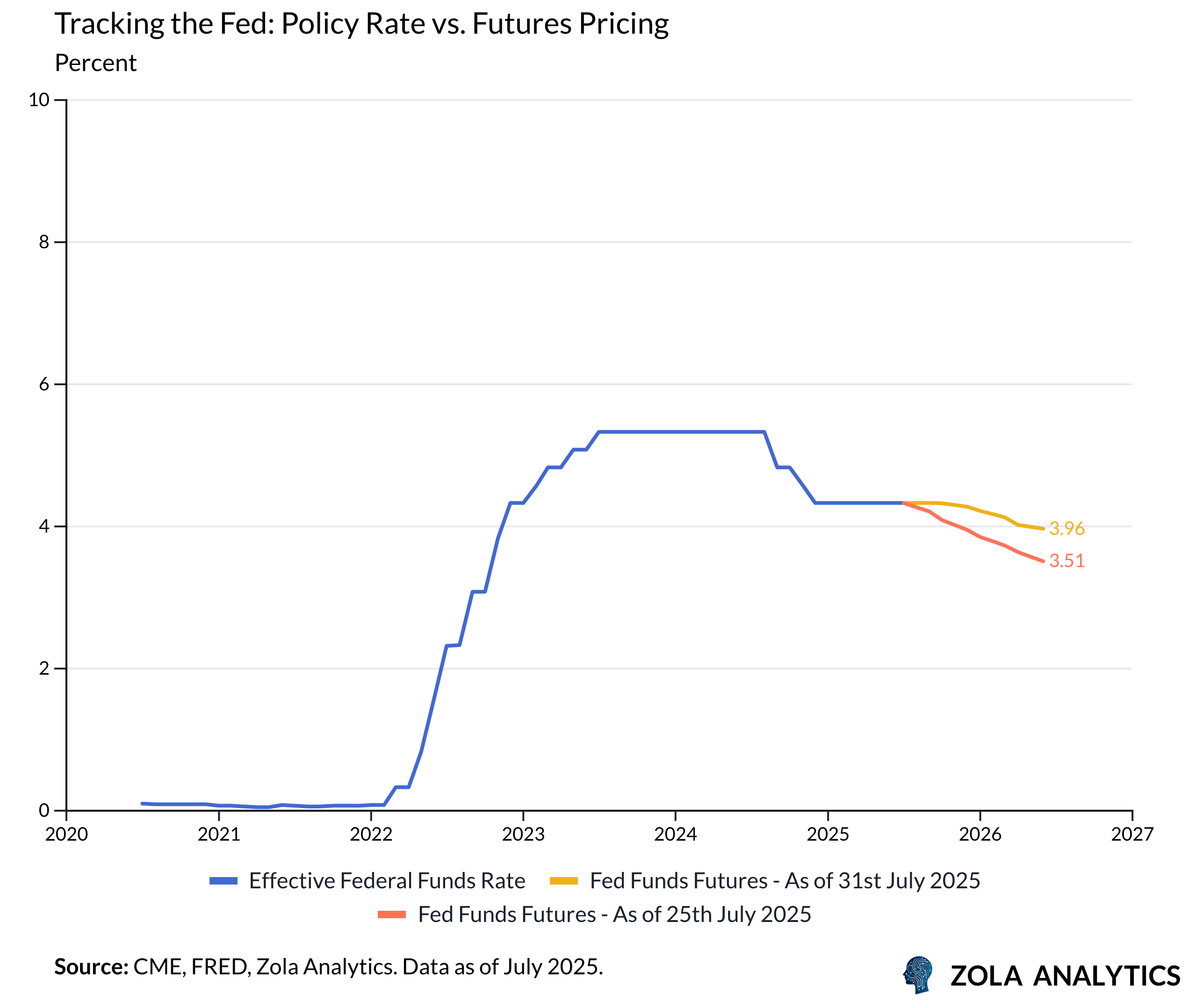

The Federal Reserve maintained the fed funds rate at 4.25–4.50% for a fifth consecutive meeting in July, signalling a continued wait-and-see posture amid lingering inflation concerns and early signs of labor market softening. Despite dissent from Governors Bowman and Waller in favour of immediate cuts, the majority of the Committee remains cautious, leaning on data dependence and inflation vigilance to justify the current stance.

Powell Pushes Back on Dovish Hopes

Chair Powell’s press conference leaned hawkish despite acknowledging two-way risks. He emphasised that policy remains “modestly restrictive,” noting that inflation is still above target—even excluding tariff effects—and that goods inflation could be underestimated. While Powell did not rule out rate cuts later this year, his tone raised the bar for near-term easing, dampening market hopes for a September cut.

Markets adjusted accordingly: front-end yields rose, implied cuts for 2025 fell below 40bps, and pricing for a September move slipped toward a coin flip. Several analysts noted that this was the most hawkish market reaction to an FOMC meeting in 2025.

Labor Market: The Swing Variable

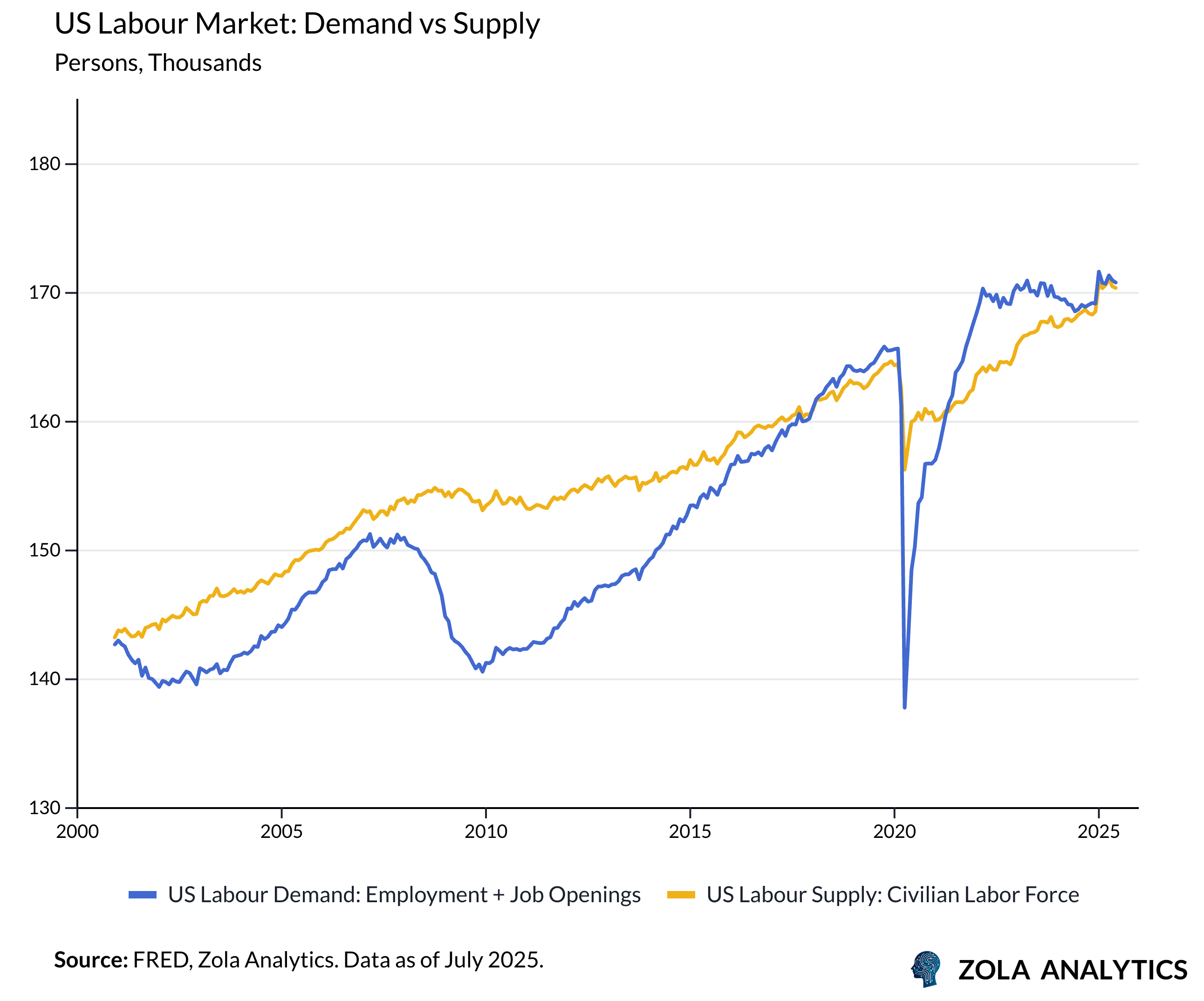

A consistent theme across reports is that the path to rate cuts hinges on the labor market. The unemployment rate remains low, and Powell described conditions as “in balance”—a reflection of slowing demand offset by declining labor supply, partly due to immigration shifts.

Hiring is slowing, and demand for workers is weakening, but the effects on the unemployment rate have been muted. That’s because labor supply appears to be falling in tandem with demand, likely due to slower immigration growth. This dynamic complicates the Fed’s assessment, as reduced participation may mask underlying softness in job creation.

To justify a more aggressive easing path, there will need to be clearer signs of slack. The unemployment rate will likely need to trend toward 4.5% in the near term to meet this threshold, as modest NFP deceleration alone may not be enough if offset by falling supply.

Waller and Bowman dissented explicitly on labor concerns, arguing the soft underbelly of employment data is being overlooked. Most analysts agree that a marked deterioration in the labor market remains the clearest path to unlock earlier cuts, as inflation alone is unlikely to prompt near-term action.

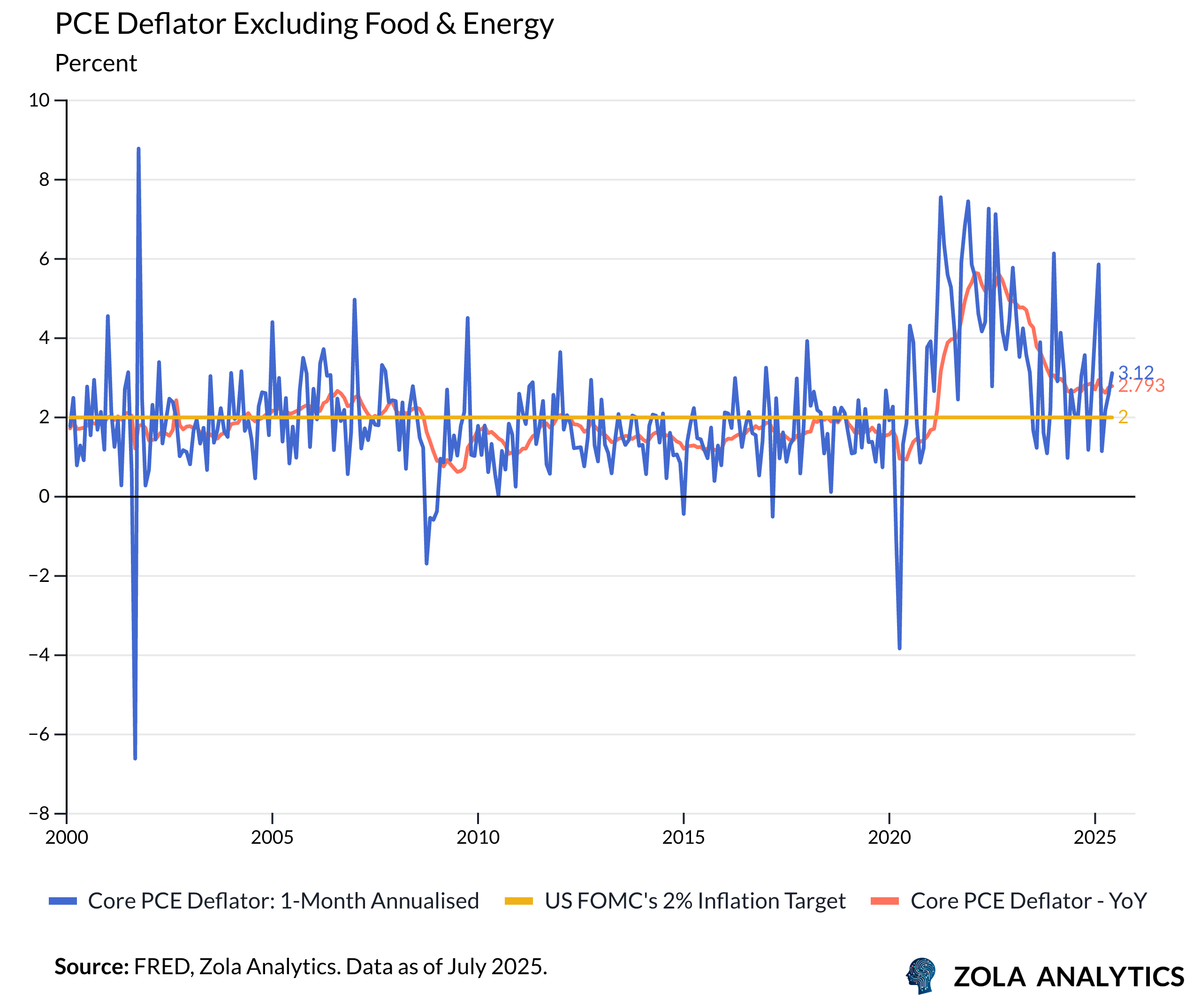

Tariff Inflation and Stagflation Fears

Tariff-related inflation remains a wild card. Powell acknowledged that while current price increases may reflect one-off shifts, the risk of persistence can’t be ignored. Businesses appear to be passing on more of the cost to consumers, and policymakers are wary of unanchored expectations. Still, the Fed appears reluctant to react prematurely to what may be a transitory impulse.

The challenge lies in balancing a stagnant real economy with sticky inflation—hallmarks of a potential stagflationary environment. This raises the threshold for easing: absent a sharp labor deterioration, cuts will be sparing.

Outlook: Optionality and Data Dependence

Analysts broadly agree that the Fed is keeping its options open. September is still in play, but the odds now lean toward a later start—October or December—depending on how upcoming payrolls and inflation data evolve. Rate path projections cluster around two cuts in 2025, with some forecasting three (Sept/Oct/Dec), and further easing in 2026 as growth stays below trend.

The tone of the July meeting suggests that clarity will only come through accumulating evidence. Between now and the September FOMC, two employment reports and two inflation prints will be released—along with greater visibility on tariff policies.

Disclaimer: Zola Analytics provides this material for informational and entertainment purposes only. It does not constitute investment advice.