Published 8th December 2025

7 minute read

The Missing Arrow

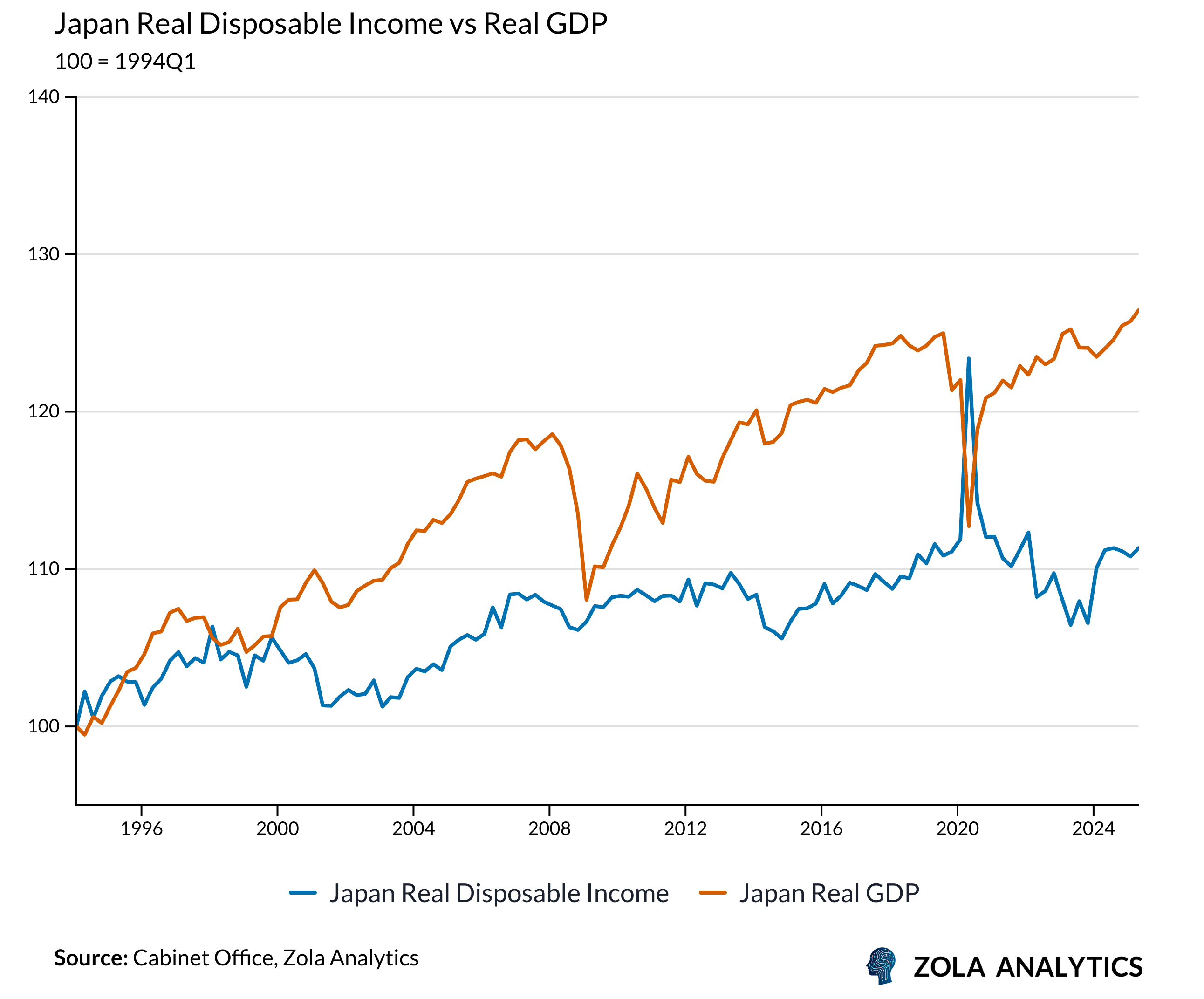

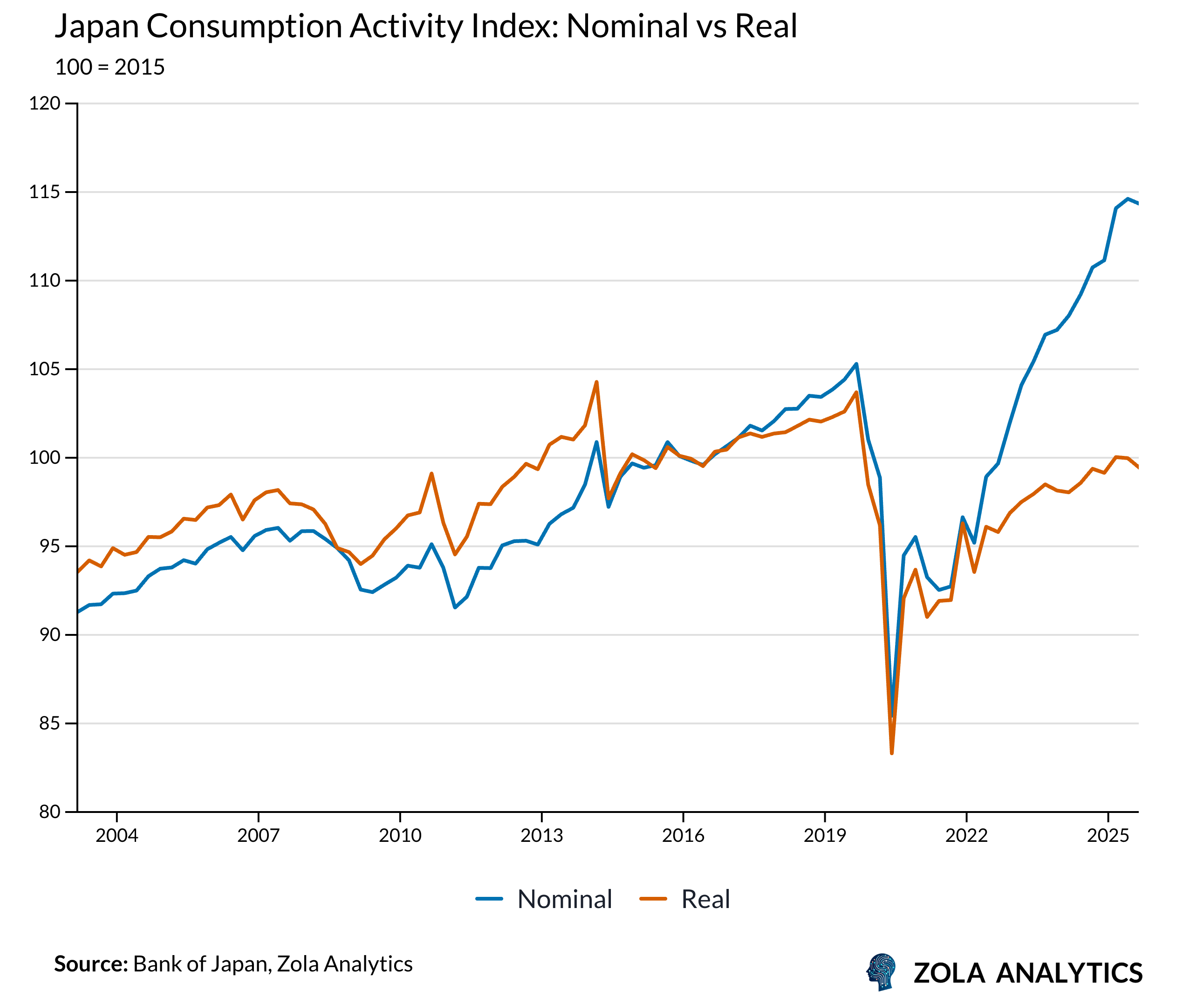

Japan's lost decades were never a growth failure, they were a transmission failure. Over the past 30 years, Japan's real GDP grew by 26% while household real disposable income grew by just 9%. Prime Minister Sanae Takaichi knows distributional problems are not solved with standalone stimulus but by shifting income toward households, with her USD 270 billion stimulus designed to ensure 'income flows securely to households.' But shifting income toward households carries high political costs in a consensus-driven system.

Takaichi has long cited Margaret Thatcher as her political idol, admiring the Iron Lady's conviction in pushing through painful reforms. To succeed, she will need to apply that conviction not merely to policy, but to fundamentally overturning Japan’s economic consensus.

Where The Growth Went

Why did this GDP growth not accrue to households? It leaked out at three stages.

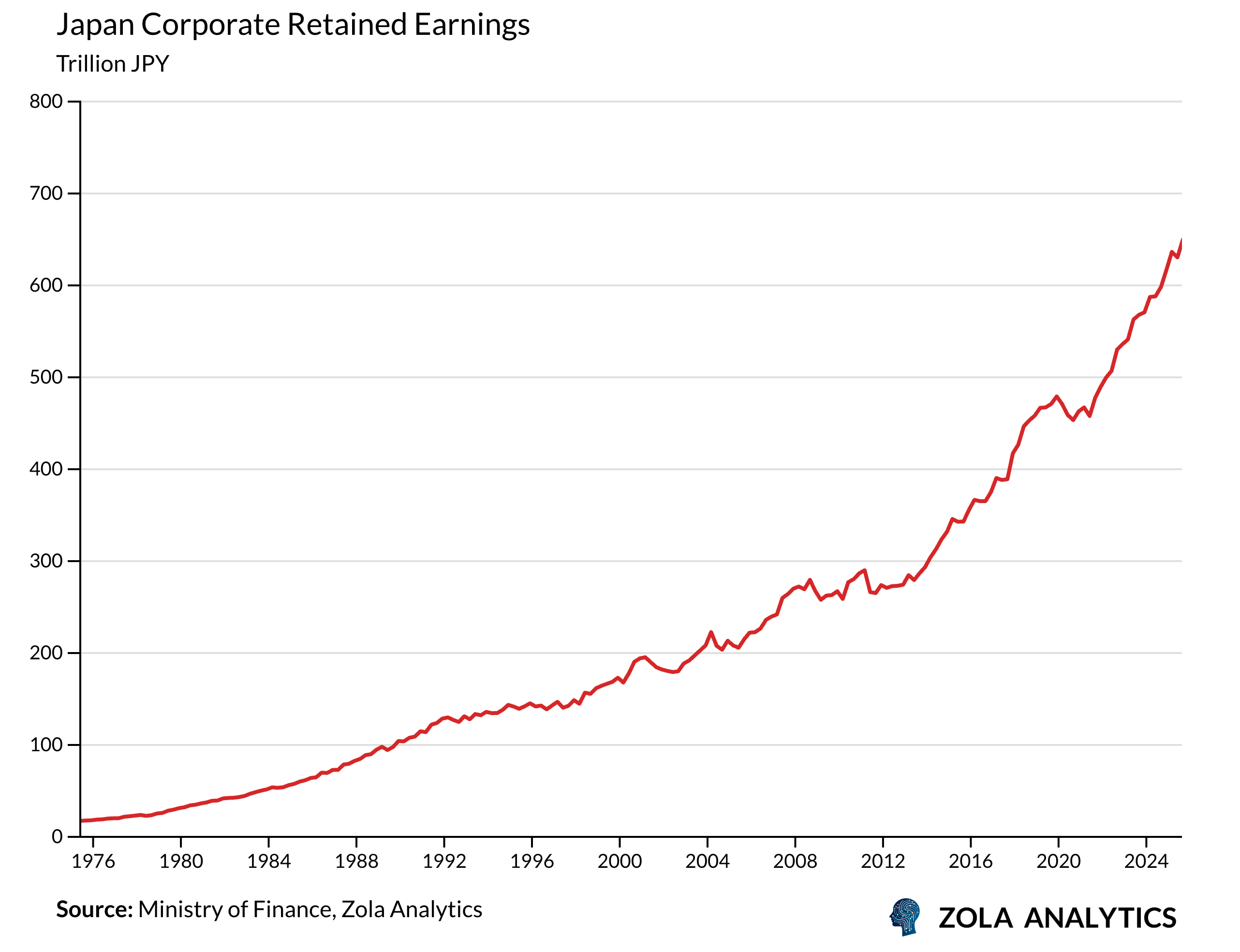

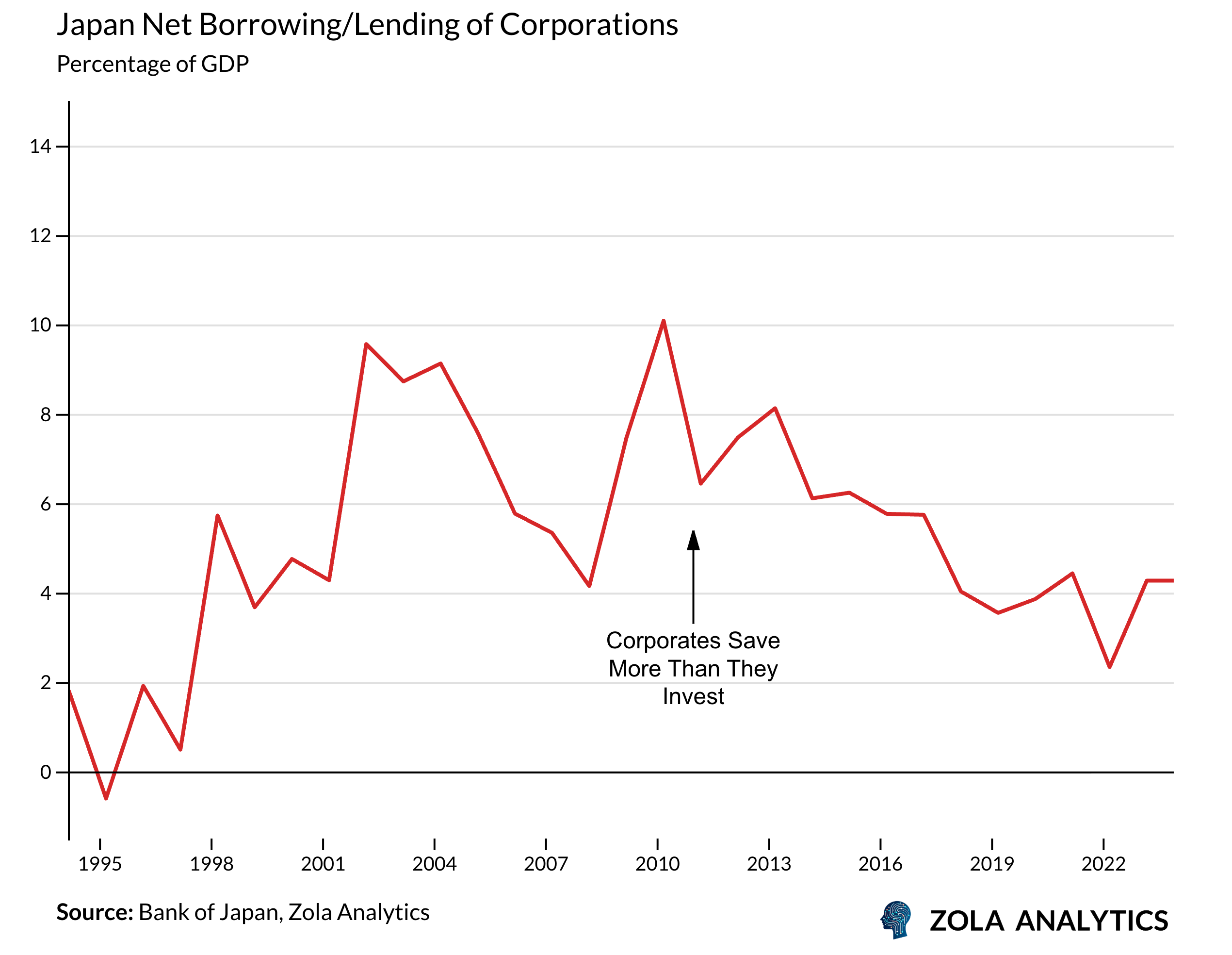

First, corporate profits have surged, with retained earnings now exceeding JPY 600 trillion, meaning cash is being hoarded rather than distributed to either shareholders or workers.

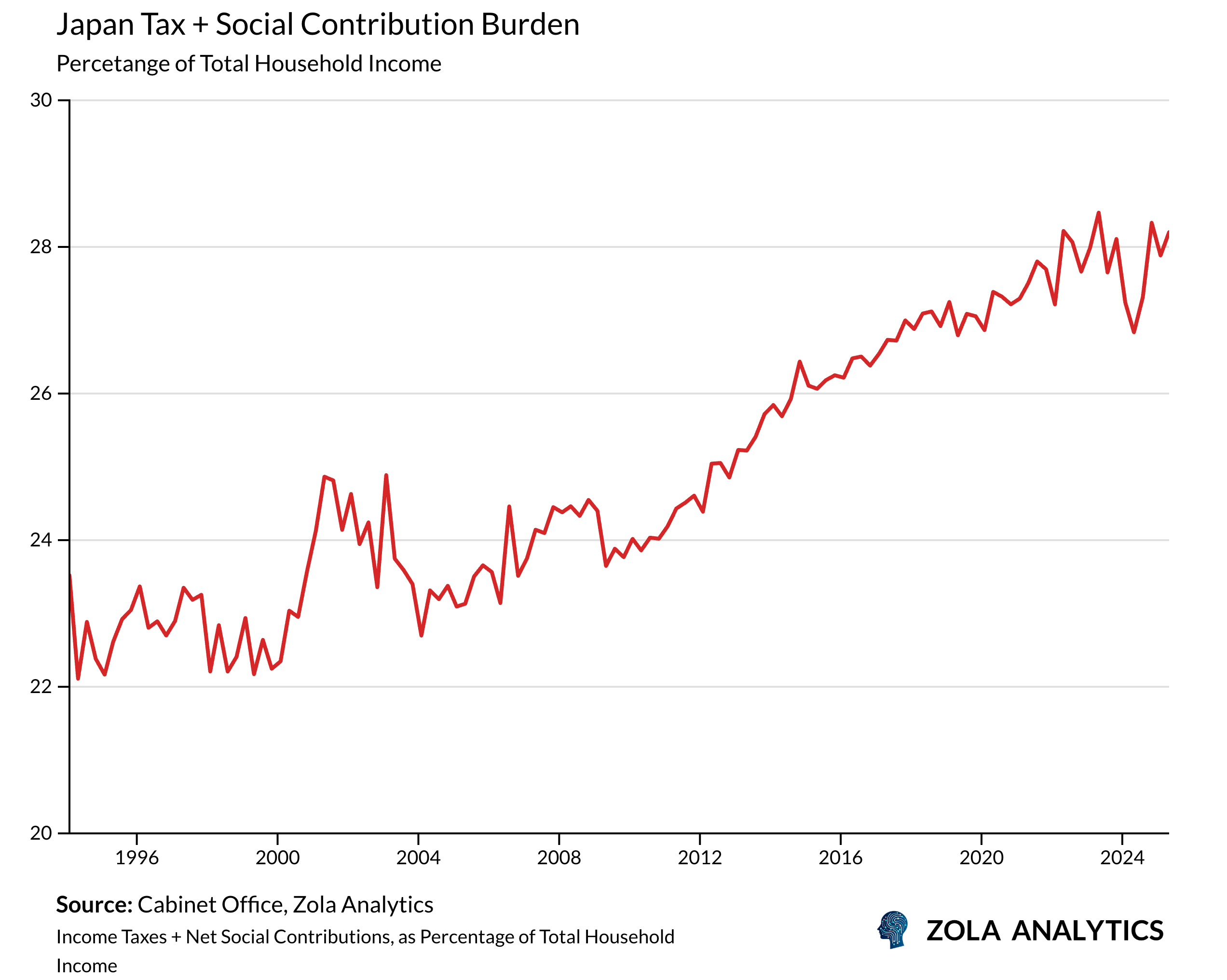

Second, wage growth did not translate into disposable income growth. Social security contributions increased by 65% as each worker now supports nearly twice as many retirees as in 1994. Taxes and social contributions together currently claim 28% of gross household income, up from 22%.

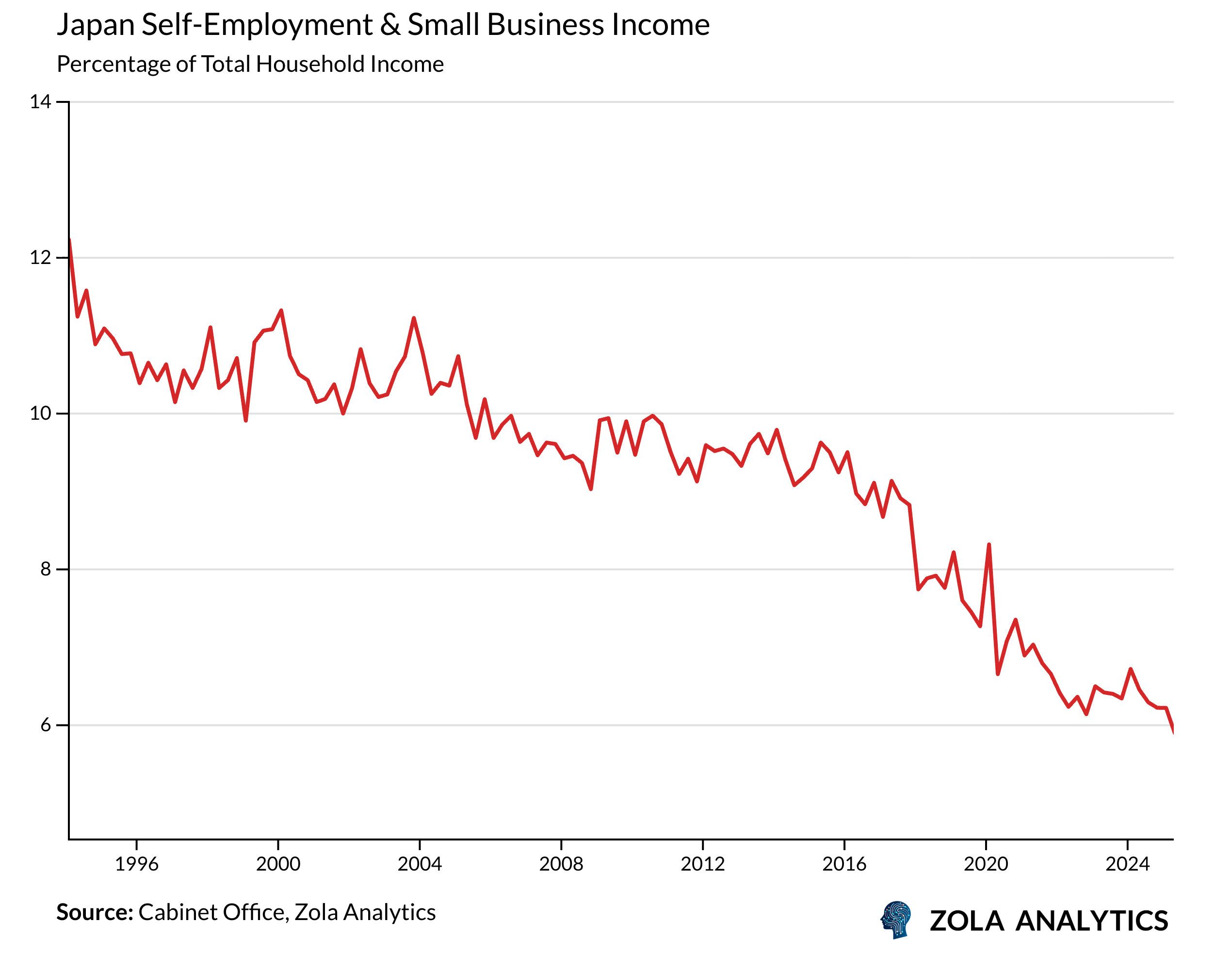

At the same time, business income collapsed as small business owners saw their share of household income fall from 11% to 6%, with ultra-low interest rates keeping zombie firms alive and strangling viable competitors by hoarding labor and capital in unproductive sectors.

Third, the inflation surge since 2022, driven by yen weakness and energy costs, consumed the first meaningful wage gains in decades.

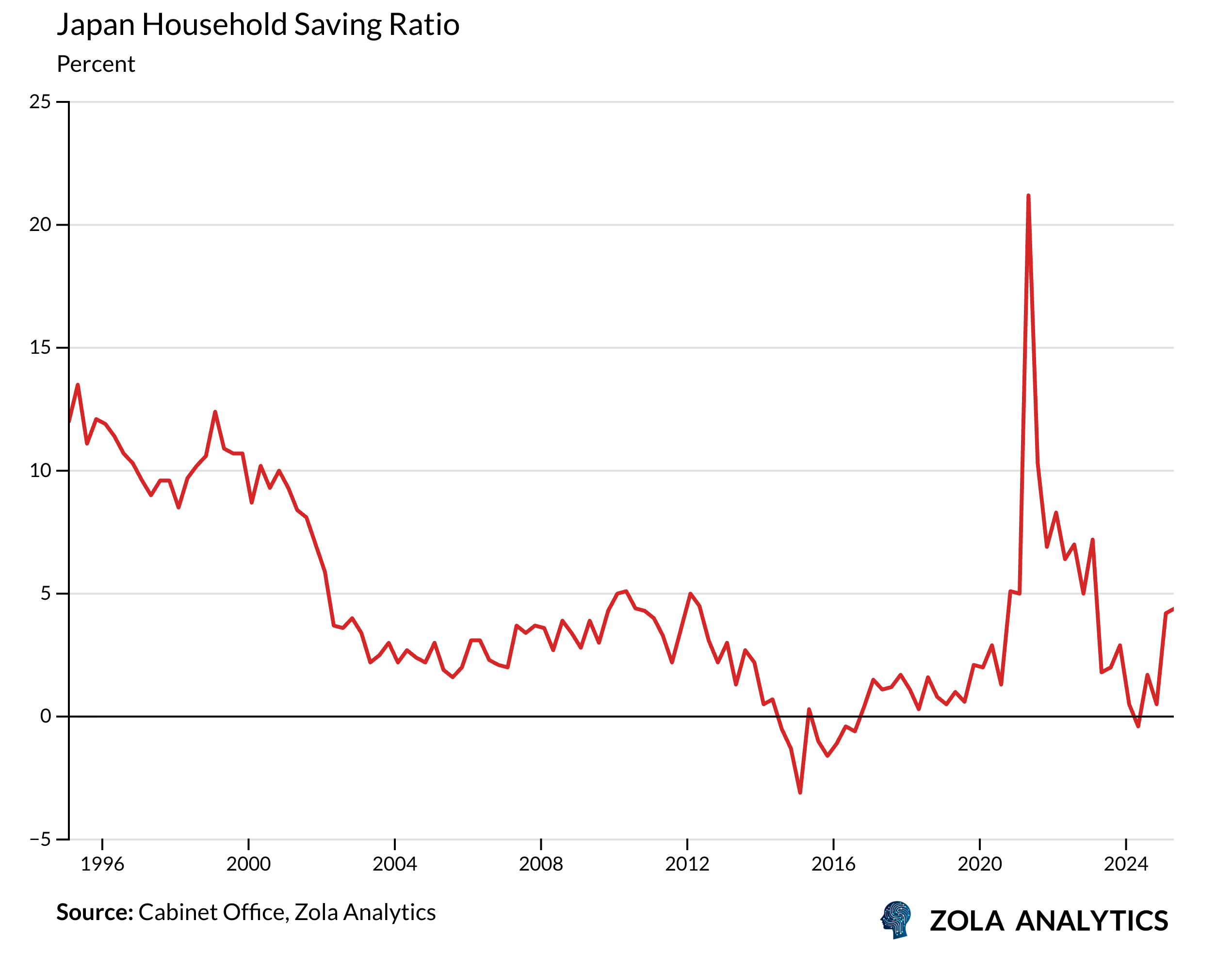

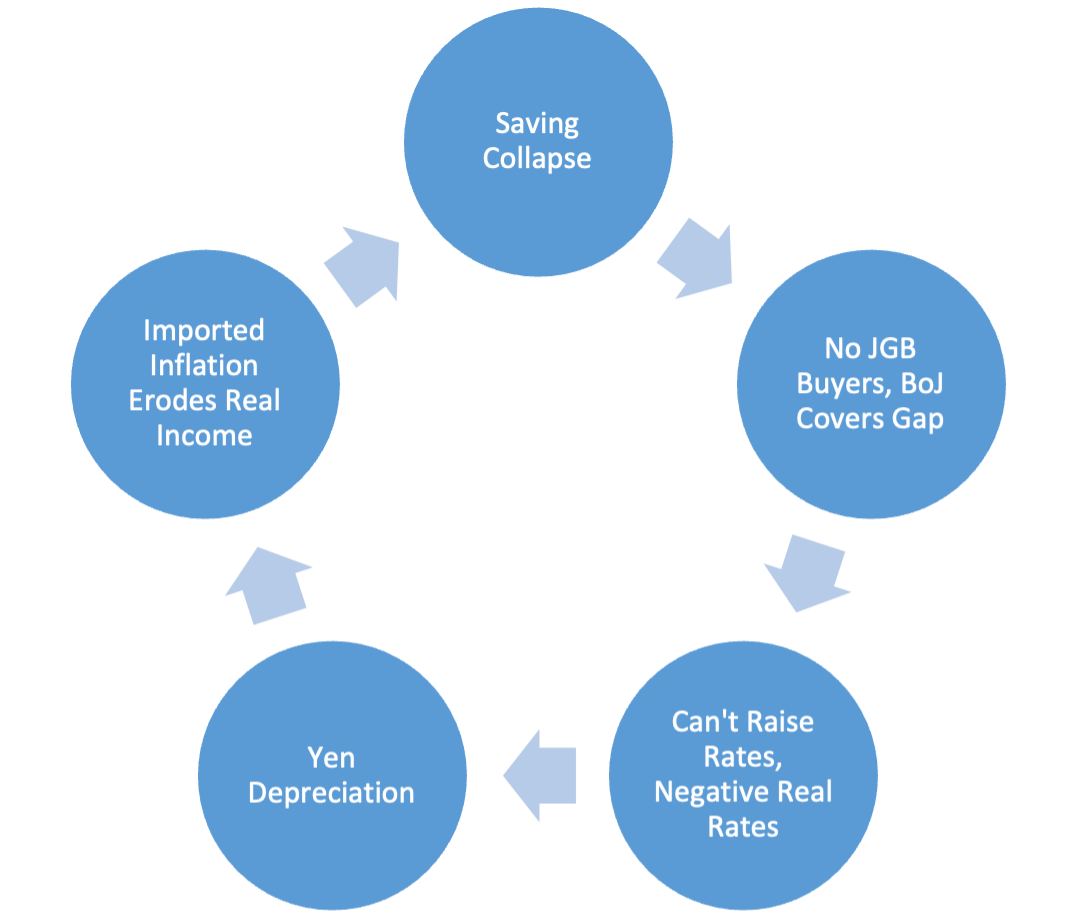

As a result, the savings rate began to fall, from 12% in 1994 to negative territory by 2013. Households were not hoarding cash waiting for the right conditions to spend, instead they were drawing down savings just to maintain consumption.

The Household Savings Trap

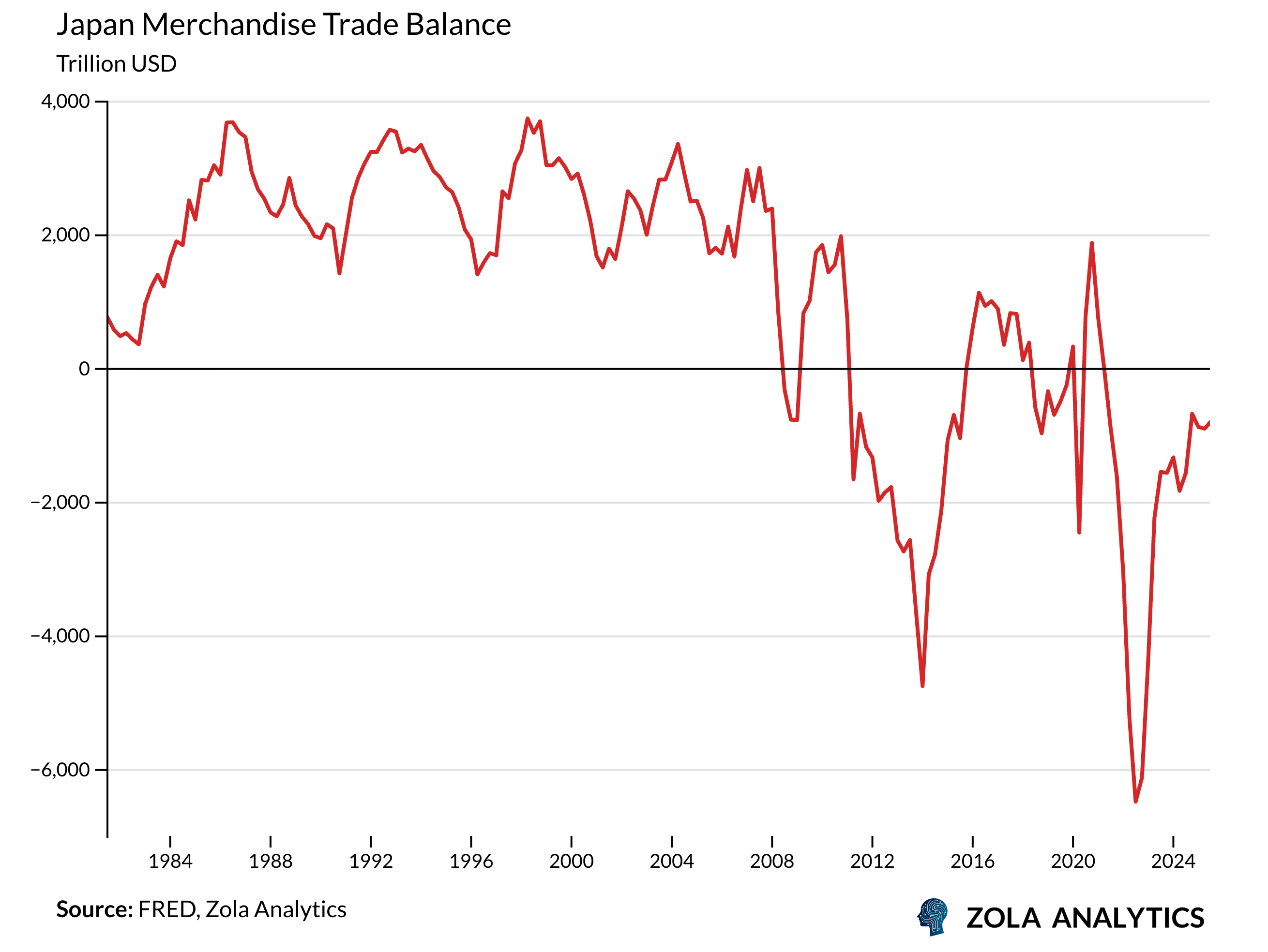

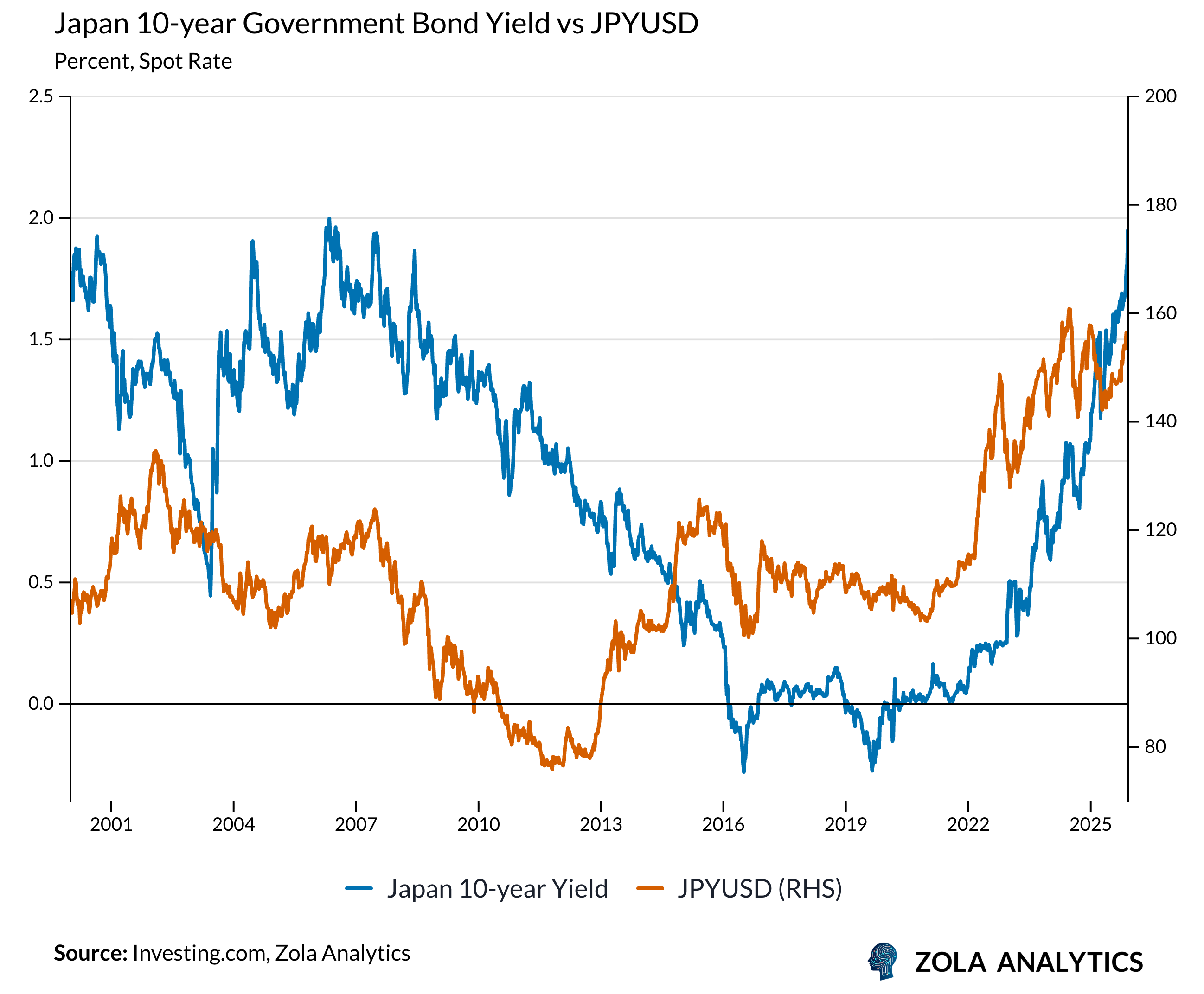

The collapse of household savings broke Japan's financing model. For decades, trade surpluses funded domestic savings, which banks channeled into government bonds. Multiple forces eroded this funding source: the Fukushima disaster in 2011 shuttered nuclear plants and left Japan dependent on expensive LNG imports; the yen weakened under Abenomics, raising import costs further; and an aging population began drawing down savings accumulated over decades of growth. Japan still earns from overseas, but increasingly through corporate investment returns rather than export revenues that become household wages.

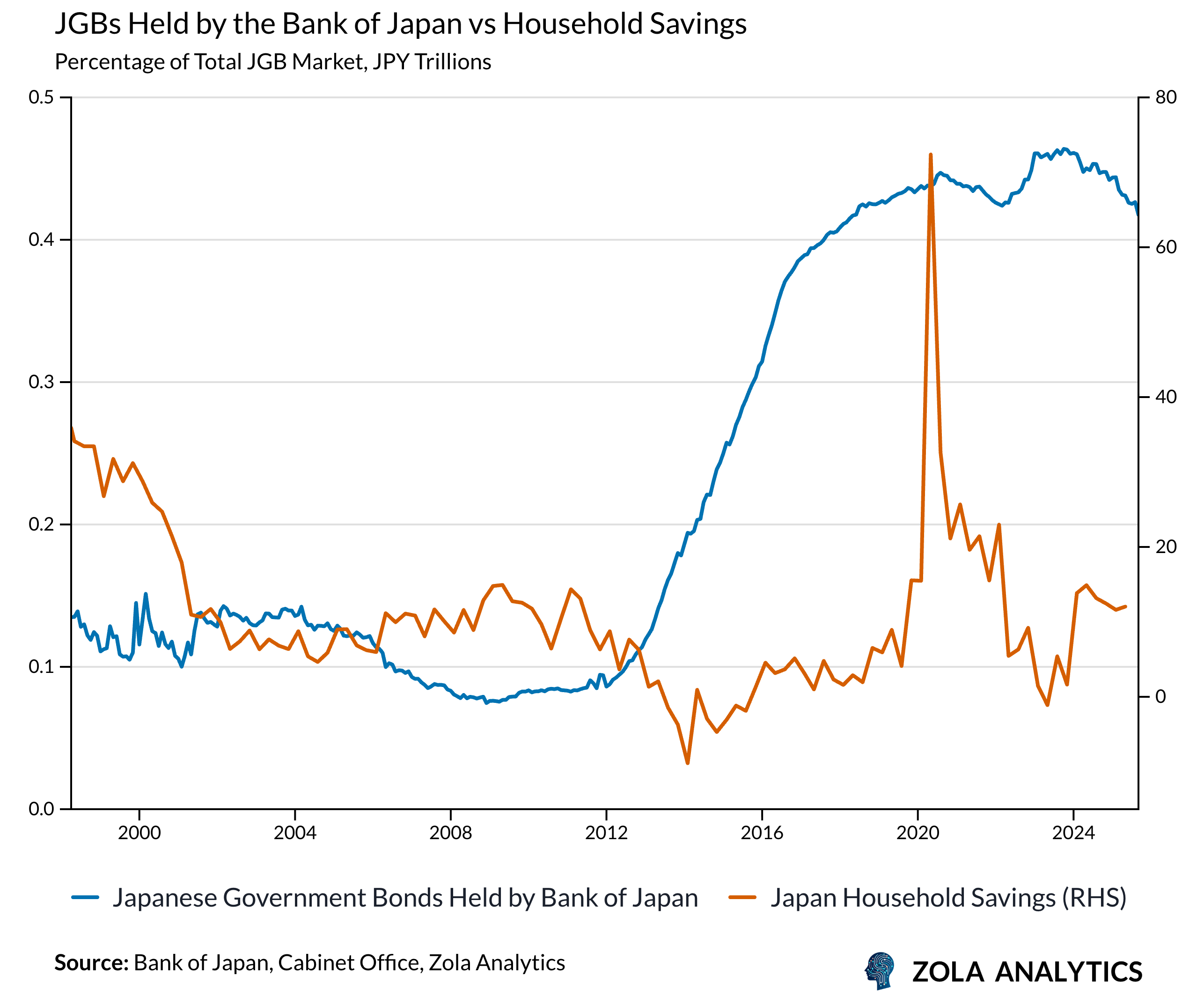

As domestic funding dried up, the Bank of Japan stepped in, gradually accumulating over 50% of the JGB market through a decade of quantitative easing. With gross debt exceeding 250% of GDP, even modest rises in borrowing costs would consume an ever-larger share of government revenue. The BoJ must keep yields low to prevent debt from compounding faster than the economy can grow.

But suppressing yields requires continued monetary accommodation, which weakens the yen. Japan can protect the bond market or the currency, but not both. It has always chosen the bonds. Households bear the cost through higher import prices, which erode the incomes families need to rebuild savings. Declining savings forces the BoJ to intervene, and its intervention perpetuates declining savings, a circular trap.

A False Choice: Demand vs. Decline

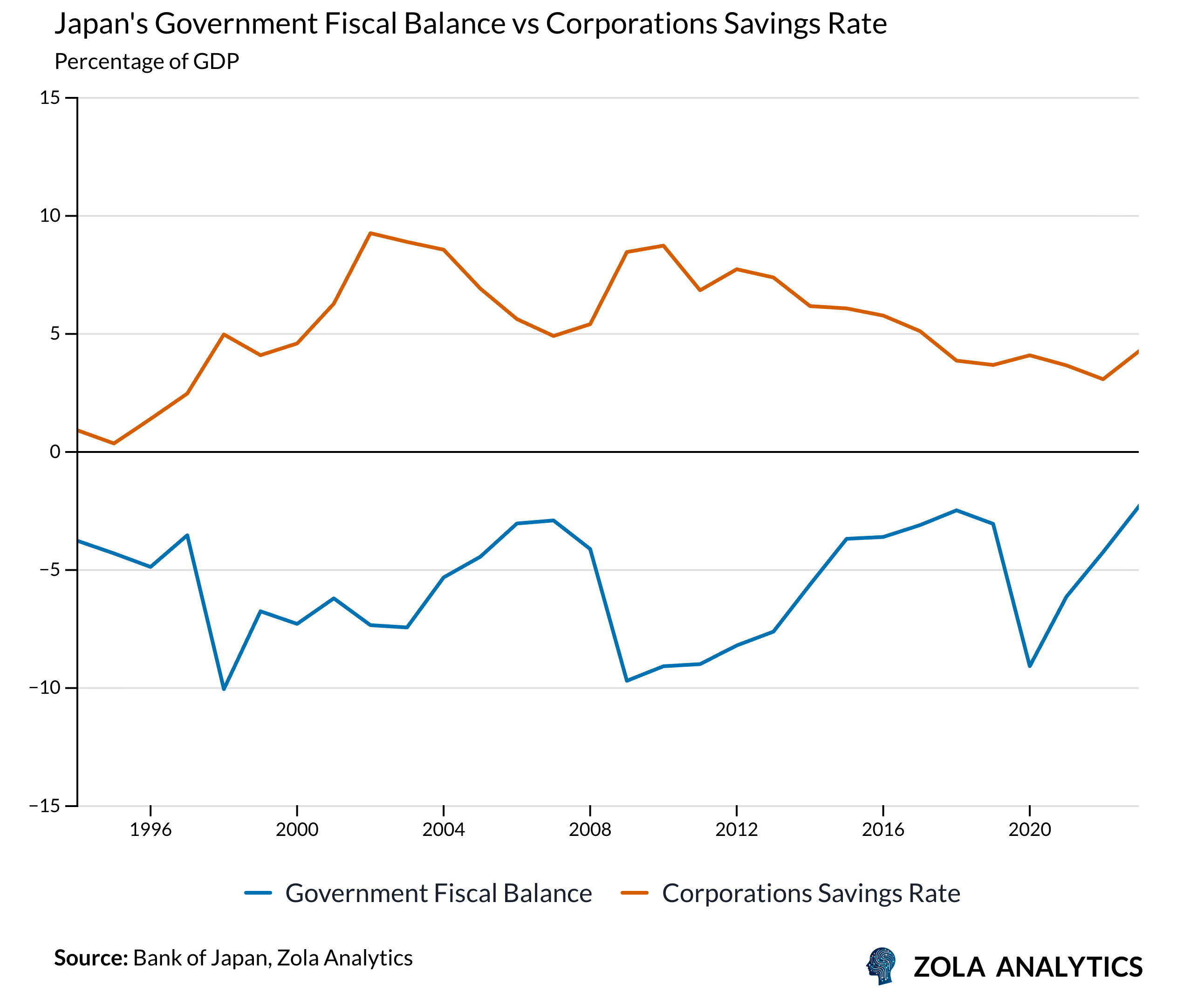

Fiscal expansionists argue Japan's problem remains insufficient demand. Corporations have become massive savers rather than borrowers. When the private sector will not borrow, the government must.

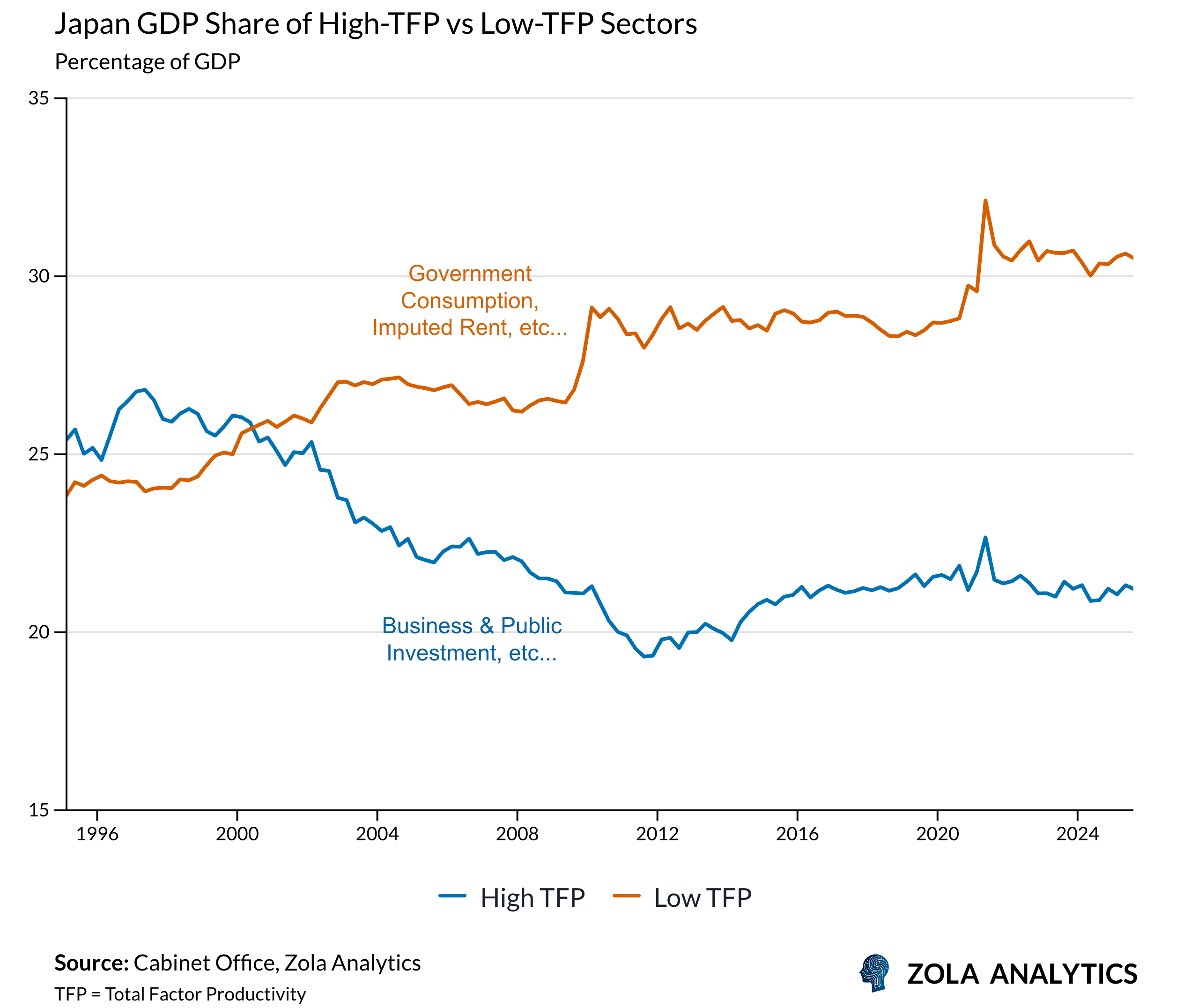

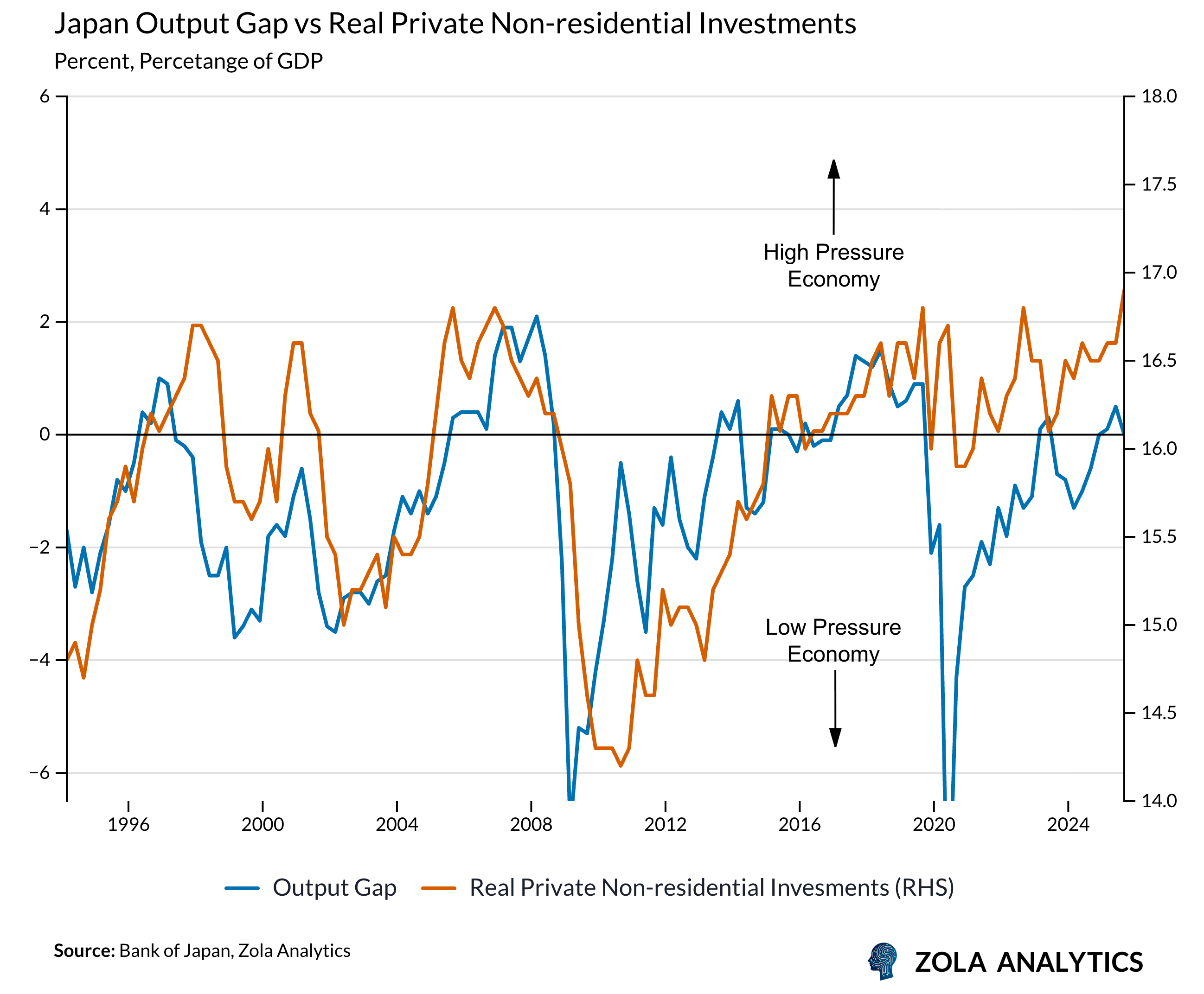

Structural pessimists counter that Japan's problem is permanent. The elderly share doubled from 14% to 29%, and when 30% of your economy consists of activities with near-zero productivity growth, aggravated by ultra-low interest rates keeping zombie firms alive, aggregate productivity is mathematically capped.

Both sides have compelling evidence, yet their focus on either demand or decline obscures the core structural problem: a failure of economic transmission. Despite GDP gains, wealth consistently failed to flow to families. Injecting more stimulus through these same broken channels is merely a guarantee of the same result.

Takaichi’s Stress Test

Takaichi represents a philosophical break from Abenomics and from her mentor Shinzo Abe. Where Abe's governance reforms prioritised shareholders, Takaichi has called corporate hoarding a problem and promised to revise the code to direct resources toward employees. Where Abenomics relied on monetary easing and hoped spending would follow, Takaichi accepts monetary tightening while pursuing fiscal expansion through pro-growth policies. Her priorities are defense, nuclear energy, and semiconductors, with the explicit goal of ensuring the resulting income reaches households.

Her mechanism targets our three leakages directly. A high-pressure economy with an output gap above 2% should force wages up. Social security reform should let more of those wages reach disposable income. And by accepting the monetary tightening needed to stabilize the yen, she aims to halt the inflation eroding household wealth. However, this forces the BoJ onto a narrow path, tightening enough to stabilize the currency without pushing yields high enough to destabilize debt dynamics. Takaichi's fiscal expansion makes this balance harder, not easier.

Success, therefore, rests on behaviour change. The corporations that hoarded JPY 600 trillion are now expected to invest and distribute. The social security system that captured household gains is promised reform. Three decades of similar promises suggest intent alone changes little. Thatcher broke such logjams through singular confrontation against unions; Takaichi must break hers through consensus-building within her own corporate-backed coalition.

Household prosperity should have been Abenomics' fourth arrow. Takaichi appears to understand this and her embrace of 'Iron Lady' resolve signals a desire for decisive action. Yet the Japanese political consensus system acts as an anchor on radical change. Her core challenge is achieving a profound structural consensus among corporate Japan that redirects profits away from balance sheets and back to workers. If the established order continues to funnel gains elsewhere, her term will be another cycle on the treadmill.

Ultimately, the only measure that matters is whether this conviction can compel the consensus system to deliver prosperity directly to the household.