Published June 10th 2025

US May Employment: Labour Strength Masks Weakness

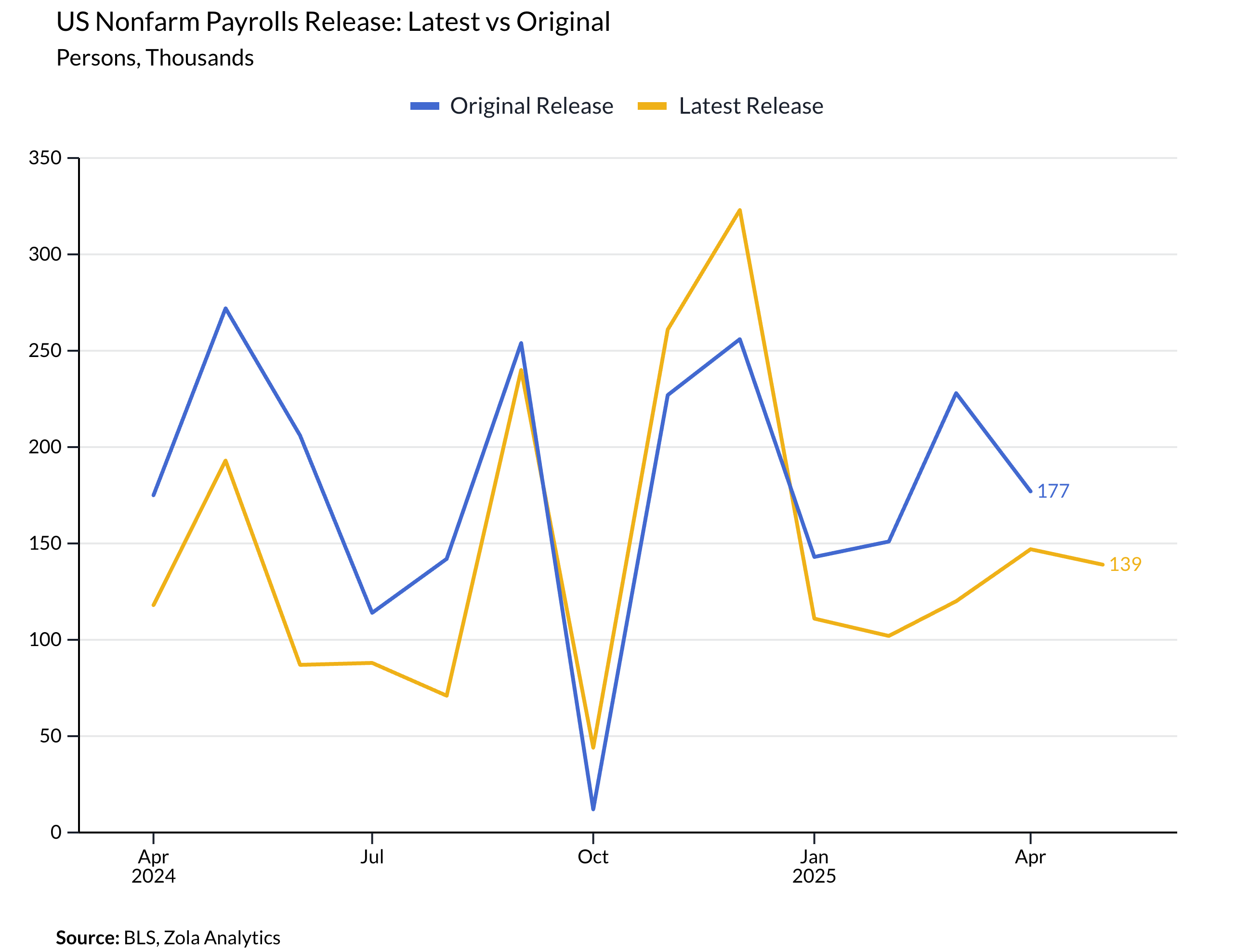

The May Nonfarm Payrolls (NFP) report delivered what, on the surface, looked like a reassuring message. Job growth came in at +139k, a modest beat over the consensus and a marked improvement on the whisper number. But scratch beneath the surface, and a more cautious narrative begins to emerge—one that should temper any hawkish inclinations at the Federal Reserve and reinforce expectations of policy easing later this year.

Yes, the three-month moving average of payroll growth ticked up slightly, now sitting at +135k, up from +123k. However, this was achieved not through a sudden surge of employment strength but via a technical sleight of hand—revisions to previous months were substantially negative, totalling -95k. March’s gain was slashed to +120k from an initially reported +228k. This isn’t a fluke; it's part of a broader pattern of downward revisions that underscore fragility in the labour market’s underlying momentum.

Meanwhile, the unemployment rate stayed put at 4.2%, which would normally suggest stability. But this was only achieved thanks to a fall in the participation rate. The household survey—which often flags turning points earlier than the headline establishment survey—showed a staggering loss of nearly 700,000 jobs. That is not the kind of labour market strength that would support consumer confidence or robust real income growth.

Wages did offer a glimmer of strength, with average hourly earnings up 0.4% on the month, holding the annual pace at 3.9%. However, in the current context—where fiscal drag, tighter immigration, and weak investment confidence are all taking a toll—this is unlikely to alarm the Fed. If anything, wage growth without corresponding employment gains hints at margin compression rather than inflationary overheating.

What does this all mean for policy? While the Fed is unlikely to jump the gun in June, the cumulative evidence suggests softening. The risk of an employment-led downturn may not yet be imminent, but the direction of travel is clear. With inflation proving sticky, the Fed faces a difficult balancing act—but a labour market losing its breadth and depth could well tip the scales toward cuts by September.

Markets might still be operating on reflexive hope, supported by the “TACO trade” logic (Trump Always Chickens Out), but the reality is that the labour market is quietly cooling. This is not yet a recession story—but it is very much a “muddle through” scenario, where policy will need to remain nimble, and any assumptions of US economic exceptionalism should be quietly revised.