Published July 4th 2025

June US Employment: A Resilient Facade Hiding Cyclical Weakness

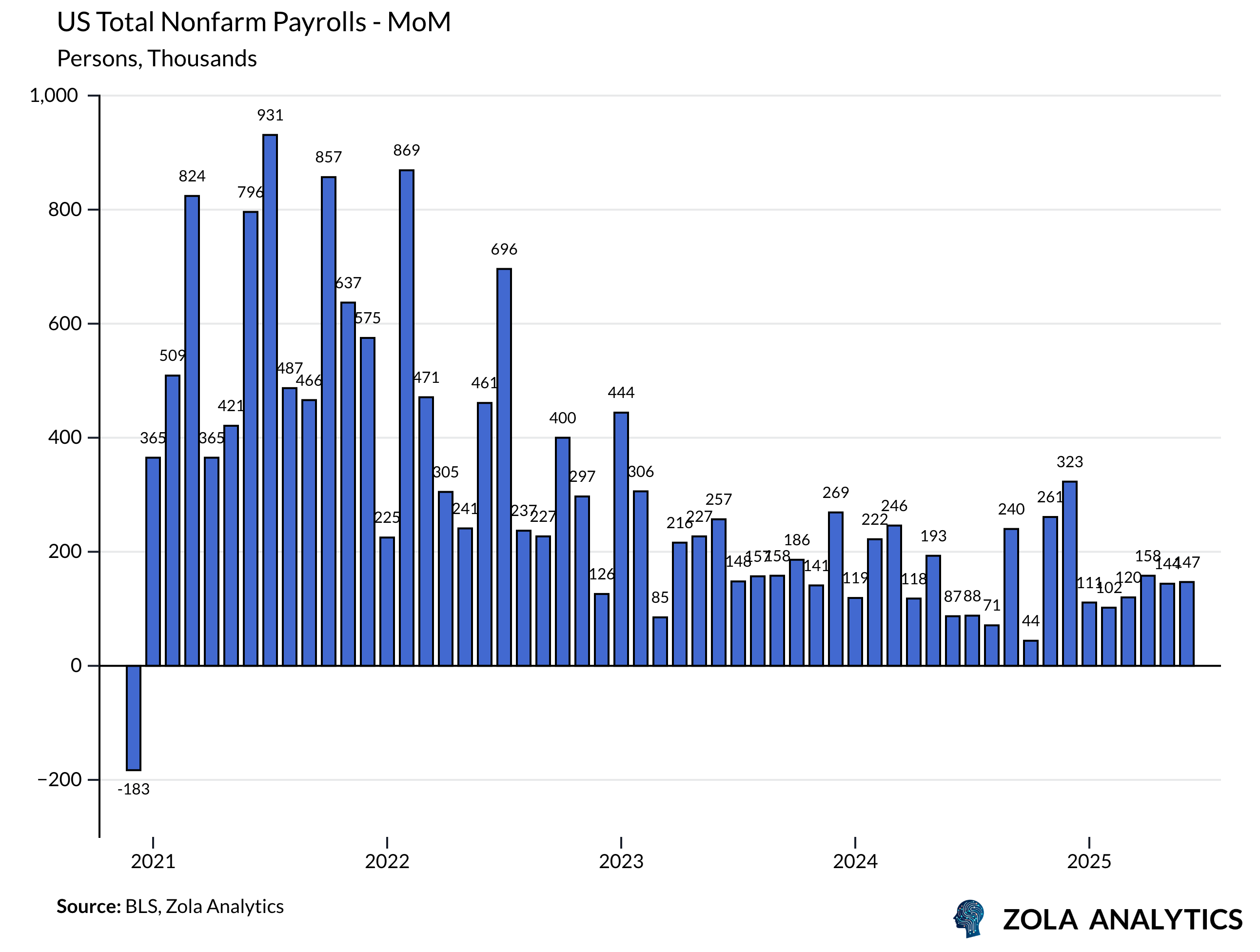

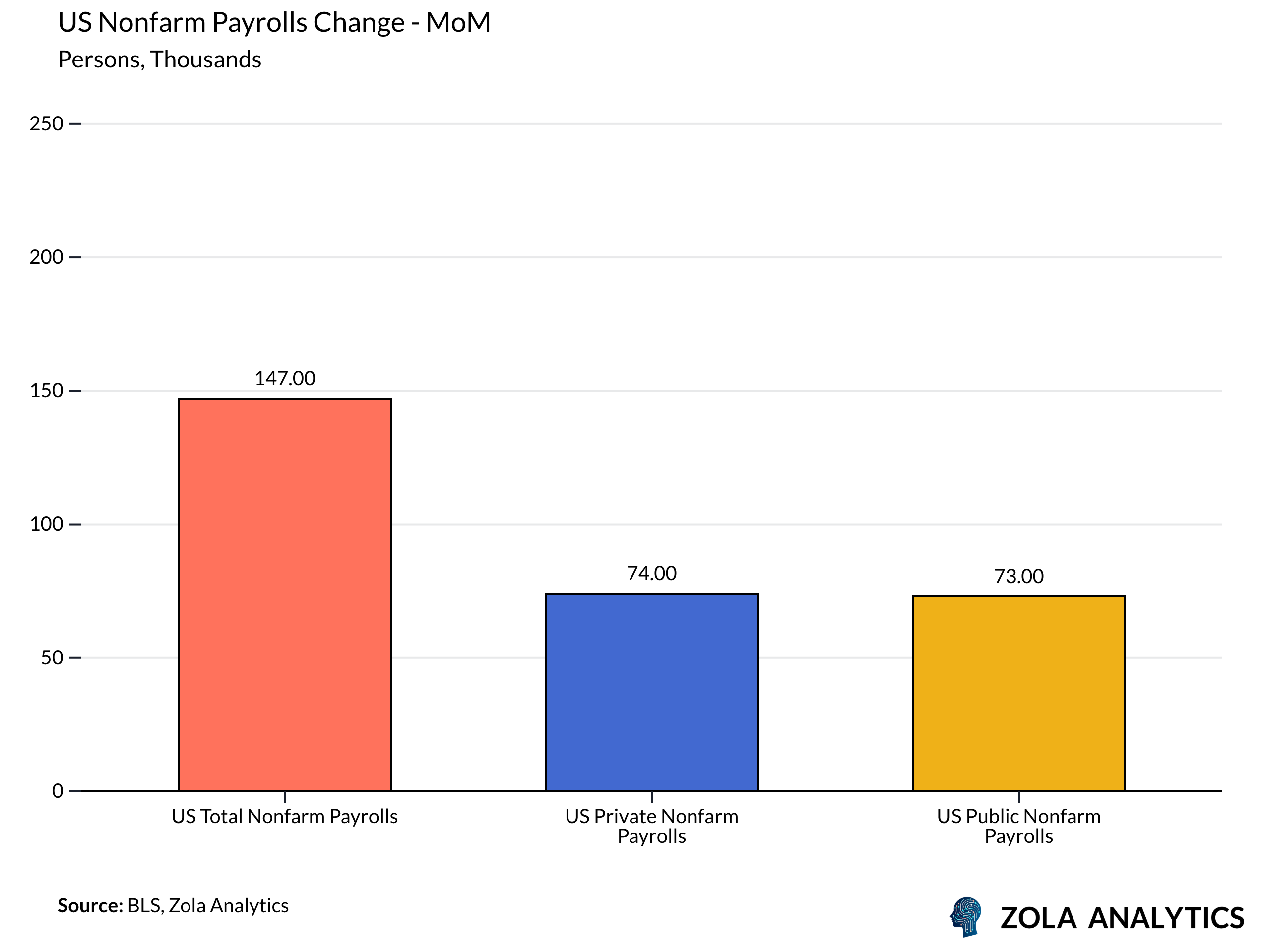

The June 2025 U.S. jobs report offered a striking headline: nonfarm payrolls rose by 147,000, beating expectations of around 110,000, and the unemployment rate fell to 4.1%, below forecasts of an increase. On the surface, these figures suggest a robust labor market. Yet a deeper look reveals a more fragile foundation — with job gains increasingly concentrated in sectors less sensitive to economic cycles and structural shifts underway that could challenge this apparent resilience.

Headline Strength, Underlying Fragility

Total payrolls reached a record 159.7 million in June, buoyed significantly by government hiring, which contributed 73,000 jobs — nearly half of the month’s total gains. The private sector added just 74,000 jobs, well below expectations of 105,000–120,000. Notably, the three-month average of private payroll growth has slowed to 115,000 from 128,000, signaling deceleration in underlying labor demand.

This dynamic mirrors a broader trend: cyclical sectors — those most exposed to shifts in economic momentum, such as manufacturing, construction, and business services — have shown limited hiring appetite in recent months. Meanwhile, education and healthcare remain primary engines of job creation, even as education employment itself has started to contract. Such reliance on government and structurally driven healthcare hiring underscores that labor market strength may be more superficial than durable.

Participation Distortions and Immigration Trends

Another key driver of the surprisingly low unemployment rate is a contracting labor force. Evidence suggests stricter immigration policies have sharply reduced new entrants into the workforce, lowering participation rates. With fewer people actively seeking jobs, the unemployment rate has mechanically declined — a dynamic reminiscent of the reverse scenario under the prior administration, when elevated immigration temporarily lifted unemployment figures. This distortion risks obscuring weakness beneath headline metrics.

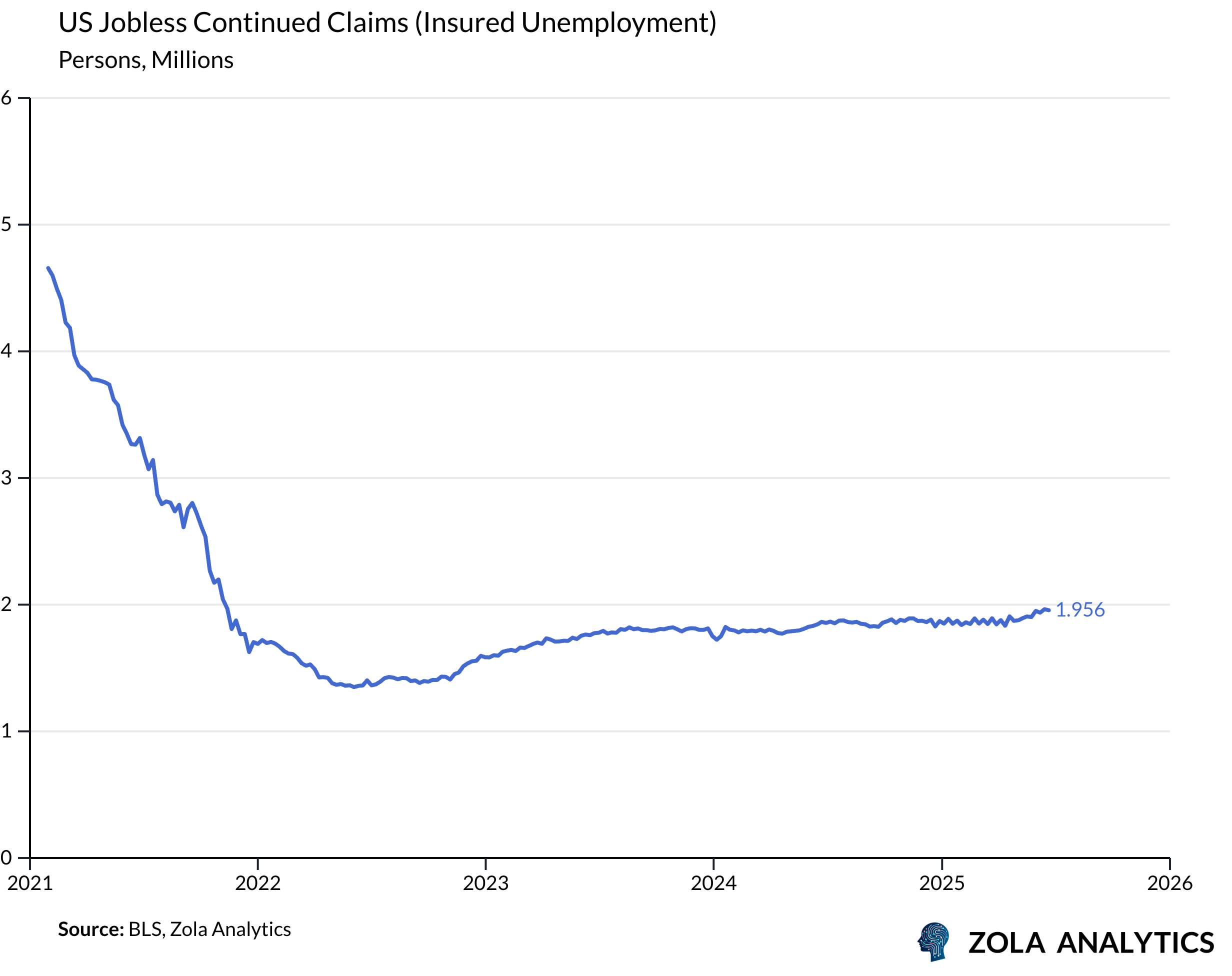

Further complicating the picture, jobless claims remain elevated. Continuing claims stand at 1.96 million, the highest since late 2021. This indicates that while layoffs have not surged, those who lose jobs are struggling to find new ones — a hallmark of a labor market with weak cyclical demand.

Policy Implications: Fed Caught Between Conflicting Signals

The stronger-than-expected payrolls and falling unemployment rate likely diminish the prospects of a July Federal Reserve rate cut. Markets have almost entirely repriced expectations, shifting from anticipating a 50-basis-point cut by September to a base case of unchanged rates in the near term.

However, risks to the labor market persist. A potential slowdown in healthcare hiring — with recent job gains already nearing the pre-pandemic trend — could remove a key support pillar. Moreover, proposed federal budget cuts to healthcare funding could accelerate this shift, amplifying labor market weakness.

The Fed faces a dilemma: headline strength in jobs data justifies policy patience, but underlying softness in private sector hiring and rising continuing claims suggest deteriorating conditions ahead. Inflation pressures, especially in services, further constrain the central bank’s flexibility.

Short-Term Growth Rebound but Long-Term Risks

Despite a weak Q1 GDP reading of -0.5%, Q2 growth appears to be rebounding, with the Atlanta Fed GDPNow model tracking at +2.5% as of early July. Yet if cyclical job creation does not improve, the sustainability of this rebound is in question. The economy risks becoming dependent on sectors driven by government spending and demographic trends rather than broad-based private investment.

Should healthcare job growth stall or reverse, and cyclical hiring fail to pick up, the labor market could quickly lose its apparent strength. This would not only pressure growth but could also force the Fed’s hand on rate cuts — though likely only once clear evidence of declining nonfarm payrolls emerges.

Disclaimer: Zola Analytics provides this material for informational and entertainment purposes only. It does not constitute investment advice.