Published May 9th 2026 12 minute read

Heavy Lies the Crown

On a Sunday evening in August 1971, Americans tuning in to watch Bonanza were met instead by Richard Nixon behind a desk in the Oval Office. In a solemn address, he announced the “temporary” suspension of the dollar’s convertibility into gold. For nearly three decades, Bretton Woods had tied America’s currency to the metal that anchored global finance. The moment could have marked the end of American monetary primacy. Instead, it was the beginning of a new, more flexible order; one in which the dollar shed its anchor but kept its crown.

In this edition of Zola Chartbook, we examine the dollar’s position as the world’s reserve currency: how it was built and how it has endured. The dollar remains the backbone of global trade, energy, and finance. But the very pillars that entrenched its dominance now expose it to pressure.

Dollar Dominance

Reserve currency transitions are rare. The last time one occurred was when sterling gave way to the dollar. That process began during World War I, when Britain’s finances were stretched and the U.S. emerged as the world’s largest creditor. But it was not until after World War II, that the dollar fully displaced sterling at the center of the system.

This long handover illustrates two lessons. First, network effects make incumbent currencies hard to dislodge: the more widely a currency is used, the harder it is to replace. Second, even as relative economic weight shifts, change only sticks when the new anchor can provide deep markets, open capital accounts, and political stability.

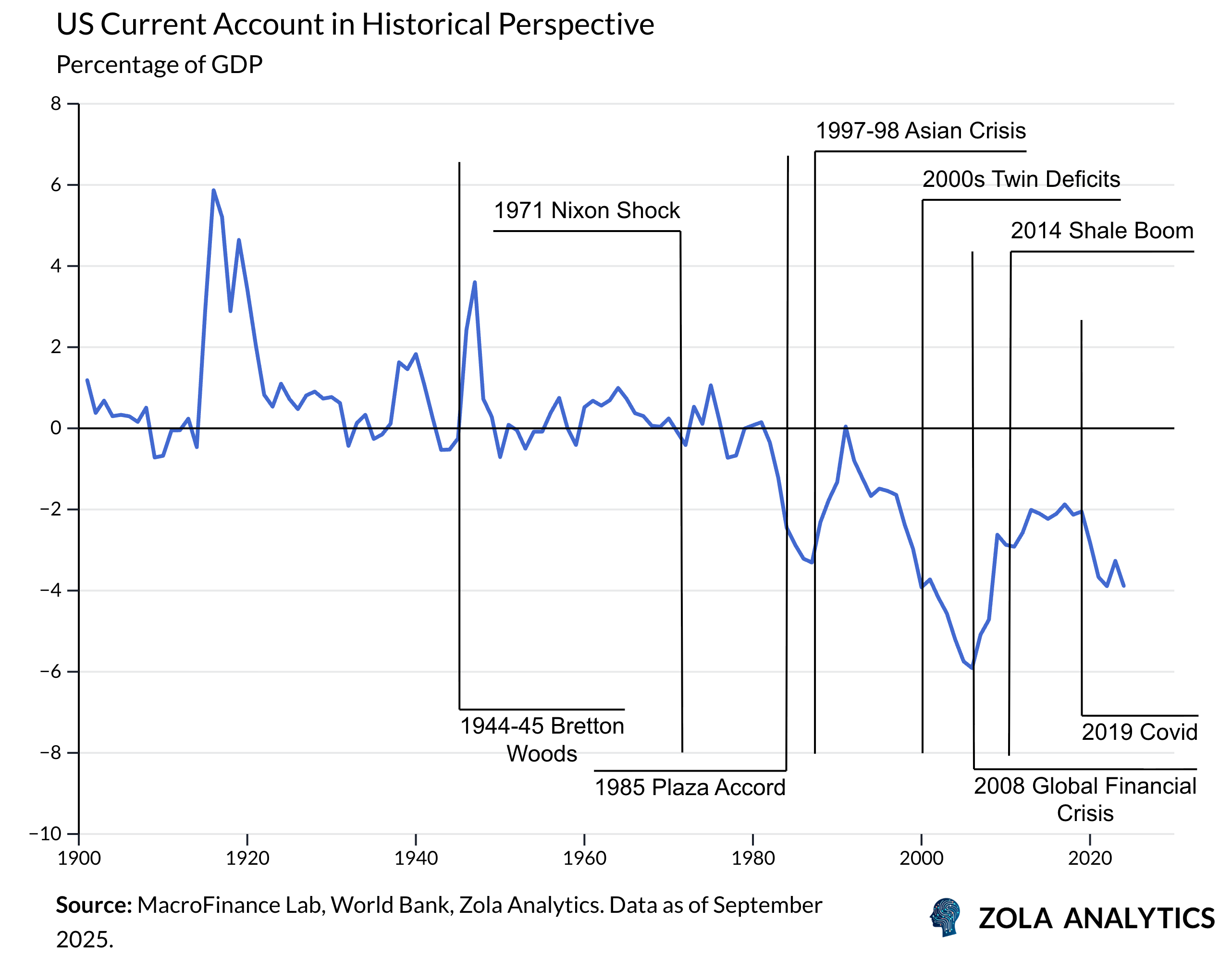

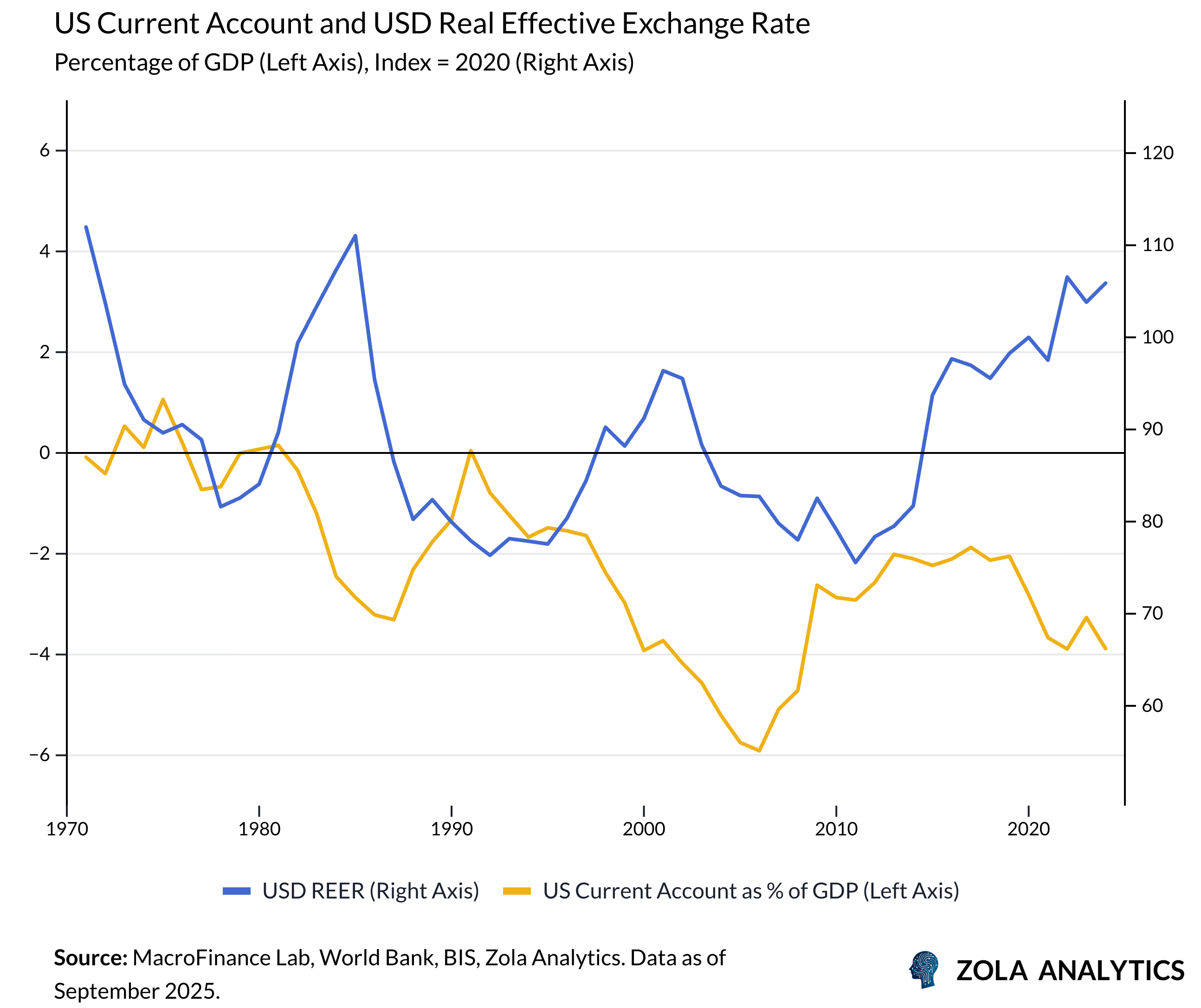

The dollar’s rise can be traced through the shifting pattern of America’s external balances. Each turning point in the currency’s role, from Bretton Woods, the Nixon shock, and the Plaza Accord, to the imbalances and crises of the 2000s, left a visible mark on the current account.

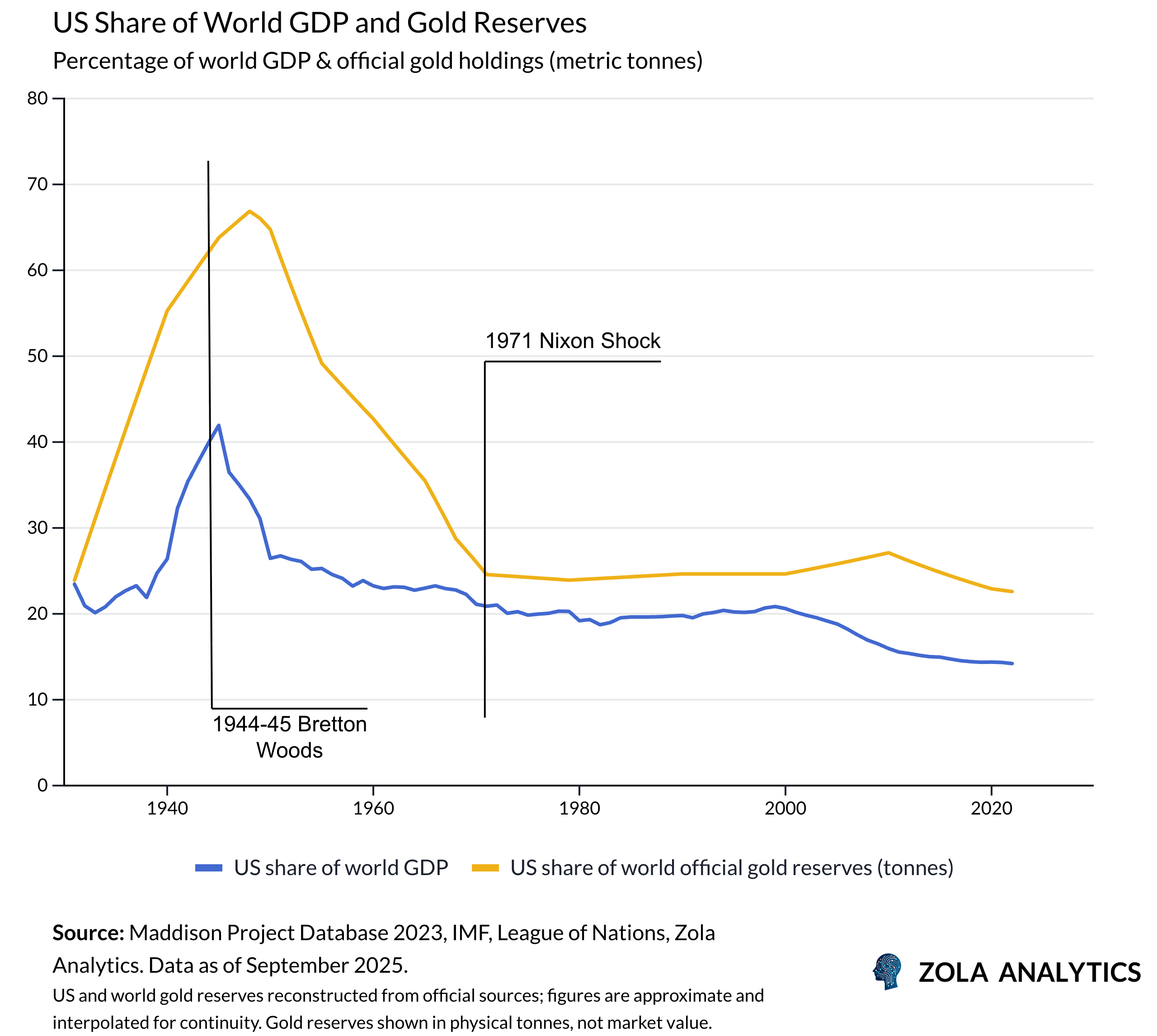

In the late 1940s, the U.S. produced nearly half of world GDP and commanded the largest gold reserves. The Marshall Plan catalysed the dollar’s entrenchment in global finance. Aid was disbursed in dollars, spent largely on U.S. goods, and cleared through U.S. banks. This forced European firms and central banks to learn the plumbing of the dollar system and accumulate dollar claims. With gold anchored in New York and Treasuries offering the only market deep enough to absorb surpluses, U.S. debt became the natural reserve counterpart. The result was not just reconstruction, but a monetary order that tied postwar trade and finance to the dollar.

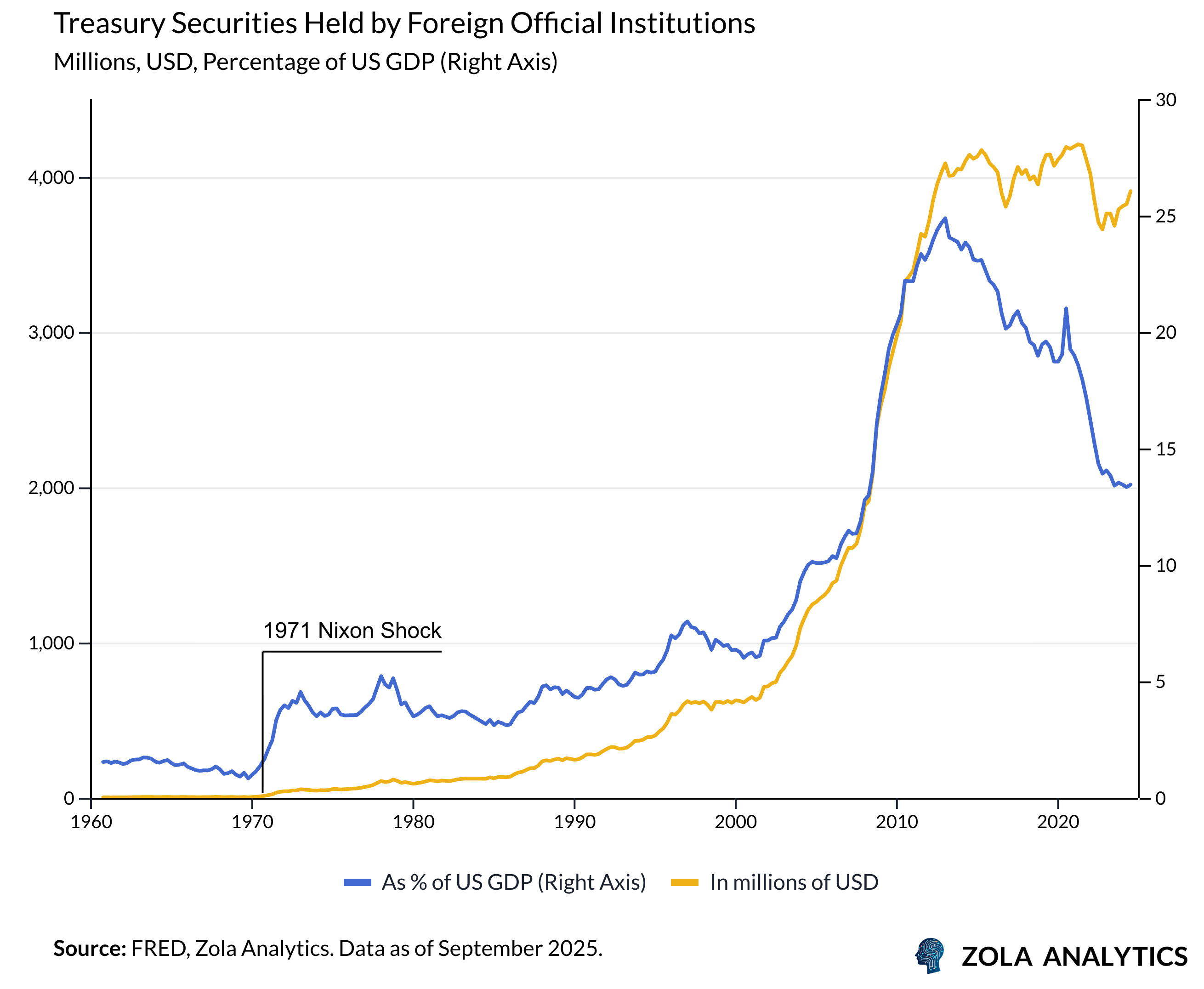

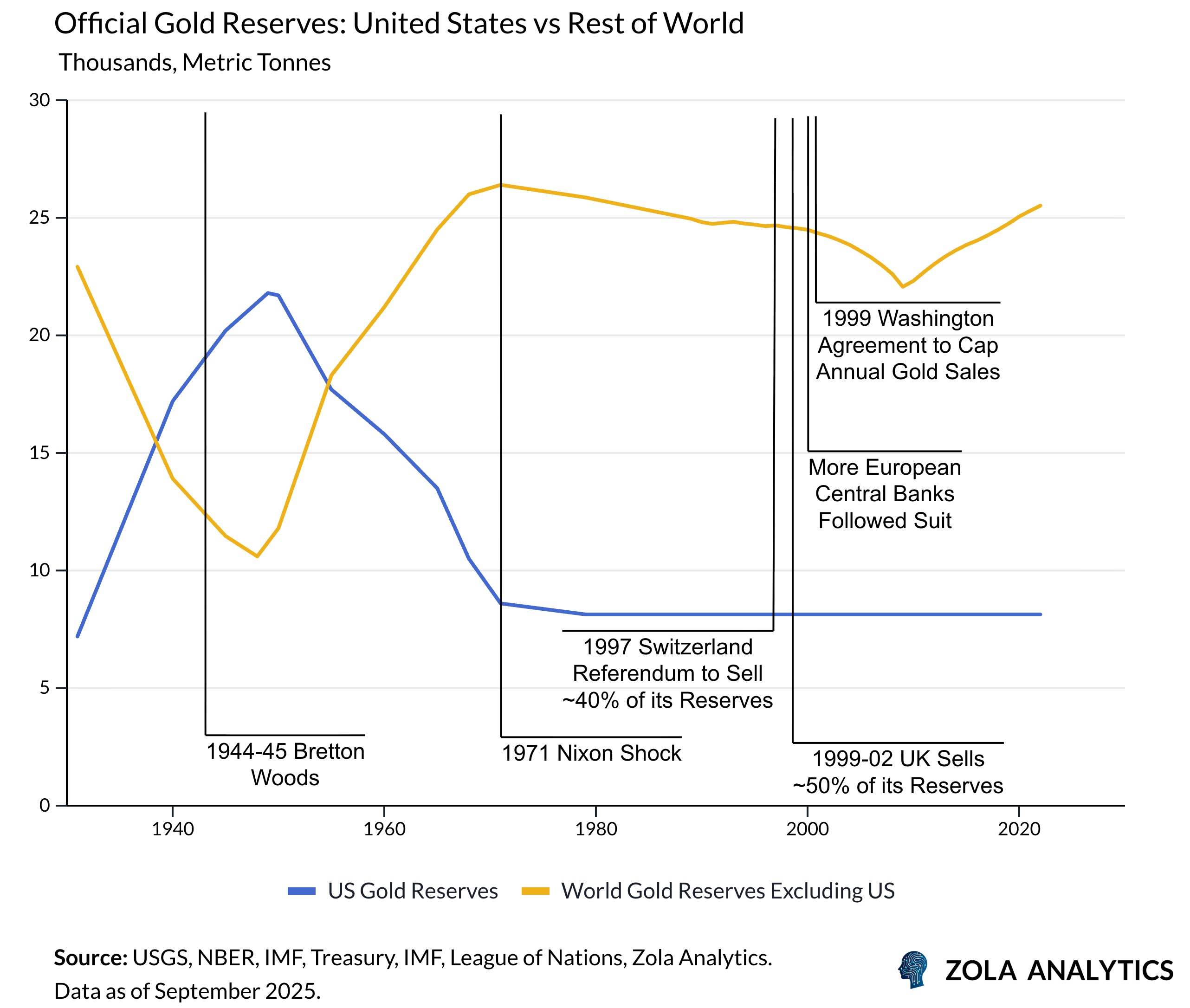

In 1944, the Bretton Woods agreement had codified the dollar’s centrality. Other currencies were fixed to the dollar, and the dollar was fixed to gold. This arrangement exported U.S. monetary stability to the world: central banks held dollar reserves, trade was invoiced in dollars, and the Federal Reserve’s credibility underpinned global finance. Yet the system contained a contradiction. To provide the liquidity others needed, the U.S. had to run persistent external deficits. By the 1960s, foreign central banks had accumulated more dollar claims than U.S. gold stocks could back, and some began converting their holdings into bullion. The result was mounting pressure on the peg: either restrict dollar supply and risk starving global liquidity, or keep running deficits and undermine confidence in convertibility.

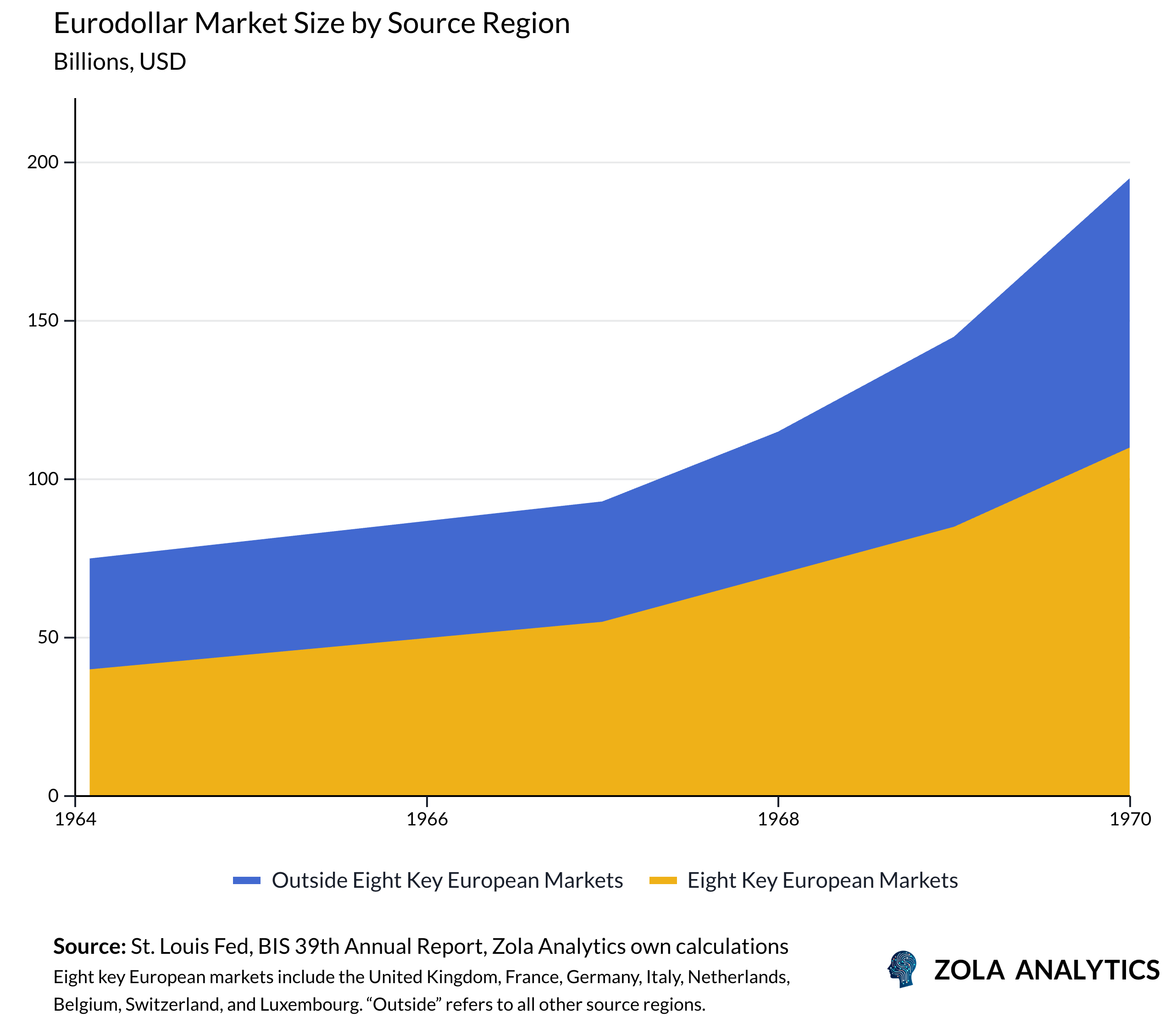

Even before the gold link broke, dollars were spilling beyond the system’s official limits. From the late 1950s, banks in London and elsewhere began taking deposits and making loans in dollars outside U.S. jurisdiction. This eurodollar market expanded rapidly through the 1960s, multiplying global dollar liquidity without drawing on U.S. gold reserves. It gave firms and central banks a parallel channel to transact in dollars offshore, reinforcing the currency’s global role even as Bretton Woods creaked under the weight of deficits and dwindling gold.

By 1971, the contradictions were unsustainable and the system broke apart. Yet instead of losing its role, the dollar maintained supremacy. Deep U.S. financial markets, a dense payments infrastructure, and the absence of credible alternatives meant that Treasuries assumed the anchoring role once played by gold.

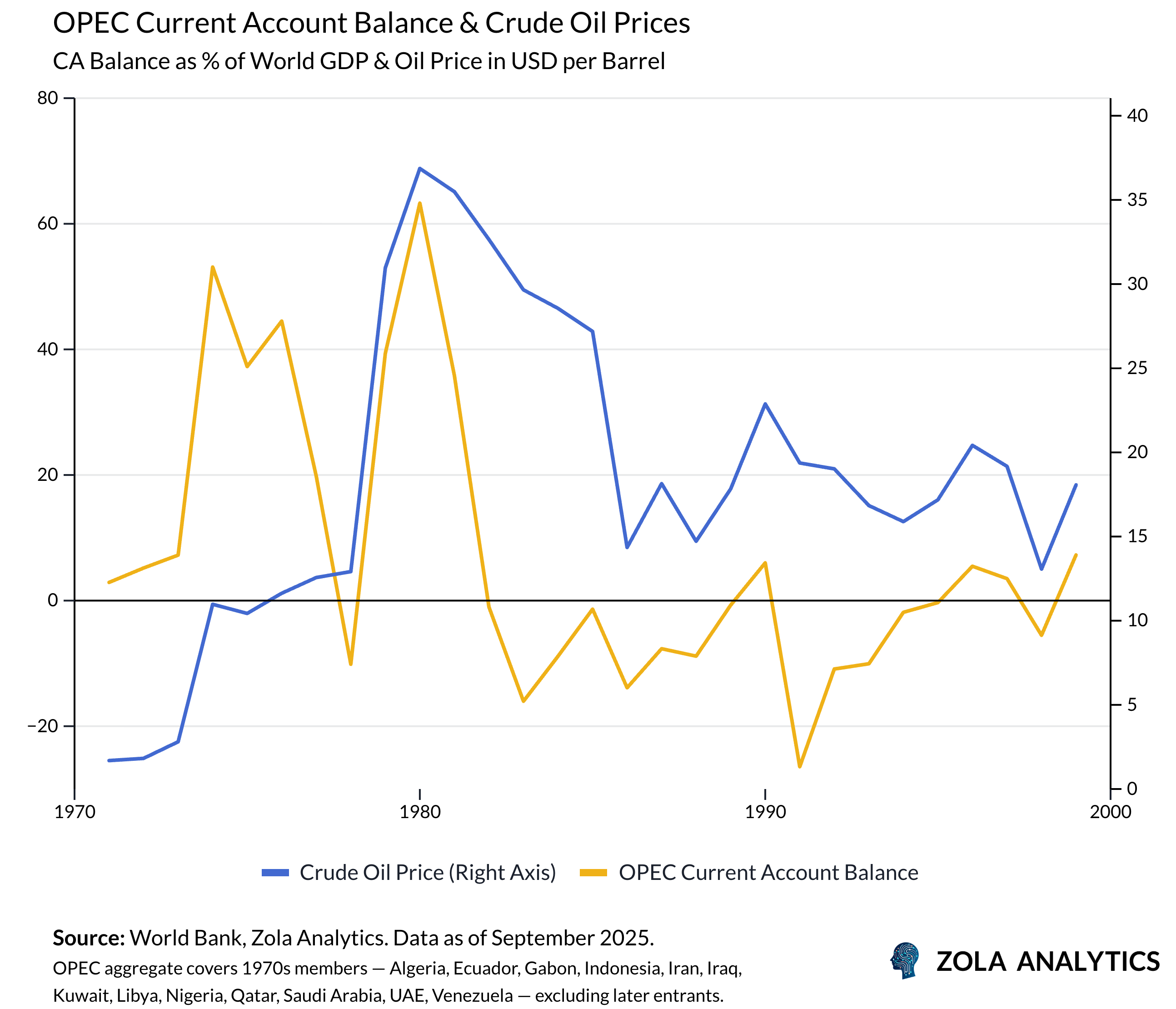

That order was secured in the 1970s through the oil trade. In the wake of the OPEC embargo, U.S. officials struck agreements with Saudi Arabia and others to price oil in dollars and recycle the proceeds into U.S. markets. This structure created a consistent need for dollar liquidity, as it tied energy transactions to the dollar system. Surpluses recycled into Treasuries ensured that, even without gold, the dollar’s primacy endured.

Imbalance In All Things

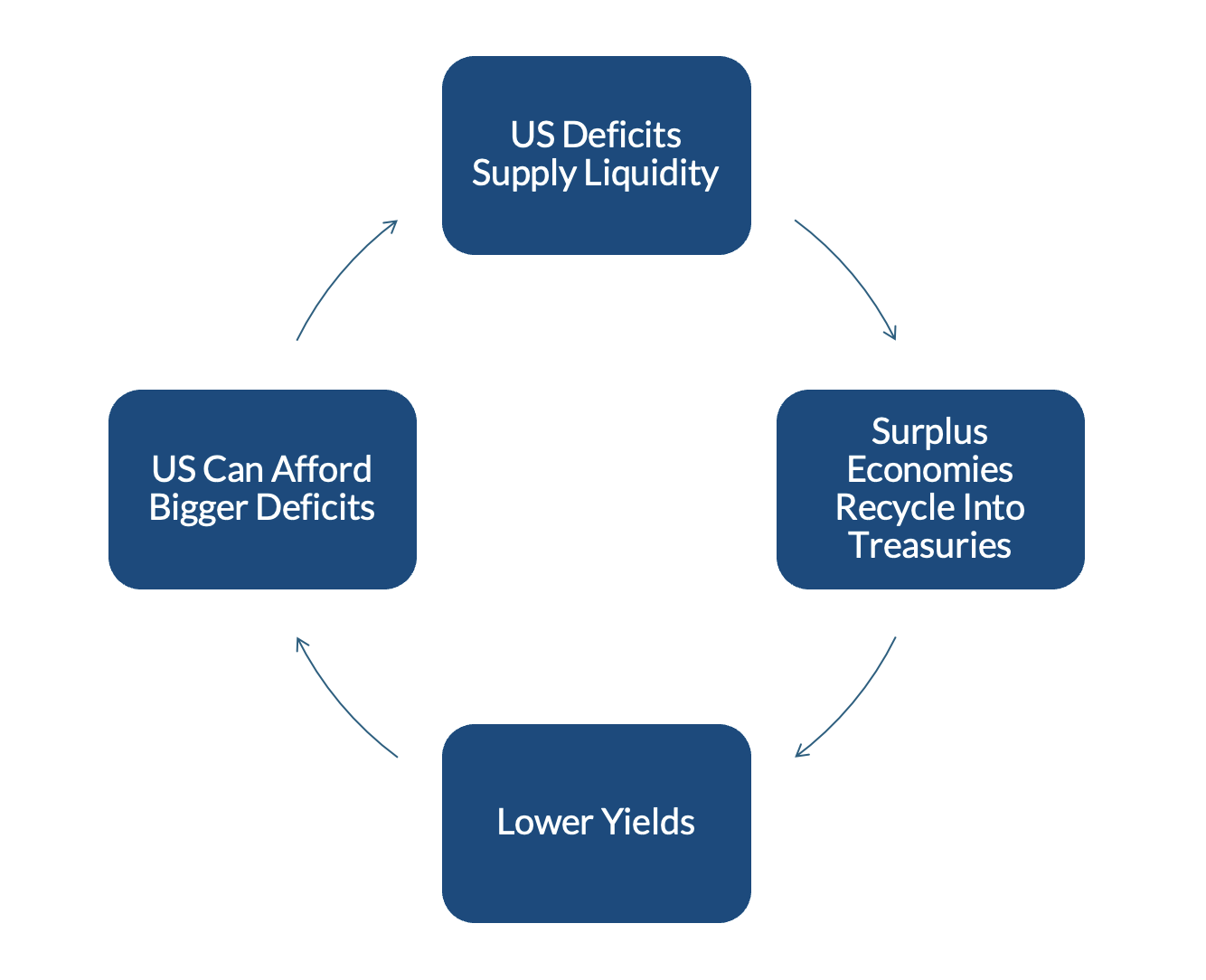

From the 1980s onwards, the dollar system entered a new phase. Persistent U.S. current-account deficits became a feature, not a bug: they supplied the world with the safe assets it demanded. Surplus economies recycled their savings into Treasuries, holding down yields. Low yields enabled more U.S. borrowing and spending, which in turn widened deficits. The feedback loop was self-reinforcing.

For surplus economies, this pattern became a development model. Japan in the 1980s ran large trade surpluses, funnelling its excess savings into Treasuries. The Plaza Accord drove a sharp yen appreciation but also triggered domestic credit expansion, culminating in the bubble and crash of the early 1990s. Emerging Asia took note. In the 1990s, under pressure from the Washington Consensus, many opened their capital accounts. When the Asian financial crisis hit, they rebuilt a different strategy: run persistent surpluses, keep currencies competitive, and accumulate large dollar reserves as insurance against sudden stops.

China amplified this logic. Its high-savings, investment-heavy model generated persistent surpluses, while capital controls and a managed renminbi held down exchange-rate pressures. The reserves that piled up were not the aim in themselves, but the by-product of a growth strategy built on exports and suppressed consumption. With few alternatives deep enough to absorb them, those surpluses were parked in Treasuries, binding China’s rise ever more tightly to the dollar system. Oil exporters in the 2000s followed a parallel path, recycling windfalls through sovereign wealth funds and central banks. In each case, the accumulation of U.S. assets flowed less from conscious preference than from the mechanics of their development models.

From the U.S. side, the arrangement was just as consequential. By absorbing foreign surpluses, Washington could finance widening fiscal and external deficits in its own currency. Foreign demand for Treasuries kept interest rates low even as borrowing swelled, sustaining consumption at home and liquidity abroad. But the other side of the bargain was risk: while surplus countries parked their savings in safe paper, U.S. households, firms, and financial intermediaries absorbed the credit and market risk made cheaper by foreign inflows. The result was a financial system that became larger, more leveraged, and more crisis-prone.

Après Le Déluge

The global financial crisis marked a turning point. The very surpluses that had sustained the system, from Chinese reserves to petrodollar inflows and Asian savings, turned out to be a double-edged sword. Their recycling into U.S. markets had kept yields low, but it also fuelled leverage and fragility inside the American system. When the crash came, demand for Treasuries paradoxically surged even higher. In a world short of safe assets, there was still no substitute for the dollar.

The 2010s then brought a new force: the shale revolution. By transforming the U.S. from a major energy importer into the world’s largest producer, it reduced America’s external vulnerability and softened the traditional link between oil prices and the dollar. Petrodollar recycling no longer worked as it once had. Instead of oil exporters alone funnelling surpluses into Treasuries, the U.S. itself became a net supplier of energy, reinforcing the dollar’s role through trade and pricing while diminishing reliance on external inflows from producers.

Reserve accumulation, meanwhile, slowed sharply after 2014. Central banks, once the automatic stabilisers of the system, stopped expanding their holdings at the pace required to match U.S. deficits. In their place, portfolio investors such as Taiwanese insurers, Japanese pension funds, and European asset managers became the marginal buyers of Treasuries.

Their motives are different: they are not compelled by reserve mandates but drawn by yield and the depth of U.S. markets. The “bid for dollars” now rests less on reserve status and more on perceptions of U.S. exceptionalism.

That shift has also exposed the dollar’s political dimension. The currency is not only the medium of global trade and finance, it is also a lever of U.S. power: access can be restricted and flows frozen when sanctions are imposed. China, scarred by the global financial crisis and wary of this weaponisation, has sought to diversify by internationalising the renminbi, building alternative payment systems, and accumulating gold. Russia and Iran, long subject to sanctions, accelerated their own shift into gold and alternative networks. Oil exporters, facing volatile revenues and political risk, have directed more of their surpluses through sovereign wealth funds with broader mandates. Across these cases, the lesson is the same: reliance on the dollar carries political as well as financial risk.

The dollar remains dominant in trade invoicing, reserves, and cross-border finance. But its role is no longer underwritten by passive flows from central banks. It now depends on a continuous stream of private capital inflows, sustained only as long as U.S. markets deliver superior returns.

It Has Been A Privilege

The pandemic was another test that the dollar passed with flying colours. Panic selling in March 2020 produced a global scramble for dollar liquidity, forcing the Fed to reopen swap lines and expand facilities on a scale not seen since 2008. Once again, the dollar’s indispensability was demonstrated in the breach: when everything else was being sold, Treasuries were the asset of last resort.

The aftermath brought a different challenge. Fiscal expansion and supply shocks pushed U.S. inflation to its highest level in four decades, and the Fed responded with the sharpest tightening cycle since Volcker. Higher yields pulled in foreign capital as U.S. growth outpaced the rest of the world. But the nature of those inflows underscored a shift. Where once the dollar’s strength rested on official reserves recycled into Treasuries, today it is driven by private investors pouring cash into U.S. assets, above all into the tech giants that dominate global equity benchmarks. American exceptionalism, in markets as much as in geopolitics, became the magnet for flows.

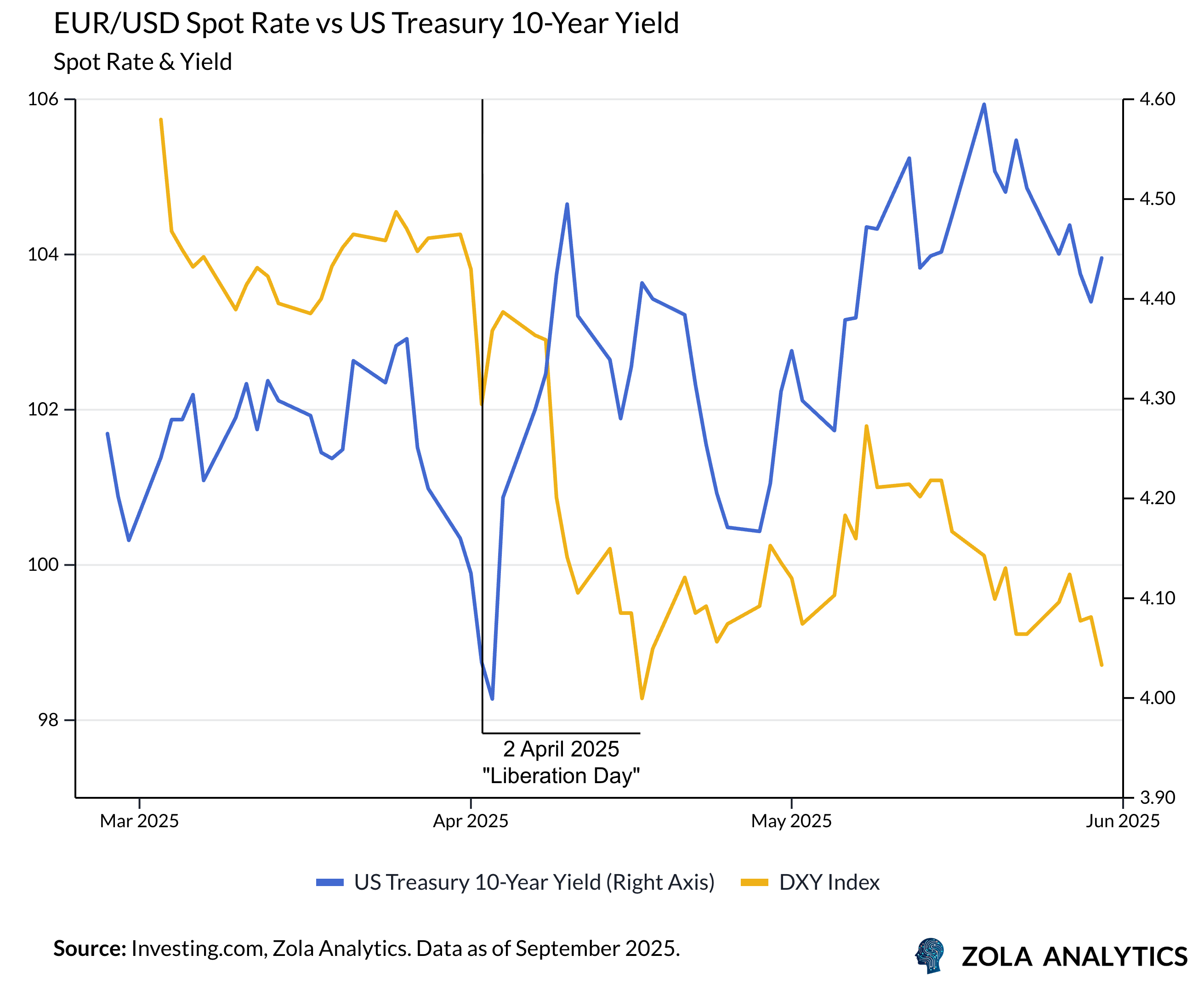

Since Trump’s return to the Oval Office, the contradictions in U.S. policy have grown sharper. Washington has pressed for tariffs and a weaker dollar to revive industry, yet monetary policy has had to stay tight to restrain inflation. In the past, such policies might have been absorbed by passive reserve inflows. Today, with flows increasingly shaped by private investors and surplus economies no longer compelled to park savings in Treasuries, markets react more quickly. Attempts to cheapen the dollar risk colliding with higher yields and volatile inflows. This is the fragility of the system: a currency still unrivalled in scale, but more exposed to shifts in sentiment than at any time since it rose to dominance.

In Spring 2025, following Trump’s threats of an aggressive trade policy, higher U.S. yields coincided with a softer dollar, a pattern more often associated with emerging markets than the issuer of the world’s reserve currency. That divergence captures the uncertainty of the moment. The real exorbitant privilege has never been simply the ability to borrow in one’s own currency, but to draw in global capital on favourable terms even as debt climbs. Half a century after Nixon declared the dollar unmoored from gold, the question is whether it can keep its crown without the same faith in U.S. stewardship.

Sign up to receive the Zola Global Macro Chartbook every week: https://www.zolaanalytics.com/insights?signUp