Published June 19th 2025

Fed Stuck in the Middle

The June FOMC meeting delivered no surprises, with the Fed opting to hold the lower bound of the Fed Funds rate steady at 4.25% for the fourth consecutive time. This pause, following 100bps of easing since September, underscores a strategic patience as policymakers navigate persistent uncertainties. Chair Powell emphasised that the current policy stance remains appropriate, with no urgency to shift course until the data provide a clearer signal.

SEP Signals: Growth Downgraded, Inflation Sticky

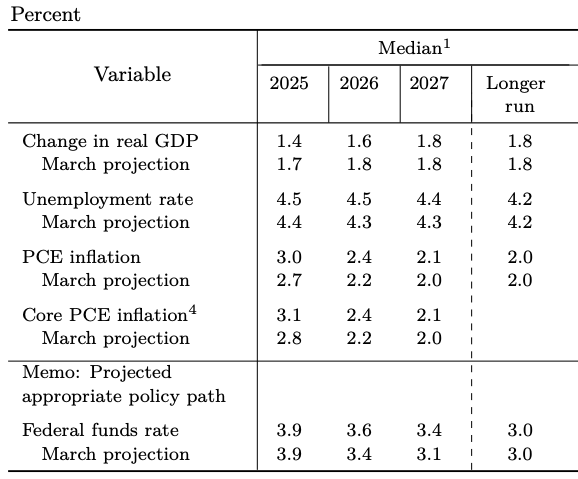

The Summary of Economic Projections (SEP) reaffirmed the median expectation of two rate cuts in 2025, keeping the end-year target rate at 3.875%. But the underlying revisions reflect a more cautious economic outlook:

Core PCE inflation was revised up to 3.1% (from 2.8% in March), suggesting persistent price pressures.

GDP growth was marked down to 1.4% for 2025, below long-run estimates, with downward revisions continuing into 2026.

Unemployment projections increased to 4.5%, above the longer-term equilibrium rate.

This combination of slowing growth, sticky inflation, and softening labor dynamics points to a Fed balancing between credibility on inflation and growing sensitivity to labor market risks. The projected rate cuts suggest the latter is gaining traction.

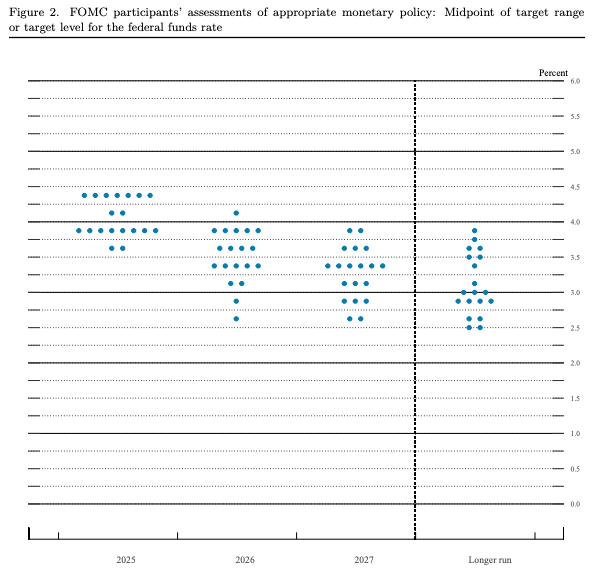

Dots Reveal Divided Committee

The dot plot distribution reveals a narrow consensus. Just one vote separates the current median projection from a more hawkish stance:

7 members see no cuts (up from 4 in March)

2 see one cut

8 see two cuts

2 expect three cuts

This signals a more hawkish tilt overall but preserves an easing bias, reflecting the committee’s willingness to support the labor market if downside risks materialise.

Trade Policy Adds to the Fog

Complicating the macro picture is the unresolved trade backdrop. The 90-day suspension of reciprocal tariffs tied to Liberation Day is set to expire on July 9. If no bilateral agreement is reached, tariffs could spike again, potentially de-anchoring inflation expectations and pressuring corporate margins.

Powell acknowledged that trade policy uncertainty limits the Fed’s visibility on the appropriate policy response. For now, the central bank appears content to remain reactive, not preemptive—especially given the limited data reflecting the full impact of recent tariff moves.

Inflation Compression Delayed, Not Defused

While headline inflation has been “well-behaved,” the composition of price pressures is evolving. Inventory drawdowns and margin compression have so far absorbed much of the cost increases. But restocking at higher input costs is likely to feed into consumer prices over the summer, setting the stage for more visible inflationary pressures. This delayed pass-through may complicate the inflation trajectory in Q3, especially if trade frictions worsen or commodity prices rebound.

Labor Slack Emerging Slowly

Despite higher unemployment projections, actual labor market data remains relatively steady. Firms appear reluctant to shed workers, likely reflecting both tight labor supply and macro uncertainty. The Fed appears to expect a gradual drift upward in unemployment, giving it space to act later rather than now.

Wait Until October

Given the prevailing mix of high inflation, slowing growth, and rising unemployment, the Fed seems comfortable waiting through the summer. Barring a sharp labor market deterioration or inflation surprise, the next policy shift may not come until October, with a possible 25bps cut. From there, a gradual cutting cycle could bring rates to 3.0% by mid-2026.

Disclaimer: Zola Analytics provides this material for informational and entertainment purposes only. It does not constitute investment advice.