Published June 17th 2025

Less Taper, Not Less Tight: Decoding the BoJ’s Mixed Signals

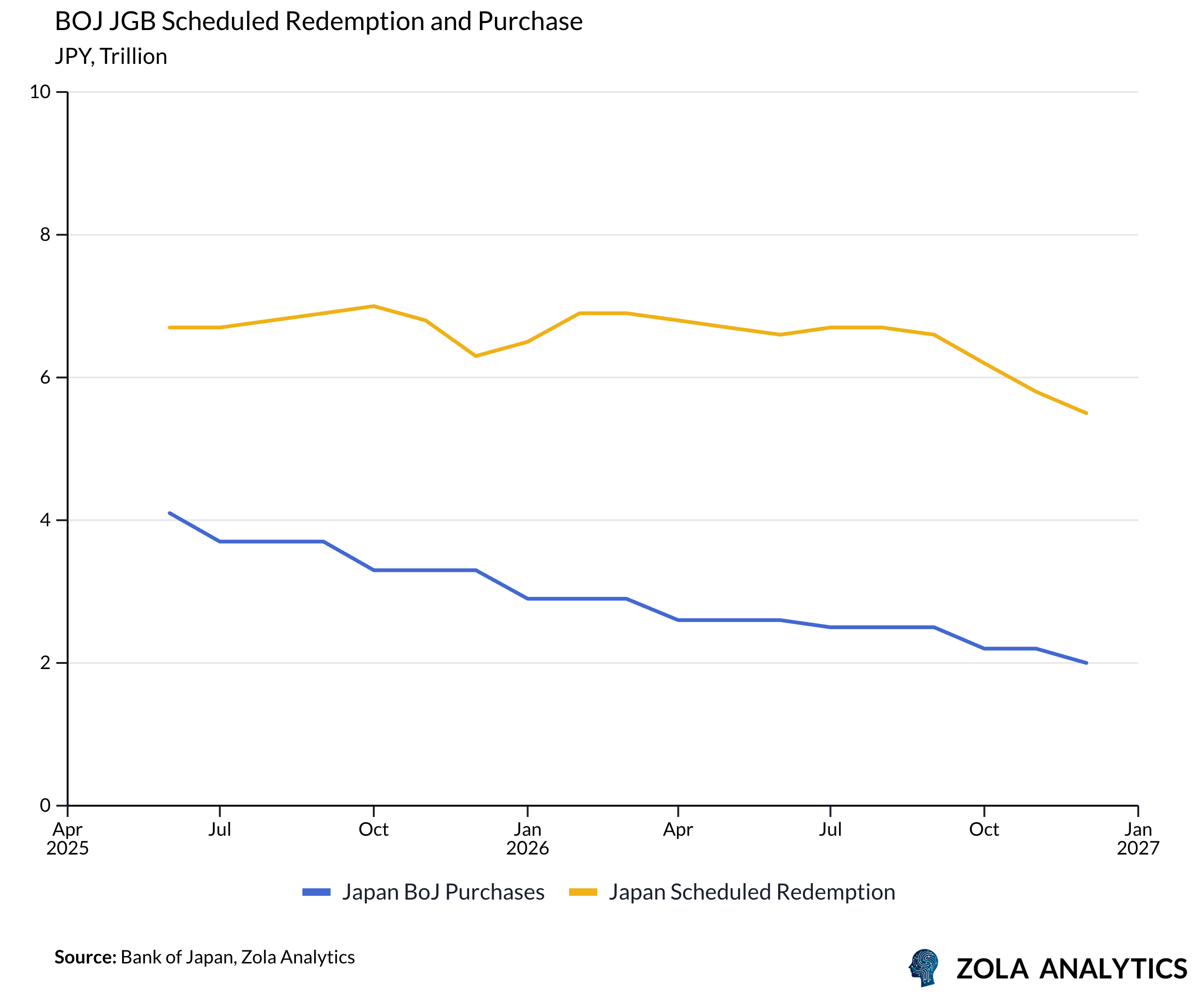

The Bank of Japan left its policy rate unchanged at 0.5% in the June Monetary Policy Meeting (MPM), maintaining its current stance while signalling a cautious, data-dependent path forward. The central bank will continue reducing its Japanese Government Bond (JGB) purchases by JPY 400 billion per quarter until March 2026, after which the pace will slow to JPY 200 billion per quarter. This measured deceleration reflects the BoJ’s desire to preserve market stability while slowly unwinding its balance sheet.

Despite holding steady, market participants were left parsing nuances. Governor Ueda emphasized that inflation expectations remain below target and reiterated concern over the impact of global trade tensions—particularly tariffs—on domestic investment and wage growth. These remarks reinforced the BoJ’s “wait-and-see” posture even as inflation remains elevated in parts of the economy.

QT Strategy: Slower, but Still Moving

While some observers read the slower tapering as dovish, others argue the BoJ’s Quantitative Tightening (QT) path is still accelerating in net terms. The central bank is set to reduce its JGB holdings by roughly JPY 33 trillion in 2025 and JPY 46 trillion in 2026, regardless of the gross pace of purchases. This distinction—between gross and net purchases—matters: it suggests the BoJ is pursuing QT more aggressively than headlines imply.

That said, a dissenting voice emerged. Board member Tamura opposed the slowdown, arguing for a more market-driven yield curve and warning that maintaining large-scale JGB purchases may hinder bond market functionality.

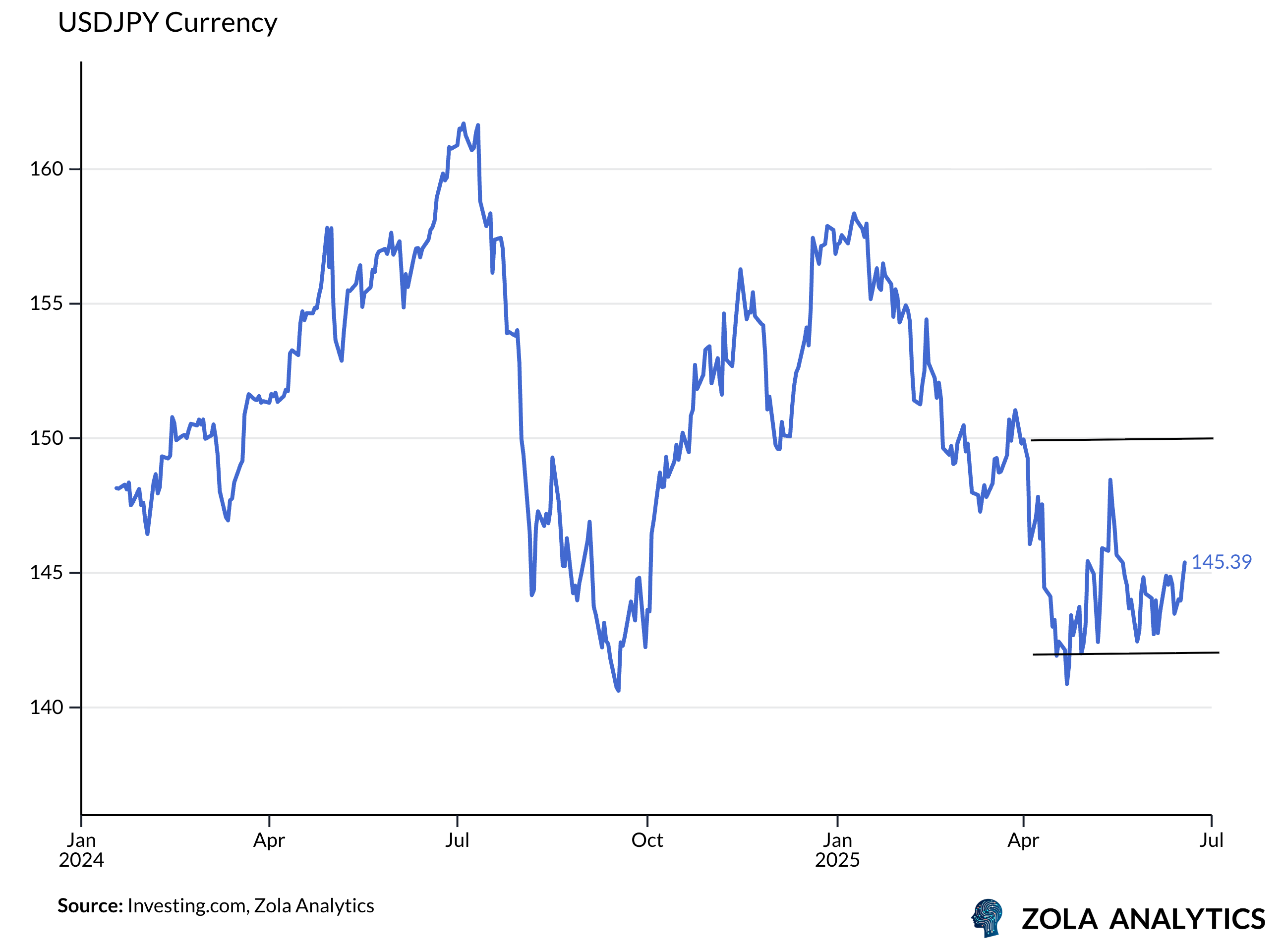

FX Implications: JPY Path Remains Mixed

From a currency market perspective, the BoJ’s measured tone contributed to a mixed outlook for the Japanese yen. The yen remains under pressure against the euro and other crosses despite recent weakness in the US dollar. Analysts see the USDJPY pair supported around USDJP 142, with potential rebounds toward USDJPY 150 in the near term, especially if oil prices remain elevated or if risk-on sentiment persists in global markets.

Broadly, the yen’s direction hinges less on BoJ decisions and more on broader macro drivers—US interest rate path, global equities, and energy prices. A sustained JPY recovery likely requires a shift toward risk aversion or a clear inflection point in BoJ tightening, neither of which are visible for now.

Inflation Risks Still Simmering

Inflationary pressures remain embedded in Japan’s economy. Earlier price shocks in food and energy have begun passing through to services and manufactured goods. Rents are also picking up, reinforcing underlying inflation dynamics. Still, the BoJ maintains that inflation expectations have yet to sustainably anchor at 2%, justifying its cautious approach.

Despite the subdued tone, some expect the July Outlook Report to revise inflation projections higher, potentially paving the way for a rate hike in Q4. But until inflation expectations become more entrenched and wage gains broader-based, the central bank appears reluctant to tighten aggressively.

Forward Guidance Still Elusive

The BoJ’s forward guidance remains deliberately vague. While underlying inflation has surprised to the upside, the lack of a clear signal on the rate path leaves markets speculating. With the next interim JGB purchase review scheduled for June 2026, and inflation assessments tied to volatile external factors like US tariffs and oil prices, the policy bias appears to lean hawkish in principle but dovish in execution.

Disclaimer: Zola Analytics provides this material for informational and entertainment purposes only. It does not constitute investment advice.