Published July 21st 2025

Gold’s Supercycle

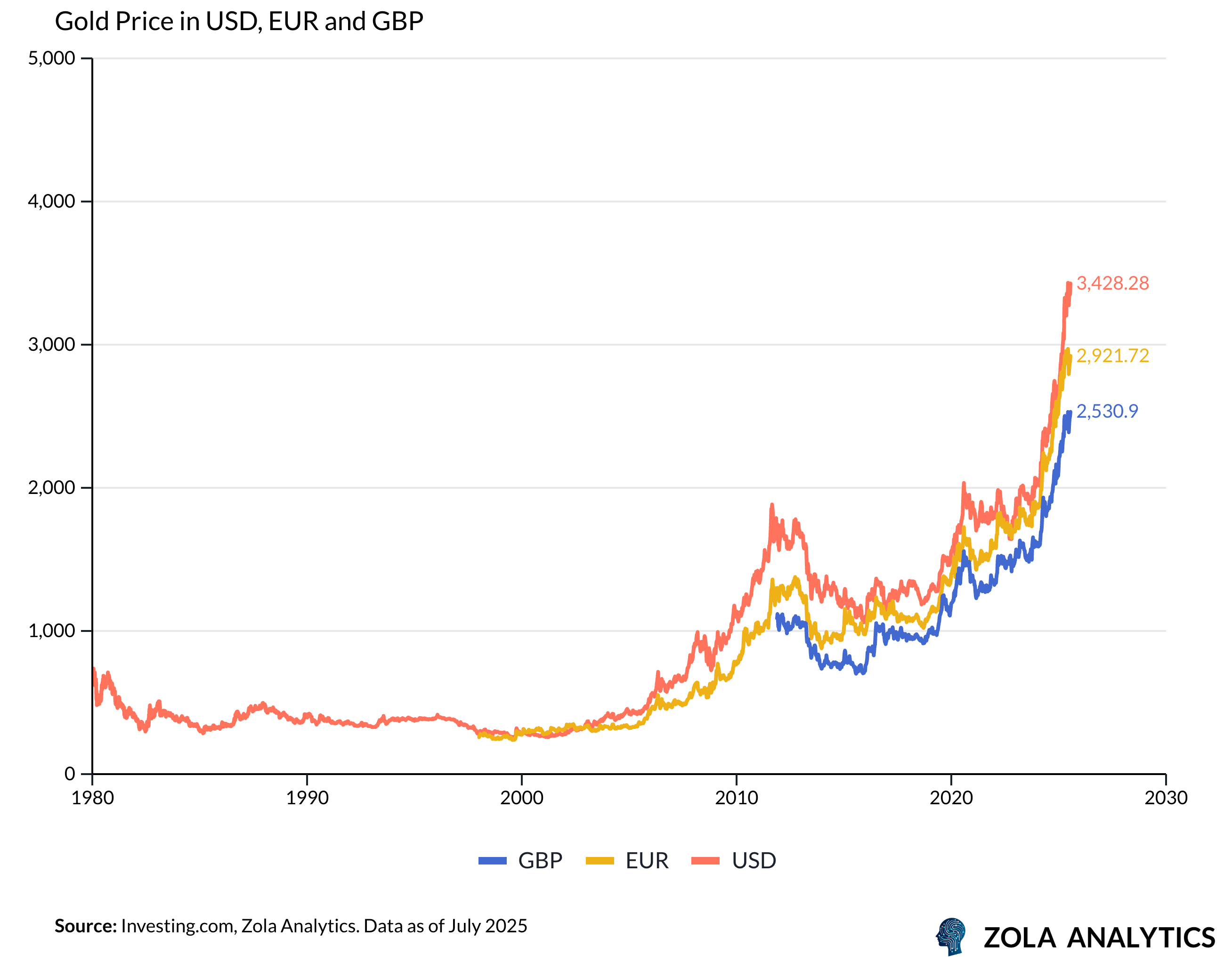

The gold market in 2025 stands at the confluence of powerful structural and cyclical forces, with prices hovering near all-time highs and forecasts eyeing the elusive USD 4,000 per ounce mark. Behind the glitter is a deeply rooted shift in how investors and central banks perceive risk, shaped by geopolitical tensions, fiscal strains, and evolving dynamics in the global financial system. At the heart of this transformation lies a powerful trifecta of structural drivers: persistently high central bank accumulation, accelerating de-dollarisation reshaping global reserves, and rising concerns about fiscal instability that erode confidence in fiat currencies. Together, these forces are propelling gold into a new era of sustained strength.

A New Bull Market Rooted in Structural Shifts

Central Banks Drive Unprecedented Demand

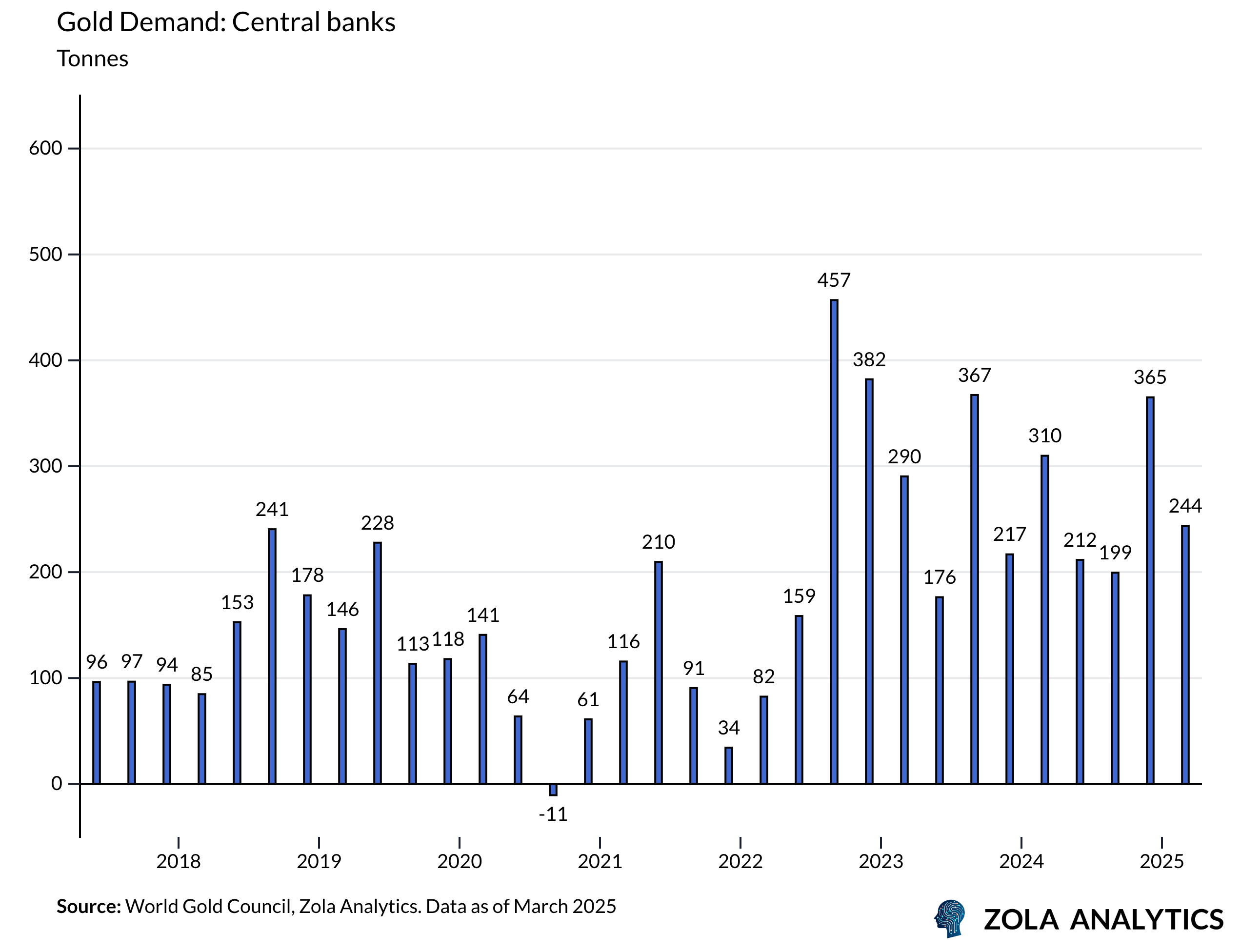

Since 2022, central bank demand for gold has surged to levels unseen since Bretton Woods, with net purchases averaging 1,000 tonnes in 2025 alone — roughly double the historical average of ~450 tonnes recorded from 2017 through early 2022. This surge began in earnest following the Russian asset freeze, which sparked a structural re-evaluation of gold’s role as a reserve asset. Annual central bank purchases have consistently topped 1,000 tonnes since then, moderating only slightly this year while remaining historically elevated.

A key driver of this persistent demand has been the increasingly multipolar geopolitical order and heightened sanctions risks, which have prompted central banks to diversify reserves beyond the US dollar. The dollar’s share of global FX reserves has declined markedly over the past two decades, falling from nearly 73% in 2001 to approximately 57% by the end of 2024 — a structural shift reflecting efforts to reduce reliance on the dollar.

At the same time, gold’s rising share of global reserves demonstrates the search for assets insulated from geopolitical pressures. By the end of 2024, gold had overtaken the euro as the second-largest component of global central bank reserves, accounting for 19% of total reserves at market prices, compared to the euro’s 16%, while the dollar continued its steady decline to 46%.

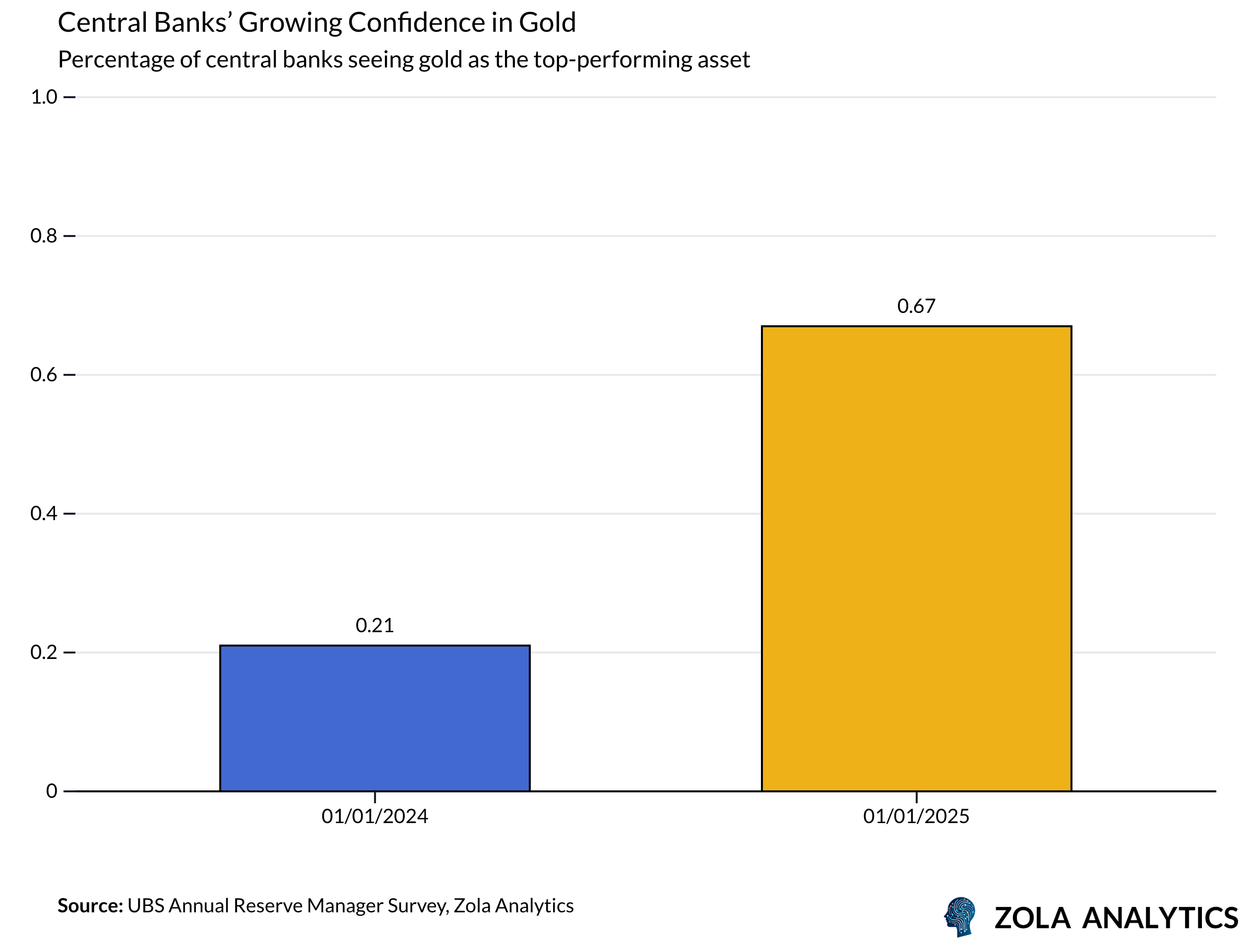

This structural shift has been matched by a marked change in sentiment: a recent UBS survey of nearly 40 central banks found that nearly half now see the “weaponisation” of FX reserves as a major investment risk — up sharply from previous years — with 52% planning to increase their gold holdings over the next year to hedge against these risks.

China’s Silent Shift: PBoC’s Gold Strategy

China’s evolving FX reserve strategy further underscores the structural forces driving gold’s ascent. While the country still holds approximately USD 3.3 trillion in foreign reserves — the world’s largest — the People’s Bank of China (PBoC) has become acutely aware of the geopolitical risks tied to a USD-dominated system. Recent statements from Governor Pan have repeatedly highlighted the vulnerabilities of relying heavily on US dollar assets, citing the increasing risk of financial sanctions and the weaponisation of payment systems. Despite maintaining adequate reserve levels to manage short-term liquidity, the PBoC’s capacity to reduce dollar exposure quickly is constrained by limited domestic credit demand. This reality has made diversification into gold an essential component of China’s reserve management strategy, as it seeks assets that can insulate its financial system from external shocks without destabilising its currency or money supply. The opaque but steady accumulation of gold, coupled with discreet adjustments in the composition of FX holdings, reflects Beijing’s commitment to safeguarding reserves while quietly rebalancing away from dollar dependence.

Undeclared Buying & Hidden Flows

Beyond central banks’ declared purchases, a significant portion of global gold demand stems from “undeclared” official buying — in practice, central banks accumulating gold through opaque channels that delay or obscure reporting. China’s accumulation strategy epitomises this trend: despite official data showing gold at under 7% of declared reserves, estimates suggest its true holdings could exceed 5,000 tonnes, highlighting a deliberate approach to quietly shift away from dollar assets without roiling markets. Discreet purchases on international exchanges and understated customs flows have widened the gap between reported and real reserve levels.

Fiscal Disorder: Gold’s Historical Catalyst Reemerges

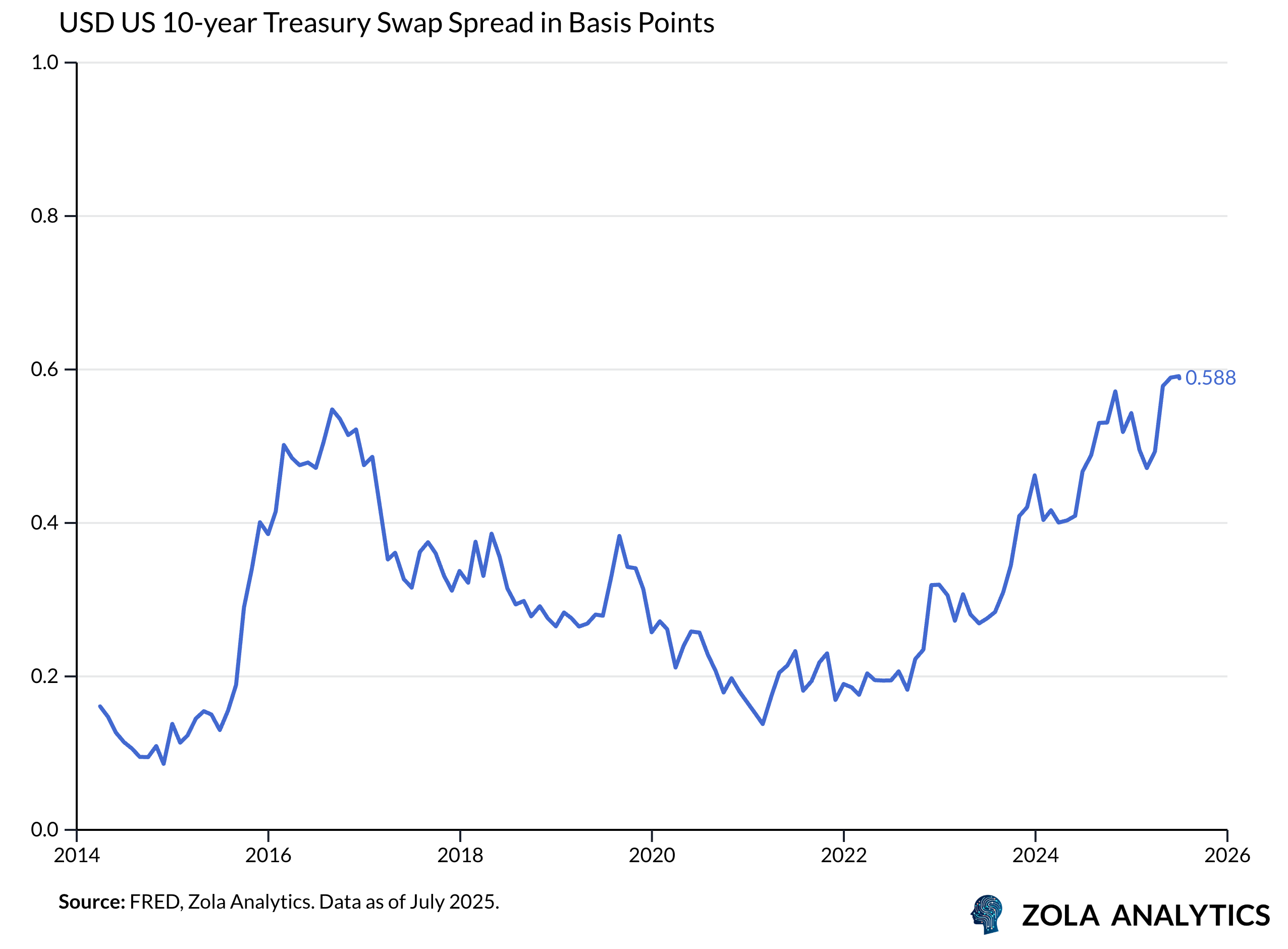

Echoing patterns from the 1970s and 2000s, ballooning deficits have reasserted their role as a key driver for gold. Massive fiscal packages — such as the so-called “Big Beautiful Bill” — are projected to add nearly USD 3 trillion to US deficits over the next decade. This stokes concerns about debt sustainability and fuels fears of future debasement of fiat currencies. These fiscal strains have weakened confidence in US debt markets, with foreign investors showing a diminishing appetite for Treasuries. This trend is reflected in widening US swap spreads — the difference between Treasury yields and interest rate swap rates — which signal rising fears over the US government’s creditworthiness. Historically, widening swap spreads have correlated with periods of fiscal concern and have often coincided with gold price rallies as investors seek safe-haven assets.

Concurrently, the ongoing global reallocation away from the dollar has reinforced a structural bear market in the greenback, creating a tailwind for gold. Even as real yields have risen, gold’s apparent decoupling from traditional valuation anchors since 2022 highlights how central bank and strategic investor buying have overwhelmed conventional pricing relationships, establishing a new paradigm in which gold can strengthen alongside positive real rates.

A Historical Constant in Times of Change

History shows that during periods of fiscal expansion, geopolitical upheaval, and eroding confidence in fiat stability, gold tends to shine brightest. Today’s environment exemplifies this reality. The trifecta of central bank accumulation, de-dollarisation, and fiscal instability is creating powerful, persistent tailwinds for gold’s ascent.

Moreover, the freezing of Russia’s foreign reserves in 2022 has set a precedent that shifted the calculus for many emerging market reserve managers. Countries aligned geopolitically with China and Russia have sharply increased their gold allocations since late 2021, seeking insulation from sanctions risks and over-dependence on Western financial systems. Even as real yields rose globally, this fear of financial isolation has driven a surge in gold demand — underscoring how deeply geopolitical shifts now anchor gold’s rally.

Yet there are limits to every rally. Recent geopolitical escalations have failed to push gold beyond its April highs, suggesting that even greater shocks may now be required for significant new advances. Still, the underlying direction appears set. Investors seeking protection from fiscal instability, geopolitical volatility, and persistent uncertainty should recognise that gold’s historic role as a store of value has rarely looked more relevant — or more essential.