Published 21st October 2025

4 minute read

Siesta or Fiesta?

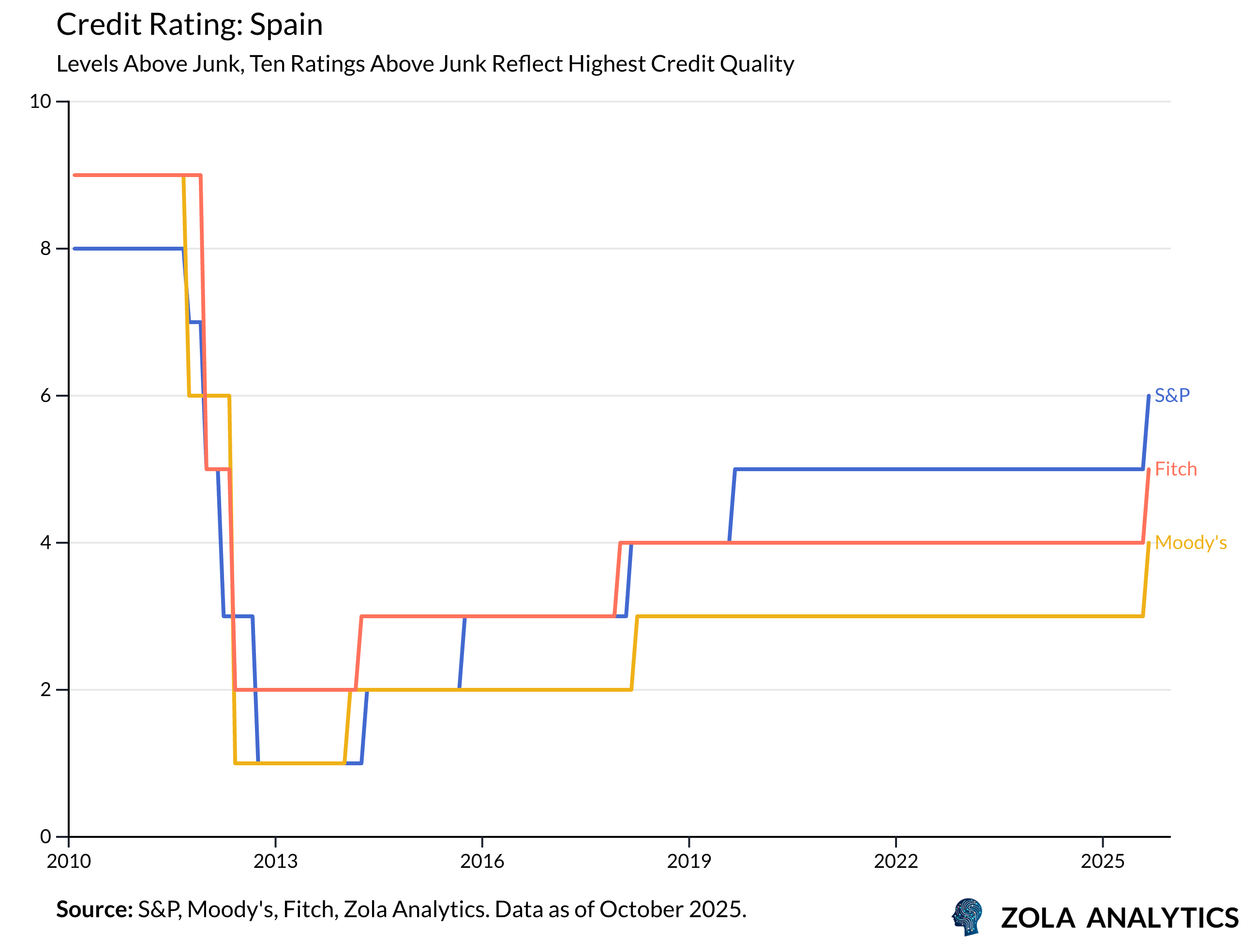

Two Spain’s credit story has been one of quiet repair. After deep downgrades during the sovereign debt crisis, ratings have climbed steadily since 2014. The latest upgrades by S&P, Moody’s, and Fitch confirm stronger fiscal discipline and lower volatility. Yields have narrowed, maturities have lengthened, and investors once again price Spain as a near-core borrower.

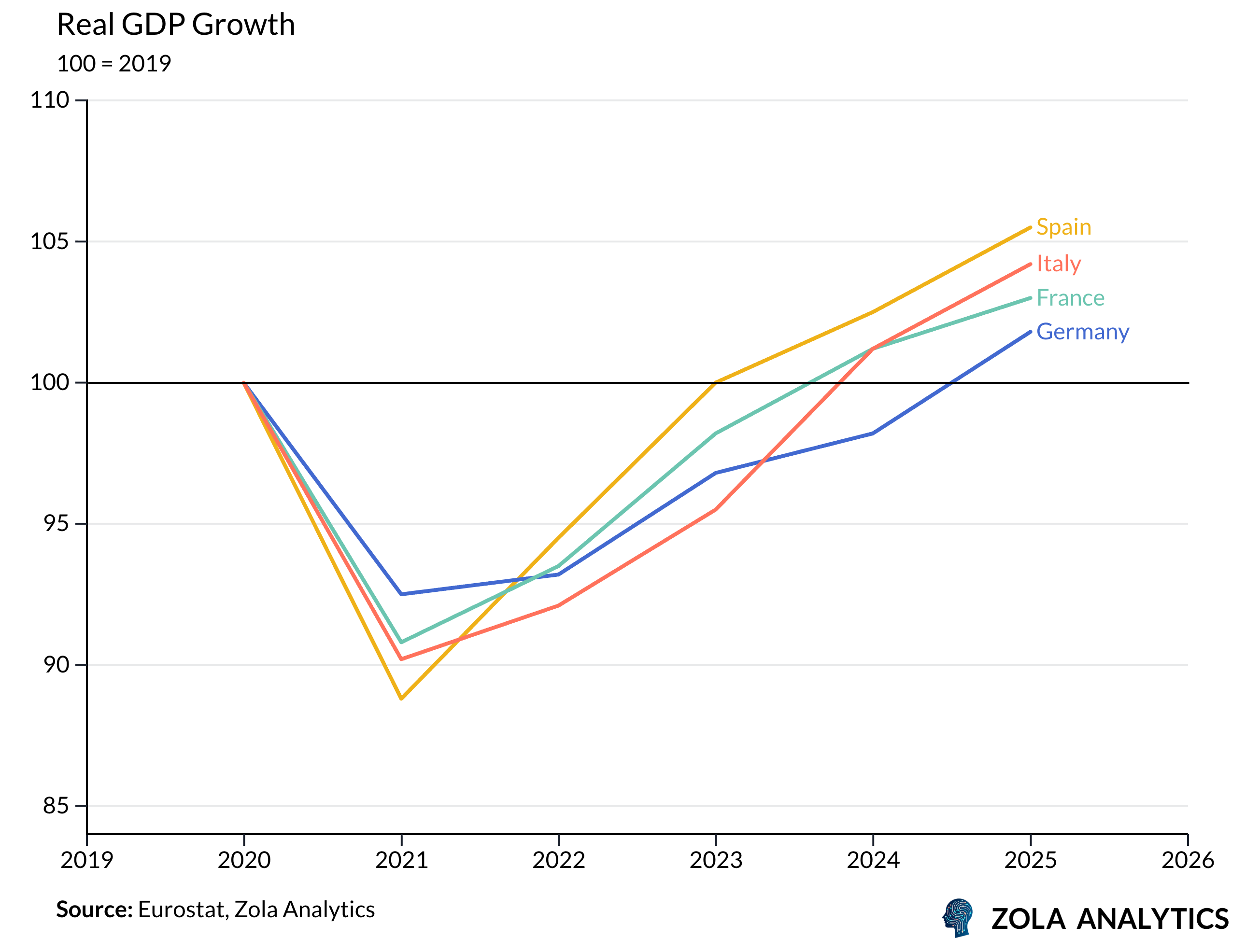

Behind that renewed confidence lies real performance. Since 2020, Spain has outpaced every major Eurozone economy. Real GDP now stands over 6% above its pre-pandemic level, compared with 5% in Italy, 4% in France, and 2% in Germany. Services, tourism, and public investment have all contributed, producing growth that is not only strong but broad. Yet breadth does not guarantee depth — and the composition of growth matters more than the headline rate.

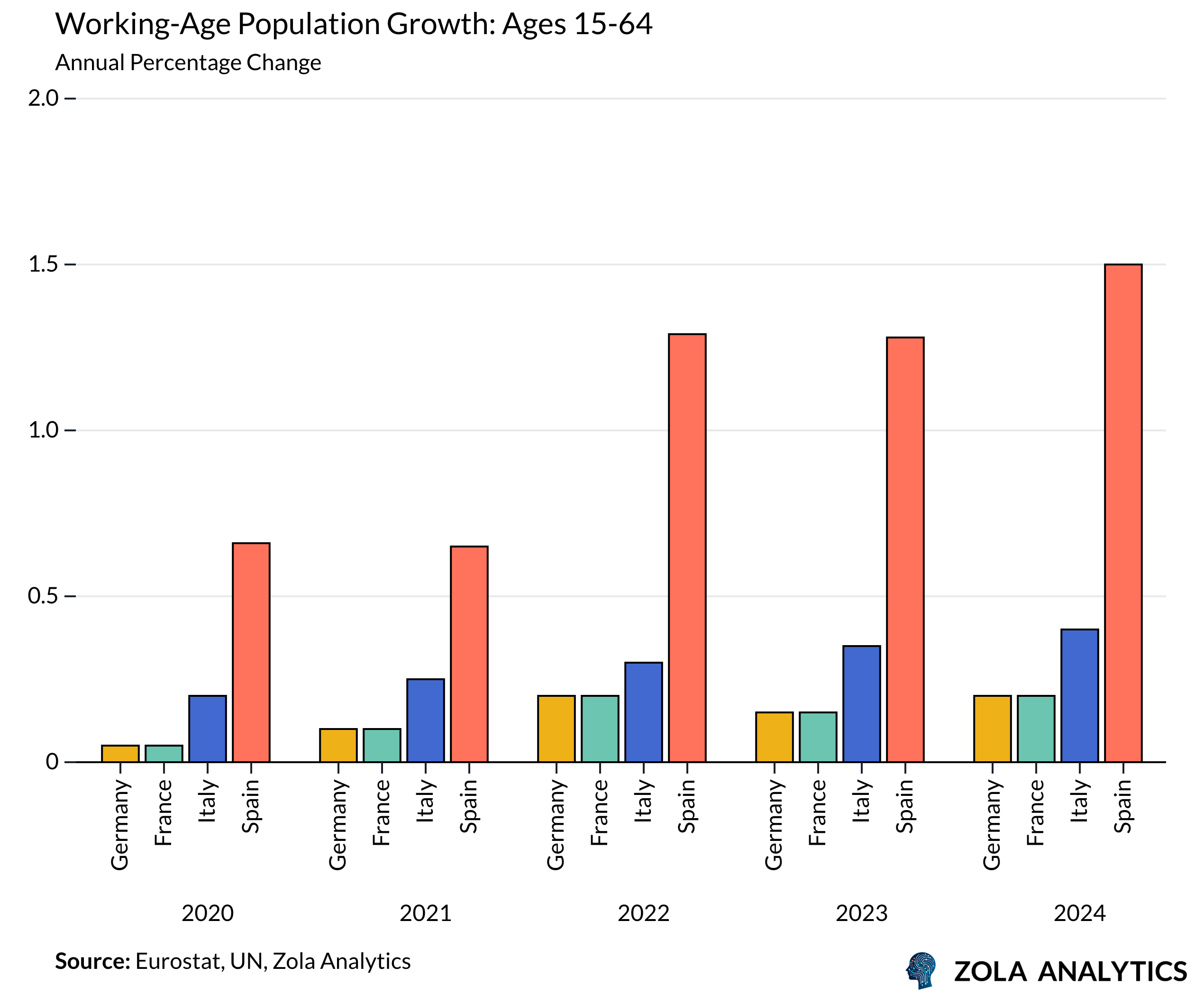

Demographics explain much of the surprise. Spain is the only large Eurozone country where the working-age population has expanded meaningfully since 2020. Immigration has added more than one million people of working age, reversing a decade of decline. The inflows have filled vacancies, lifted consumption, and eased post-pandemic labour shortages. The labour market, long a constraint, has become a driver of expansion.

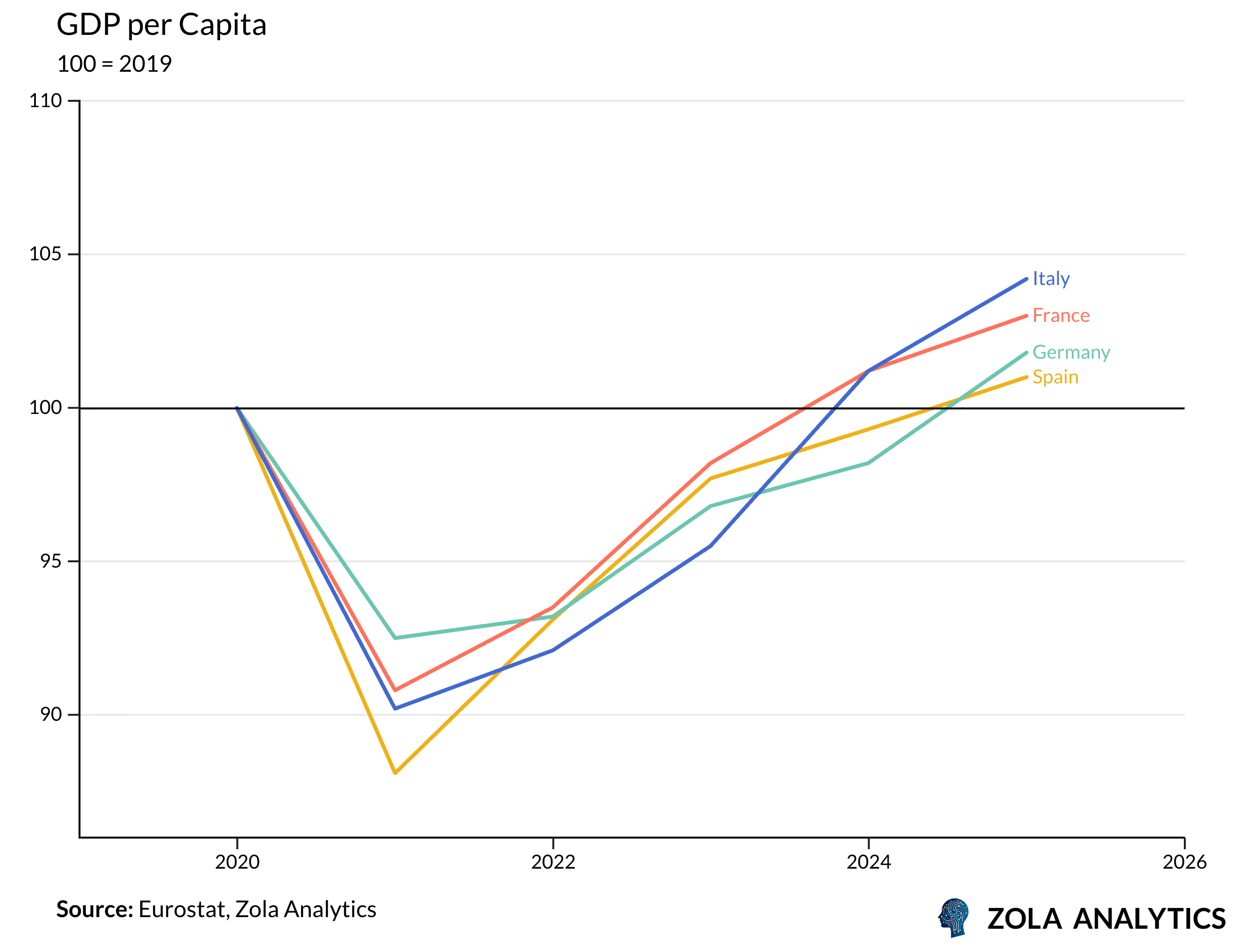

But when output is spread across a larger population, prosperity per head looks thinner. Real GDP per capita has barely risen since 2019, trailing Italy and France. Growth has been extensive, not intensive — built on labour supply, not productivity. The recovery has relied on more workers rather than better work. In the long run, that imbalance constrains how far incomes can rise.

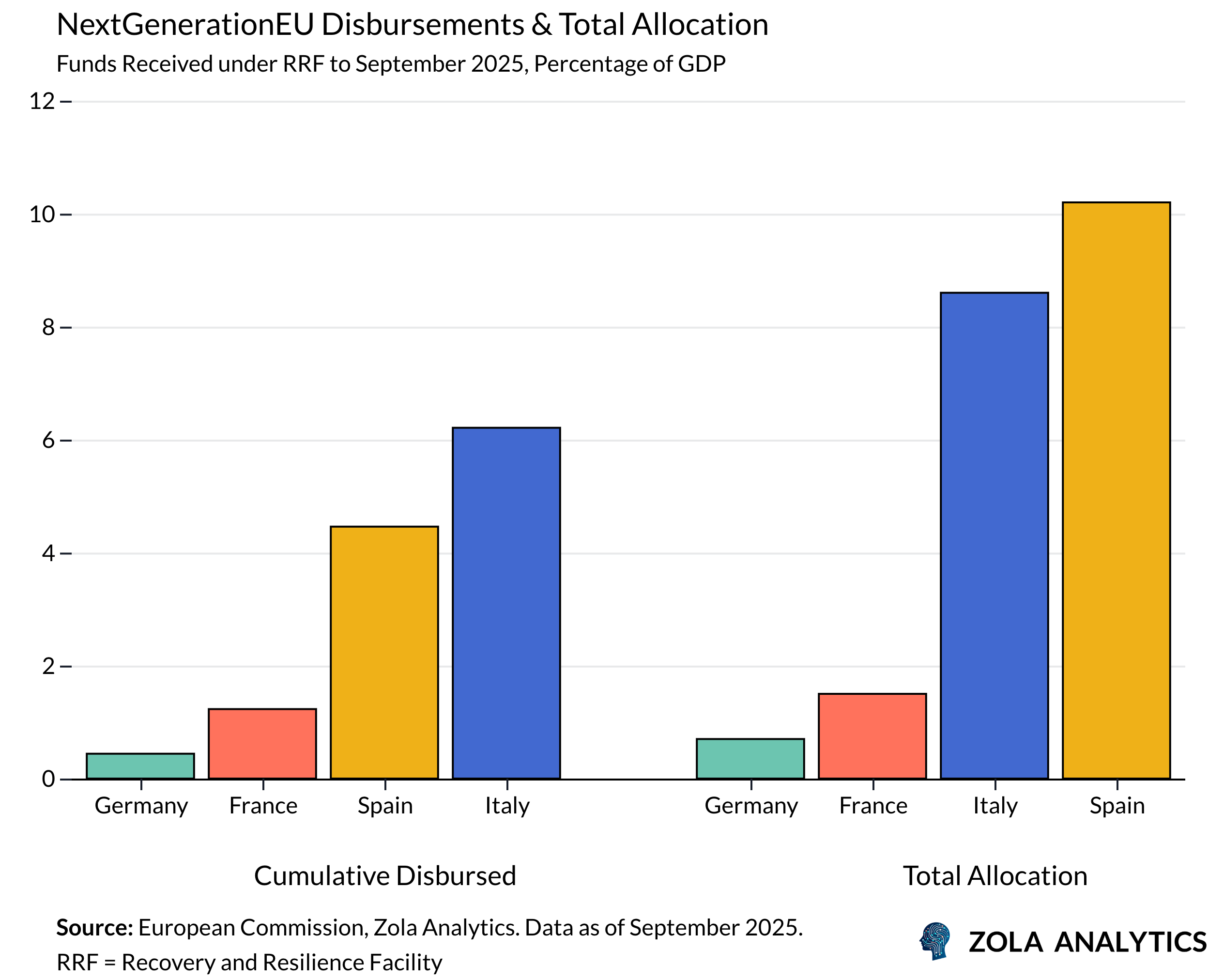

Fiscal policy has amplified the cycle. Spain is among the largest beneficiaries of the EU’s Recovery and Resilience Facility (RRF), the fiscal core of NextGenerationEU. By September 2025, disbursements exceeded 4.5% of GDP, with total allocations above 10%. The inflows have supported investment in green and digital infrastructure, accelerated consumption, and softened post-pandemic volatility. They have also insulated public finances, masking the absence of deeper reform.

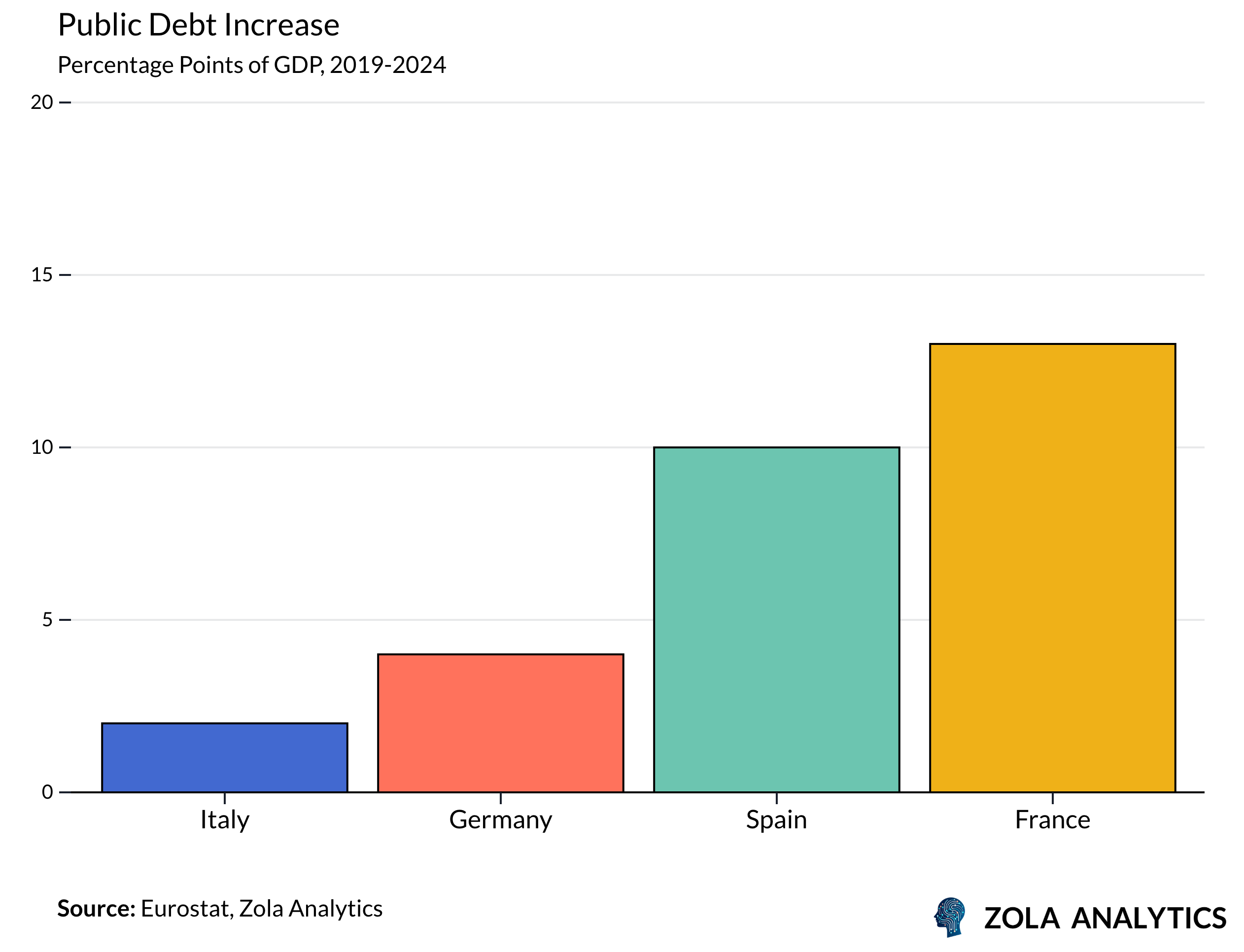

This combination of demographic and fiscal tailwinds has provided both stimulus and cushion, but also dependence. Between 2019 and 2024, Spain’s debt ratio rose by about 10 percentage points of GDP. Cheaper financing has kept it manageable, but fiscal space remains narrow. Even during an expansion, consolidation has been deferred.

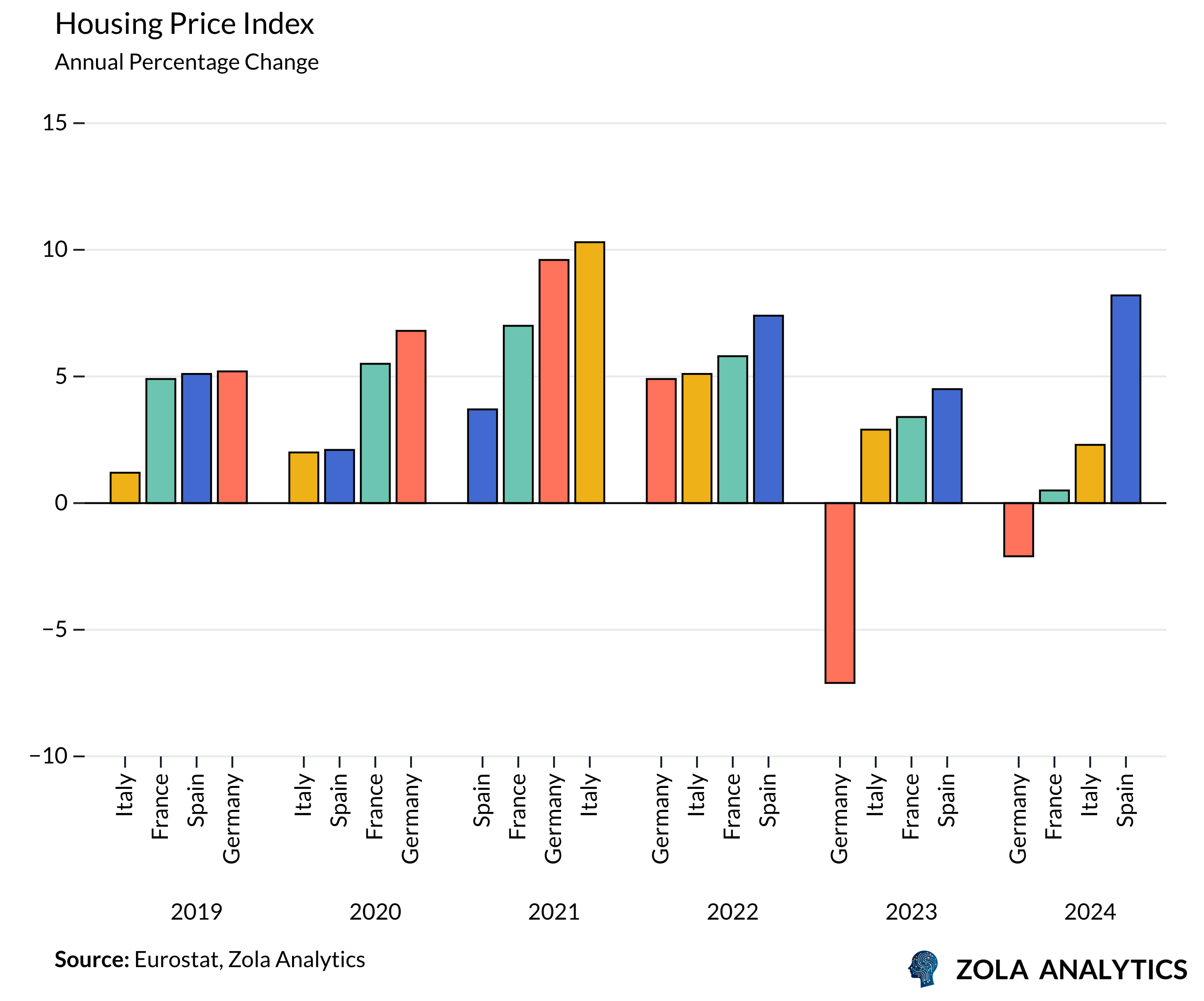

Nowhere are the pressures clearer than in housing. Population inflows and stimulus-fuelled demand have collided with constrained supply. Construction remains limited, and completions well below pre-crisis levels. Prices rose sharply through 2022 and 2024, even as property markets cooled elsewhere in Europe. In cities such as Madrid and Barcelona, rent burdens have reached record highs, fuelling social tension and political unease. The same forces driving growth are also deepening inequality.

Spain’s renewed credibility rests on macro stability, a favourable demographic tide, and extraordinary EU fiscal inflows. Together they have rebuilt confidence and lifted output. Yet the recovery’s foundations remain uneven, dependent on people and public spending, not productivity or technological depth.

The test will come when external support fades and the demographic tide slows. Unless Spain can convert today’s momentum into genuine productivity gains and fiscal resilience, the next phase may reveal how much of this expansion was cyclical rather than structural. The fiesta is real, but the rhythm is borrowed, and the encore uncertain.

Sign up to receive the Zola Global Macro Chartbook every week: https://www.zolaanalytics.com/insights?signUp

Disclaimer: Zola Analytics provides this material for informational and entertainment purposes only. It does not constitute investment advice.