Published March 13th 2026

7 minute read

Treat the Root, Not the Branch

There is a saying in traditional Chinese medicine, “treating the branch, not the root”, that cautions against remedies that address symptoms whilst leaving underlying causes untouched. Chinese policymakers would do well to heed the wisdom in this warning.

The root of China’s problems is weak household demand. Yet the growth model that fostered China’s imbalances remains in place. Subsidies, credit and misaligned incentives continue to expand industrial capacity even as demand falters.

Stressed property markets, indebted local governments, and overcapacity are all symptoms of this deeper imbalance. China watchers have long asked whether Beijing will keep pruning the branches or summon the will to treat the root.

Anatomy of an Imbalance

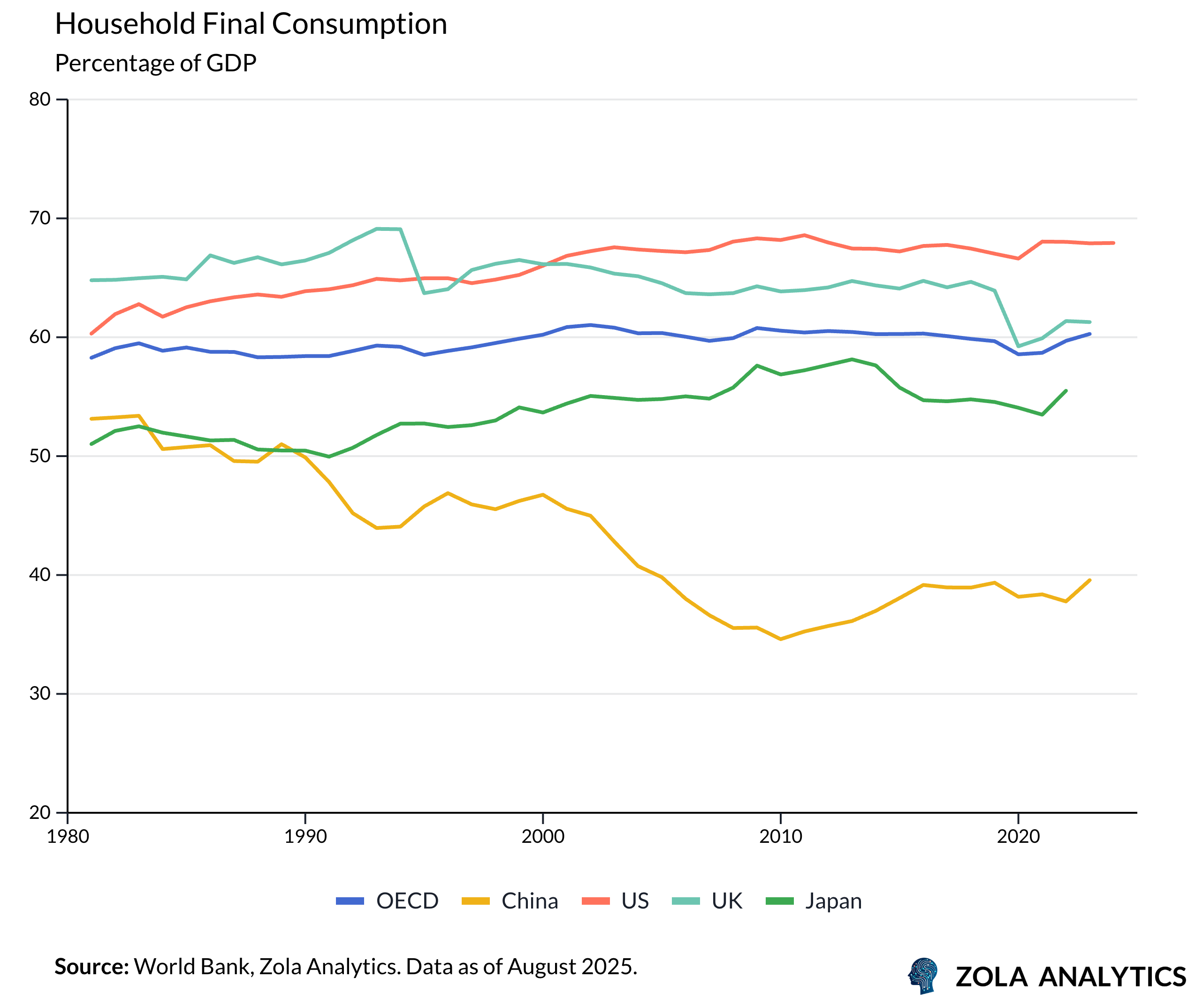

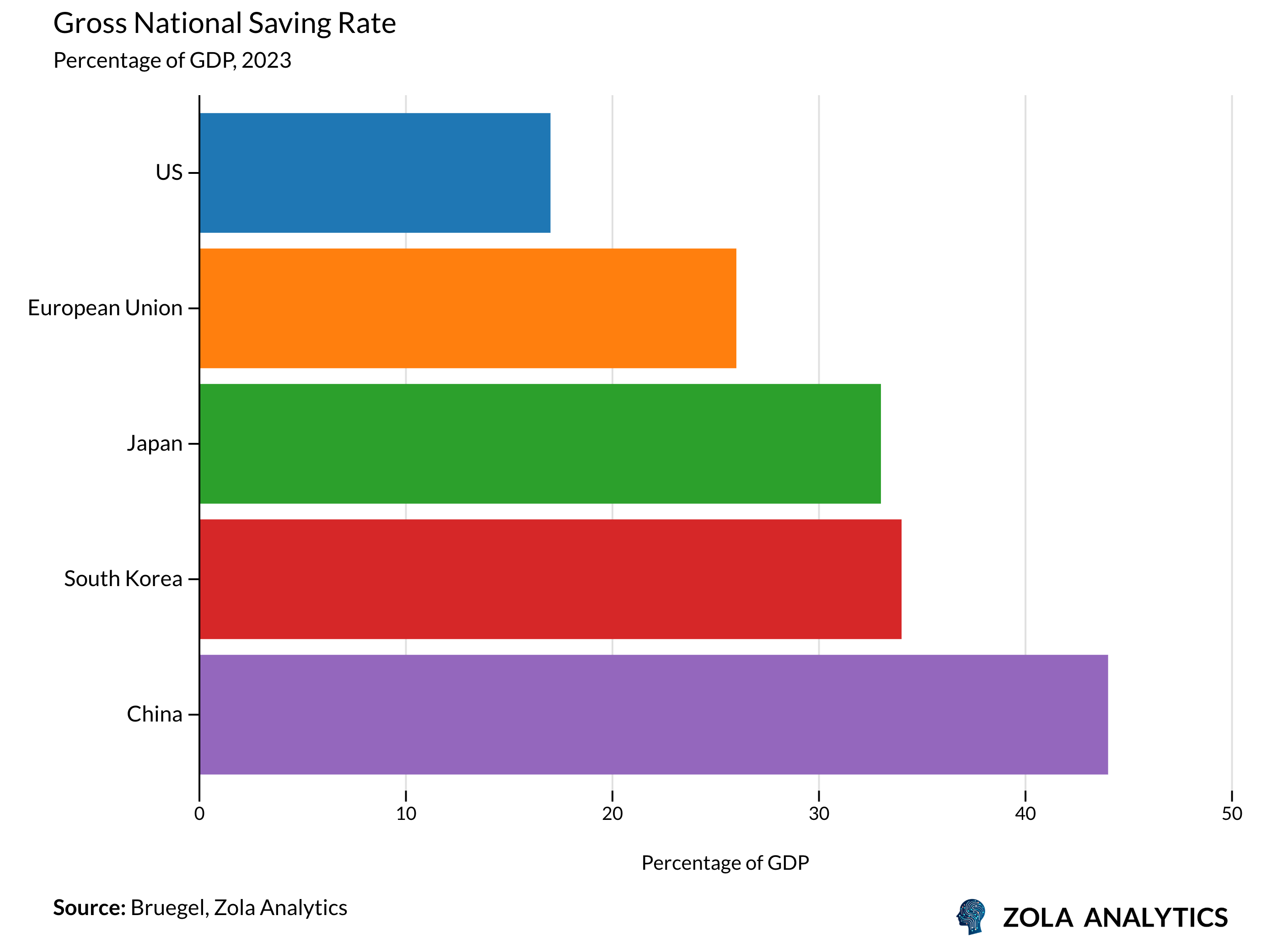

China’s economy faces a convergence of structural pressures, each reinforcing the others. At the heart of China’s imbalances lies weak household demand. Despite rising incomes, consumption remains an unusually small share of GDP compared with other major economies. High precautionary savings, driven by limited social safety nets, continue to hold back spending.

Once a driver of economic strength, a weak property market now compounds China’s problems. Falling home sales and prices have eroded household wealth, whilst local government financing vehicles, long reliant on land sales, are heavily indebted. The impact on balance sheets has curtailed both public investment and private confidence.

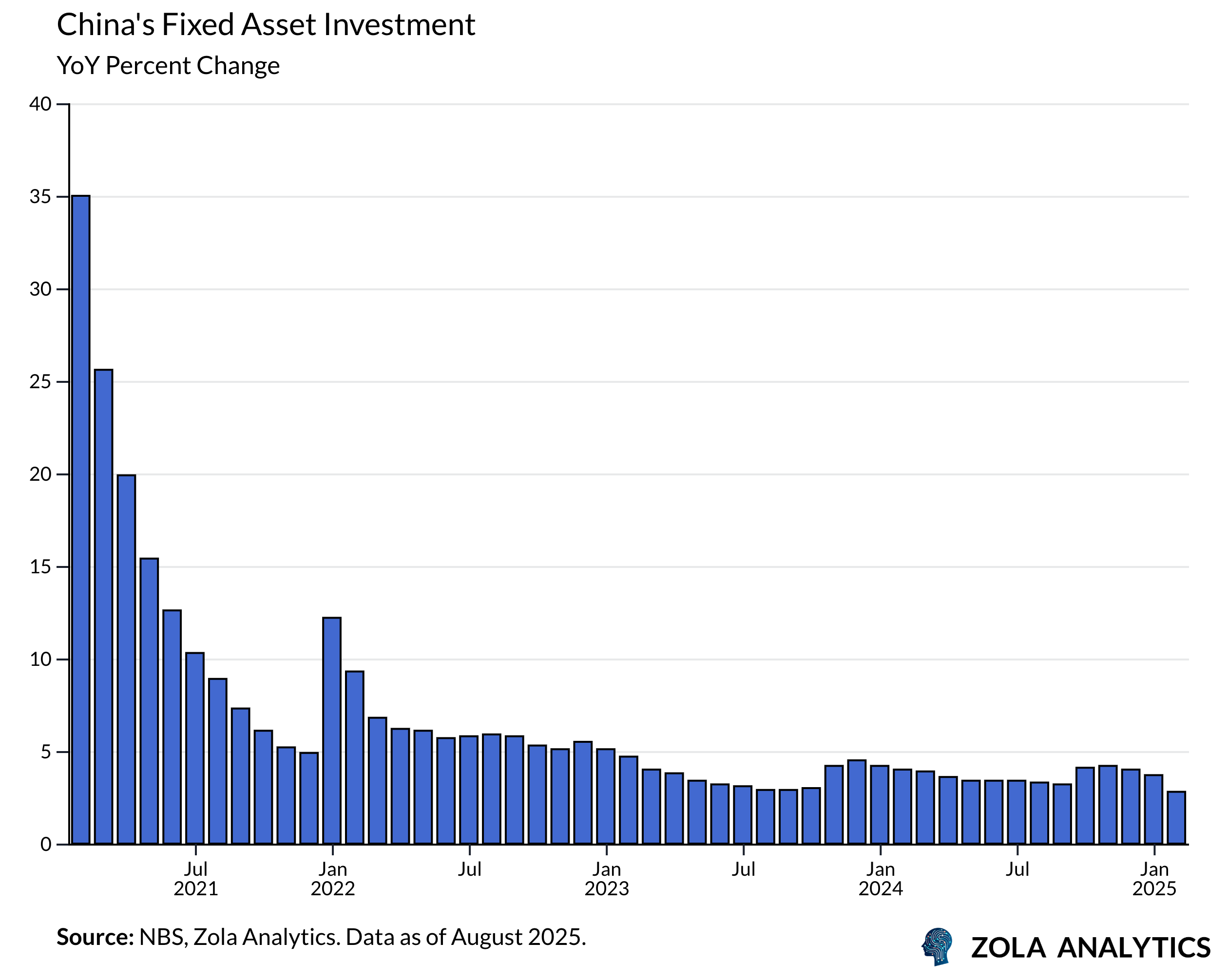

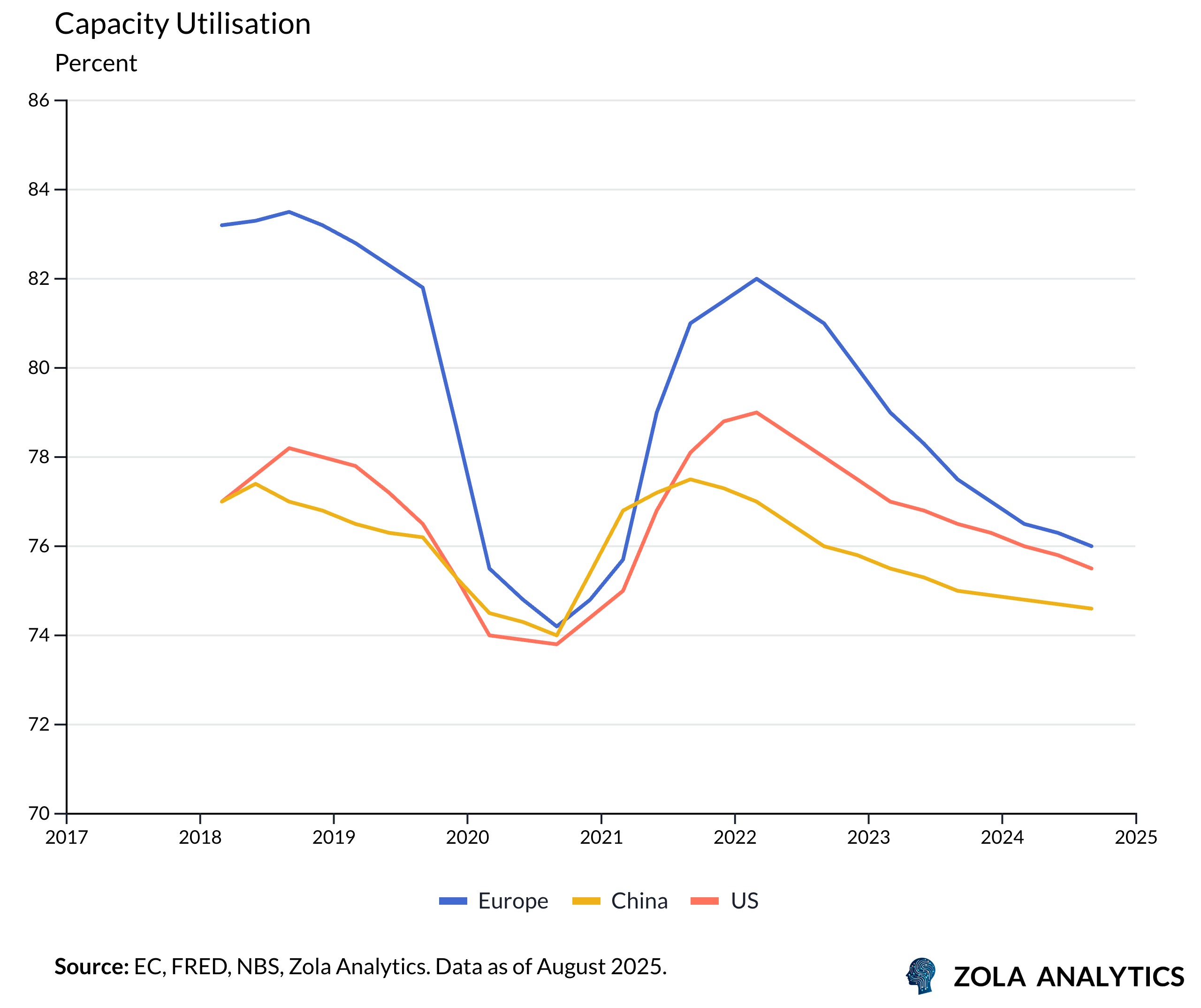

Long reliant on government stimulus and external demand, Chinese industry now suffers from chronic overcapacity. Falling prices leave firms struggling to cover costs, with little incentive to invest. Whilst other countries have also experienced declining capacity utilisation in recent years, China’s decline has occurred in an environment of gargantuan subsidies and rapid credit expansion.

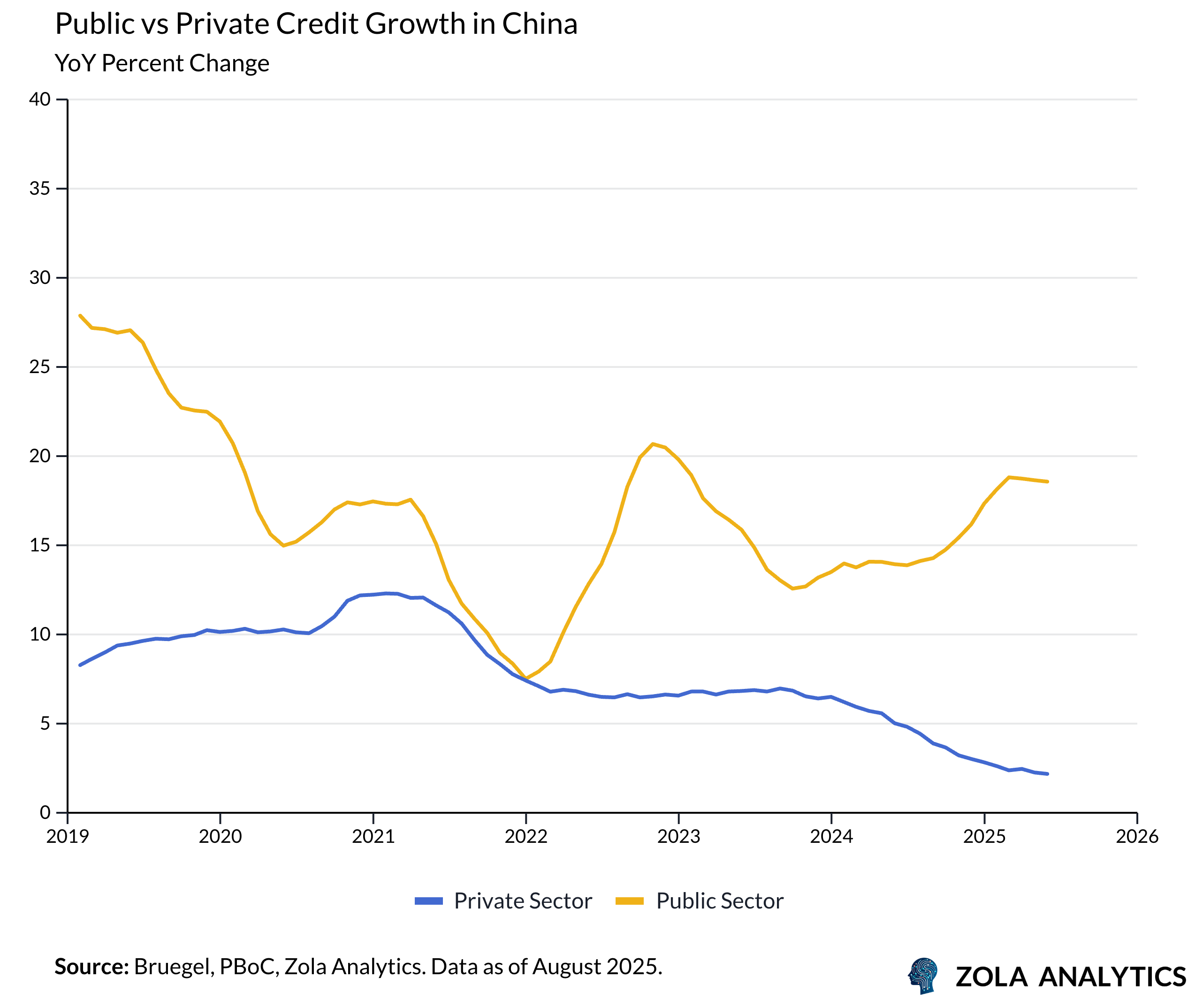

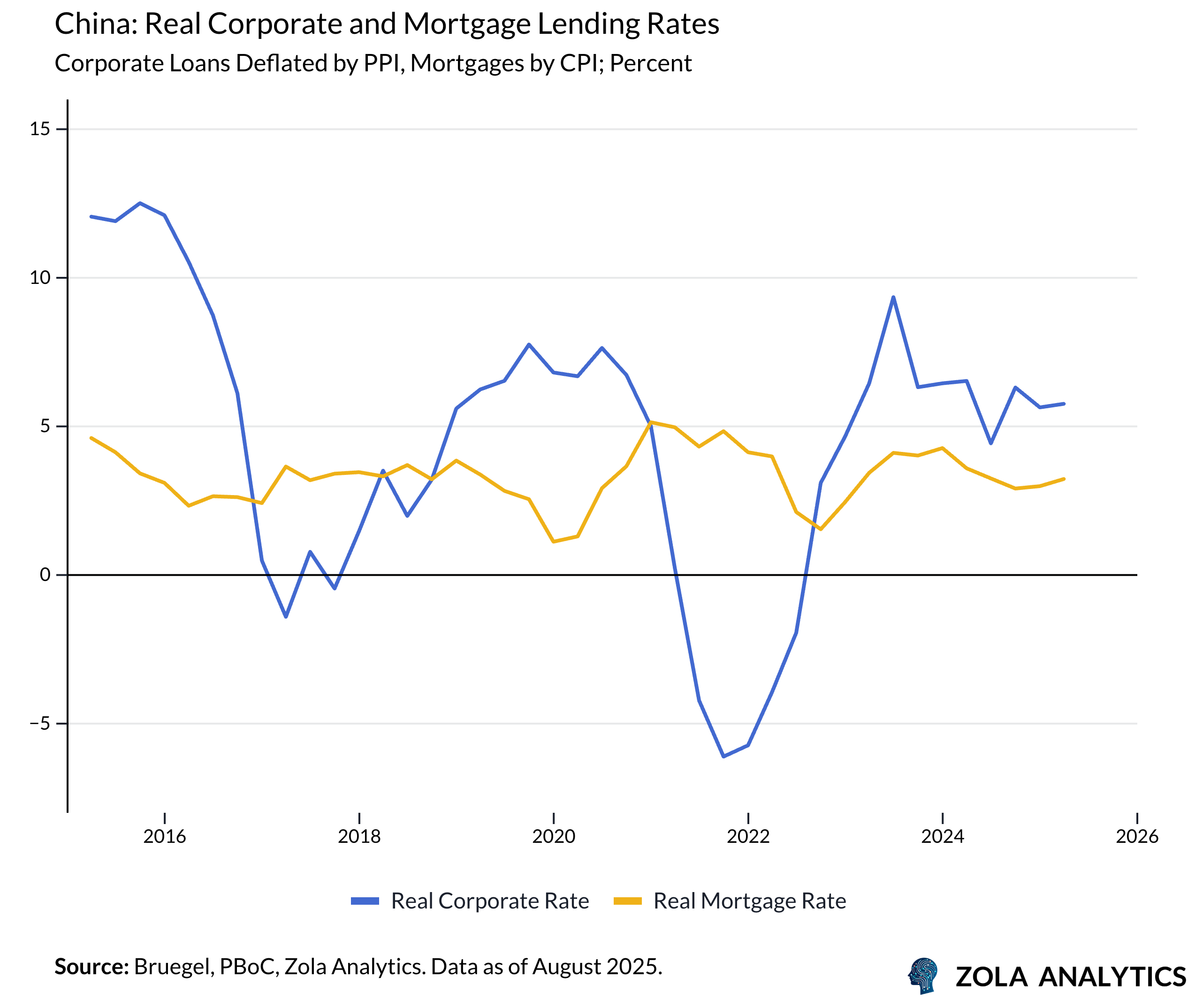

Capacity keeps expanding because the government lacks other levers to deal with fluctuations in economic activity. Since COVID, the impairment of China’s policy tools has become more apparent. Credit has been increasingly channelled toward the government sector, whilst households and corporates have seen little growth in lending. Local governments continue to back projects that raise headline GDP, reinforcing the bias.

The limited appetite for credit from households and corporates demonstrates the lack of worthwhile investment projects. Even after repeated cuts, real interest rates remain high, adding further pressure on borrowers.

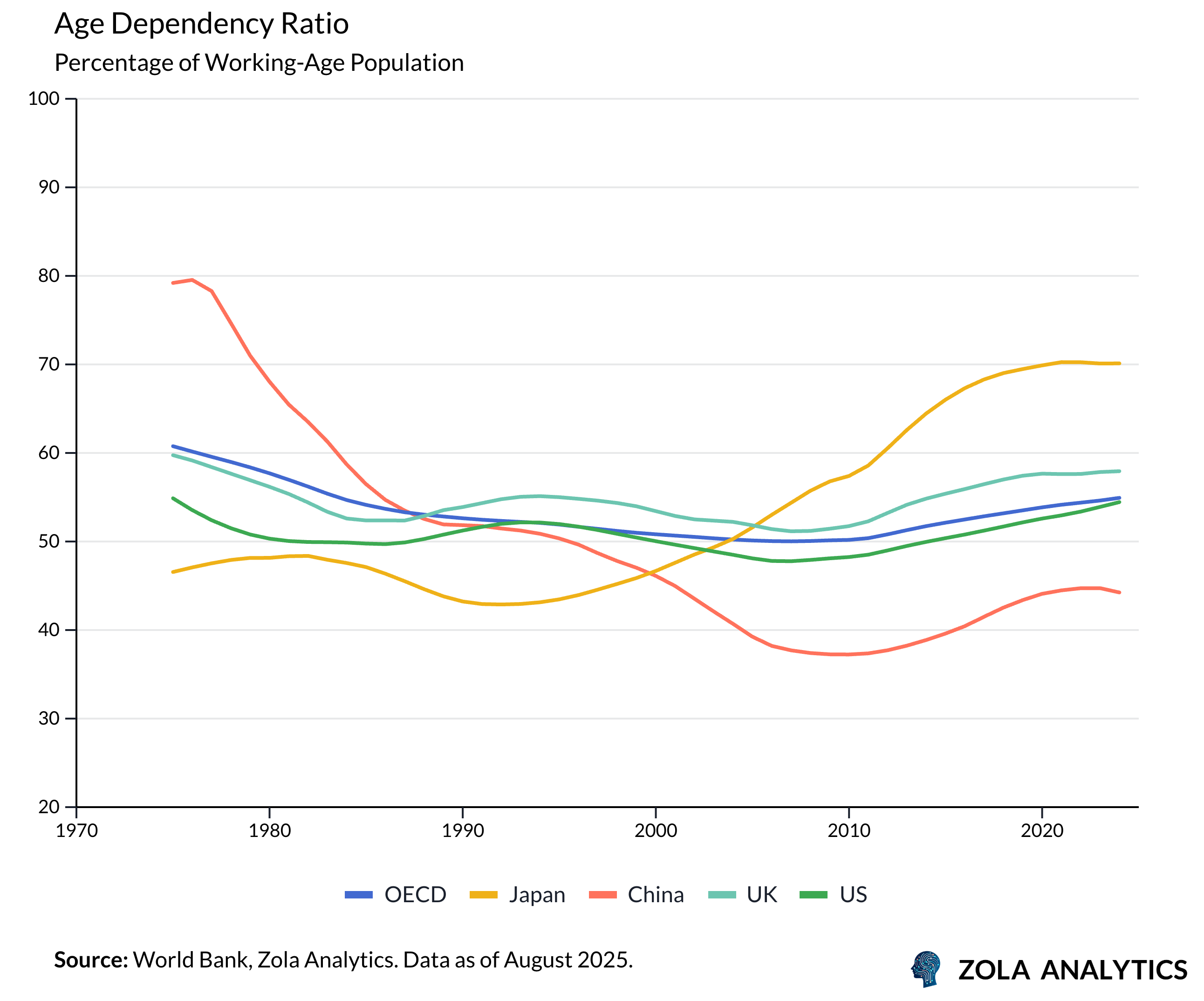

A tailwind since the 1960s, China’s demographics, became a headwind in the early 2010s. This magnifies the strain and presents a daunting challenge to the government in coming years. Fewer workers, more dependents, and persistently low fertility will mean China gets old before it gets rich.

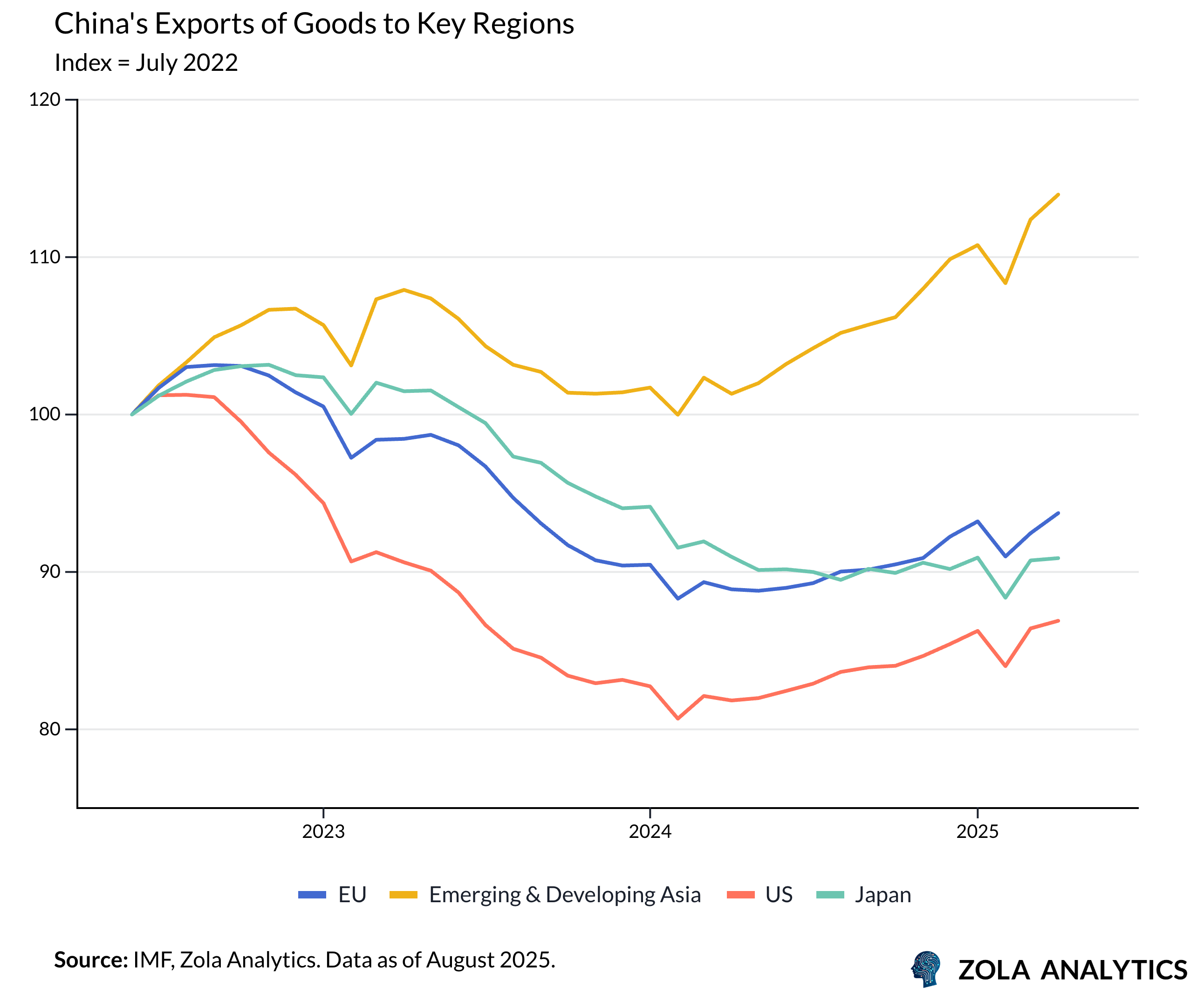

Meanwhile, external demand is no longer the cushion it once was. Exports to the US and Europe have declined, pressured by tariffs, technology controls, and weaker demand, forcing greater reliance on ASEAN and emerging markets.

Taken together, these forces will manifest as low growth, with households and firms focused on paying down debt rather than taking on new obligations. In China’s case, the trap is compounded by global spillovers from industrial overcapacity, making the challenge both domestic and international.

Why Rebalancing Stalls

Beijing is as aware of these issues as anyone. But so far their efforts, such as the anti-involution campaign that focuses on cutting production capacity and curbing disorderly pricing schemes, do nothing to address a fundamentally broken growth model. They are pruning the branches rather than treating the root. Without stronger household demand, even a leaner industrial base will not deliver sustainable growth.

How could China reduce the savings rate? First it needs a stronger welfare state. A comprehensive system could reduce precautionary savings, give households the confidence to spend, and ease demographic pressures through childcare and eldercare provision. Portable benefits would reduce regional gaps, whilst fiscal clarity would improve policy transmission.

If the solution is so simple, why has it not been implemented? Part of the answer lies in financial stability. With most household wealth tied up in property, any large-scale transfer of income risks spilling into speculation rather than steady consumption. Past attempts at supporting equity markets have quickly morphed into margin-fuelled rallies, whilst episodes of capital flight show how easily new savings can leak offshore. Policymakers also worry about the renminbi. Since 2023, state banks have been leaned on to steady the exchange rate; a shift toward consumption-led growth would narrow the trade surplus just as outflow pressures mount, complicating currency management and forcing heavier intervention.

The political economy is just as constraining. Expanding welfare would shift resources and influence away from the Party’s traditional levers - local governments, state-owned firms, and infrastructure projects - toward households. That risks undermining promotion pathways for cadres, narrowing the leadership’s crisis-management flexibility, and loosening central control over growth. Welfare outlays are also less visible than new factories or rail lines and harder to defend as “investment.” For a system built on production targets and supply-side mobilisation, redirecting income to households threatens both political authority and fiscal habits.

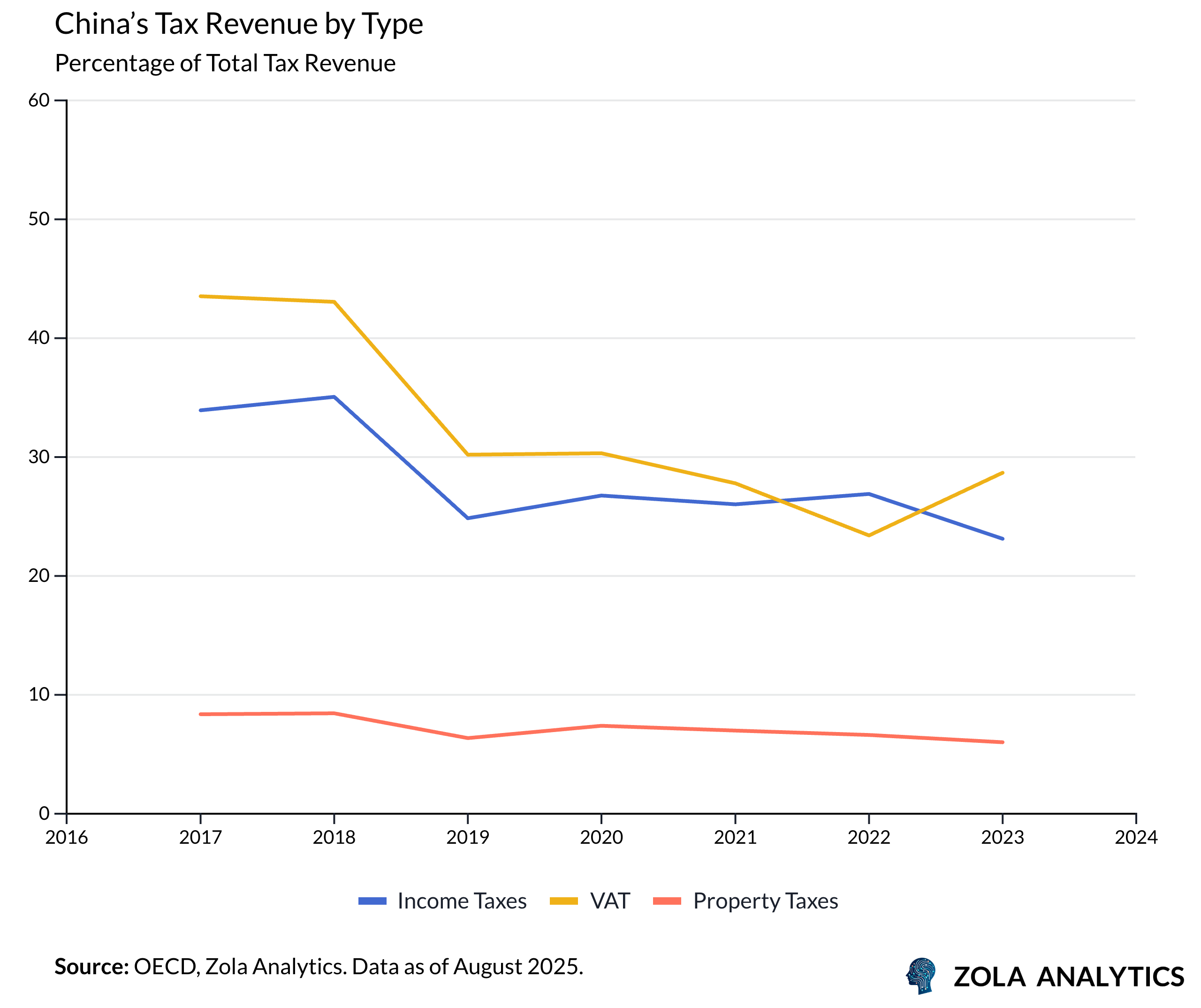

China’s fiscal architecture reinforces this bias. Revenues lean on production and transactions - VAT and turnover-type levies - whilst income and property bases remain comparatively narrow. That mix rewards throughput over household purchasing power, underfunds social insurance, and locks local governments into capacity-first behaviour.

A shift toward broader income and property taxation would better finance welfare and lift disposable incomes - supporting demand - yet it would also reallocate power and expose balance-sheet strains, which helps explain Beijing’s caution.

A Political Choice

Beijing’s anti-involution and industry consolidation efforts can trim some excess capacity, but they do not change incentives. Investment that fails to raise household incomes leaves firms chasing too few customers, keeping margins thin and disinflationary pressure alive.

The remedy is structural: a stronger welfare state, a fiscal shift toward income and property bases, and cadre evaluations that reward household prosperity, not sheer output. Without this pivot, China settles into a slow-growth equilibrium whilst its surpluses spill abroad as gluts and price wars. Pruning buys time; only a shift of power and income to households changes the path.

Sign up to receive the Zola Global Macro Chartbook every week: https://www.zolaanalytics.com/insights?signUp