Published June 30th 2025

Spain: Solid Fundamentals, Soft Institutions

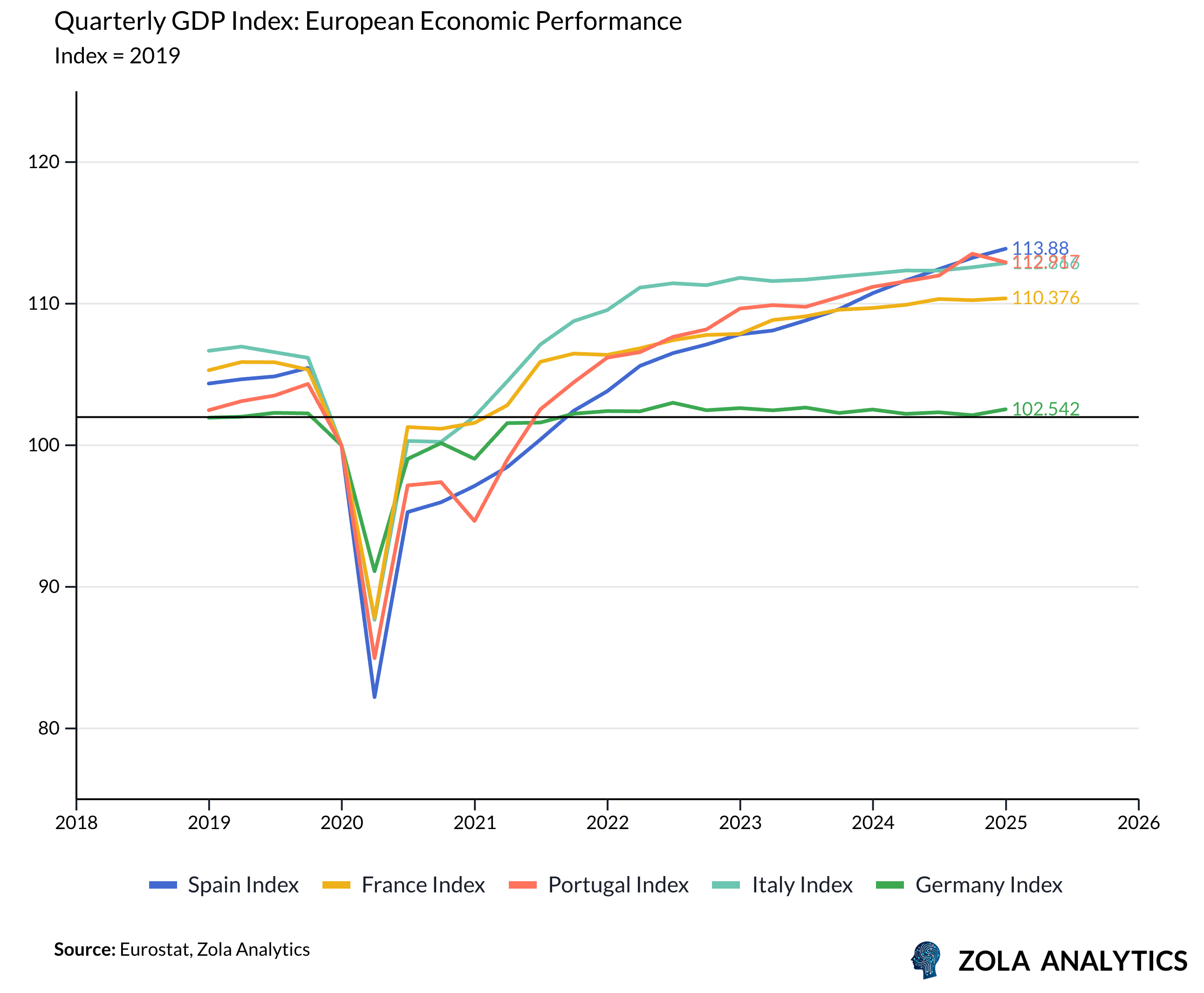

Spain has emerged from the pandemic and energy crisis not only unscathed but notably stronger, outperforming many advanced economies. It posted the fastest GDP growth among major developed economies in 2024 and is expected to retain a leading position in 2025. This performance is underpinned by a deliberately counter-cyclical response to the COVID-19 shock, a significant shift from the austerity-led strategy of the previous crisis. Key components of Spain’s post-pandemic model include:

Robust labor market dynamics, bolstered by 2021 labor reforms that drastically reduced temporary employment and incentivized permanent contracts.

Record job creation, notably in high-value sectors such as ICT, and a labor force increasingly supplemented by immigration, particularly from Latin America.

Improved productivity, enhanced by targeted investments and structural reforms.

Social inclusion policies, with minimum wage hikes and guaranteed income support mechanisms compressing wage inequality to the lowest level among advanced economies.

On the external front, Spain has moved away from its historic dependence on foreign capital. It now runs a sizeable current account surplus (4.2% of GDP), driven by both traditional tourism and a more diversified export base including IT, financial services, and consulting. Spain has also become one of the top global destinations for greenfield investment.

On the fiscal side, Spain has achieved a notable consolidation. The debt-to-GDP ratio has fallen by over 22 percentage points from its 2021 peak, and the budget deficit has dipped below the EU’s 3% threshold — all while maintaining support for the welfare state and investing in long-term productivity.

Political Turbulence Looms Though

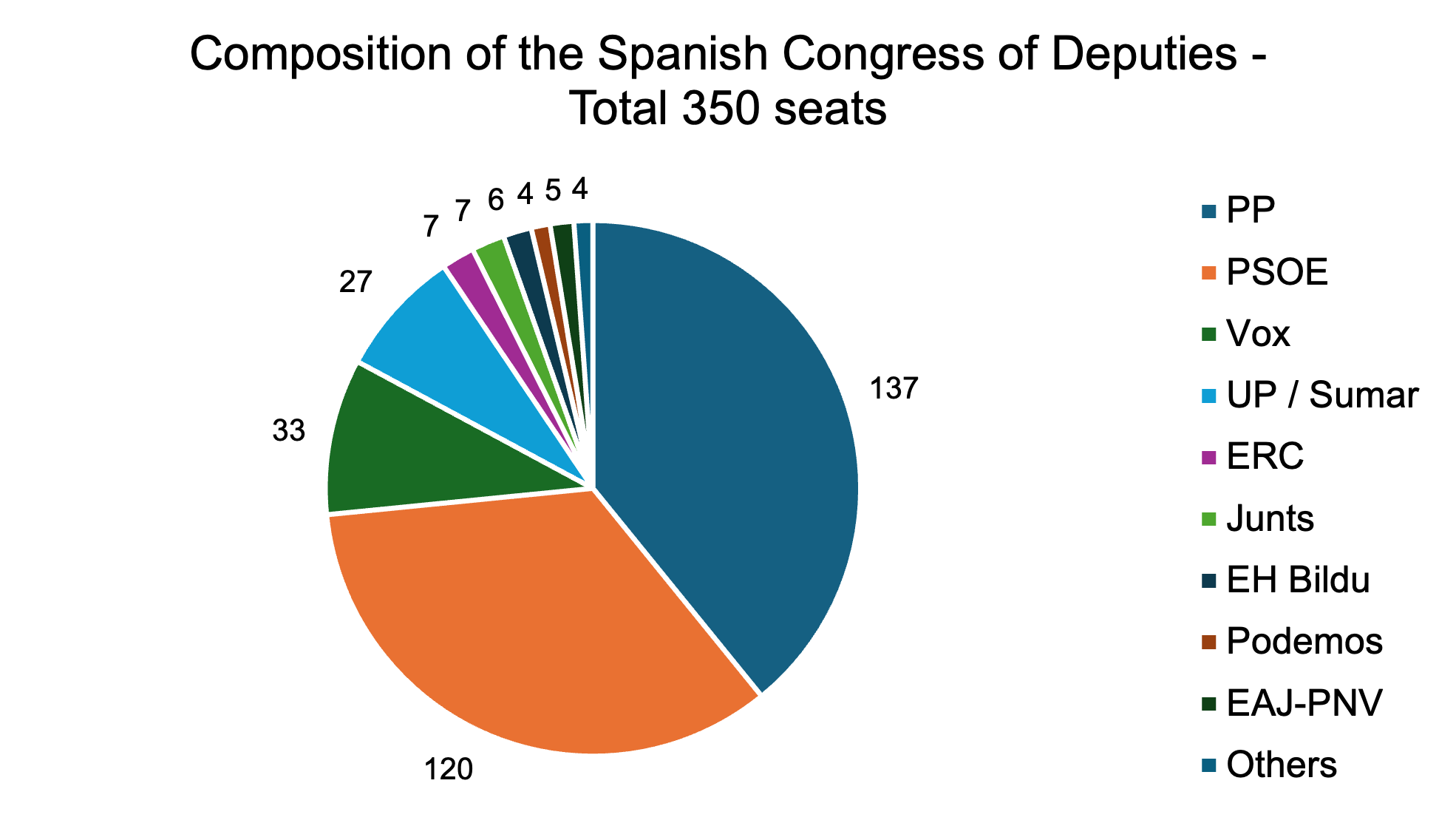

This economic renaissance is unfolding against a backdrop of growing political vulnerability. The Socialist-led government, already reliant on a fragile and fragmented coalition, is facing a deepening crisis triggered by corruption investigations targeting top allies of Prime Minister Pedro Sánchez. These scandals have eroded public trust and are threatening to destabilize the legislative process.

The government’s survival prospects through to the scheduled July 2027 elections are increasingly doubtful. Key risk triggers include:

Failure to pass the 2026 budget: After failing to approve budgets in both 2024 and 2025, a third failure could force either a snap election or the dissolution of parliament.

Coalition cracks: The support of regionalist and independentist parties, essential for legislative passage, is waning, especially with public sentiment turning against perceived corruption.

Upcoming regional elections: Particularly the June 2026 vote in Andalusia — historically a Socialist stronghold — could act as a referendum on the national government and trigger early elections.

Possible motions of censure or confidence votes remain on the table, though less likely in the short term due to the complexity of constructing a viable alternative majority.

Polls indicate that if elections were held today, the Socialist Party would likely lose to the centre-right opposition, with the far-right gaining ground. This creates perverse incentives for both the opposition and regional allies to delay intervention, allowing the government to weaken further.

Balancing the Narrative: Durable Growth Meets Institutional Uncertainty

The contrast between Spain’s economic and political trajectories is stark. On one hand, Spain’s macro fundamentals are arguably stronger than at any point in recent memory: low unemployment, fiscal stability, external surpluses, and sustained productivity-enhancing reforms. On the other, political risk is rising, with potential implications for policy continuity and investor confidence.

While the economic model appears structurally resilient, a prolonged period of political instability could eventually impair reform momentum, especially in areas like housing, defense, and climate transition — all of which require fresh legislative resources.

At this stage, markets appear to have confidence in the macro path, as evidenced by strong sovereign bond demand and recent credit rating upgrades. However, the outlook could darken if the political crisis escalates into an institutional impasse or leads to an abrupt policy shift post-election.