Published 16th December 2025

8 minute read

After the Miracle

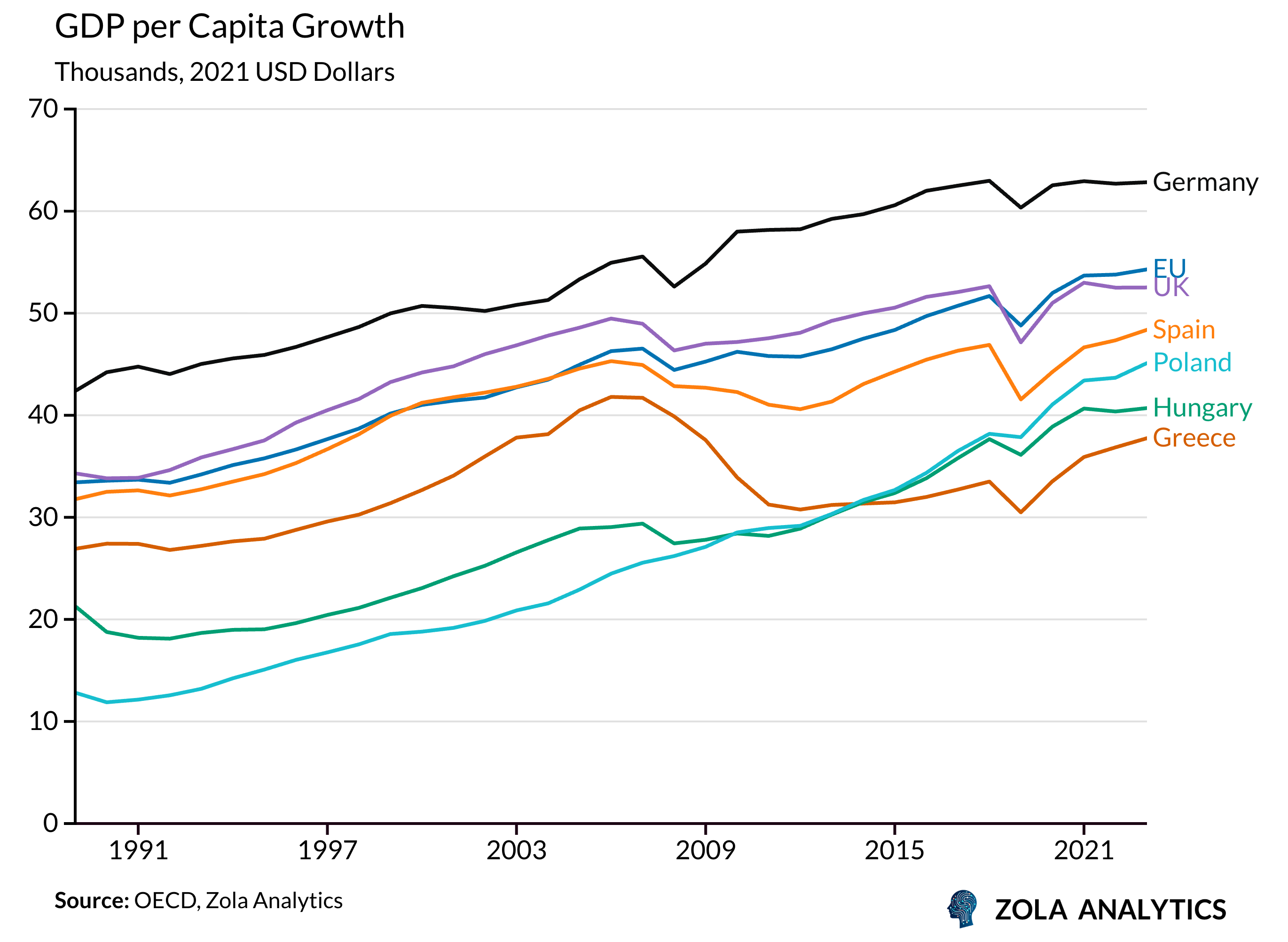

For many years following the fall of the Berlin Wall, the Polish plumber was cast as the embodiment of cheap labour emigrating to Western Europe from the former-communist East. In 1995 Polish GDP per capita was 36% the level of the UK’s. It is now 81%. With this gap expected to narrow further, these tired stereotypes are badly outdated. The performance of the Polish economy over the last three decades has been stellar, but it faces new challenges in the coming years. This edition of Zola Chartbook investigates how that happened, and whether it can continue.

The Making of a Growth Engine

Among post-communist economies, Poland stands out as a success story. The Balcerowicz Plan of 1990 imposed harsh austerity but crushed hyperinflation and enabled a market transition. Russia's parallel attempt at shock therapy collapsed into oligarchy and economic chaos, in part because Poland maintained stronger state capacity and sequenced privatisation more carefully.

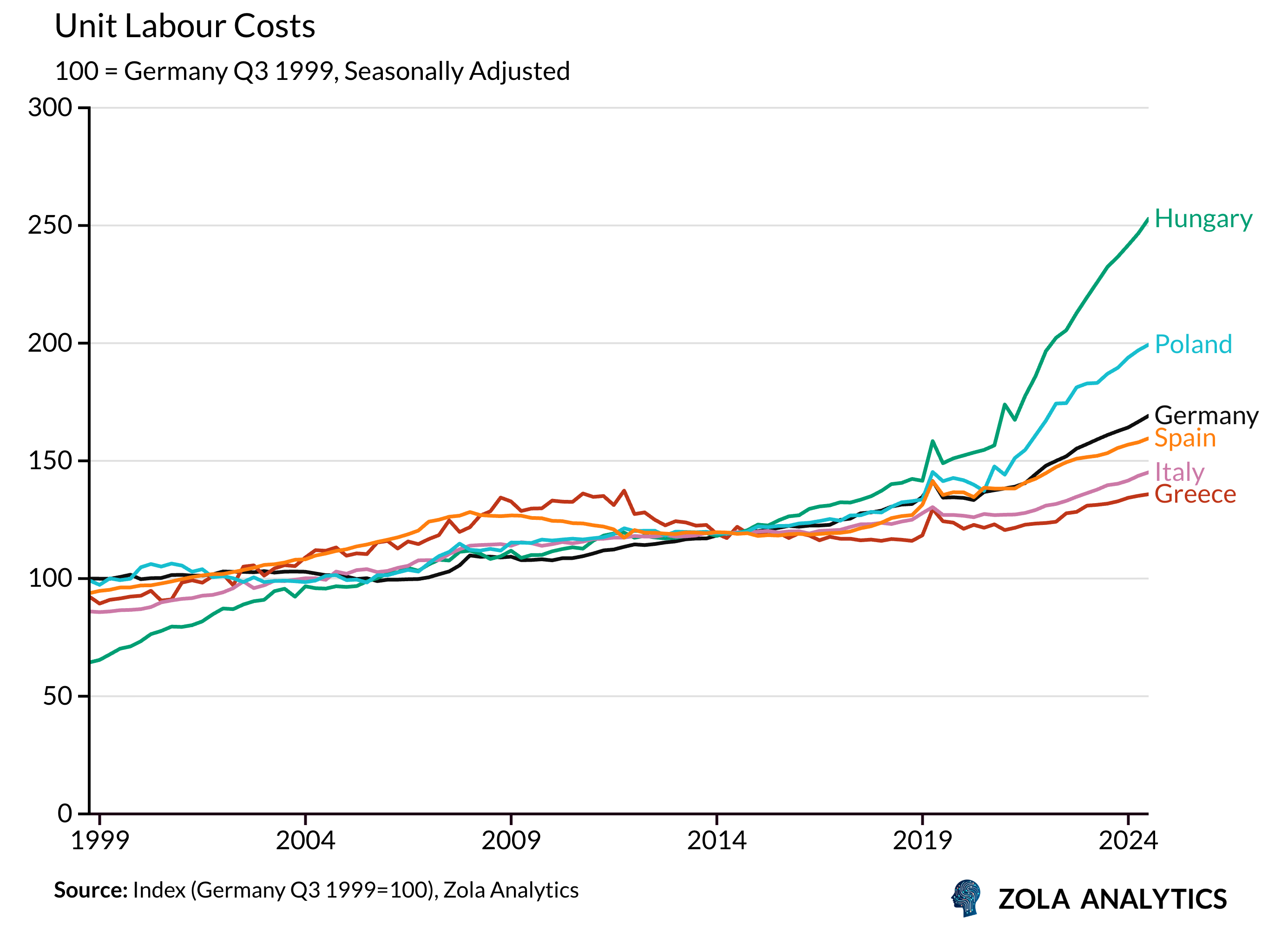

EU membership cemented Poland's gains, bringing investment, structural funds, and access to the single market. Manufacturing labour costs remain below German levels, but the gap is closing as wages rise and the workforce shrinks.

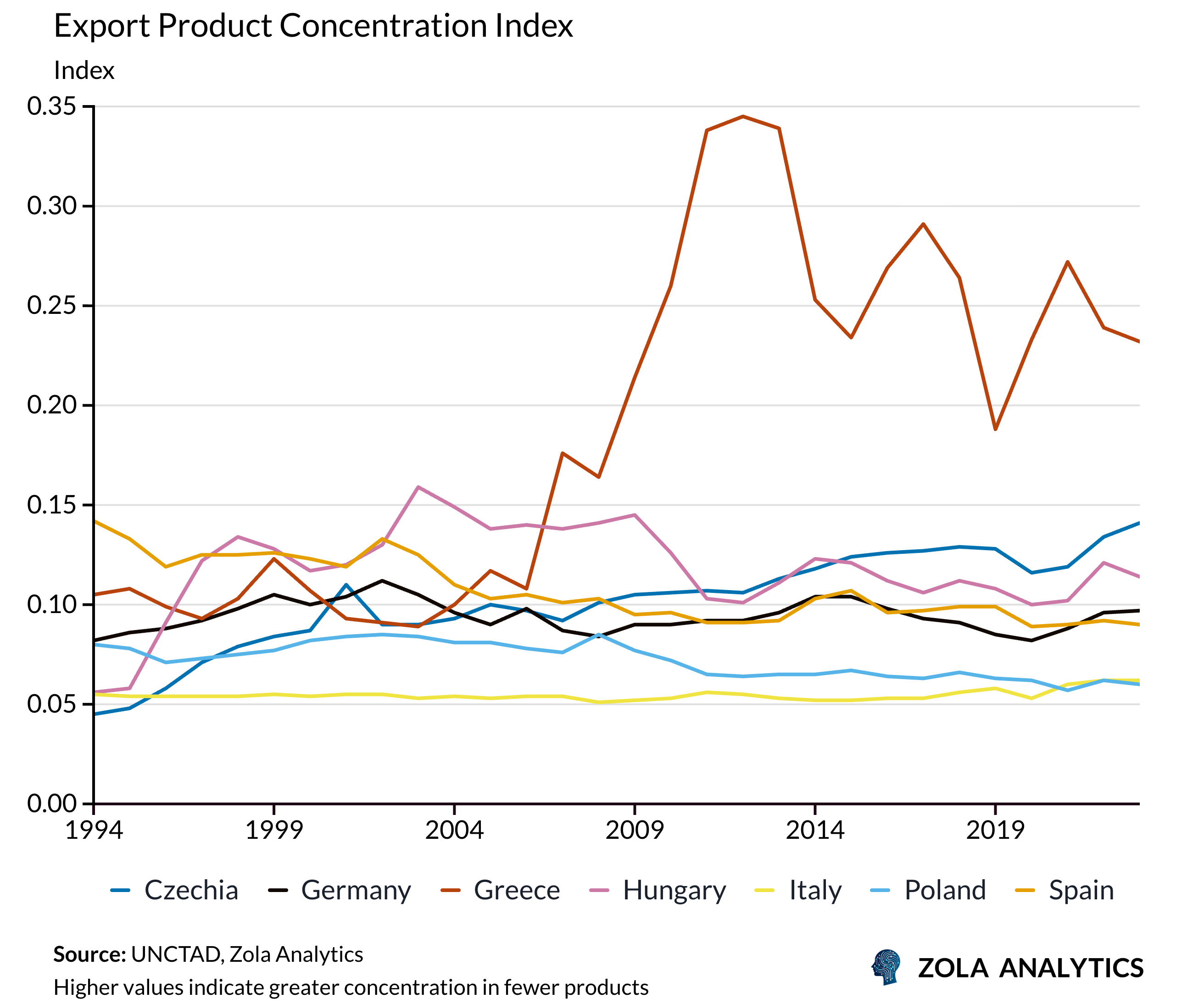

Today Poland is the EU's sixth-largest economy. While other European economies share some of these attributes, Poland had several unique advantages.Its central location between Germany and the former Soviet bloc made it a natural hub for manufacturers seeking access to both Western and Eastern markets. A large domestic market of 38 million people provided internal demand, cushioning the economy against external shocks. Its exports are among the least concentrated in the world, comparable to Italy and the United States, helping the country weather economic volatility.

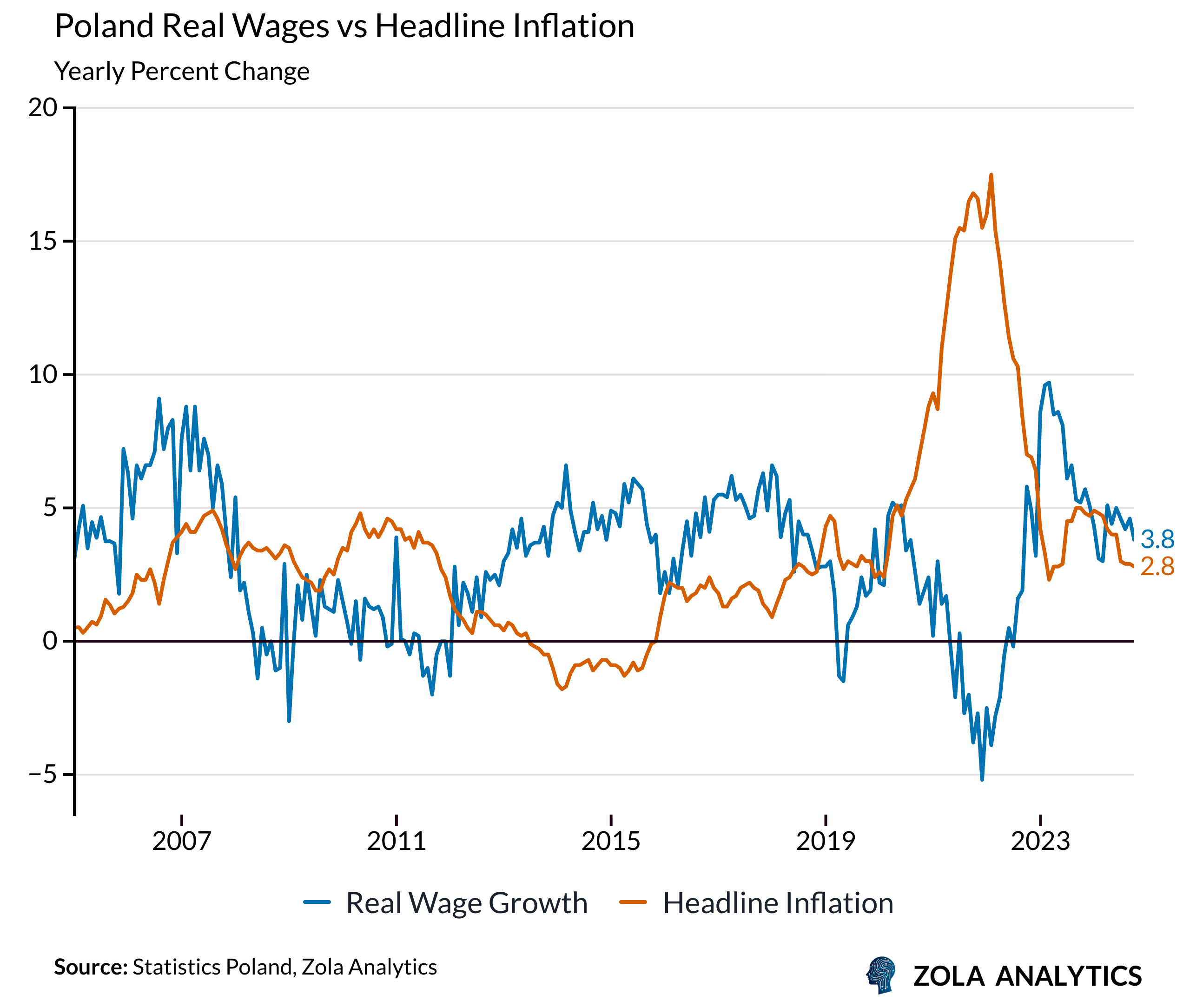

These structural foundations are now paying dividends. Third-quarter 2025 growth came in at 3.8%, driven by fixed investment up 7.1%, concentrated in public works and defence procurement. This was matched by robust government consumption, which surged 7.4%. In previous cycles, household spending regularly outpaced output. Now Poland's growth is more balanced, with Q3 private consumption growing only 3.5%.

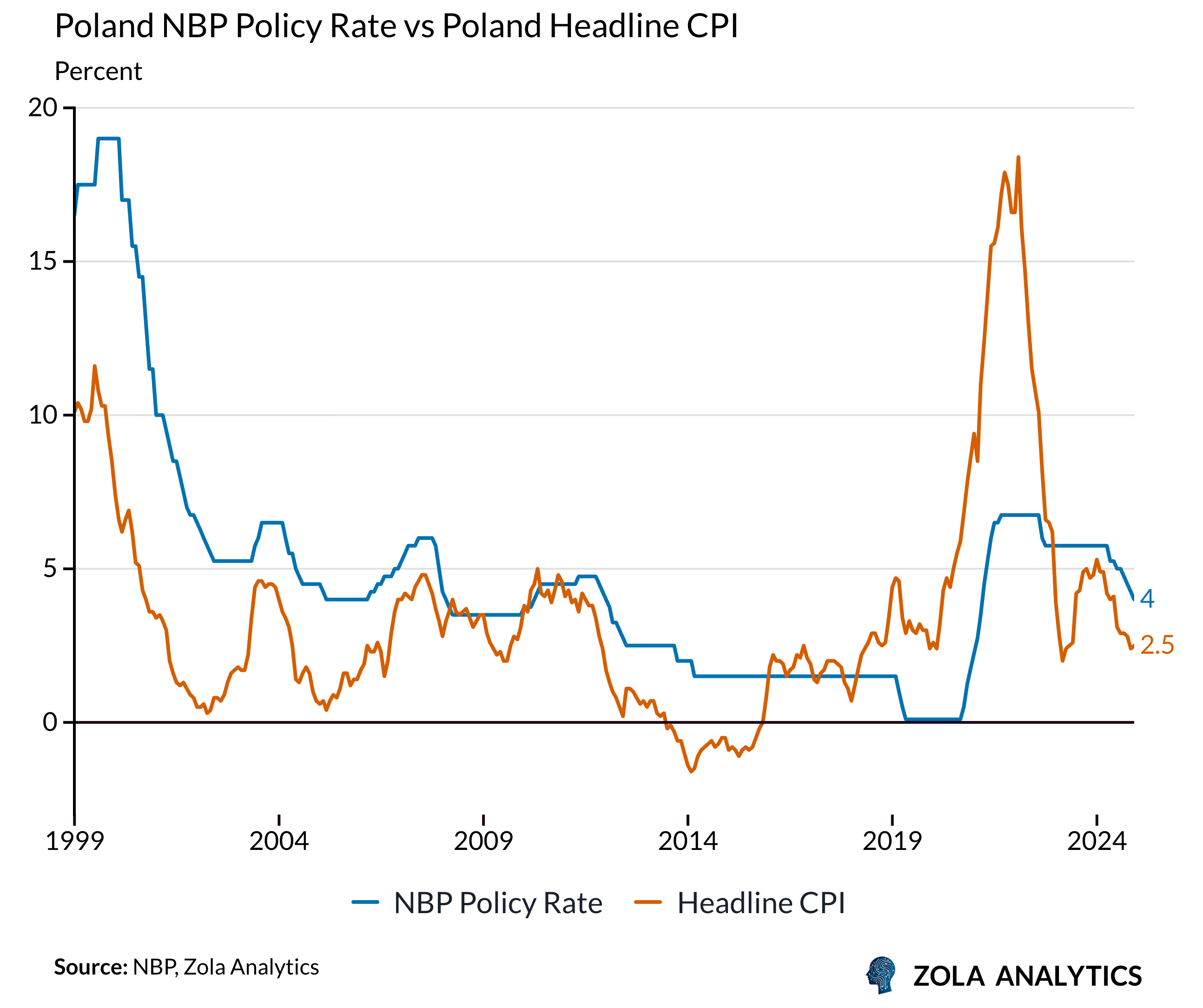

This composition has kept inflation contained. Core prices fell to a six-year low in November and nominal wage growth has eased to its weakest in five years. The National Bank of Poland responded with four rate cuts since May, bringing its benchmark to 4.0% in December, and markets expect further easing toward 3.25% by the end of 2026.

A House Divide

In June 2025, Karol Nawrocki won the Polish presidency with backing from the opposition Law and Justice party. Since then, he has enjoyed a testy relationship with Prime Minister Donald Tusk. The pro-European coalition holds a parliamentary majority but lacks the three-fifths supermajority required to override presidential vetoes, and Nawrocki has used that leverage to freely block tax increases, reject ambassadorial appointments and veto energy price caps. The legislative agenda is frozen until parliamentary elections in October 2027.

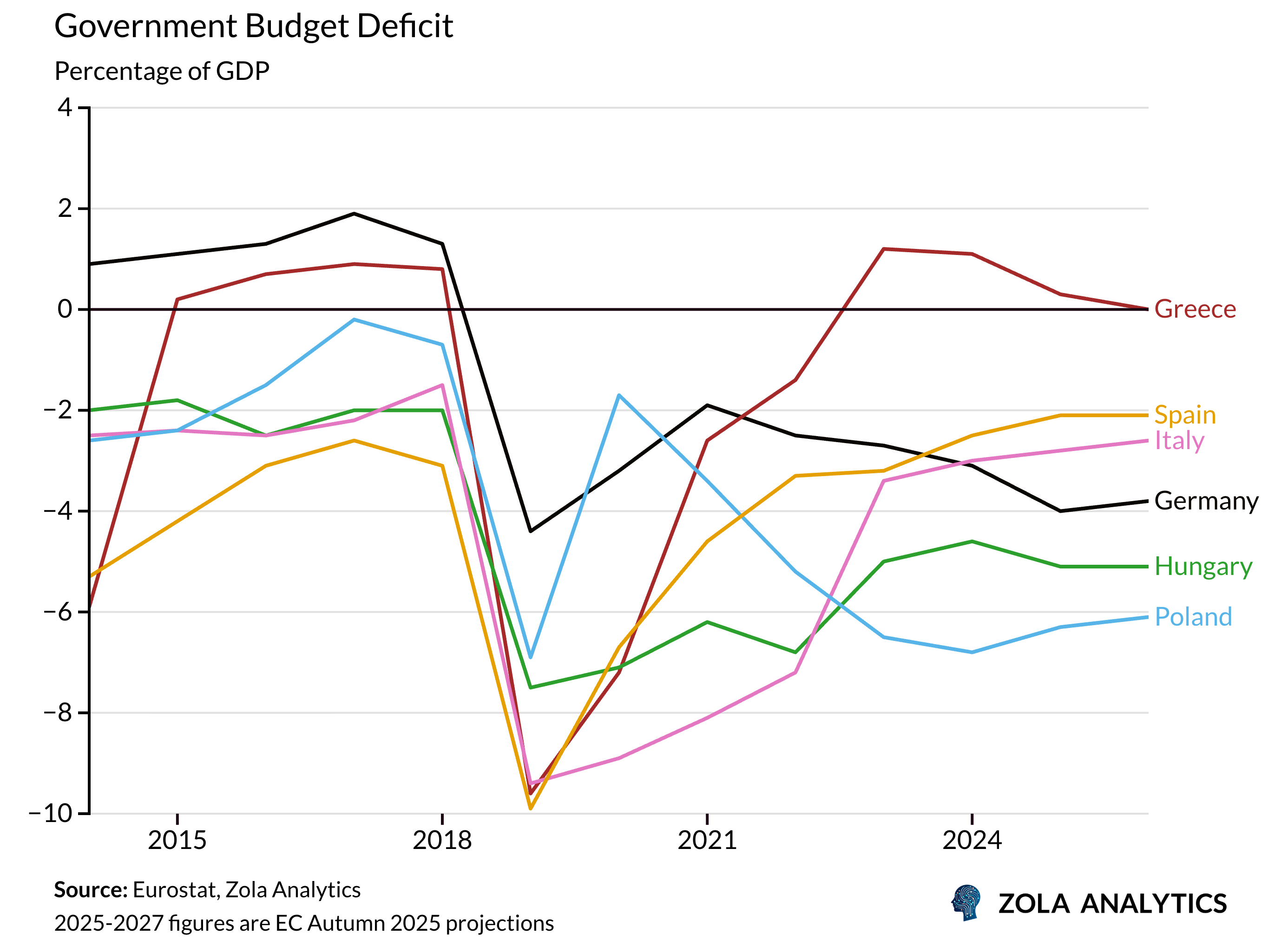

The fiscal consequences are significant. Poland's budget deficit has climbed from 1.7% of GDP in 2021 to 6.6% in 2024, triggering the EU's Excessive Deficit Procedure. It is now approaching 6.8%, which will push public debt close to the 60% ceiling enshrined in both EU rules and the Polish constitution. Yet Brussels has shown unexpected leniency. In November 2025, the European Commission accepted Poland's invocation of the defence escape clause, acknowledging that the deficit reflects security imperatives rather than structural mismanagement. The Excessive Deficit Procedure remains in place, but its sting has been dulled.

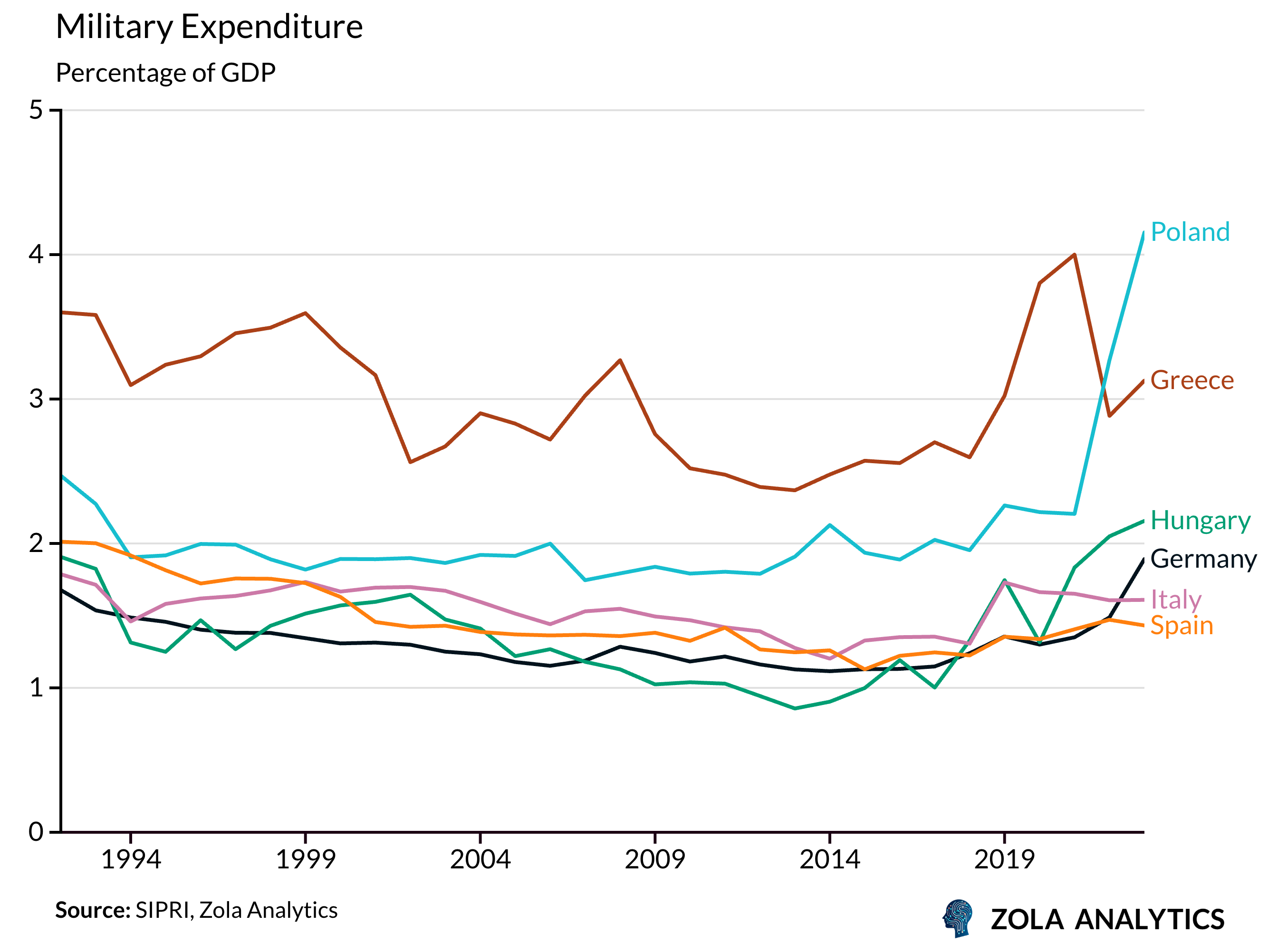

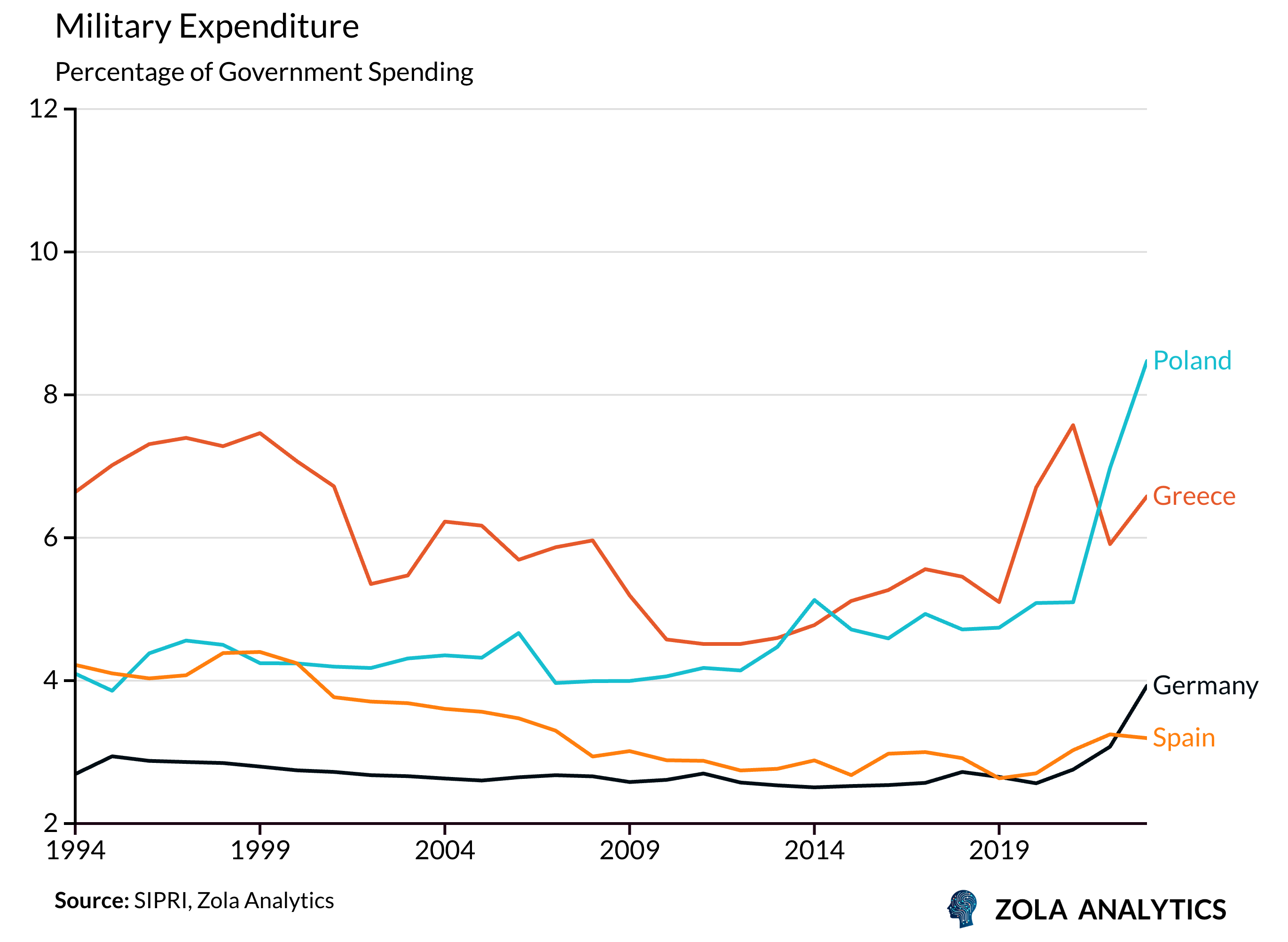

Defence is the one domain where political paralysis does not apply. Military spending has tripled since 2014 to reach 4.7% of GDP in 2025, the highest ratio in NATO after the United States. As a percentage of government spending, the shift is even starker. Defence now consumes nearly 9% of the Polish budget, more than double the German or Spanish share. The build-up crowds out some private investment but also acts as stimulus. In November, the European Commission upgraded its 2026 growth forecast for Poland to 3.5%, citing the resilience of what amounts to a war economy. For now, the scale of military investment is allowing the economy to outrun its political dysfunction.

Brussels' Leverage

Since 2004, Poland has received some EUR 425 billion from EU coffers but EUR 160 billion remain earmarked. Brussels unlocked the Recovery and Resilience Facility after years of dispute over judicial independence, extending the spending deadline to December 2026, but political paralysis in Warsaw has stymied the flow.

Grant absorption has stalled at 35%, well below the EU average of 54%. President Nawrocki's vetoes block the technical legislation needed to distribute funds, and in late August the government reduced its RRF loan request by PLN 22 billion, acknowledging it could not process the money in time.

The government has found workarounds, with the state development bank BGK signing PLN 55 billion in subsidised loans to keep energy grid modernisation alive. And recognising that green funds were stalling, the government pivoted to security, reallocating PLN 26 billion of RRF loans into rearmament and locking in EUR 44 billion from the new Security Action for Europe facility, the bloc's largest allocation. Pre-financing triggers in early 2026, providing a fiscal bridge just as borrowing needs peak.

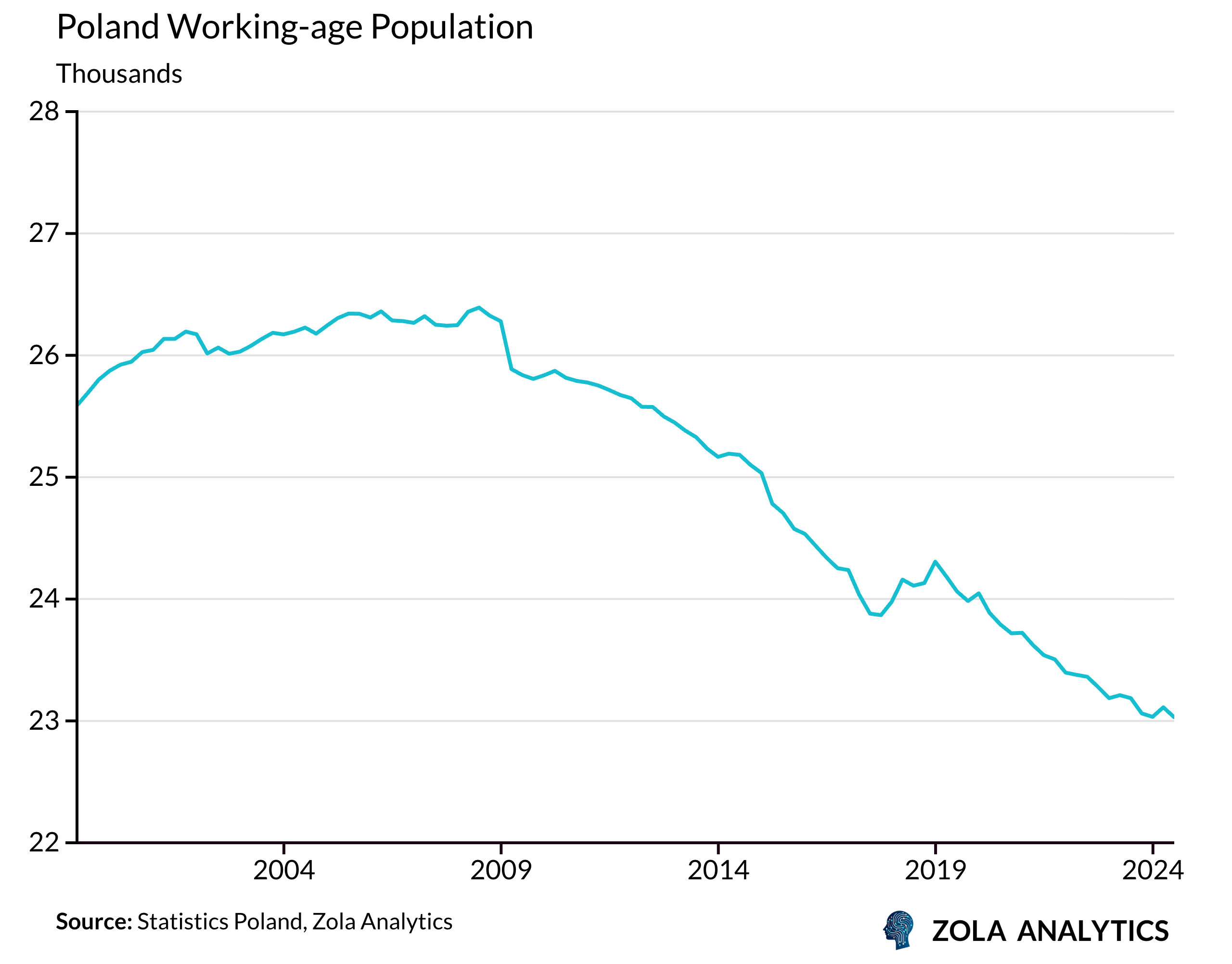

The Labour Cliff

Some of Poland’s advantages have now begun to erode. Poland's working-age population has been shrinking since 2009, and the decline will steepen. The share aged 15-64 is projected to fall from 63% today to 51% by 2055, while those over 65 will increase by a third and those over 80 will double.

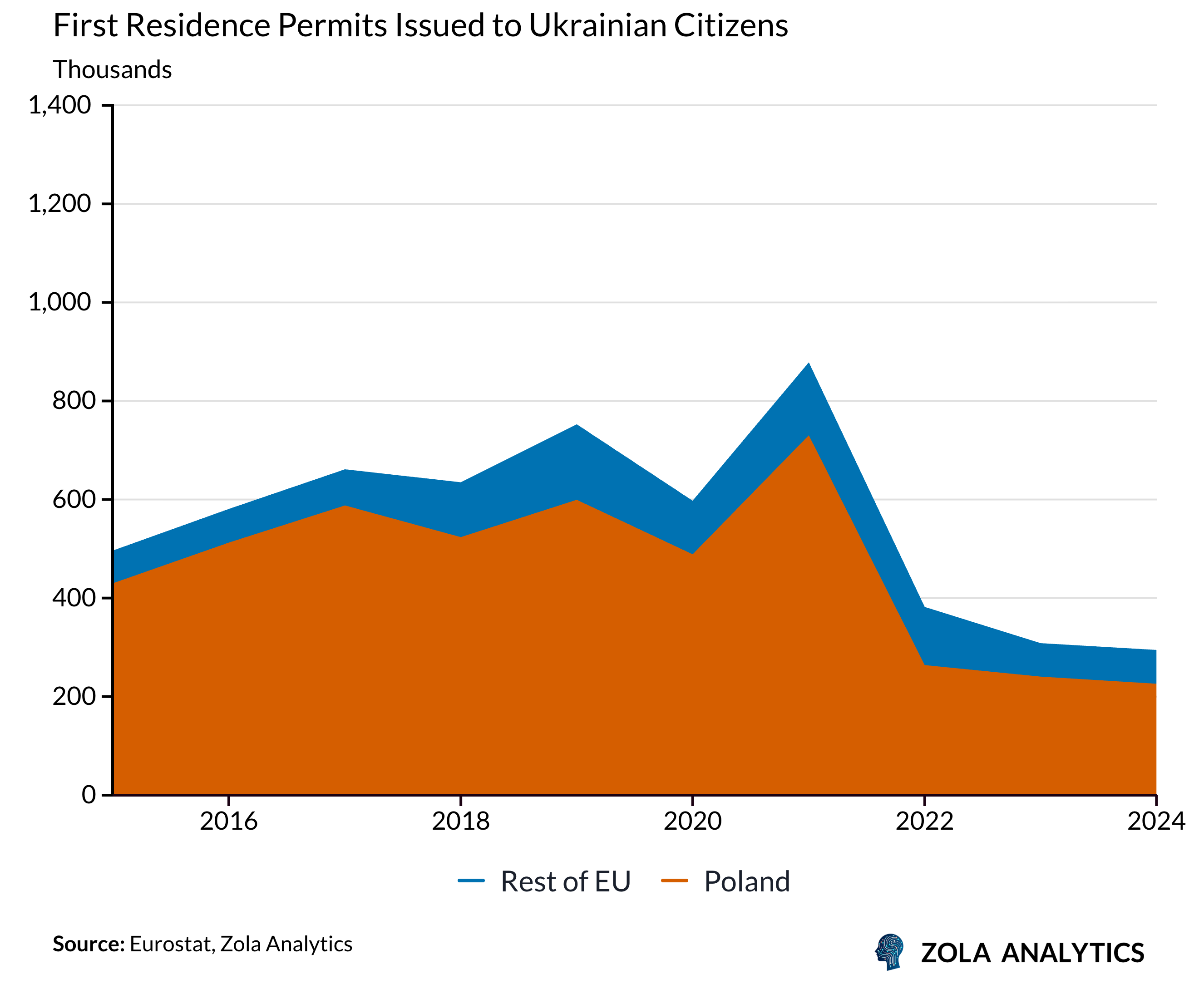

For most of the past decade, tight supply has been a feature of Polish labour markets. Unemployment fell below 4% in 2018 and stayed there, powering real wage gains that lifted consumption and narrowed the gap with Western Europe. Between 2022 and 2024, nominal wages rose 12% annually. Around one million Ukrainian refugees eased that pressure somewhat, filling gaps in construction, logistics, and services.

By late 2025, the picture has changed. The refugee influx has now stabilised, and the political window for further immigration has shut. Prime Minister Tusk's "Reclaim Control, Ensure Security" strategy suspended asylum rights and tightened visas in late 2024. By December 2025 the first sections of Shield East were complete, a EUR 2.5 billion fortification that began as border controls and evolved into a barrier against both military threats and irregular migration. Residence permit data shows the surge and its tapering. Poland absorbed most of the initial wave, but the flow has normalised.

The constraints are now becoming binding. The IMF estimates that shrinking labour supply will subtract 0.6 percentage points from potential growth by 2028-29. The European Commission warns that without productivity gains, headline growth could halve to 1.5% within three years. The demographic drag that was deferred will soon start to bite.

The Bet on Growth

Warsaw's response is to outgrow its problems. Rather than tighten, the government will sustain investment, absorb EU funds as fast as bureaucracy allows, and let growth stabilise the debt ratio over time.

The fiscal reprieve from Brussels and the pivot to national security have reversed the coalition's fortunes. Polls from early December show Tusk leading Law and Justice by 34% to 29%. The immediate threat of a populist takeover has receded, buying time for the bet to play out.

Time, however, is precisely what Poland is running short of. The model that carried it this far cannot carry it much further. The question is whether Warsaw uses this window to build something new, or discovers too late that it has closed.