Steven Bell on the UK’s Fiscal Reckoning

Steven Bell spent his career reading governments and central banks, both as a policymaker and a portfolio manager. Today, he sits down with Zola to walk through the fiscal challenges facing Andy Burnham, the ideas on the table to get around them, and why his call on rates puts him at odds with the consensus.

When The Tailwinds Turn

You have been analysing British fiscal policy for many decades. How has the UK ended up in its current predicament?

The big picture is that our fiscal position used to benefit from some favourable long-term factors. They have now gone into reverse.

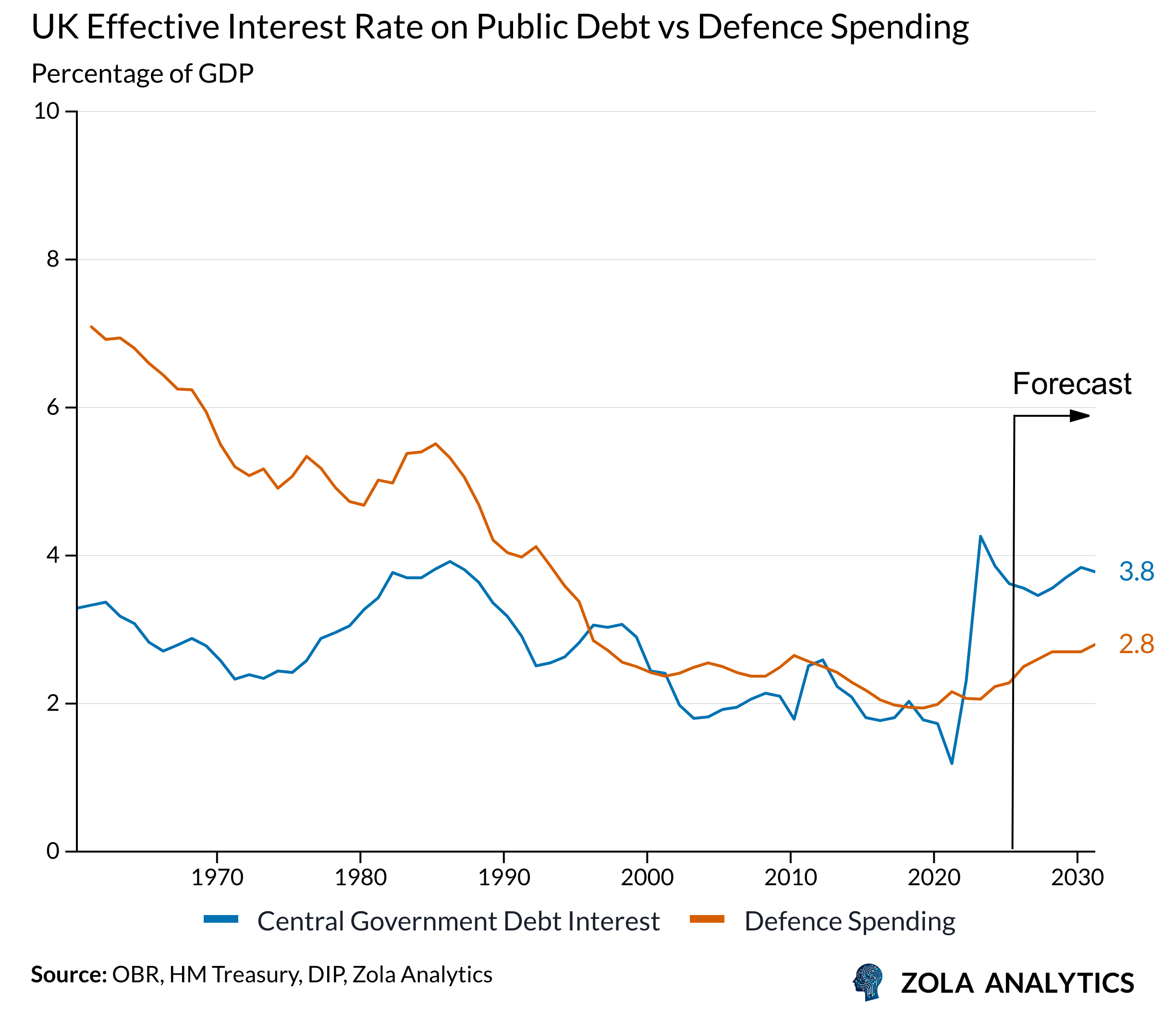

The first, ironic given where we are today, is defence. After the Second World War we were spending around 7% of GDP on defence, and that gradually declined. When the Wall came down and the Soviet Union stopped looking like a threat, it fell further still. That’s now stopped, and it’s reversing.

The second is interest rates. They came down from about 1980 onwards. Government debt sits at much longer maturities than most households’ or companies’ borrowing, so it takes time to feed through — but rates fell and fell until they hit zero, and from the late 1980s the debt-interest burden came down with them. On top of that, the debt stock itself fell as a share of GDP. It was around 250% after the war and it just kept coming down, even though we were running deficits.

Well, both have reversed. COVID and the global financial crisis massively increased the stock of debt, and interest rates have gone back up.

So it all comes down to the gap between growth and interest rates?

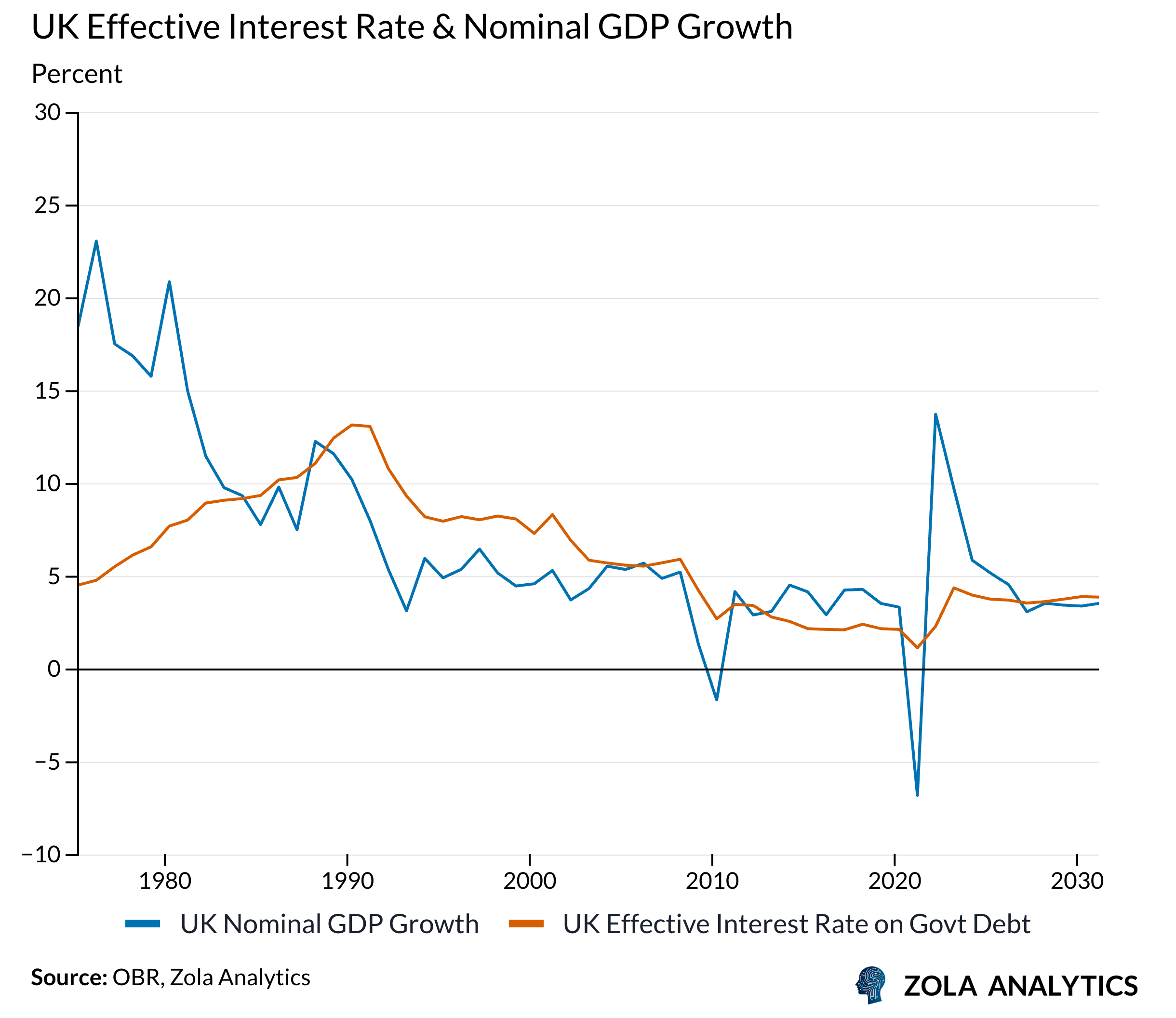

That’s exactly it. If you’ve got a stock of debt and you want to keep it constant as a share of GDP, the key question is whether the economy is growing faster than the interest you are paying on that debt.

If nominal growth is high enough, you can borrow each year and keep the debt ratio stable, because GDP is growing too. But if the interest rate is the same as the nominal growth rate, you can’t really do that: the borrowing capacity is used up paying the interest. You can refinance and stand still with a zero primary balance, but that is all.

Go back to the post-war period and we had very rapid growth and tiny interest rates; short rates were fractions of 1%. Now it is the other way round. Growth is low, inflation has been running around 3%, and the nominal interest rate is well above the nominal growth rate. That is the bad news. It means you need a primary surplus just to stand still.

What about the growth side of that equation?

There’s no doubt we had unexpectedly good growth after the war. Some of that was reconstruction, taking people out of the army and putting them back into work, but there was genuine rapid growth beyond that too.

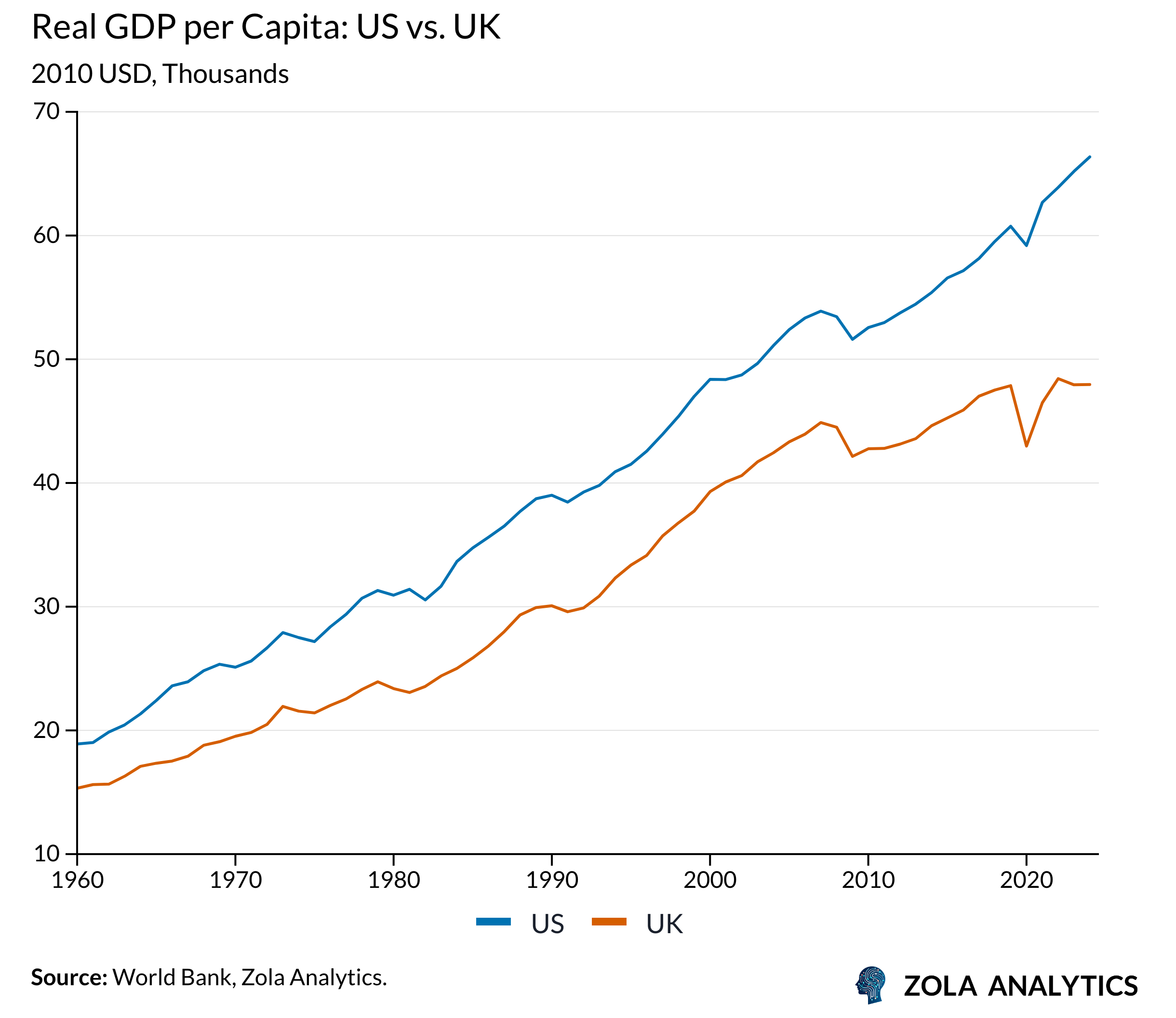

That growth rate has fallen, and that’s true across advanced economies. The US looks to be doing better than the other majors, but even there growth is slower than it was. And we’re doing particularly badly. UK per-capita growth is pretty dismal. This parliament will probably produce the lowest growth in personal disposable income of any parliament, matched only by the decline in the last one. Put the two together, and it is the longest stretch of terrible income growth in the post-war period.

Women entering the labour force is an interesting example. When I first had GDP explained to me, the textbook line was that if two women swapped housework and paid each other, GDP would go up. In a funny way, that is what happened. A lot of women went out to work, which increased demand for childcare, cleaners and other paid services, and that added to GDP. But that process is now pretty much done.

Equally, it isn’t simply that people live longer. It is that they live longer with needs they expect to be met. The NHS and other public services were squeezed and squeezed under what opponents called austerity, and you can’t keep squeezing without doing damage. A council can only close its libraries once.

Make Me Virtuous, But Not Today

How has the Labour government tried to face up to this challenge?

Well, they’ve announced a really tough fiscal policy, but they’ve started off doing the opposite. We’ve had a record increase in taxes, and an even bigger increase in spending. It’s the Steven Bell physical-adjustment policy: I plan to lose weight and get fit. In five years’ time I’ll be at zero booze and chocolate and going to the gym three times a week. Meanwhile, I’m off to the pub with a bar of chocolate and I won’t be near the gym this year.

It’s forward guidance.

It’s forward guidance, exactly. Promise the tax rises and spending cuts, but further out. And “further out” is now becoming now, which is the problem the next Prime Minister inherits. It comes back to what we used to call the porcupine curve in the Treasury: every projection had spending rising a bit and then declining after the next few years. Eventually, you can’t keep doing that.

The OBR must follow stated government policy, which is why they keep projecting the deficit hits zero and debt falls, but they also tell you the probability of meeting it, and there it’s obvious we have a big fiscal problem. Every single major country has an unsustainable fiscal policy.

Taxing Times

On the revenue side, you’ve been highlighting that a social care levy could be part of the new government’s approach. How would that work?

There are various permutations and the debate will come front and centre when Baron Casey’s report on social care comes out later this month. But one option would be an age-related levy: very small for the young, who’ll be paying it far longer, and higher for the elderly. Possibly an individual pot, some pooling, and certainly some redistribution.

In effect, it’s an increase in income tax rather than National Insurance, which means it applies to savings income as well as employment income. It would fund an increase in social care spending, but the inflow would be much bigger than that, so you could use the surplus for defence, or to raise the higher-rate threshold, and so on. The economist Gerry Holtham did exactly this calculation for the Welsh government: age-related, low in your 20s, and rising as you approach retirement.

The parallel I’d draw is the Beveridge Report. Beveridge was a Liberal and a near-godlike figure in Labour circles. He set up the National Insurance Fund with a 20-year phasing-in period. A national care levy could work in a similar way: something close to an individual pot, so it isn’t obviously a tax, with a big inflow up front. People may accept that, and may even reduce their savings in response, which supports demand.

It would also relieve bed-blocking. We have old people sitting in expensive hospital beds who should be in cheaper care homes, except local authorities and individuals can’t afford the places. Every care bed you open frees a hospital bed and cuts corridor care. It would of course mean breaking a manifesto commitment. It could be presented not as a tax but as a levy that working people would get back when they needed it. It is also a hypothecated tax, rather like Boris Johnson’s plan to raise NIC to fund extra spending on the NHS. That was popular.

The government seems to be hoping for cross-party consensus, to tie both themselves and the next government to the mast. Is that possible given the politics?

The view inside Labour, and Andy Burnham’s in particular, is that they’ve lost voters to the Greens and must move left to win them back. We estimate around 200,000 people have left the Labour Party since the election, and the Greens, who do publish, have gained about 250,000 members. The assumption is that most of the lost 200,000 have gone Green. Burnham had to beat Reform to become an MP, he must tilt left to carry Labour MPs, and then move to the radical centre to win the country.

So will other parties sign up to a national care levy? Why would they? People are all in favour of cutting the deficit and controlling spending, until it’s spending they benefit from. And they don’t mind tax rises that don’t touch them. So nobody signs up, and that’s the danger. It stops being a social contract people buy into because they’re paying into a fund and getting something back. Reform will promise that welfare cuts will be enough. Defection is just too tempting.

Beyond new taxes, is there more the government can do simply by collecting what it is already owed?

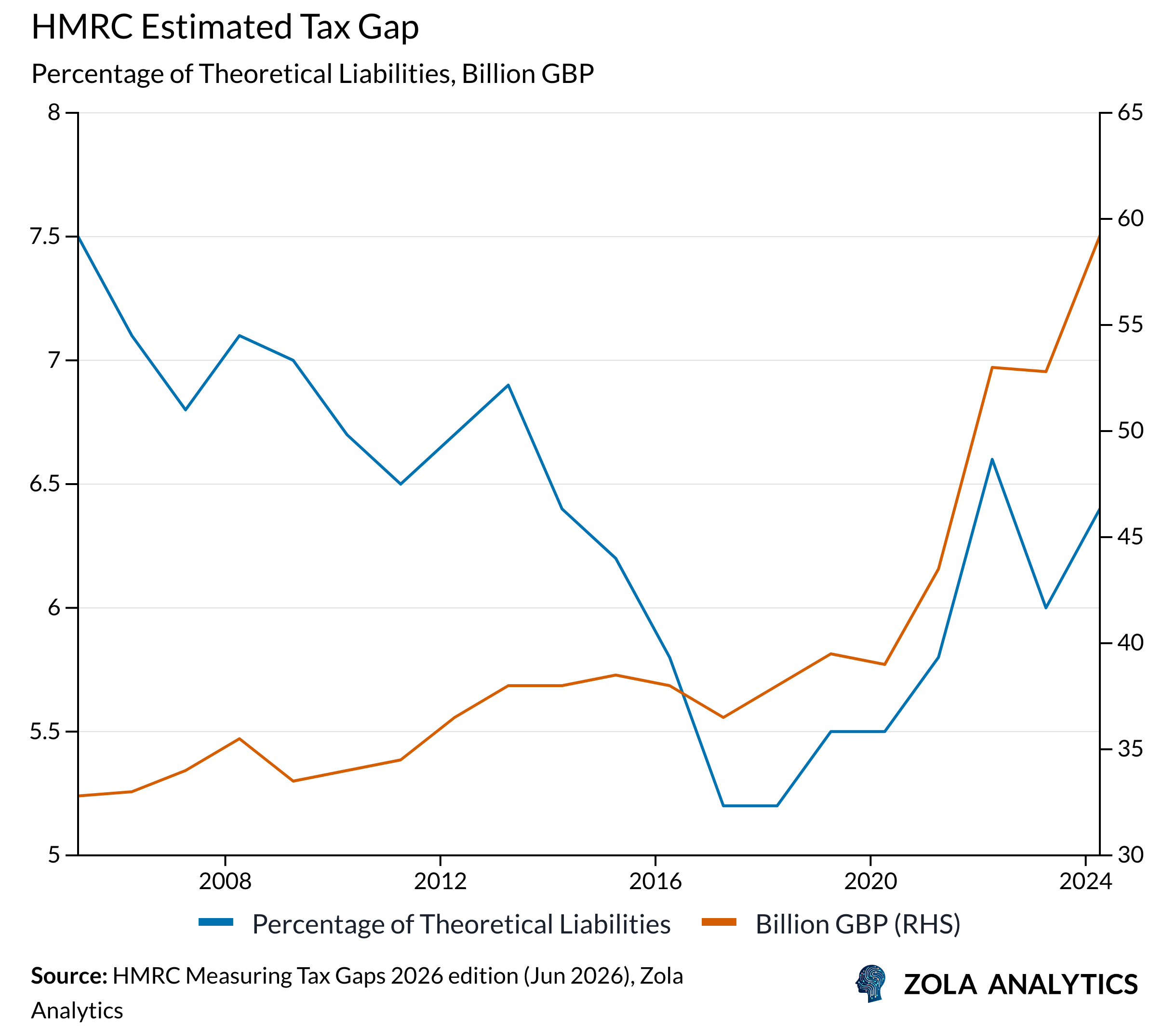

Yes. HMRC’s estimate of the tax gap has risen to a very large number. Every budget I’ve ever looked at has a line for reduced tax evasion. There’s never been a line for increased evasion, and yet I think it has gone up a lot, particularly after the announced rise in employers’ National Insurance.

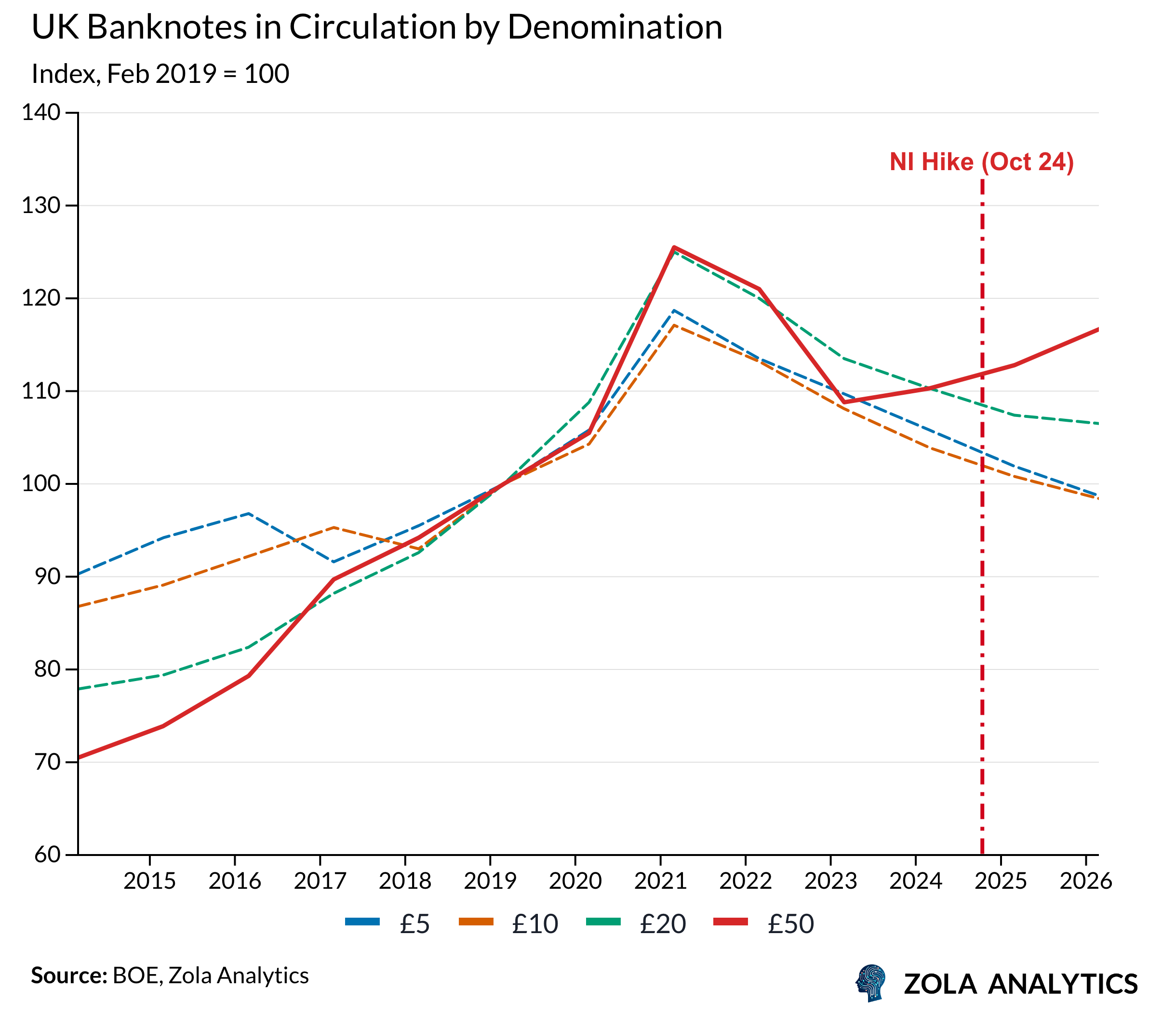

One clue is cash. The need for banknotes has been going down for obvious reasons. But that trend reversed for £50 notes after Rachel Reeves announced the huge hike in NI. Demand for smaller denomination notes continues to decline and I reckon the increase in £50 notes reflects cash-in-hand tax evasion.

But tax is basically digital now. Does that make evasion harder?

Digitisation makes it easier to catch. In 2021 they introduced Financial Information Notices, so HMRC can require your bank to hand over information, and the bank mustn’t tell you. If I withdraw £10,000 to pay a builder, HMRC can ask me to provide the builder’s details and invoices, or they may conclude I’m conspiring to evade, in which case I pay the VAT. That gets a very rapid change in behaviour.

The bigger shift is quarterly returns for much smaller businesses and the self-employed. That lets HMRC marry up whether the VAT you pay matches someone else’s VAT receipt. HMRC lost a lot of professionals over years of budget cuts, and that’s being turned round. But the direction of travel is less about highly qualified people who understand the rules, and more about systems people who can apply techniques across a much broader group.

What are some more radical options available to raise revenue?

There have been a few. They could raise the amount raised through premium bonds. There’s an interest cost, but it’s less than gilts, and the limit has been unchanged for ten years. Take it from £50,000 to £75,000, or even £100,000 over time, and those inflows reduce gilt issuance one-for-one. Because gilt yields are above the effective premium-bond yield, and the curve is positive, you gain.

More radically, we have a whole list of infrastructure funds, the British Business Bank, the Charging Infrastructure Investment Fund and so on, that take public money, sometimes alongside private money. You could let individuals invest directly, with a five- or ten-year lock-up and no interest paid out, only equity and dividends. That improves the deficit and reduces gilt supply.

The catch is that most of these projects lose money, but you are kicking the can down the road, which can be politically attractive. And instead of the ISA changes they’re planning, I’d remove the ISA allowance altogether for anyone with more than half a million already in their pot at the start of the tax year, and let them put money into this instead. The number of people with over £500,000 is quite high. Over a million it’s far lower. So you set the threshold at half a million, and it saves a fair amount.

Unpleasant Arithmetic

What about on the spending side? There the government’s menu of options seems even less palatable, particularly the rising welfare bill.

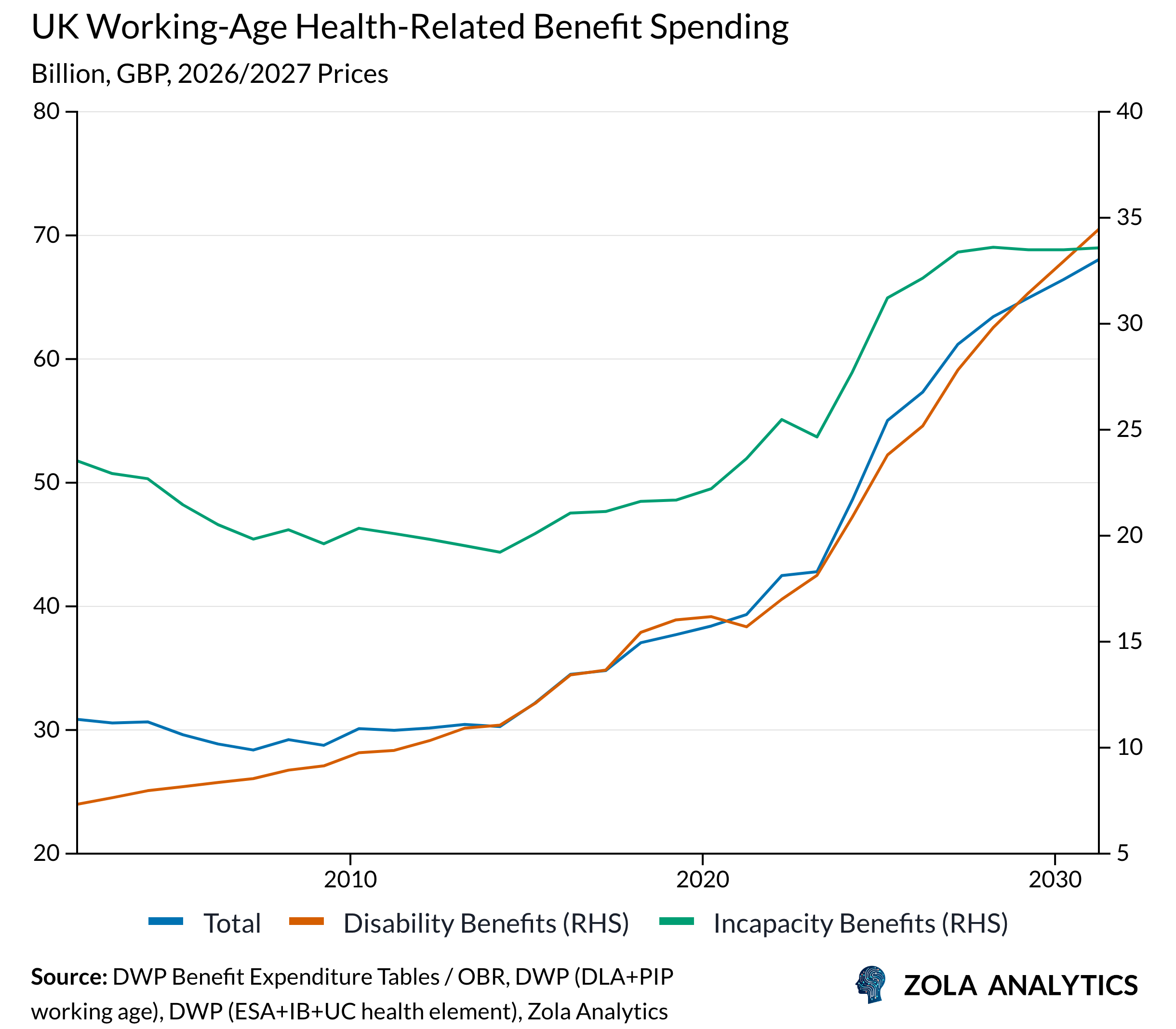

Yes, and it’s become toxic because of the failed attempts to cut it. There’s a very good IFS study projecting it to hit £100bn in real terms by 2030. That’s getting on for £4,000 per household. It’s completely unaffordable, and it’s risen enormously.

Two points. First, we used to have a big bill for out-of-work benefits, unemployment pay, and we got that right down. Other countries have had the same problem with the non-working benefits bill and brought it down too.

Second, the IFS explains why our numbers have gone up. It isn’t that more people are applying, it’s that fewer are coming off. The assessment is now done online or over the phone rather than in person. There are TikTok videos telling people exactly what answers to give, so fewer fail, and of those who pass, more and more get the top grade. You can end up with as much as £7,000 a year more for being unable to work than on jobseeker’s allowance. It has got into a complete mess.

It’s tricky, because the main conditions used to qualify, mental health, back ache, neck ache, are not observable. More to the point, they are not negatable. You can’t prove someone hasn’t got a bad back. There are rare cases where someone claims they can’t walk and then turns up dancing at a wedding on Facebook, but those are the exceptions that get exposed.

And there’s a genuine risk on the other side. If someone has their benefits stopped and then takes their own life, that’s a terrible outcome. So it’s not easy. It may even be beyond this parliament. But it has to be done, because we can’t afford this on top of everything else going the wrong way.

You said other countries have got it down. How?

The Netherlands is the example. You used to be able to be permanently signed off work from as young as 35 if two doctors said you were ill, so you found your two doctors. They made the system more rigorous.

The general lesson is that you must bring people in, in person. The parallel here is the Restart programme, piloted in the North East. People who had been out of work for two years were called in for an interview and told that if they didn’t attend, they’d be called again or lose their benefits. About 25% simply didn’t turn up. I’d expect something along those lines as a pilot.

The story is that Labour spends more, taxes more and borrows more and that will be bad for gilts. Is that how you see it?

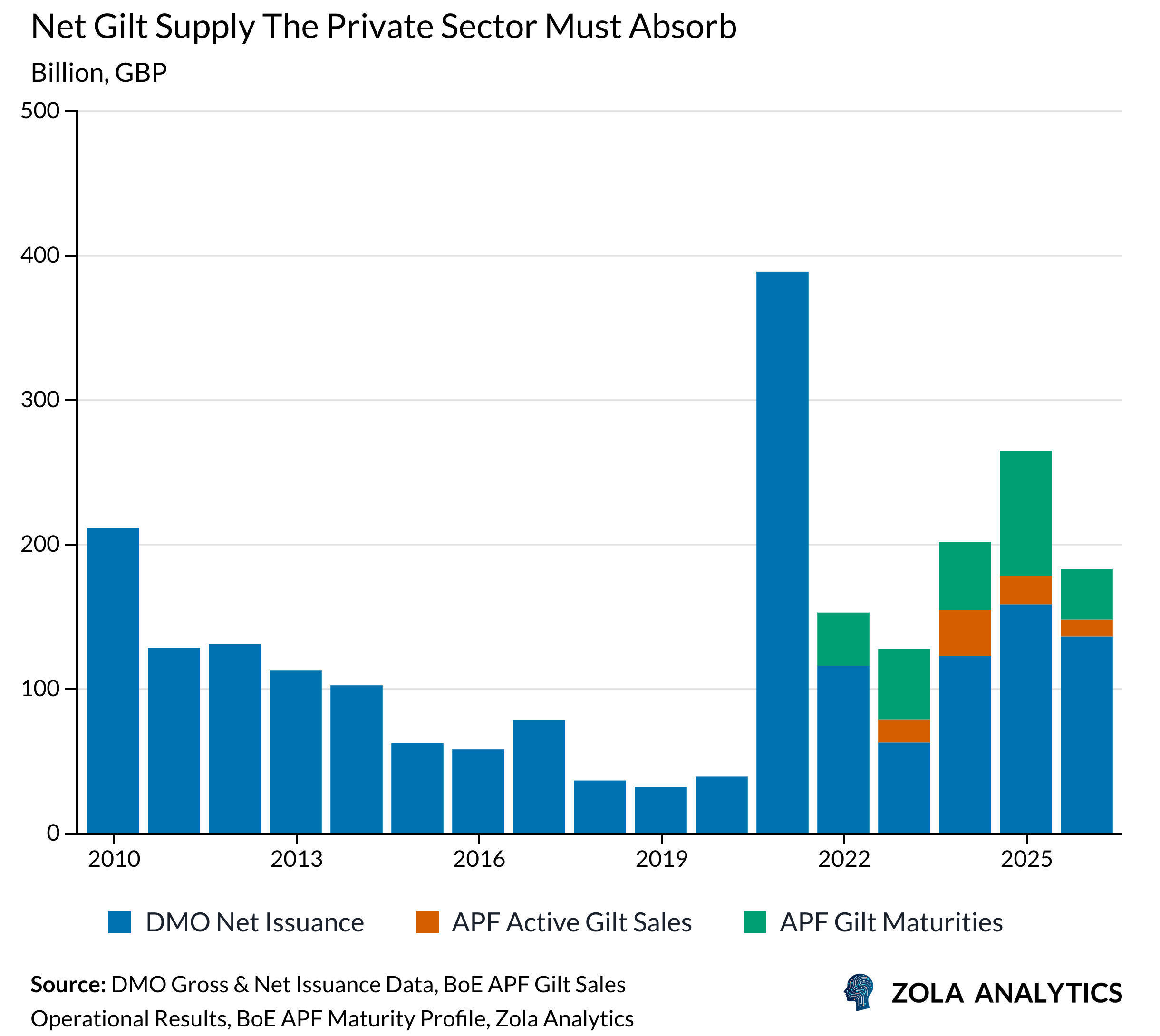

Not necessarily. What the gilt market cares about is the supply of gilts, which is linked to the budget deficit but not the same thing. Right now, the government is borrowing heavily to fund the deficit while the Bank of England is simultaneously selling off its gilt stock, which is completely crazy.

Under pressure from people like my former colleague Chris Mahon and others, they’ve already reduced the pace. There are two ways to shrink the stock: let gilts mature naturally, or actively sell them. They should do no active sales at all, just let them run off, which is what other central banks are doing.

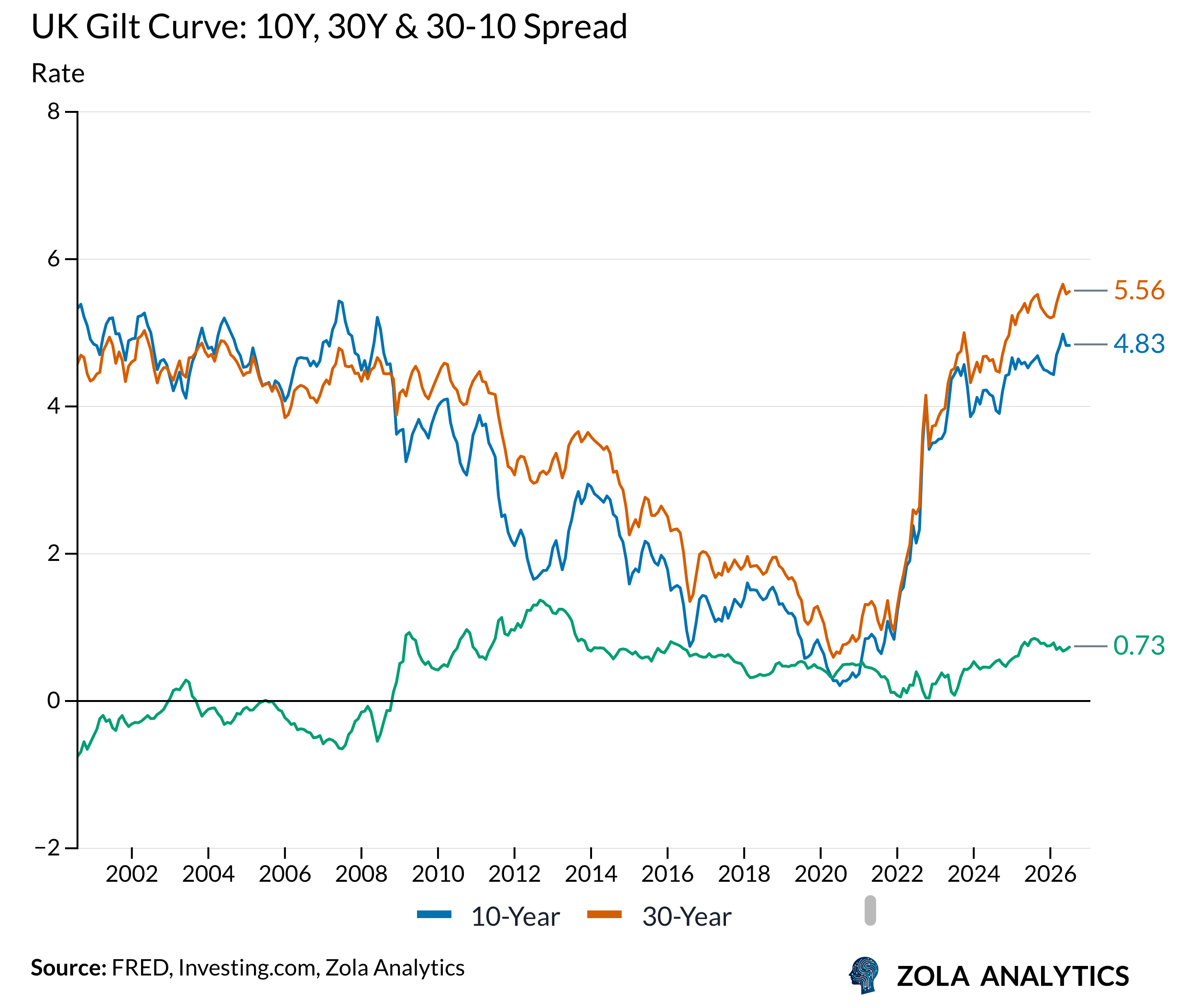

The other piece is the curve. The 10s30s spread is quite steep now. When I was in the Treasury, it was inverted, with 30-year yields below 10-year yields. Today you pay a lot more to borrow at the long end.

So if they stop issuing and selling long-dated gilts, the loss on the Bank’s asset purchase facility, which is haemorrhaging money, comes down because the prices aren’t so negative. You get a reduction in the Treasury’s funding of the Bank and a reduction in debt-interest costs, and the gilt market rallies.

They’ve already cut the programme from £100bn to £70bn a year. If they then let the rest run off, you’re talking about something over £50bn of reduced gilt sales over the next three years, depending how you do the numbers.

Is this something you think they will do, or should do?

Both. From the “should” point of view, it’s a no-brainer. The Bank has been kicking and squealing against it. They first said active sales added a few basis points to gilt yields; now they say 25. They cut the pace in a year with heavy redemptions, so the active sales were small anyway and didn’t much matter. It’s from September onwards that it starts to matter. So I think they will do it.

You could see a big rally in gilts, but it’s limited, because most of the movement in gilts is determined by their relationship with foreign yields, especially the US. If US yields don’t rally, all we do is get less of a sell-off.

And… Cut?

So that begs the question: what’s the next move in US rates?

I don’t see much pressure on the administration to cut the deficit. But I do think the Fed will cut rates not immediately, but later in the year.

That’s a contrarian view.

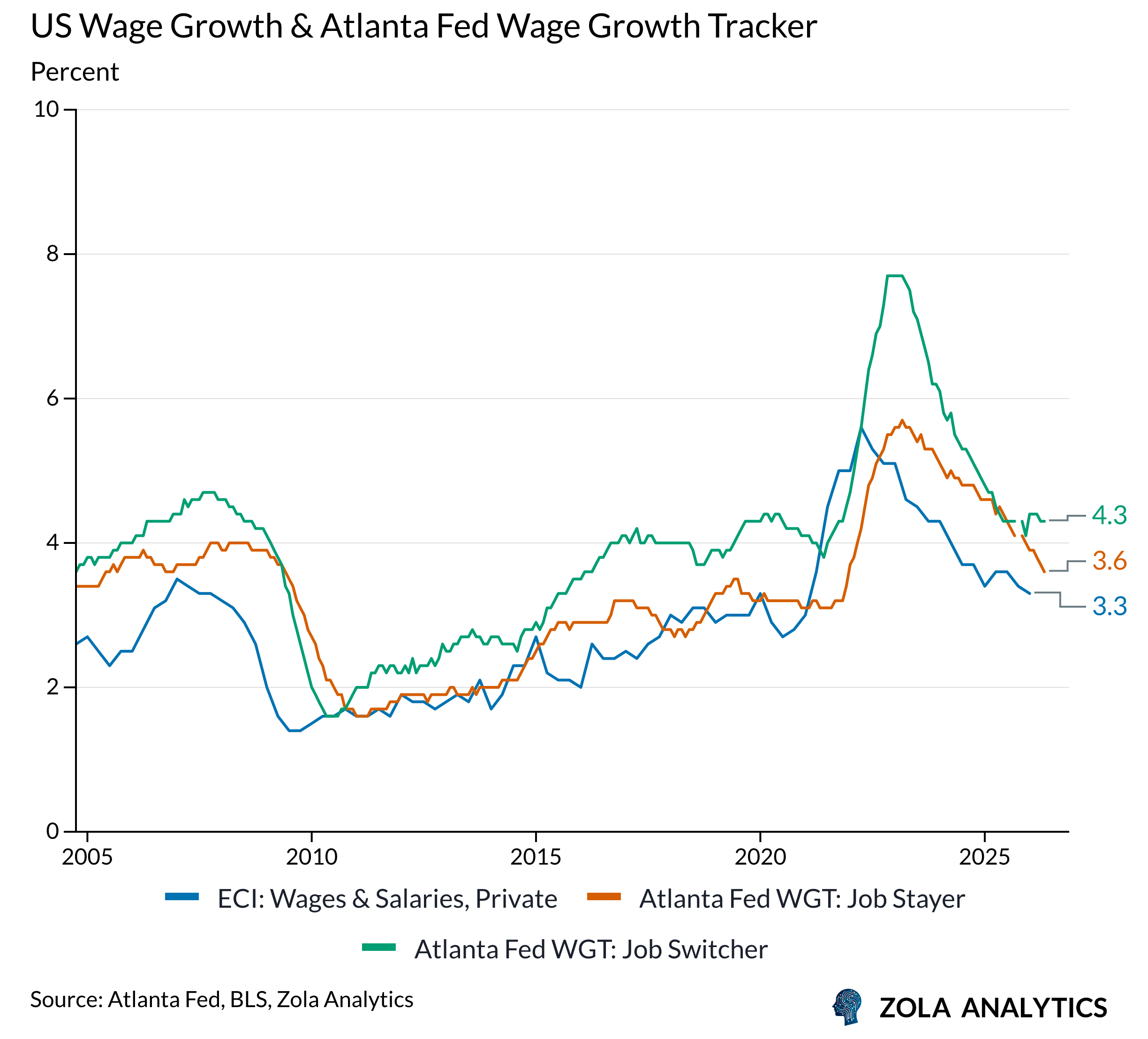

It is. My view is that inflation simply isn’t a problem in the US. The biggest driver of inflation is wages, and wage inflation has been falling significantly. The best monthly measure isn’t the average hourly earnings number everyone quotes with payrolls — it’s the Atlanta Fed’s wage tracker, which compares like for like. The latest reading was 3.5%, down from 4.3% a year ago and 5.2% two years ago. And because of how it’s measured, it tends to overstate the gold-standard Employment Cost Index by about half a point. So at 3.5% the underlying pressure is below 3%, consistent with the 2% target. When the next ECI reading comes it’s likely to show a further significant decline.

There’s a second, important force: margins. We’ve had amazing US earnings growth, and it surprised me, especially in the first three or four months of the year. Normally, consensus bottom-up S&P earnings are biased up by 5-8%, because analysts are optimistic about their own sector, so through an average year the number comes down. This year it went up, largely on margin expansion: firms raising prices by more than costs, which you’d think is inflationary.

But once you get away from the Mag Seven, it’s different. Strip out Amazon and the Mag Six employ fewer than half a million people between them. The companies that actually employ people are smaller, and their margins aren’t expanding. The smallest have low, barely stable margins. When you can’t raise prices and can’t absorb more cost, the one big controllable is wages. So there’s further disinflation coming from the margin squeeze on smaller firms.

People say inflation surged after COVID, so how can the Fed ease? But back then rates were far too low and we’d had enormous money-printing, handing people money and telling them to stay home and not spend it. We don’t have that overhang now. The US consumer has already cut the savings ratio and hasn’t much further to go. So inflation is benign, and if the economy wobbles, and it would take more than one payroll number, since the one we had was revised away, they’ll cut, because inflation isn’t in the way. Modest cuts, because they won’t want to go too far, in the second half of the year.

Alan Greenspan died recently. You traded under him. How does reading the Fed then compare with reading it now?

Greenspan was a fantastic economist. He anticipated the impact of the dot-com shift in a big way, and US productivity did improve in that period. Admittedly, a lot of it was productivity in producing computers, but there were other benefits that took a long time to come through.

He talked about irrational exuberance too. He thought the market was going too high, and it went on and on. The real dent in his reputation is the Greenspan put: we all assumed the Fed would cut when equities fell. We still think that, but the sensitivity is less now. That confidence in the market ultimately encouraged too much leverage and fed into the global financial crisis. It’s wrong to blame it all on him, but it was certainly lubricant for the process.

As for reading a central bank, you read their words and their speeches. It really matters, because they put enormous effort into writing them, and I’ve been involved in that myself. But you also have to think about what they’re really worried about. It’s a bit of psychology.

For a long time, I had the privilege of assuming they’d been to the same universities, read the same articles and held the same views as me. I’m now older than the average central banker, so I’d defer to someone who went to MIT a few years after I was in the US.

You mention Greenspan’s management of the late 1990s supply shock. How does the impact of AI factor into your expectations of inflation now?

Views differ by individual, and a given individual will change their mind over time, because we just don’t know. The first and most obvious point is that the investment boom itself is pushing prices up: electricity prices in the US, and the prices of the commodities and equipment everyone is scrambling for, on a winner-takes-all assumption. So there is upward pressure. On the other hand, if AI displaces demand for labour, that reduces wage pressure. Competition may also pull prices down as firms lose out to rivals.

The “AI fairy”, as people called it, may do that. Warsh was talking about this when he was being considered for Fed chair, saying his previously hawkish views had changed because of AI. But if I were on the Fed, I’d want hard evidence before reacting to it. The investment is relatively low in labour intensity, and it doesn’t matter much to domestic producers if the kit is bought from abroad. So on that score, it is less important. The powerful channel is electricity prices, in the same way that any investment boom hits capacity constraints in the goods market.

Interestingly, even the hyperscalers are now hunting for cheaper alternatives, and more energy-efficient chips are the new fashion, so there are responses. I can’t tell you whether the investment bubble bursts or runs on, but it’s a less powerful inflationary force than if it came through a broad rise in employment.

That sounds like AI may be less inflationary than people fear, but the investment boom itself still looks extraordinary. Does that make you worry about a bubble?

Yes, the equity bubble is the thing I’d flag. I’ve talked to two of the best equity strategists I know, and putting them together I’d say we’re seeing many of the ingredients of a bubble, but I don’t think it bursts yet.

I don’t want to over-quote Chuck Prince going into the financial crisis, but as long as the music’s playing it may be worth continuing to dance. Personally, though, I’ve turned cautious on equities, particularly on some of these IPOs, which look almost engineered to produce a pop.