Published July 4th 2025

From King Dollar to Weaker Buck

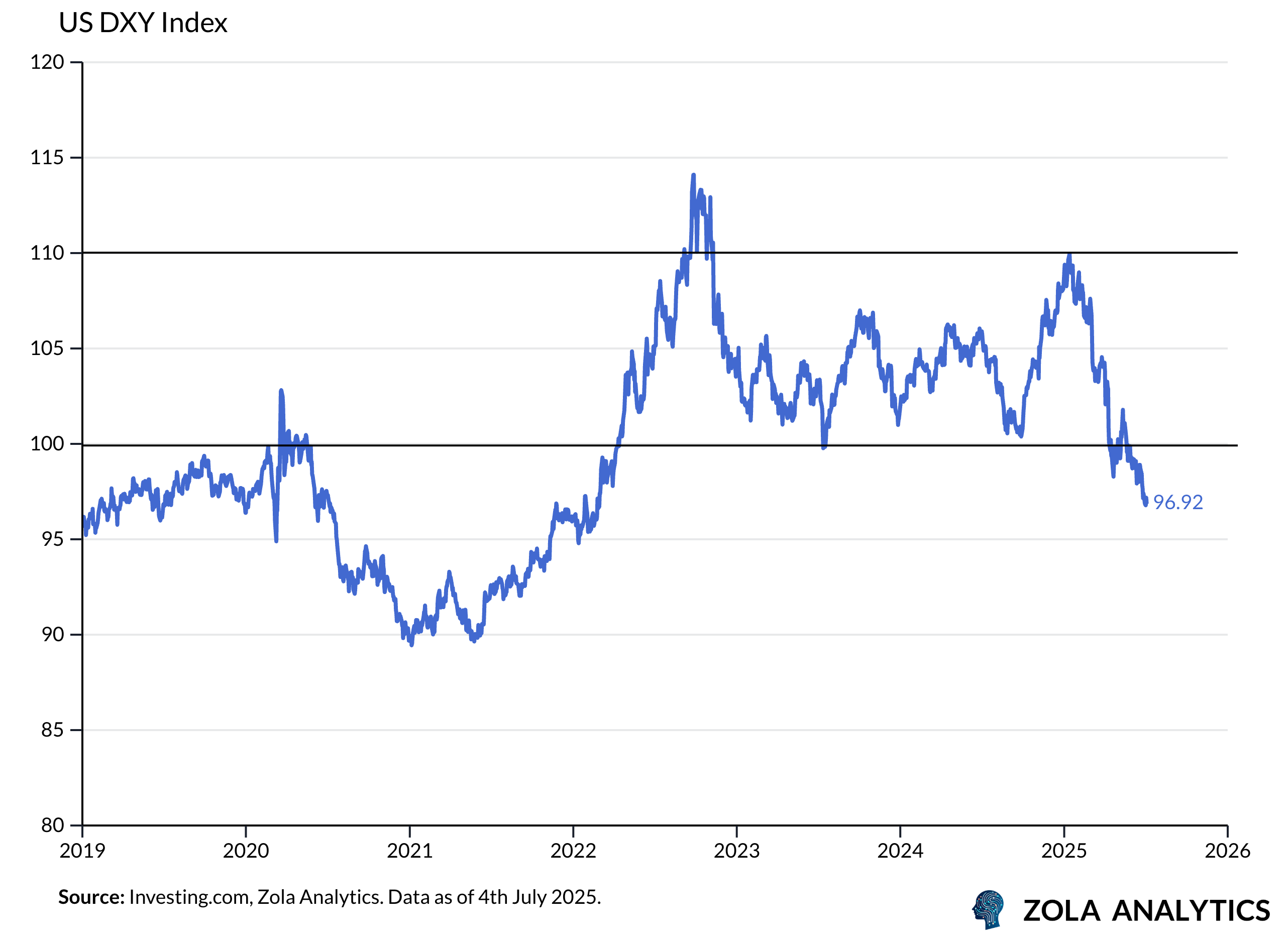

This Fourth of July, Americans toast liberty — but the weakening dollar suggests the cost of that freedom may be rising. The US dollar has declined sharply year-to-date, breaching levels unseen since the 1980s. The question now is whether this move reflects a temporary overshoot or signals the start of a broader structural trend. A reassessment of cyclical and structural forces suggests that a bearish stance on the dollar remains warranted through the second half of 2025.

Growth Moderation and the End of US Exceptionalism

The clearest shift is the marked moderation in US growth relative to the rest of the world. Recent data show softening domestic demand, a cooling labour market, and decelerating payrolls. Crucially, US economic surprises have turned increasingly negative, while surprises in Europe and parts of Asia have been positive. This divergence indicates that the US outperformance — a key pillar of dollar strength in recent years — is fading.

Contrarian Take: Some argue that global growth outside the US could stumble once tariff-related inventory building unwinds, reigniting dollar strength. Yet better-than-expected fiscal support and resilient domestic demand in Europe and parts of emerging markets suggest these regions could withstand headwinds, reducing the likelihood of a swift return to US growth leadership.

Quality of Carry Deteriorates

While the dollar continues to offer high nominal yields relative to most developed currencies, the quality of that carry has deteriorated. Rising term premiums — the extra compensation investors demand to hold long-dated US debt — and expectations of Fed rate cuts as growth slows have historically been toxic for the dollar. Even when carry was elevated in past cycles, the dollar weakened meaningfully as growth momentum softened and investors priced in declining real returns.

Contrarian Take: Elevated carry can cushion downside, but history shows it rarely sustains dollar strength when fundamentals erode and markets start pricing in Fed easing.

FX Hedge Rebalancing Pressures

A significant but often overlooked driver of dollar weakness lies in FX hedge rebalancing flows. Many large global asset owners remain structurally under-hedged on substantial US equity holdings. As correlations between US equities and the dollar turn more positive — meaning equity rallies increasingly coincide with dollar gains — investors are incentivised to raise hedge ratios, mechanically selling USD and exerting systematic downward pressure on the currency.

Systematic Hedging Flows Amplify Dollar Moves

When pension funds, insurers, or sovereign wealth funds raise target hedge ratios — for example, from 30% to 50% hedged on USD assets — they must sell large volumes of USD regardless of valuations. These programmatic flows can amplify dollar volatility and drive overshoots disconnected from fundamentals.

Recent analysis from the Bank for International Settlements (BIS) shows confirms that ex post FX hedging activity by Asian institutional investors played a major role in the dollar’s sharp slide inApril–May 2025, with the largest declines occurring during Asian trading hours. This provides concrete evidence that rising hedge ratios can significantly amplify dollar weakness, especially given the enormous foreign holdings in US assets (over USD 17 trillion in equities and USD 13 trillion in bonds).

Importantly, recent data indicate that the dollar’s drop was not driven by foreign selling of US assets outright. Treasury International Capital (TIC) data show continued foreign buying of US equities and credit during the first half of 2025. Instead, the weakness reflected a sharp increase in hedging activity: after decades of minimal hedging, foreign investors began hedging their USD exposures more aggressively, adding systematic selling pressure.

Contrarian Take: Some argue these flows move slowly or are already priced in. However, the BIS analysis indicates the rebalancing process is still incomplete, with pension funds and insurers in Europe, Canada, and Asia remaining below historical hedge norms — leaving ample room for continued USD selling.

Structural Shifts Amplify Vulnerability

The dollar’s recent slide is not merely a technical correction. Several structural factors suggest a regime change:

Fiscal risks remain high, with debt levels climbing and policy uncertainty elevated.

Tariffs have imposed both inflationary and growth-dampening effects on the US economy, shifting real yield differentials in favor of other regions.

Global portfolio diversification continues, with investors adding non-US assets, reducing the automatic recycling of capital into dollar-denominated securities.

This trend of de-dollarisation is also propelling structural flows into alternative reserve assets such as gold. As discussed in our recent analysis of the emerging gold supercycle, rising fiscal instability and shifting geopolitical dynamics are reinforcing long-term vulnerabilities in the dollar.

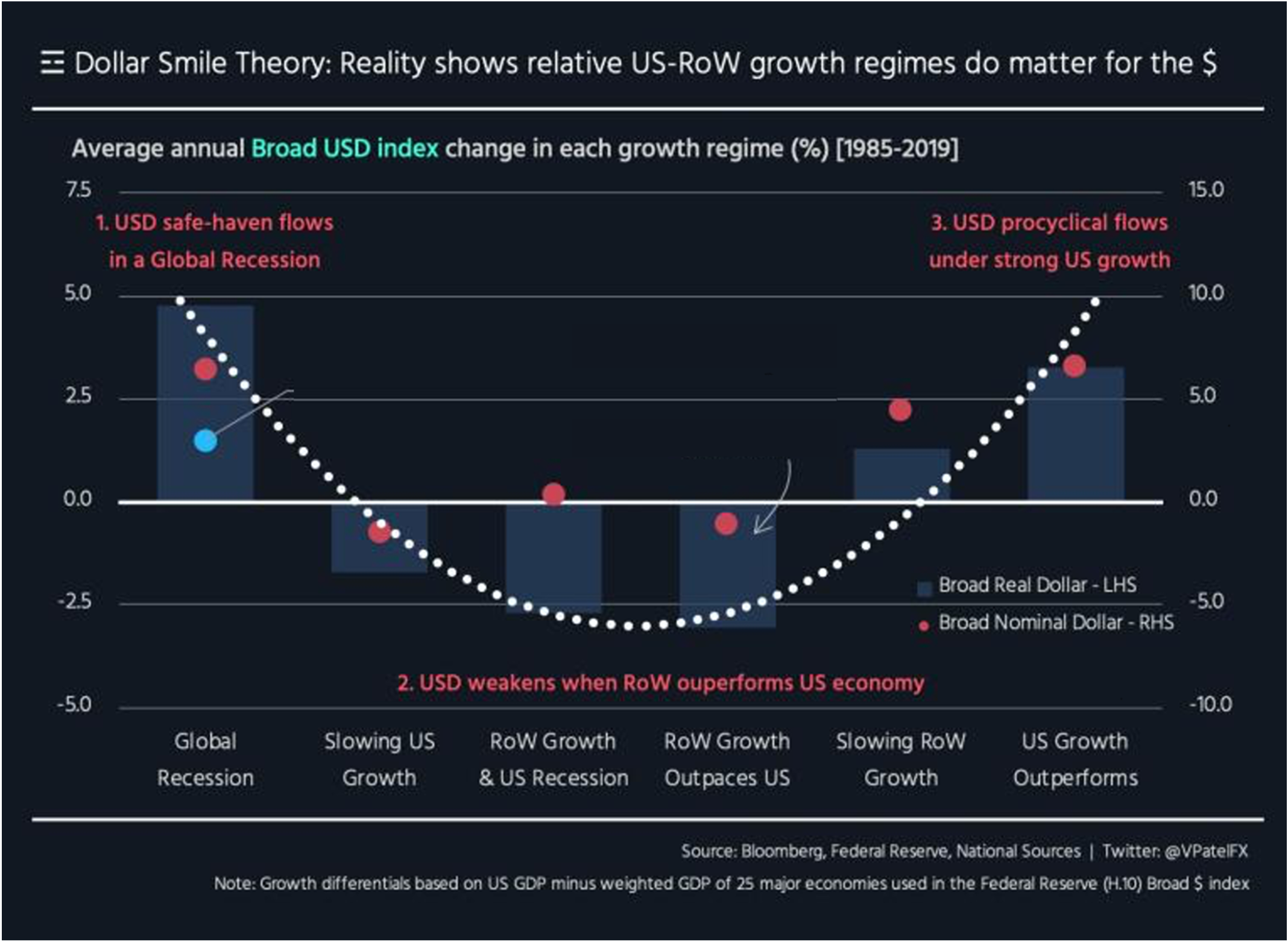

Limits of the Dollar Smile

The dollar smile framework suggests the dollar strengthens either when US growth outperforms sharply or during global crises that spur safe-haven demand — the two “ends” of the smile. However, in periods of middling global growth and slowing US momentum — the “middle” of the smile — the dollar tends to weaken.

In today’s environment, this framework is looking increasingly more unreliable. Erratic policy moves, such as abrupt tariff escalations and unconventional interventions like handwritten demands for rate cuts, have undermined perceptions of US institutional stability. These episodes have eroded global confidence in America’s economic governance, prompting foreign investors to hedge or reduce their dollar exposures even as US equities rally. Rather than benefiting from safe-haven flows, the dollar is instead weighed down by fears that capricious decision-making will erode long-term economic prospects. Without a decisive global shock to reignite haven demand or a clear return to consistent policymaking, the dollar is likely to remain under sustained pressure.

Investment Implications

The confluence of weakening macro fundamentals, deteriorating real yields, and structural shifts in global capital flows reinforces a bearish stance on the dollar. While episodic rebounds may occur—driven by data surprises or geopolitical tensions—these are likely to prove transitory against the backdrop of persistent policy uncertainty and eroding US exceptionalism. Positioning should continue to favour dollar downside, particularly versus currencies backed by robust external balances, credible fiscal frameworks, and cyclical growth tailwinds. Investors should also consider hedging USD exposure where practical, as the greenback increasingly serves as the release valve for global concerns over US policy volatility.

Disclaimer: Zola Analytics provides this material for informational and entertainment purposes only. It does not constitute investment advice.