Published September 12th 2025 7 minute read

Fault Lines

The title of ‘sick man of Europe’ has had multiple claimants over the years. Originally used by Tsar Nicholas I to refer to the crumbling Ottoman empire, by the 1970s the label belonged to the UK. In the late 1990s, Germany earned the moniker for the first time. But for most of the first quarter of the 21st century, it seemed to many that the German economy was the most dynamic in Europe. Now, only five years after John Kampfner’s panegyric Why the Germans Do it Better: Notes from a Grown-Up Country became a Sunday Times bestseller, many are asking whether Germany has become the ‘sick man’ once more.

Germany is struggling. It is currently enduring its longest slump since reunification. GDP fell -0.3% in 2023 and -0.2% in 2024. It remains to be seen whether 2025 will become the third successive year of decline, or just mere stagnation. In this edition of Zola Chartbook, we examine how this slump arose, the structural vulnerabilities it has exposed, and whether Germany’s historic fiscal shift can deliver the renewal it promises.

A Generation of Neglect

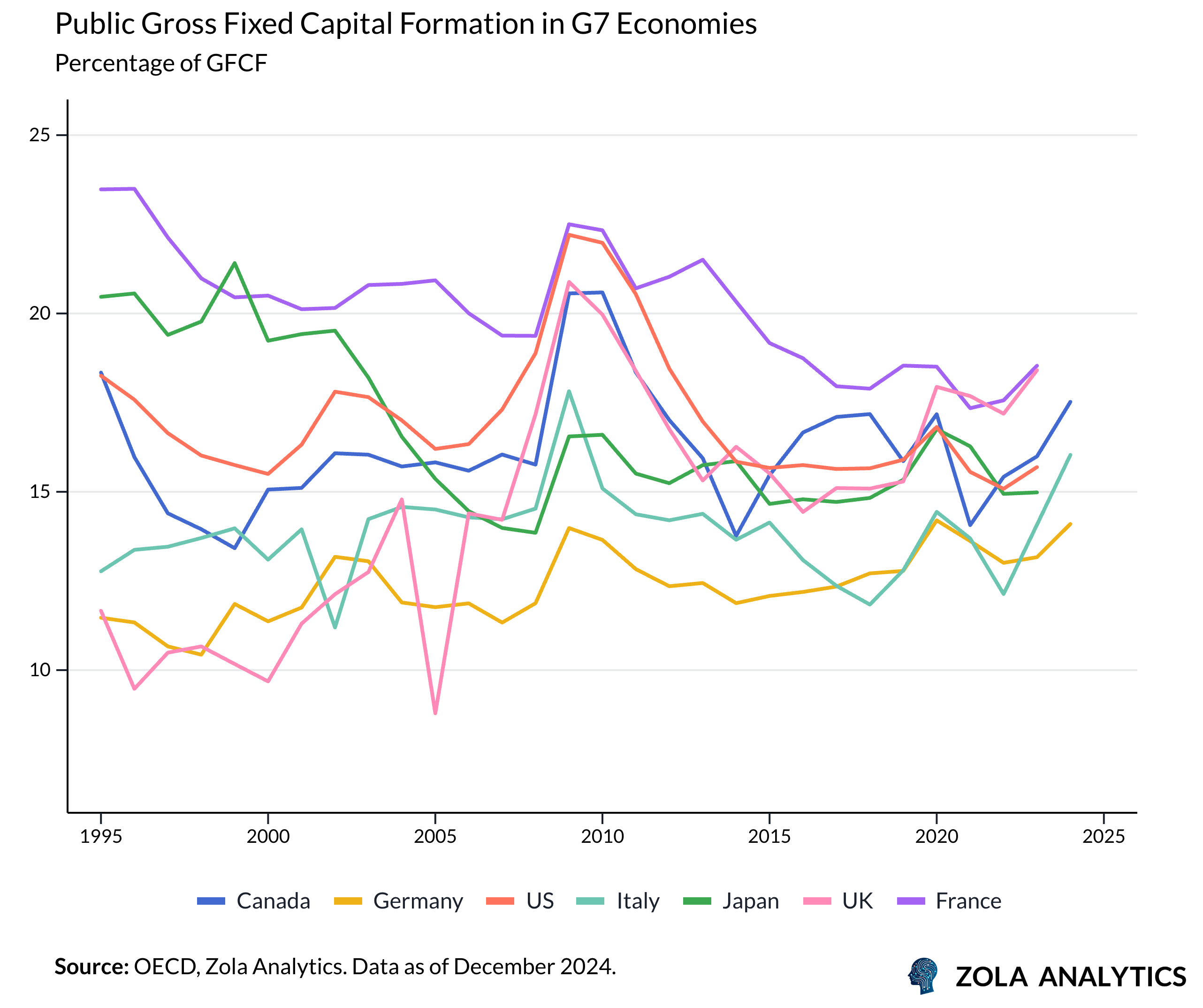

Germany’s deepest policy error was chronic underinvestment. Since the late 1990s, net public investment has hovered near zero, with depreciation outpacing new capital formation. By the 2000s, Germany was already falling behind G7 peers.

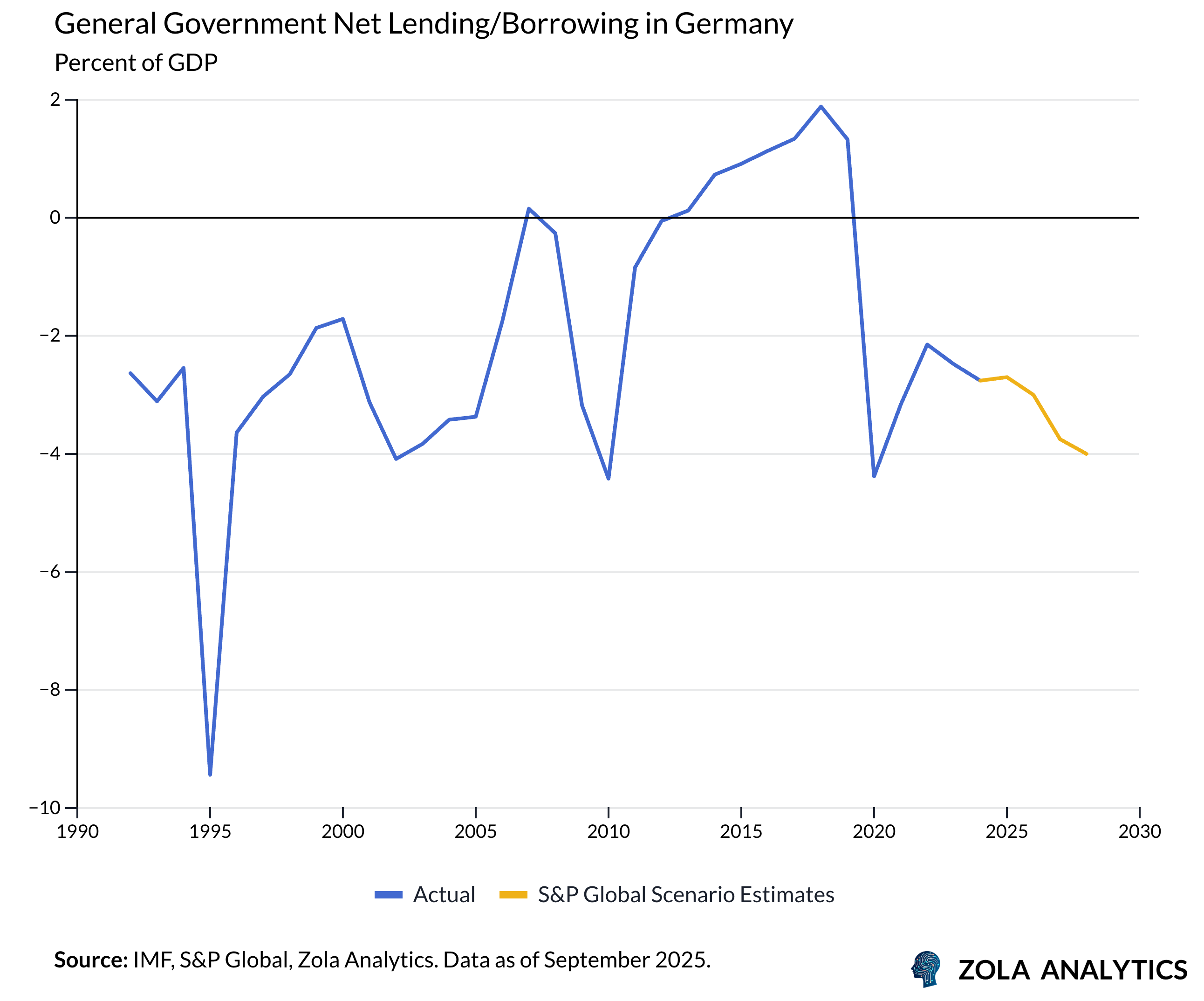

The government’s rationale was rooted in history. The vast fiscal transfers required for reunification in the 1990s left a legacy of debt aversion. To many policymakers, the profligacy of southern Eurozone partners after 1999 reinforced the sense that credibility could only be restored through restraint. This ethos culminated in the Schuldenbremse (debt brake), enshrined in the Basic Law in 2009 and fully binding from 2016. Balanced budgets - the Schwarze Null - became dogma.

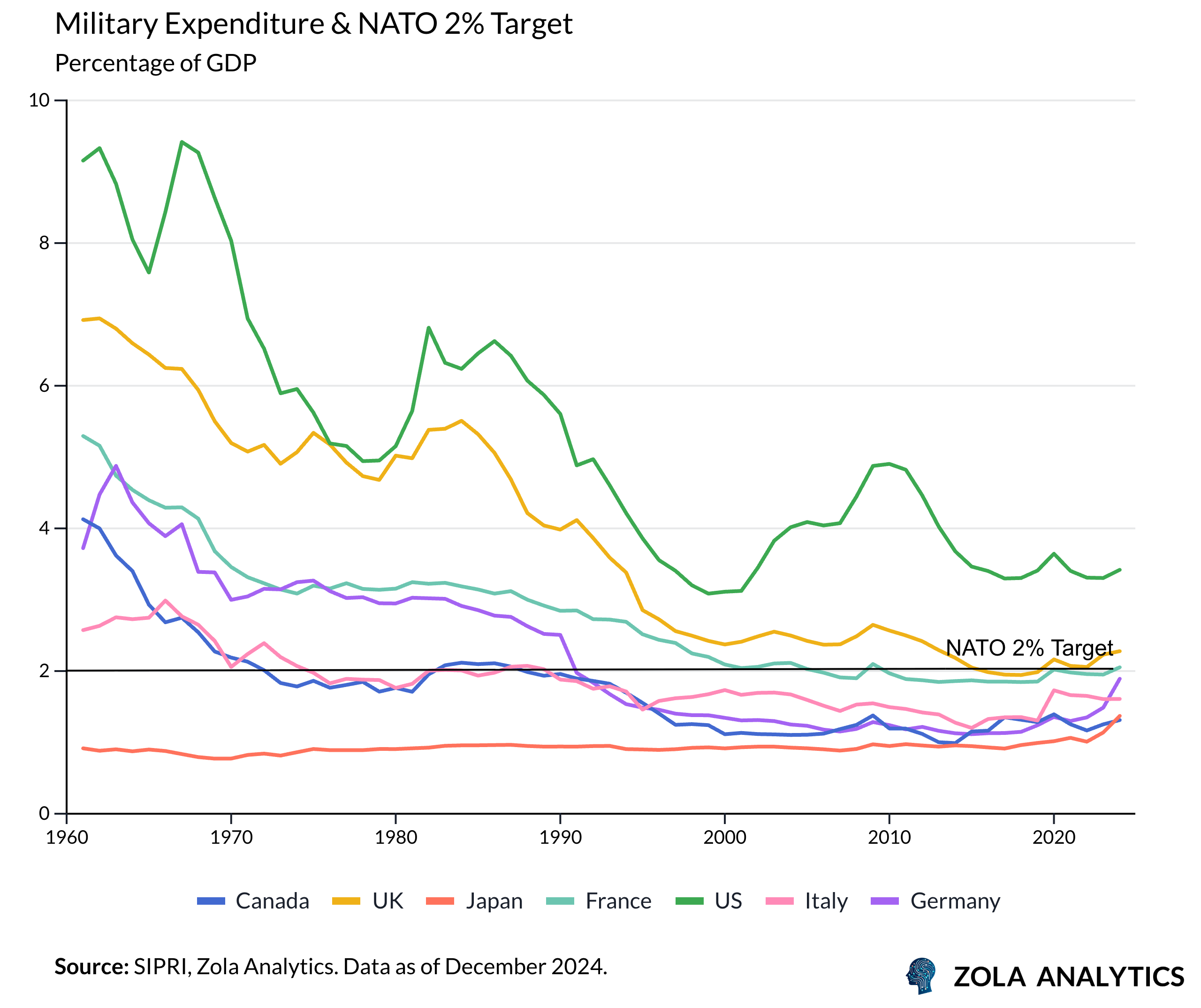

The consequences of this neglect are structural - infrastructure has deteriorated, digital networks have lagged those of peers, and electricity grids failed to expand in line with the energy transition. Defence spending undershot NATO’s 2% benchmark for decades, leaving capacity gaps just as geopolitical risks mounted.

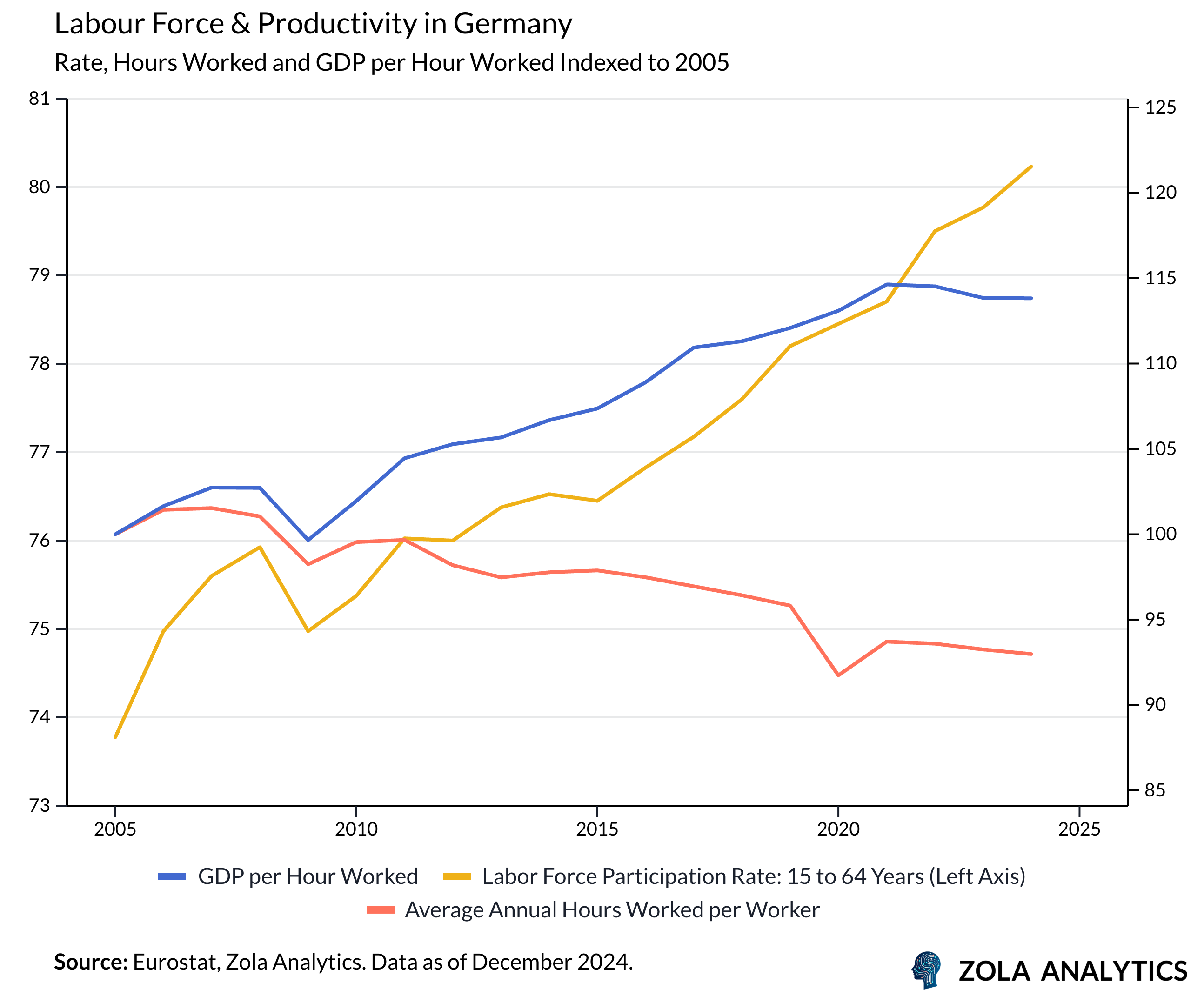

At the same time, the 2003-05 Hartz labour market reforms reshaped the German model. Designed to curb unemployment that had surged after reunification, they succeeded in boosting participation and reducing joblessness. But the reforms also entrenched low-wage, part-time, and insecure work. Household income growth was subdued, consumption remained weak, and the savings rate rose.

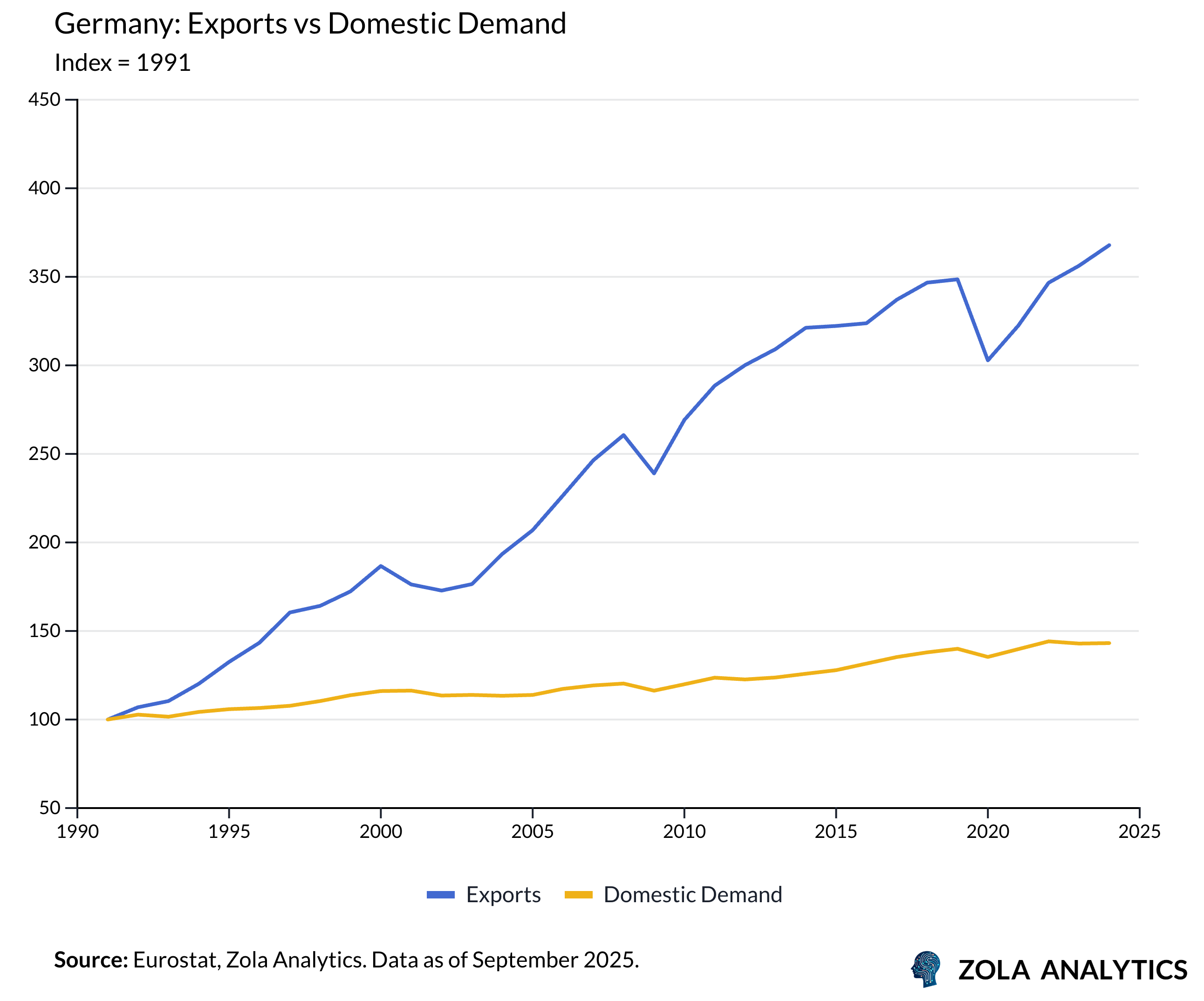

With high savings rates in both private and public sectors, Germany’s growth model hinged on the external sector. When energy was cheap and global trade networks flourished, this model was successful.

But reliance on external demand carries hidden costs. A model built on wage restraint and foreign surpluses can only thrive while others were willing to absorb German exports. As that willingness wanes the foundations of the old model are eroding. High energy costs, ageing infrastructure, and intensifying competition from Chinese steel, autos, and batteries are squeezing margins at home and abroad.

Fragile Foundations

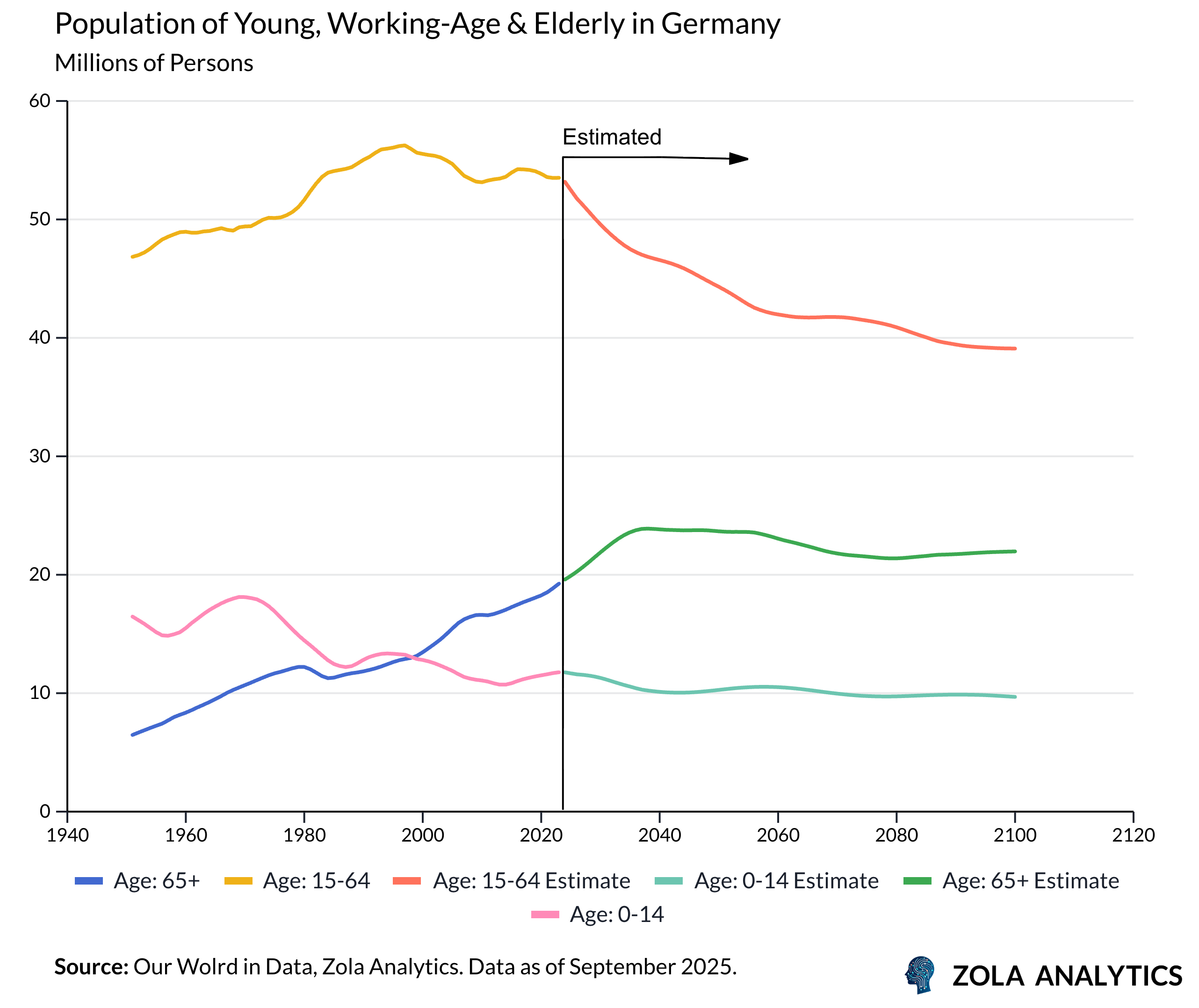

The weakness of domestic demand was mirrored by a slow erosion of supply capacity. A shrinking workforce, high part-time incidence, and falling average hours worked have reduced labour input. Participation rose after the Hartz reforms, but even record participation cannot offset the steady decline in hours per worker - among the lowest in the OECD. Demographics sharpen the drag: by 2030, the labour force will shrink by the size of Berlin.

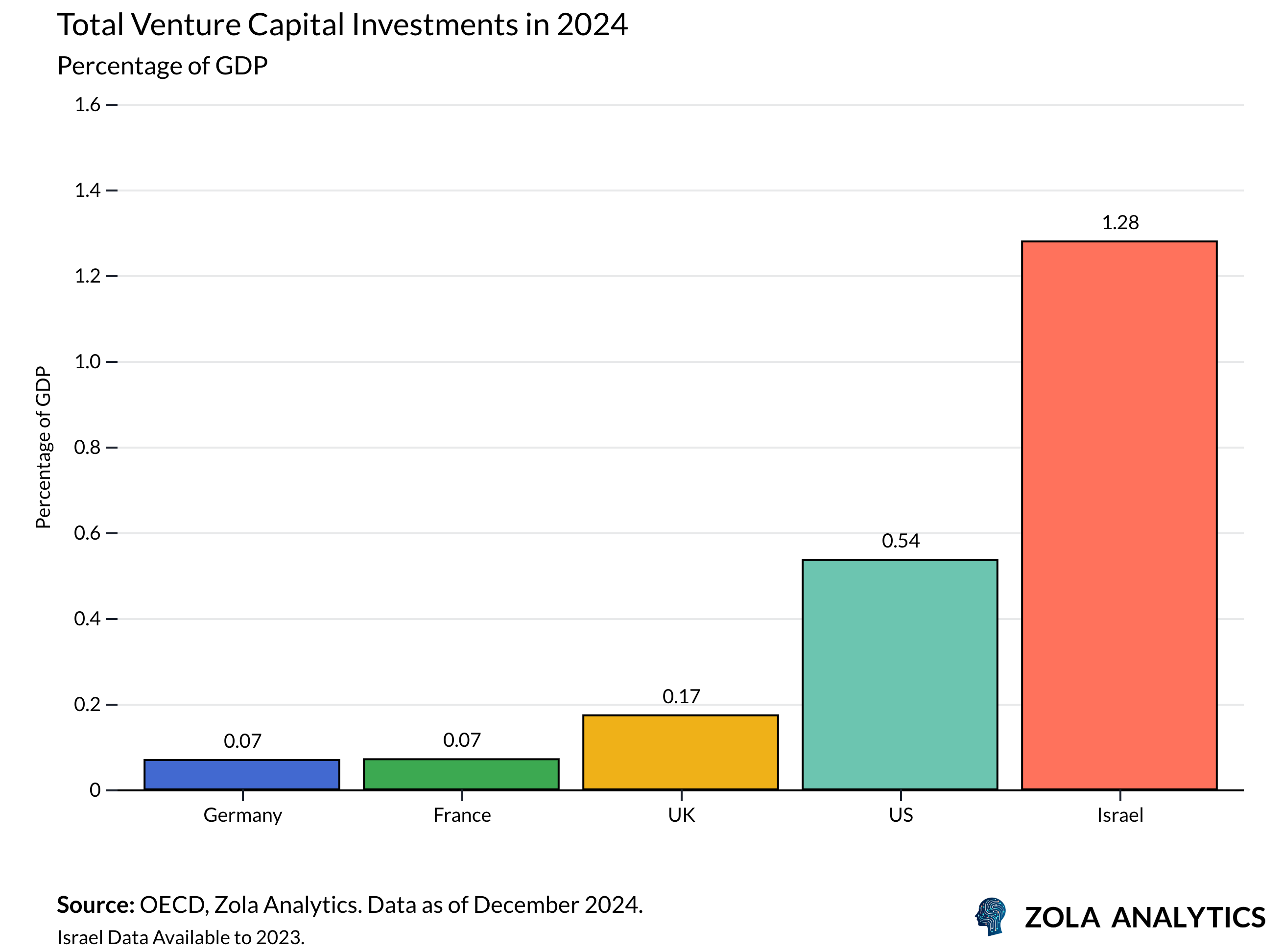

Nor has innovation provided relief: despite high research spending, commercialisation is weak and venture funding shallow. Meanwhile, the Mittelstand continues to depend heavily on foreign markets and investors. Compared with the United States, where deep capital markets accelerate adoption, Germany’s innovation ecosystem is thin and fragmented.

A Fiscal Earthquake

Faced with a brittle supply side, fading export demand, and ratcheting geopolitical pressure, Berlin has finally acted decisively. Lawmakers amended the Basic Law, exempted defence outlays above 1% of GDP, and created a EUR 500bn Special Fund for Infrastructure and Climate Neutrality. Net borrowing will rise to EUR 143bn in 2025 and EUR 173bn in 2026, pushing the deficit above 3% of GDP. Public investment is set to climb by more than 50%.

Markets have afforded Berlin unusual leeway. Debt ratios remain low by advanced-economy standards, and Bunds still command safe-haven status. Stagnation, not borrowing, is seen as the greater risk. This credibility buys time, but it is finite.

Structural Strains

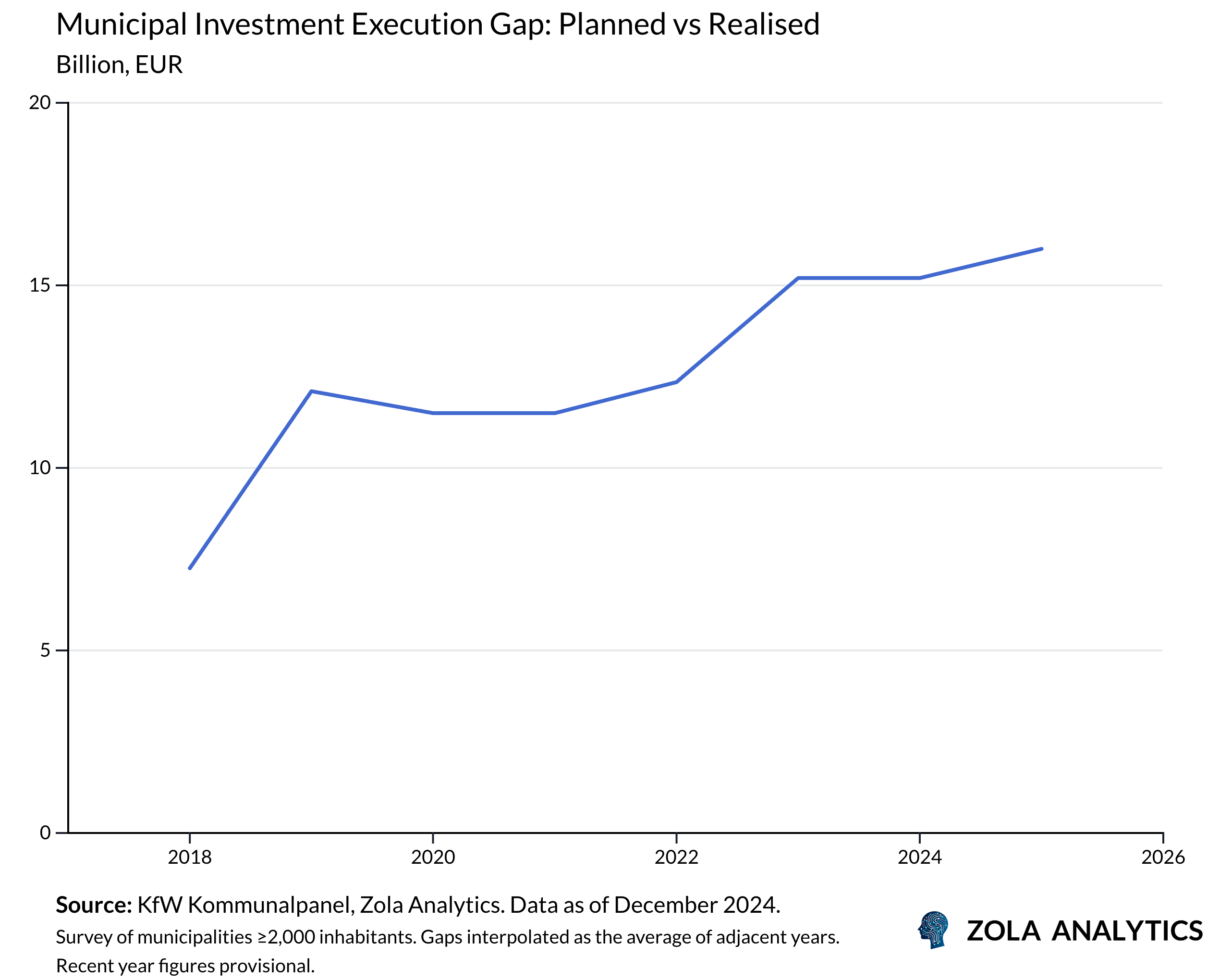

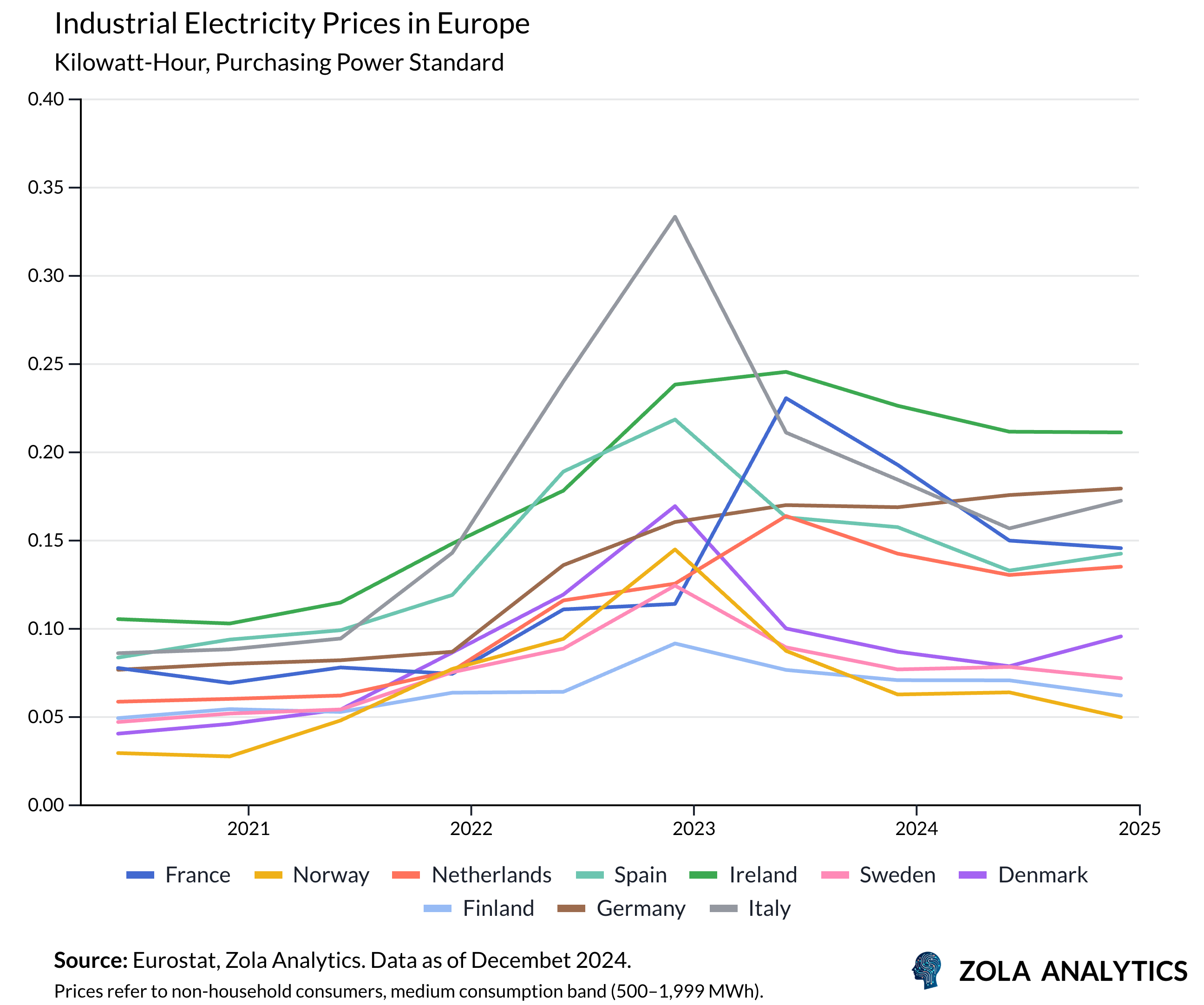

Yet money alone cannot resolve Germany’s bottlenecks. Energy costs remain among the highest in Europe, with grid delays keeping industrial electricity prices nearly double those in the US. Infrastructure projects face long planning cycles, overstretched municipalities, and permitting backlogs that slow deployment.

Demographics have added further pressure. By 2030, the workforce will shrink by the size of Berlin. Dependency ratios are climbing, shortages are spreading across skilled trades and high-tech industries, and productivity growth remains too weak to compensate.

Global shifts are making the adjustment even more difficult. Chinese overcapacity in steel, autos, and batteries squeezes German producers at home and abroad. Deglobalisation raises barriers in key markets, while US protectionism weighs on machinery and car exports. Public money can repair roads, extend grids, and stimulate demand, but it cannot neutralise these headwinds overnight.

Renewal or Drift?

When you announce a record fiscal package, interest rates rise but your currency strengthens, you are in a position most countries would envy. Yet that very reaction is also a warning: it suggests you could have afforded to spend more, sooner. Germany has not been punished for borrowing, but it has suffered from its prudence.

Berlin’s fiscal turn is an opportunity, but the challenge it faces is stark. If investment raises productivity, modernises infrastructure, and strengthens labour supply, the economy can rebuild its domestic core and shed the “sick man” label. If bottlenecks persist and global headwinds intensify, fiscal power will cushion stagnation rather than reverse it.

Sign up to receive the Zola Global Macro Chartbook every week: https://www.zolaanalytics.com/insights?signUp

Disclaimer: Zola Analytics provides this material for informational and entertainment purposes only. It does not constitute investment advice.